|

市場調查報告書

商品編碼

1636281

義大利電動汽車電池材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Italy Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

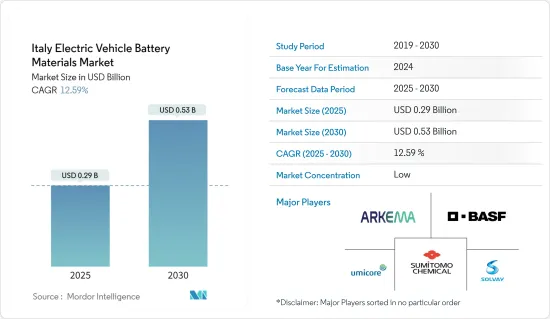

預計2025年義大利電動車電池材料市場規模為2.9億美元,2030年將達5.3億美元,預測期內(2025-2030年)複合年成長率為12.59%。

主要亮點

- 從中期來看,電動車(EV)銷售的成長以及政府的支持性措施和法規預計將在預測期內推動電動車電池材料的需求。

- 另一方面,蘊藏量短缺可能會明顯抑制電動車電池材料市場的成長。

- 電池技術的進步,如提高能量密度、縮短充電時間、提高安全性和延長使用壽命等,預計將在不久的將來為電動車電池材料市場的參與企業提供重大商機。

義大利電動汽車電池材料市場趨勢

電動車 (EV) 銷量的成長推動市場

- 義大利電動車(EV)銷量的增加正在推動該地區對電動車電池材料的需求。隨著電動車銷量的增加,對鋰、鈷、鎳和石墨等關鍵電池組件的需求也在增加。這種不斷成長的需求不僅促進了當地生產,還吸引了投資並加強了義大利的電池材料供應鏈。

- 義大利正在協調一致地轉向清潔能源,重點是電動車。近年來,義大利電動車銷量激增。例如,根據國際能源總署(IEA)的報告,2023年義大利電動車銷量為13.6萬輛,較2022年成長19.29%。由於近期歐洲政府的多項計劃和舉措,電動車銷售量預計將大幅成長,對電池材料的需求也相應增加。

- 義大利政府正積極培育電動車市場,推出補貼和稅收優惠,並實施更嚴格的排放法規。這些支援措施不僅增強了電動車市場,也有利於電池材料產業。政府制定了雄心勃勃的目標,旨在在未來幾年內將電動車銷量翻兩番。

- 例如,2023 年,義大利承諾在 2023 年和 2024 年每年撥款 6.5 億歐元(7.09 億美元)。這筆資金旨在鼓勵購買電動低排放氣體。獎勵針對插電式混合動力汽車和混合動力汽車汽車,補貼最高可達 4,000 歐元(4,368 美元)。這些強力的舉措不僅將促進電動車的生產和銷售,還將增加未來幾年對電池材料的需求。

- 義大利充滿活力的電動車市場正在推動電池技術的創新。當地公司正在與全球領導者合作開發下一代材料,預計將提高電動車的能量密度、延長使用壽命並提高安全性。該地區的主要企業齊聚一堂,預計先進電動車電池的需求將大幅增加。

- 例如,2024 年 2 月,StoreDot 推出了一款革命性的電池,只需 5 分鐘即可充電 100 英里。他們雄心勃勃的計畫目標是到 2028 年將這一時間減少到三分鐘,到 2032 年減少到驚人的兩分鐘。透過策略合作夥伴關係,StoreDot 將向 Italvolt 授權這項創新技術並開始在義大利生產。這些進步不僅將推動對複雜電動車電池的需求,還將擴大該地區對電池材料的需求。

- 考慮到這種發展形勢,很明顯,電動車的銷售勢頭以及支持它的電池材料的需求將繼續增加。

鋰離子電池佔市場主導地位

- 電動車(EV)鋰離子電池產量的增加正在顯著影響電池材料市場。製造業的激增正在推動對鋰的需求,其區域發現對原料成本有直接影響。

- 為了因應這一趨勢,主要市場參與企業正在加大對鋰蘊藏量的投資和研發舉措。其目的是雙重的。目的是擴大鋰離子電池的產量,並滿足快速成長的電池原料需求。隨著新蘊藏量的發現,鋰離子電池的價格已大幅下降。

- 例如,預計2023年電池價格將降至139美元/kWh,降幅為13%。鑑於目前的技術進步和製造效率,專家預測2025年價格可能進一步降至113美元/千瓦時,到2030年降至80美元/度。

- 此外,為了應對日益嚴重的環境問題,義大利政府正在大力推動電動車鋰離子電池的生產。該國政府熱衷於實現淨零碳排放,並已推出多項舉措來提高鋰離子電池產量,以滿足該地區對電動車日益成長的需求。

