|

市場調查報告書

商品編碼

1665285

空間物流市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Space Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

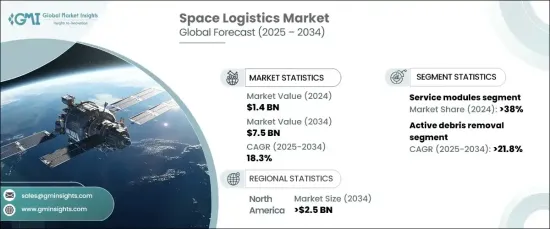

2024 年全球太空物流市場價值為 14 億美元,將經歷強勁成長,預計 2025 年至 2034 年的年複合成長率(CAGR) 為 18.3%。 這一成長主要受到衛星部署、在軌服務和太空探索計劃日益成長的需求的推動。可重複使用發射技術的創新,加上用於通訊和地球觀測的衛星星座的不斷增加,大大增加了對太空高效運輸和營運支援的需求。此外,太空旅遊和採礦等商業活動的興起,以及政府主導的雄心勃勃的月球和火星計劃,正在催化技術進步並開闢新的成長機會。

太空物流市場分為多種類型,包括服務模組、任務擴展艙(MEP)、貨物模組、機械手臂和操縱器以及太空拖船。 2024 年,服務模組部門將佔據 38% 的市場佔有率,預計將實現顯著成長。這些模組透過提供推進、動力和通訊系統等關鍵功能,對於維持衛星運作至關重要。隨著衛星星座部署的擴大,服務模組在延長衛星壽命和支援軌道永續性方面發揮關鍵作用,推動了其在整個領域的快速應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 75億美元 |

| 複合年成長率 | 18.3% |

市場還根據營運進行細分,關鍵領域包括壽命延長、最後一英里交付、主動碎片清除、空間態勢感知以及在軌組裝和製造。預計到 2034 年,主動碎片清除領域將以驚人的 21.8% 的複合年成長率成長。正在開發機械手臂、網和魚叉等尖端工具來捕獲未使用的衛星和碎片,而人工智慧演算法則提高複雜軌道環境中的導航和操作精度。

預計到 2034 年,北美太空物流市場規模將達到 25 億美元。可重複使用運載火箭的採用在降低營運成本、增加發射頻率方面發揮了關鍵作用,使太空物流運作更有效率、更具成本效益。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 衛星發射需求增加

- 太空運輸和基礎設施的進步

- 不斷成長的可重複使用發射系統和太空船

- 太空中複雜有效載荷部署的需求不斷成長

- 轉向太空服務以及部署和管理衛星艦隊的靈活模式

- 產業陷阱與挑戰

- 太空行動成本高昂

- 空間交通管理與碎片減緩

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 任務擴展艙 (MEP)

- 貨物模組

- 服務模組

- 機械手臂和機械手

- 太空拖船

第6章:市場估計與預測:按營運,2021-2034 年

- 主要趨勢

- 最後一哩配送

- 空間態勢感知

- 延長壽命

- 主動清除碎片

- 在軌組裝和製造

第 7 章:市場估計與預測:按 Orbit,2021 年至 2034 年

- 主要趨勢

- 近地軌道

- 低地球軌道

- 地球靜止軌道

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 商業的

- 政府和國防

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Arianespace

- Astroscale

- Atomos Space

- Blue Origin

- ClearSpace

- D-Orbit

- Exolaunch

- Japan Aerospace Exploration Agency

- Lockheed Martin

- Maxar Technologies

- Northrop Grumman

- Rocket Lab

- SpaceX

- Thales Alenia Space

The Global Space Logistics Market, valued at USD 1.4 billion in 2024, is set to experience robust growth with a projected compound annual growth rate (CAGR) of 18.3% from 2025 to 2034. This growth is largely driven by the increasing demand for satellite deployment, in-orbit servicing, and space exploration programs. Innovations in reusable launch technologies, coupled with the rising deployment of satellite constellations for communication and Earth observation, have significantly boosted the need for efficient transportation and operational support in space. Furthermore, the rise of commercial ventures, such as space tourism and mining, along with ambitious government-led missions to the Moon and Mars, are catalyzing technological advancements and opening up new growth opportunities.

