|

市場調查報告書

商品編碼

1626882

分散式發電-市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Distributed Power Generation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

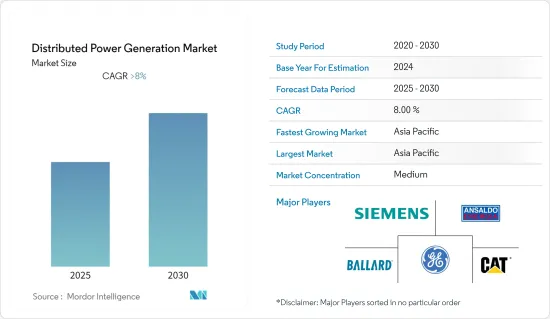

預計分散式發電市場在預測期內將維持8%以上的複合年成長率。

COVID-19 對 2020 年市場產生了負面影響。目前,市場已達到疫情前水準。

主要亮點

- 中期來看,由於可再生能源發電、系統成本降低以及世界各國政府的支持措施,以分散式太陽能發電為中心的可再生能源分散式發電的轉變將取得進展。

- 另一方面,由於初始投資較低且不需要發電空間,消費者往往喜歡併網發電而不是離網發電。預計這將阻礙預測期內分散式發電市場的成長。

- 人們對環境問題的認知不斷提高、遏制碳排放的國際要求以及一些國家政府引入再生能源來源的有利措施,為我正在做的分散式發電市場提供了機會。

- 亞太地區佔最大的市場佔有率,中國、印度和東協成員國等國家的能源需求不斷增加。中國擁有蓬勃發展的製造業,需要電力運作。因此,該地區正在使用分散式發電來提供不間斷的電力。

分散式發電市場趨勢

太陽能主導市場

- 預計住宅市場將在預測期內迅速擴張。帶有電池儲存系統的離網屋頂太陽能發電為住宅家庭提供可靠的二次電力,推動了整個細分市場的產品需求。為了因應電力需求高峰變化而引入大規模儲能系統,導致採用超大型屋頂太陽能發電系統,將必要的電力儲存在電池中。

- 屋頂太陽能發電系統可以根據您的要求建造。這可以讓消費者節省電費。一般家庭的太陽能發電設備稱為電錶後端太陽能。分散式太陽能發電系統被稱為電錶後端太陽能發電系統,因此消費者無需為其產生的太陽能電力向電力公司付費。

- 根據其位置的不同,在陽光明媚的中午,太陽能電池板只能將總太陽輻射的 15% 到 20% 轉化為電能。多晶或結晶面板安裝在屋頂、開放空間或牆壁上,正面面向太陽,以產生足夠一天的能量。

- 根據國際可再生能源機構(IRENA)統計,2022年太陽能發電容量約為10,46,614兆瓦,與前一年同期比較成長22.4%。這段時期的趨勢顯示持續成長的趨勢。

- 隨著太陽能電池板和電池儲存價格的下降以及建築成本的下降,安裝帶有電池儲存系統的分散式太陽能發電並以11kV或33kV傳輸太陽能變得有吸引力。它可以減少輸電線路損耗,提高農村支線的電網彈性,避免輸配電損耗,降低發電成本,並降低新發電設備的投資成本。

- 因此,隨著太陽能發電技術的介入,較低的發電成本和易於建造的太陽能發電系統有望推動分散式發電市場的發展。

亞太地區主導市場

- 亞太地區佔最大的市場佔有率,中國、印度和東協成員國等國家的能源需求不斷增加。中國擁有廣泛的製造業,需要電力來運作。因此,該地區依靠分散式發電來提供不間斷電力。

- 可再生能源市場的關鍵驅動力是政府的大力支持、技術進步和碳排放管理意識。這有利於中國可再生能源產業的快速發展。到2022年終,中國預計將安裝分散式發電48GW。我國分散式太陽能發電主要以工商企業為主,採用EMC(合約能源管理)模式建置DSPV電站。由於中國土地價格高昂,安裝太陽能屋頂的機會正在增加。