- 例如,2024年2月,Automotive Cells公司獲得47億美元資金,在法國、德國和義大利建立三個鋰離子電池超級工廠。該合資企業得到了 Stellantis、梅賽德斯-奔馳和帥福得(TotalEnergies 子公司)等行業巨頭的支持,強調了其對鋰離子電池作為能源來源的承諾,並將有助於推動未來對電池材料的需求。

- 近年來,義大利已成為鋰離子電池回收先進技術的先驅。公司和研究機構都在創新方法,以有效地從這些電池中提取鋰、鈷和鎳等有價值的材料。

- 例如,2024年1月,義大利卡車和巴士製造商依維柯集團與德國化學巨頭BASF合作,回收電動車(BEV)的鋰離子電池。該合作夥伴關係的財務細節尚未披露,但它與依維柯的循環經濟願景相呼應,該願景的重點是延長電池壽命和最大限度地減少對環境的影響。這種合作不僅促進了鋰離子原料的生產,而且預計將增加電動車電池原料的產量。

- 因此,這些進步和舉措有望提高鋰離子電池的產量,並在未來幾年顯著增加對電動車電池材料的需求。

義大利電動汽車電池材料產業概況

義大利電動汽車電池材料市場已減半。主要參與企業(排名不分先後)包括住友化學、BASF、阿科瑪、索爾維和優美科。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 至2029年市場規模及需求預測(單位:十億美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車銷量成長

- 政府扶持措施及措施

- 抑制因素

- 對原料供應的依賴

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子電池

- 鉛酸電池

- 其他

- 材料

- 正極

- 負極

- 電解

- 分隔符

- 其他

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Sumitomo Chemical Co., Ltd.

- BASF SE

- Arkema SA

- Solvay SA

- Umicore SA

- Midac Batteries

- FIB SpA

- Ferroglobe

- SGL Carbon

- Fiamm Energy Technology

- 其他知名公司名單

- 市場排名/佔有率分析

第7章 市場機會及未來趨勢

- 電池技術的進步

簡介目錄

Product Code: 50003568

The Italy Electric Vehicle Battery Materials Market size is estimated at USD 0.29 billion in 2025, and is expected to reach USD 0.53 billion by 2030, at a CAGR of 12.59% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- On the other hand, the lack of raw material reserves can significantly restrain the growth of the electric vehicle battery materials market.

- Nevertheless, technological advancements in batteries like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for electric vehicle battery materials market players in the near future.

Italy Electric Vehicle Battery Materials Market Trends

Growing Electric Vehicle (EVs) Sales Drives the Market

- Rising electric vehicle (EV) sales in Italy are driving up the demand for EV battery materials in the region. As sales of EVs climb, so does the need for key battery components like lithium, cobalt, nickel, and graphite. This heightened demand is not only boosting local production but also attracting investments, thereby strengthening Italy's battery material supply chain.

- Italy is making a concerted shift towards clean energy, with electric vehicles taking center stage. Over recent years, EV sales in Italy have seen a remarkable surge. For instance, the International Energy Agency (IEA) reported that in 2023, Italy sold 136,000 electric vehicles, marking a 19.29% increase from 2022. With numerous projects and initiatives recently rolled out by the European government, EV sales are poised for significant growth, subsequently driving up the demand for battery materials.

- The Italian government is actively nurturing the EV market, rolling out subsidies, tax incentives, and enforcing stricter emission regulations. These supportive measures not only bolster the EV market but also extend their benefits to the battery material industry. The government has set ambitious targets, aiming for a fourfold increase in EV sales in the coming years.

- For instance, in 2023, Italy pledged an annual allocation of EUR 650 million (USD 709 million) for both 2023 and 2024. This funding is aimed at incentivizing the purchase of electrified and low-emission vehicles. The incentives cover plug-in hybrids and hybrids, with potential subsidies reaching up to EUR 4,000 (USD 4,368). Such robust initiatives are set to not only boost EV production and sales but also elevate the demand for battery materials in the coming years.

- Italy's dynamic EV market is driving innovations in battery technology. Local firms are collaborating with global leaders to develop next-gen materials that promise better energy density, longer lifespans, and enhanced safety for EVs. Major players in the region are uniting efforts, anticipating a significant uptick in demand for advanced EV batteries.

- For instance, in February 2024, StoreDot showcased a groundbreaking battery that can achieve a 100-mile charge in just five minutes. Their ambitious timeline aims to reduce this to three minutes by 2028 and an impressive two minutes by 2032. In a strategic collaboration, StoreDot has licensed this innovative technology to Italvolt, which is set to kick off production in Italy. Such advancements are poised to not only boost the demand for sophisticated EV batteries but also amplify the need for battery materials in the region.

