|

市場調查報告書

商品編碼

1624595

冷凍食品包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Frozen Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

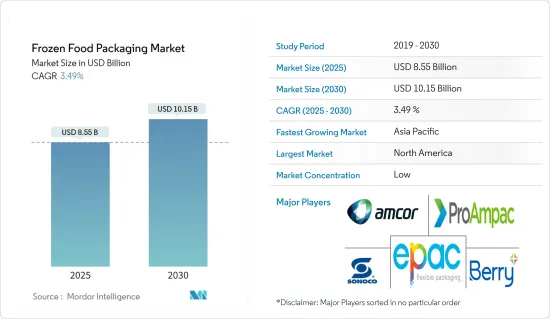

冷凍食品包裝市場規模預計到2025年為85.5億美元,預計到2030年將達到101.5億美元,預測期內(2025-2030年)年複合成長率為3.49%。

冷凍食品包裝具有輕量、不易破損和可重新密封的特點,可以減少石化燃料的使用,減少溫室氣體排放和水的使用,從而創造一個更綠色的環境。

主要亮點

- 市場消費者更喜歡零售店、超級市場和大賣場。有組織的零售商店在全球範圍內佔有重要地位,並佔據了市場的很大一部分。有組織的零售連鎖店的興起與冷凍食品行業對食品包裝解決方案的需求直接相關。

- 肉類、家禽和魚貝類等冷凍食品包裝在其他食品應用中成長最快。全球許多領先的食品包裝公司都推出了極具創造性和裝飾性的包裝。

- 例如,2023 年 8 月,纖維產品製造商 Ahlstrom 與永續包裝供應商 The Paper People 合作,推出了冷凍食品的永續包裝解決方案。這種完整的纖維包裝由兩家公司共同開發,旨在替代傳統的化石塑膠和薄膜,主要用於冷凍食品包裝。這種可回收包裝可與現有包裝設備一起使用,包括垂直成形充填密封、立式袋和 SOS 型系統。

- 此外,2023 年 5 月,Sabic 與 Estiko Packaging Solutions 和挪威品牌所有者 Coldwater Prawns 合作,設計和製造了一種用於冷凍蝦的新型永續包裝袋。該袋由循環認證的隨機聚合物級 Sabic PP(聚丙烯)晶體(Estico Packaging Solutions 提供的多層薄膜)製成,含有約 60% 的海洋塑膠。

- 然而,政府包裝法律和法規可能會限制市場成長。在美國,食品藥物管理局(FDA) 負責監管食品中添加物質的安全性。整體而言,冷凍食品包裝需要以下基本特性:耐低溫和高溫,一定的機械強度,耐酸、油和食品中存在的其他分解化學物質,以及一定的衛生水平和相似性。

冷凍食品包裝市場趨勢

肉類和海鮮食品佔據主要市場佔有率

- 冷凍肉類市場預計在未來幾年將顯著成長,這主要是由於食品偏好的變化。 COVID-19 爆發後,對冷凍肉類和包裝已調理食品的需求激增。隨著時間的推移,肉類產業已經多元化,現在許多加工公司提供冷凍肉類和已調理食品。值得注意的是,該行業幾乎在世界每個地區都在擴張。

- 消費者越來越願意為更高的品質支付溢價。消費者始終更喜歡優先生產不含防腐劑或最少防腐劑的冷凍肉類產品的品牌。因此,消費者對健康飲食的偏好不斷增加,將推動以「有機」且不含防腐劑的方式銷售的冷凍肉和魚產品的需求。現在,許多人對購買冷凍肉品充滿信心,因為它們具有比生鮮肉更長的保存期限等優點。

- 據紐西蘭統計局稱,2023 年紐西蘭冷凍雞肉產量將略高於 68,000 噸,高於前一年的約 63,000 噸。這種成長趨勢預計將持續下去,進一步推動冷凍食品包裝的需求。