- 在印度,預計2022年太陽能發電裝置容量將達到61吉瓦。為了實現100吉瓦太陽能裝置容量的目標,太陽能園區計畫、VGF計畫、CPSU計畫、防禦計畫、運河岸/運河頂部計畫、捆綁計畫、併網太陽能屋頂計畫等許多計畫都在規劃和實施近年來已訂定措施。

- 印度計劃在2030年在其電網中新增500GW大規模可再生能源,規劃什麼樣的電網架構將支援這種水準的可再生能源併網至關重要。分散式可再生能源有充分理由成為未來電網的重要組成部分。

- 此外,分散式發電可以為無法擴展電網的各種偏遠地區的企業和業主帶來顯著的好處。

- 亞太地區在擴展分散式能源系統(DES)方面具有巨大潛力,特別是離網和住宅太陽能發電。電網基礎設施效率低下、電力供不應求以及分散技術的可擴展性正在推動該地區的部署,特別是在中國和印度。

分散式發電產業概況

分散式發電市場適度細分。市場的主要企業包括(排名不分先後)Ansaldo Energia SpA、Ballard Power Systems Inc.、Caterpillar Inc.、Siemens AG 和 General Electric Company。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 至2028年市場規模及需求預測(單位:百萬美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 科技

- 太陽能

- 柴油發電機

- 天然氣發電機

- 微型電網

- 其他

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 南美洲

- 中東/非洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Ansaldo Energia SpA

- Ballard Power Systems Inc.

- Bloom Energy

- Capstone Turbine Corporation

- Caterpillar Inc.

- Cummins Inc.

- Fuelcell Energy Inc.

- General Electric Co.

- Schneider Electric SE

- Siemens AG

- Sunverge Energy

- Canadian Solar Inc.

第7章 市場機會及未來趨勢

簡介目錄

Product Code: 48339

The Distributed Power Generation Market is expected to register a CAGR of greater than 8% during the forecast period.

COVID-19 negatively impacted the market in 2020. Currently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, the increasing shift toward renewable distributed power generation, mainly distributed solar PV installation, owing to declining renewable power generation and system costs, coupled with supportive government policies worldwide.

- On the other hand, consumers tend to prefer grid power over off-grid power owing to the low initial investment and no space requirement to generate electricity. This is expected to hamper the growth of the distributed power generation market over the forecast period.

- Nevertheless, the growing environmental concerns, international mandates to curb carbon emissions, and conducive policies by the governments of several countries to install renewable energy sources provide an opportunity for the distribution power generation market.

- Asia-Pacific holds the largest market share and has witnessed increasing energy demand in countries such as China, India, and ASEAN member states. China has a widespread manufacturing sector, which creates a need for power for operations. Thus, distributed power generation is used in this region to supply uninterrupted power.

Distributed Power Generation Market Trends

Solar PV to Dominate the Market

- The residential segment is expected to expand rapidly over the forecast period. Off-grid rooftop solar PV equipped with an energy battery storage system provides reliable secondary power to residential households, thereby boosting product demand across the segment. The deployment of large-scale storage systems to protect against peak demand power changes has resulted in the adoption of extra-large rooftop solar PV systems to store desired power in batteries.

- Rooftop Solar energy systems can be built, depending on the requirements. It enables consumers to save on their electric utility bills. Solar installations in households are called behind-the-meter solar," since the meter captures how much electricity the consumer is purchasing from a utility. Since distributed solar energy systems are called behind-the-meter, consumers do not pay the utility for the solar power generated.

- According to the location, the solar panels only convert between 15% and 20% of the total solar irradiation at noon on a bright, sunny day into electricity. The polycrystalline or monocrystalline panels are installed on rooftops, open grounds, or walls, with the front facing the sun, to produce sufficient energy in a day.

- As per International Renewable Energy Agency (IRENA) statistics, in 2022, the solar photovoltaic energy capacity was around 10,46,614 MW, up by 22.4% from the previous year. In the period under consideration, figures presented a trend of continuous growth.

- With the downward trend of solar panel and battery storage prices and declining construction costs, establishing distributed PV with a battery storage system and evacuating solar energy at 11 kV or 33 kV is an attractive proposition. It will reduce transmission line losses, increase grid resilience for rural feeders, avoid transmission distribution losses, reduce generation costs, and reduce investment costs in new utility generation capacity.