The space logistics market is segmented into various types, including service modules, Mission Extension Pods (MEPs), cargo modules, robotic arms and manipulators, and space tugs. In 2024, the service modules segment held a substantial 38% market share and is expected to see significant growth. These modules have become essential for maintaining satellite operations by providing critical functions such as propulsion, power, and communication systems. As the deployment of satellite constellations expands, service modules are playing a key role in extending satellite lifespans and supporting orbital sustainability, driving their rapid adoption across the sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 billion |

| Forecast Value | $7.5 billion |

| CAGR | 18.3% |

The market is also segmented by operation, with key areas including life extension, last-mile delivery, active debris removal, space situational awareness, and on-orbit assembly and manufacturing. The active debris removal segment is forecasted to grow at an impressive CAGR of 21.8% through 2034. This growth is fueled by advancements in autonomous robotics and artificial intelligence (AI) technologies, which enhance space debris management systems. Cutting-edge tools such as robotic arms, nets, and harpoons are being developed to capture unused satellites and debris, while AI-powered algorithms improve navigation and operational precision in complex orbital environments.

North America space logistics market is projected to reach USD 2.5 billion by 2034. The U.S. market, in particular, is experiencing significant growth due to the increasing demand for satellite deployment and advancements in space infrastructure. The adoption of reusable launch vehicles has played a critical role in reducing operational costs and increasing launch frequencies, making space logistics operations more efficient and cost-effective.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased satellite launch demand

- 3.6.1.2 Advancements in space transportation and infrastructure

- 3.6.1.3 Growing reusable launch systems and spacecraft

- 3.6.1.4 Rising demand for complex payload deployment in space

- 3.6.1.5 Shift toward space as a service and flexible models for deploying and managing satellite fleets

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of space operations

- 3.6.2.2 Space traffic management and debris mitigation

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Mission extension pods (MEPs)

- 5.3 Cargo modules

- 5.4 Service modules

- 5.5 Robotic arms and manipulators

- 5.6 Space tugs

Chapter 6 Market Estimates & Forecast, By Operation, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Last mile delivery

- 6.3 Space situational awareness

- 6.4 Life-extension

- 6.5 Active debris removal

- 6.6 On-orbit assembly and manufacturing

Chapter 7 Market Estimates & Forecast, By Orbit, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Near earth orbit

- 7.3 Lower earth orbit

- 7.4 Geostationary orbit

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government and defense

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arianespace

- 10.2 Astroscale

- 10.3 Atomos Space

- 10.4 Blue Origin

- 10.5 ClearSpace

- 10.6 D-Orbit

- 10.7 Exolaunch

- 10.8 Japan Aerospace Exploration Agency

- 10.9 Lockheed Martin

- 10.10 Maxar Technologies

- 10.11 Northrop Grumman

- 10.12 Rocket Lab

- 10.13 SpaceX

- 10.14 Thales Alenia Space

2025 年至 2033 年按車型、運輸方式、最終用途和地區分類的物流市場規模、佔有率、趨勢和預測

2025 年至 2033 年按車型、運輸方式、最終用途和地區分類的物流市場規模、佔有率、趨勢和預測 整車物流市場規模、佔有率及成長分析(按模式、車輛、服務、最終用途和地區)- 產業預測,2025-2032 年

整車物流市場規模、佔有率及成長分析(按模式、車輛、服務、最終用途和地區)- 產業預測,2025-2032 年 整車物流,全球 2025-2029

整車物流,全球 2025-2029 整車物流 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

整車物流 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 資料中心物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

資料中心物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 2024 年中程配送全球市場報告

2024 年中程配送全球市場報告 2024 年全球汽車廢棄物市場報告

2024 年全球汽車廢棄物市場報告 2024 年製造物流全球市場報告

2024 年製造物流全球市場報告 完成2024年汽車物流全球市場報告

完成2024年汽車物流全球市場報告 港口物流市場評估:類型·服務·用途·產業·各地區的機會及預測 (2018-2032年)

港口物流市場評估:類型·服務·用途·產業·各地區的機會及預測 (2018-2032年)