- 根據挪威風險管理和保證公司挪威船級社(DNV)的水產品預測,到2050年,全球人均水產品需求將穩定成長。隨著市場的擴大,維持水產品的品質已成為最重要的議題。這需要包裝解決方案能夠減少微生物生長,防止冷凍,促進快速冷凍,並透過最大限度地減少滴水損失來延長保存期限。因此,包裝水產品產品的消費不斷增加,推動了對冷凍水產品包裝的需求。

- 市場主要企業不斷推出新的冷凍水產品產品,從而擴大了包裝供應商的機會。例如,2024 年 5 月,Scott & Jon's 擴大了其冷凍蝦系列,新增了一款可微波爐加熱的鮭魚碗。這些最新產品是 Scott &Jon 於 2023 年推出注重健康的蝦碗系列後推出的。

亞太地區將經歷最快的成長

- 在亞太地區,人口成長正在推動食品需求的擴大。都市化以及人們對食物中毒、浪費和腐敗的認知不斷提高,推動了對更高品質產品的需求。中國在亞太冷凍食品包裝市場中佔有主要佔有率。該國龐大的人口和都市化刺激了人們對冷凍食品日益成長的需求。當今的消費者優先考慮便利性和品質。

- 印度的冷凍食品產業正在迅速擴張。每個品牌的冷凍食品都成功地從偶爾聚會上提供的輕食轉變為各個年齡層的人都喜歡的必備品。對已調理食品(RTE) 和簡便食品的需求正在迅速增加,尤其是隨著勞動力的成長。這種趨勢在現代夫婦中更為明顯,他們生活忙碌,為家人尋求快速、營養的膳食。

- 隨著健康和健身趨勢在整個全部區域蓬勃發展,冷凍食品產業也不甘落後。包裝在這個行業中起著至關重要的作用。食品製造商優先考慮確保其產品從生產到消費的整個過程都是安全且不受污染的,而強大的冷凍食品包裝解決方案有效地應對了這一挑戰。

- 由於高品質和易於準備的流行趨勢,冷凍食品包裝受到日本消費者的青睞。此外,日本跨國食品和生物技術公司味之素預測,日本家庭冷凍食品消費將從上一年的486億日元(3.3億美元)增至2023年的603億日元(4.1億美元)。 ,這將增加到 10,000,000 美元。這一激增將推動該地區冷凍食品包裝市場的發展。

- 此外,由於冷凍肉類和已烹調肉類的需求不斷增加,中國、日本、印度和其他亞洲國家的冷凍食品包裝市場規模正在擴大。根據中國國家統計局統計,近年來冷凍食品包裝產業成長近30%。

冷凍食品包裝產業概況

冷凍食品包裝市場較為分散,由幾家主要參與者組成,例如 Sonoco Products Company.ProAmpac LLC、Cascades Inc.從市場佔有率來看,目前只有少數大公司佔據市場主導地位。然而,具有創意和裝飾性包裝圖案的中小企業正在透過贏得新契約和開發新市場來增加其市場佔有率。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

第5章市場動態

- 市場促進因素

- 新興國家對冷凍食品的需求不斷擴大

- 有組織的零售店增加

- 市場限制因素

- 政府監管和干涉

第6章 市場細分

- 依食品類型

- 水果和蔬菜

- 肉類/海鮮

- 冷凍甜點和冰淇淋

- 烘焙點心

- 按包裝類型

- 包包

- 盒子

- 管杯

- 托盤

- 饒舌歌手

- 小袋

- 其他包裝

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞洲

- 中國

- 日本

- 印度

- 韓國

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- ProAmpac LLC

- Sonoco Products Company

- Amcor PLC

- Berry Plastics Group Inc.

- ePac Holdings, LLC

- Cascades Inc.

- Duropack Limited

- Smurfit Westrock plc

- Mondi Group

- American Packaging Corporation

- ThinkInk Packaging

第8章投資分析

第9章 市場機會及未來趨勢

The Frozen Food Packaging Market size is estimated at USD 8.55 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 3.49% during the forecast period (2025-2030).