- Hence, due to technological interventions in solar PV, the declining cost of electricity generation and ease of construction of solar systems are expected to drive the distributed power generation market.

Asia-Pacific to Dominate the Market

- Asia-Pacific holds the largest market share and has witnessed increasing energy demands in countries such as China, India, and ASEAN member states. China has a widespread manufacturing sector, which creates a need for power for operations. Thus, distributed power generation is used in this region to supply uninterrupted power.

- Strong government support, technological progress, and awareness regarding managing carbon emissions are the main drivers for the renewable energy market. This has facilitated the rapid development of China's renewable energy sector. By the end of 2022, China was expected to install 48 GW of distributed generation. China's distributed solar power is dominated by industrial and commercial enterprises, which mainly adopt the EMC (energy management contract) model to build DSPV power plants. The high price of land in China is creating opportunities for deploying solar rooftops.

- In India, the installed capacity of solar was expected to reach 61 GW in 2022. To complete the target of deploying 100 GW of solar installed capacity, a slew of schemes such as solar park schemes, VGF schemes, CPSU schemes, defense schemes, canal bank and canal top schemes, bundling schemes, grid-connected solar rooftop schemes, etc., and policy measures have been introduced in recent years.

- With India planning to add a massive 500 GW of renewable energy to its electric grid by 2030, it is critical to plan what kind of grid architecture will support this level of renewable integration, which is likely unprecedented anywhere else in the world. Distributed renewables present a solid case for being a big part of the future grid.

- Additionally, with various places located in remote parts of the country where grid expansion is not feasible, distributed generation can significantly benefit businesses and owners.

- Asia-Pacific holds vast potential for expanding distributed energy systems (DES), notably off-grid and residential solar. Inefficiencies in the power grid infrastructure, power supply shortages, and the scalability of decentralized technology are driving the deployment in the region, particularly in China and India.

Distributed Power Generation Industry Overview

The distributed power generation market is moderately fragmented. Some key players in this market include (in no particular order) Ansaldo Energia SpA, Ballard Power Systems Inc., Caterpillar Inc., Siemens AG, and General Electric Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD Million, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Solar PV

- 5.1.2 Diesel Gensets

- 5.1.3 Natural Gas Gensets

- 5.1.4 Microgrids

- 5.1.5 Other Technologies

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Ansaldo Energia SpA

- 6.3.2 Ballard Power Systems Inc.

- 6.3.3 Bloom Energy

- 6.3.4 Capstone Turbine Corporation

- 6.3.5 Caterpillar Inc.

- 6.3.6 Cummins Inc.

- 6.3.7 Fuelcell Energy Inc.

- 6.3.8 General Electric Co.

- 6.3.9 Schneider Electric SE

- 6.3.10 Siemens AG

- 6.3.11 Sunverge Energy

- 6.3.12 Canadian Solar Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

2025年全球發電市場報告

2025年全球發電市場報告 2030 年自發電市場預測:按燃料類型、電廠類型、技術、應用、最終用戶和地區進行的全球分析

2030 年自發電市場預測:按燃料類型、電廠類型、技術、應用、最終用戶和地區進行的全球分析 獨立型發電經營者 (IPP)

獨立型發電經營者 (IPP) 2025 年分散式發電全球市場報告

2025 年分散式發電全球市場報告 全球發電量 2025-2029

全球發電量 2025-2029 北美分散式發電:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

北美分散式發電:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 發電領域無損檢測:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

發電領域無損檢測:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 分散式能源發電系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、最終用戶、地區和競爭細分,2019-2029F

分散式能源發電系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、最終用戶、地區和競爭細分,2019-2029F 低壓工業開關設備市場機會、成長動力、產業趨勢分析與預測 2025 - 2034

低壓工業開關設備市場機會、成長動力、產業趨勢分析與預測 2025 - 2034 分散式發電市場:按技術、最終用戶、應用分類 - 2025-2030 年全球預測

分散式發電市場:按技術、最終用戶、應用分類 - 2025-2030 年全球預測

▼