|

市場調查報告書

商品編碼

1685219

麥芽糊精市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Maltodextrin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

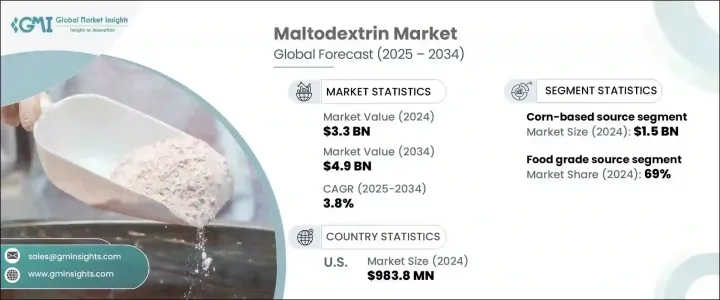

2024 年全球麥芽糊精市場價值為 33 億美元,預計將在 2025 年至 2034 年期間以 3.8% 的複合年成長率強勁成長。麥芽糊精在食品和飲料、製藥和化妝品等各行業有著廣泛而多樣的應用,因此對麥芽糊精的需求正在激增。特別是食品和飲料行業仍然是市場擴張的主要驅動力,因為麥芽糊精被廣泛用作加工食品中的填充劑、增稠劑和穩定劑。隨著消費者對簡便食品和功能性成分的偏好日益增加,麥芽糊精的需求預計將穩定上升。為了滿足不斷變化的消費者需求(包括更健康、更便利的選擇),產品開發的創新進一步推動了這一成長。隨著全球麥芽糊精市場繼續豐富其產品供應,各行各業都在利用其成本效益和功能優勢,確保未來十年的持續成長。

麥芽糊精市場分為各種來源,包括玉米、馬鈴薯、木薯、小麥等。玉米麥芽糊精是主要細分市場,2024 年其產值為 15 億美元,預計到 2034 年將達到 21 億美元。玉米麥芽糊精的廣泛可用性、價格實惠性和多功能性使其成為食品和飲料製造商的首選。同時,小麥麥芽糊精也佔據了相當大的市場佔有率,因其功能特性和在眾多行業的適應性而受到青睞。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 33億美元 |

| 預測值 | 49億美元 |

| 複合年成長率 | 3.8% |

就產品等級而言,麥芽糊精市場分為醫藥級、食品級及工業級。食品級麥芽糊精將在 2024 年佔據 69% 的市場佔有率,佔據市場主導地位,這主要歸功於其在增稠、穩定和膨脹各種食品方面的作用。它能夠改善質地並延長保存期限,這使得它在加工食品中不可或缺。藥用級麥芽糊精雖然佔有率較小,但它作為藥片和膠囊生產中的填充劑和粘合劑至關重要,有助於市場穩定成長。

美國麥芽糊精市場價值 2024 年為 9.838 億美元,在全球市場仍佔有重要地位。美國蓬勃發展的食品加工產業,加上麥芽糊精作為多功能添加劑的廣泛使用,確保了美國仍然佔據主導地位。此外,美國製藥業持續推動穩定的需求,進一步推動成長。麥芽糊精配方的技術進步和創新有望滿足消費者對功能性、便利性和健康意識食品日益成長的需求,從而進一步推動區域市場的發展。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 食品飲料產業需求不斷成長