Frozen food packaging delivers lightweight, unbreakable, and resealable features, lowers fossil fuel usage, and can reduce greenhouse gas emissions and water usage to create an eco-friendly environment.

Key Highlights

- The market's consumers prefer retail stores, supermarkets, and hypermarkets. Organized retail stores are a substantial part of the market with a significant global presence. The increase in the organized retail chain is translating directly into the need for food packaging solutions in the frozen food industry.

- Packaging for frozen foods like meat, poultry, and seafood witnessed the fastest growth among other food applications. Many large food packaging companies across the globe are launching hugely creative and decorative packaging.

- For instance, in August 2023, fiber-based products manufacturer Ahlstrom teamed up with sustainable packaging provider The Paper People to launch a sustainable packaging solution for frozen food. Co-developed by the two companies, this fully fiber-based packaging is mainly designed to substitute traditional fossil-based plastic and films for frozen food packaging. The recyclable packaging can be utilized on existing packaging equipment, including vertical form-fill-seal, stand-up pouches, and SOS-style systems.

- Also, in May 2023, Sabic joined forces with Estiko Packaging Solutions and brand owner Coldwater Prawns of Norway to design and execute a sustainable new packaging pouch for frozen prawns. The pouch is made from a multilayer film offered by Estiko Packaging Solutions utilizing a circular-certified random polymer grade of Sabic PP (polypropylene) Qrystal with an ocean-bound plastic content of around 60%.

- However, the government packaging laws and regulations could limit the market growth. In the United States, the Food and Drug Administration (FDA) regulates the safety of substances added to food. Overall, frozen food packaging should have the following essential characteristics: Resistance to low and high temperatures, a particular mechanical strength, resistance to acid, oil, and other degrading chemicals in the food product, and a specific level of hygiene and similar.

Frozen Food Packaging Market Trends

Meat and Sea Food to Account for a Major Share in the Market

- The frozen meat market is poised for substantial growth in the coming years, primarily driven by shifting food preferences. Following the COVID-19 outbreak, demand surged for frozen meats and packaged, ready-to-eat foods. Over time, the meat industry has diversified, with numerous processing firms now offering frozen meat products and ready-to-eat items. Notably, this sector is witnessing expansion in nearly every region worldwide.

- Consumers are increasingly willing to pay a premium for higher quality. They consistently prefer brands that prioritize producing frozen meat items with minimal or no preservatives. As a result, the growing consumer preference for healthy eating is set to boost the demand for frozen meat and fish products marketed as "organic" and preservative-free.Many individuals now purchase frozen meat products with confidence, drawn by advantages like extended shelf life compared to fresh meat.

- Statistics New Zealand reported that New Zealand produced just over 68 thousand metric tons of frozen chicken meat in 2023, up from approximately 63 thousand metric tons the year before. This upward trend is anticipated to continue, further driving the demand for frozen food packaging.

- According to the "Seafood Forecast" by Det Norske Veritas (DNV), a Norwegian risk management and assurance firm, global per capita seafood demand is set to rise steadily until 2050. As markets expand, maintaining seafood quality becomes paramount. This necessitates packaging solutions that extend shelf life by curbing microbial growth, preventing freezer burn, facilitating rapid freezing, and minimizing drip loss. Consequently, the rising consumption of packaged seafood products is driving up the demand for frozen seafood packaging.

- Major players in the market are consistently launching new frozen seafood products, thereby expanding opportunities for packaging vendors. For example, in May 2024, Scott & Jon's expanded its frozen shrimp entree line to include new microwavable salmon bowls. These latest offerings come on the heels of Scott & Jon's 2023 debut of its health-focused shrimp bowl line.

Asia-Pacific to Witness the Fastest Growth

- In the Asia-Pacific region, a growing population is driving an increasing demand for food products. Urbanization and heightened awareness of foodborne illnesses, wastage, and spoilage are fueling demand for higher-quality offerings. China holds a significant share of the Asia-Pacific frozen food packaging market. The country's vast population and urbanization have spurred a rising appetite for frozen food items. Today's consumers prioritize both convenience and quality.

- India's frozen food segment is witnessing rapid expansion. Brands have successfully transitioned their offerings from being occasional party snacks to regular meal items enjoyed by all age groups. The surge in demand for ready-to-eat (RTE) and convenience foods is particularly pronounced among the growing working population. This trend is even more evident among modern couples, both of whom lead busy lives and seek quick, nutritious meals for their families.

- As the health and fitness trend gains momentum across the region, the frozen foods sector is not left behind. Packaging plays a pivotal role in this industry. Food manufacturers prioritize ensuring their products remain safe and contamination-free from production to consumption, a challenge effectively addressed by robust frozen food packaging solutions.

- Due to its high quality and popular easy-to-cook trends, frozen food packaging is preferred by Japanese consumers. Moreover, Ajinomoto, a Japanese multinational food and biotechnology corporation, reported that the consumption of home-use frozen meals in Japan rose to JPY 60.3 billion (USD 0.41 billion) in 2023, up from JPY 48.6 billion (USD 0.33 billion) the previous year. This surge is poised to boost the market for frozen food packaging options in the region.

- Additionally, the size of China, Japan, India and other Asian countries frozen food packaging market is expanding due to the rise in demand for frozen meat and ready-to-eat meal products. The National Bureau of Statistics of China states that the industry saw an increase in frozen food packaging of almost 30% in the last few years.

Frozen Food Packaging Industry Overview

The frozen food packaging market is fragmented and consists of several major players, such as Sonoco Products Company. ProAmpac LLC, Cascades Inc., and more. In terms of market share, few of the major players currently dominate the market. However, with creative and decorative packaging patterns, mid-size to smaller companies are increasing their market presence by securing new contracts and tapping new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Frozen Food Demand in Emerging Countries

- 5.1.2 Rising Number of Organized Retail Stores

- 5.2 Market Restraint

- 5.2.1 Government Regulations and Interventions

6 MARKET SEGMENTATION

- 6.1 By Type of Food

- 6.1.1 Fruits and Vegetables

- 6.1.2 Meat and Sea Food

- 6.1.3 Frozen Desserts and Ice Creams

- 6.1.4 Baked Foods

- 6.2 By Type of Packaging

- 6.2.1 Bags

- 6.2.2 Boxes

- 6.2.3 Tubs and Cups

- 6.2.4 Trays

- 6.2.5 Wrappers

- 6.2.6 Pouches

- 6.2.7 Other Types of Packaging

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ProAmpac LLC

- 7.1.2 Sonoco Products Company

- 7.1.3 Amcor PLC

- 7.1.4 Berry Plastics Group Inc.

- 7.1.5 ePac Holdings, LLC

- 7.1.6 Cascades Inc.

- 7.1.7 Duropack Limited

- 7.1.8 Smurfit Westrock plc

- 7.1.9 Mondi Group

- 7.1.10 American Packaging Corporation

- 7.1.11 ThinkInk Packaging

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

冷凍袋市場報告:2031 年趨勢、預測與競爭分析自封袋市場報告:趨勢、預測和競爭分析(至 2031 年)水產品包裝市場報告:趨勢、預測和競爭分析(至 2031 年)

冷凍袋市場報告:2031 年趨勢、預測與競爭分析自封袋市場報告:趨勢、預測和競爭分析(至 2031 年)水產品包裝市場報告:趨勢、預測和競爭分析(至 2031 年) 水產品包裝市場:未來預測(2025-2030)

水產品包裝市場:未來預測(2025-2030) 中東和非洲的冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)亞太冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲冷凍食品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)美國冷凍食品包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)

中東和非洲的冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)亞太冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲冷凍食品包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲冷凍食品包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)美國冷凍食品包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)