- 健康意識不斷增強

- 擴大在藥品和化妝品領域的應用

- 產業陷阱與挑戰

- 健康問題和看法

- 原物料價格波動

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場規模與預測:按來源,2021-2034 年

- 主要趨勢

- 玉米基

- 小麥基

- 馬鈴薯為主

- 木薯為主

- 其他

第6章:市場規模及預測:依等級,2021-2034 年

- 主要趨勢

- 食品級

- 醫藥級

- 工業級

第 7 章:市場規模與預測:按應用,2021-2034 年

- 主要趨勢

- 食品和飲料

- 烘焙食品

- 糖果

- 乳製品

- 飲料

- 簡便食品

- 其他

- 藥品

- 藥物製劑中的賦形劑

- 營養補充品

- 化妝品和個人護理

- 保養產品

- 護髮產品

- 工業應用

- 黏合劑

- 黏合劑

- 塗層和封裝

- 其他

- 動物飼料

- 發酵過程

第 8 章:市場規模與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- AGRANA Group

- Archer Daniels Midland

- Avebe

- Cargill

- Golden Grain Group

- Grain Processing Corporation

- Gulshan Polyols

- Ingredion

- Matsutani America

- Mengzhou Tailijie

- Roquette Frères

- Tate & Lyle

- Zhucheng Dongxiao Biotechnology

The Global Maltodextrin Market, valued at USD 3.3 billion in 2024, is set to experience robust growth at a CAGR of 3.8% from 2025 to 2034. The demand for maltodextrin is surging due to its broad and versatile applications across various industries, such as food and beverage, pharmaceuticals, and cosmetics. In particular, the food and beverage industry remains the primary driver of market expansion, as maltodextrin is widely used as a filler, thickener, and stabilizer in processed foods. With the increasing consumer preference for convenience foods and functional ingredients, the demand for maltodextrin is expected to rise steadily. This growth is further fueled by the innovation in product development to meet evolving consumer needs, including healthier, on-the-go options. As the global maltodextrin market continues to diversify its product offerings, industries are capitalizing on its cost-effectiveness and functional benefits, ensuring sustained growth well into the next decade.

The maltodextrin market is divided into various sources, including corn, potato, cassava, wheat, and others. Corn-based maltodextrin, the leading segment, generated USD 1.5 billion in 2024 and is projected to reach USD 2.1 billion by 2034. The widespread availability, affordability, and multifunctionality of corn-based maltodextrin make it the go-to choice for food and beverage manufacturers. Meanwhile, wheat-based maltodextrin also maintains a significant share in the market, prized for its functional qualities and adaptability across numerous industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 3.8% |

In terms of product grade, the maltodextrin market is segmented into pharmaceutical grade, food grade, and industrial grade. Food-grade maltodextrin dominates the market with a 69% share in 2024, largely due to its role in thickening, stabilizing, and bulking various food products. Its ability to improve texture and enhance shelf life makes it indispensable in processed foods. Pharmaceutical-grade maltodextrin, while a smaller segment, is crucial as a filler and binder in the production of medical tablets and capsules, contributing to the market's steady growth.

The U.S. maltodextrin market, valued at USD 983.8 million in 2024, remains a major player in the global landscape. The country's thriving food processing industry, coupled with the widespread use of maltodextrin as a multifunctional additive, ensures the U.S. remains a dominant market. Additionally, the pharmaceutical industry in the U.S. continues to drive consistent demand, further fueling growth. Technological advancements and innovations in maltodextrin formulations are expected to meet the growing consumer demand for functional, convenient, and health-conscious food products, boosting the regional market even further.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand in food and beverage industry

- 3.6.1.2 Rising health consciousness

- 3.6.1.3 Expanding applications in pharmaceuticals and cosmetics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Health concerns and perception

- 3.6.2.2 Fluctuating raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn-based

- 5.3 Wheat-based

- 5.4 Potato-based

- 5.5 Cassava-based

- 5.6 Others

Chapter 6 Market Size and Forecast, By Grade, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food grade

- 6.3 Pharmaceutical grade

- 6.4 Industrial grade

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.2.1 Baked goods

- 7.2.2 Confectionery

- 7.2.3 Dairy products

- 7.2.4 Beverages

- 7.2.5 Convenience foods

- 7.2.6 Others

- 7.3 Pharmaceuticals

- 7.3.1 Excipient in drug formulations

- 7.3.2 Nutritional supplements

- 7.4 Cosmetics and personal care

- 7.4.1 Skincare products

- 7.4.2 Haircare products

- 7.5 Industrial applications

- 7.5.1 Adhesives

- 7.5.2 Binders

- 7.5.3 Coating and encapsulation

- 7.6 Others

- 7.6.1 Animal feed

- 7.6.2 Fermentation processes

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AGRANA Group

- 9.2 Archer Daniels Midland

- 9.3 Avebe

- 9.4 Cargill

- 9.5 Golden Grain Group

- 9.6 Grain Processing Corporation

- 9.7 Gulshan Polyols

- 9.8 Ingredion

- 9.9 Matsutani America

- 9.10 Mengzhou Tailijie

- 9.11 Roquette Frères

- 9.12 Tate & Lyle

- 9.13 Zhucheng Dongxiao Biotechnology

全球麥芽糊精市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球麥芽糊精市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 麥芽糊精市場:依原料、形式、應用及地區分類麥芽糊精市場規模、佔有率、成長分析,按來源、形式、應用、地區 - 產業預測,2025-2032 年

麥芽糊精市場:依原料、形式、應用及地區分類麥芽糊精市場規模、佔有率、成長分析,按來源、形式、應用、地區 - 產業預測,2025-2032 年 全球耐消化麥芽糊精市場 - 2024-2031難消化麥芽糊精市場:全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2031麥芽糊精市場:依產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2032 年

全球耐消化麥芽糊精市場 - 2024-2031難消化麥芽糊精市場:全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2031麥芽糊精市場:依產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2032 年 全球麥芽糊精市場 – 預測(~2030 年)

全球麥芽糊精市場 – 預測(~2030 年)