- Given these developments, it's clear that the momentum in EV sales and the corresponding demand for battery materials is set to continue its upward trajectory.

Lithium-Ion Battery Type Dominate the Market

- The rising production of lithium-ion batteries for electric vehicles (EVs) has significantly shaped the battery materials market. This surge in manufacturing has heightened the demand for lithium, with its regional discoveries directly influencing raw material costs.

- In response to this trend, major market players are intensifying their investments in lithium reserves and R&D initiatives. Their objective is twofold: to amplify lithium-ion battery production and to satisfy the surging demand for battery raw materials. As new reserves are discovered, prices for lithium-ion batteries are experiencing a marked decline.

- For example, in 2023, battery prices notably dropped to USD 139/kWh, a 13% decrease. Given the current pace of technological advancements and manufacturing efficiencies, experts forecast prices could further decline to USD 113/kWh by 2025 and plummet to USD 80/kWh by 2030.

- Moreover, in response to escalating environmental concerns, the Italian government is vigorously championing lithium-ion battery production for electric vehicles. With a keen focus on achieving net-zero carbon emissions, the government has launched multiple initiatives to boost lithium-ion battery production, aiming to meet the region's growing EV demand.

- For instance, in February 2024, Automotive Cells Company secured a USD 4.7 billion fund to establish three lithium-ion battery gigafactories in France, Germany, and Italy. This venture, backed by industry giants like Stellantis, Mercedes-Benz, and Saft (a TotalEnergies subsidiary), underscores the commitment to lithium-ion batteries as a pivotal clean energy source, suggesting a surge in battery material demand in the coming years.

- In recent years, Italy has emerged as a leader in pioneering advanced technologies for recycling lithium-ion batteries. Both companies and research institutions are innovating methods to efficiently extract valuable materials-like lithium, cobalt, and nickel-from these batteries.

- For instance, in January 2024, Iveco Group, an Italian truck and bus manufacturer, partnered with BASF, a leading German chemicals firm, to recycle lithium-ion batteries for its electric vehicles (BEVs). While the financial details of the collaboration remain under wraps, it resonates with Iveco's circular economy vision, emphasizing battery lifespan extension and minimizing environmental impact. Such collaborations not only expedite the production of lithium-ion raw materials but also forecast an uptick in EV battery material production.

- Consequently, these advancements and initiatives are poised to boost lithium-ion battery production and significantly elevate the demand for EV battery materials in the coming years.

Italy Electric Vehicle Battery Materials Industry Overview

Italy's electric vehicle battery materials market is semi-fragmented. Some key players (not in particular order) are Sumitomo Chemical Co., Ltd., BASF SE, Arkema SA, Solvay SA, Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 BASF SE

- 6.3.3 Arkema SA

- 6.3.4 Solvay SA

- 6.3.5 Umicore SA

- 6.3.6 Midac Batteries

- 6.3.7 FIB S.p.A

- 6.3.8 Ferroglobe

- 6.3.9 SGL Carbon

- 6.3.10 Fiamm Energy Technology

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

02-2729-4219

+886-2-2729-4219

全球電動車電池斷開裝置 (BDU) 市場:2031 年預測

全球電動車電池斷開裝置 (BDU) 市場:2031 年預測 全球電動車 (EV) 電池市場(2025-2029 年)

全球電動車 (EV) 電池市場(2025-2029 年) 全球電動車電池市場按電池類型、材料類型、電池配置、推進、車輛類型、電池容量、技術、鋰離子電池組件和地區分類 - 預測至 2035 年

全球電動車電池市場按電池類型、材料類型、電池配置、推進、車輛類型、電池容量、技術、鋰離子電池組件和地區分類 - 預測至 2035 年 中東電動車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

中東電動車電池:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 全球和中國電動汽車電池和材料:技術、趨勢和市場預測

全球和中國電動汽車電池和材料:技術、趨勢和市場預測 全球電動汽車電池單元與電池組材料市場

全球電動汽車電池單元與電池組材料市場 全球電動車工廠建設市場

全球電動車工廠建設市場 電動汽車電池工廠建設的全球市場

電動汽車電池工廠建設的全球市場 電動車 (EV) 黏合劑市場規模、佔有率、成長分析(按樹脂類型、車輛類型、基材、配置、應用和地區)- 2025-2032 年產業預測

電動車 (EV) 黏合劑市場規模、佔有率、成長分析(按樹脂類型、車輛類型、基材、配置、應用和地區)- 2025-2032 年產業預測 電動汽車電池接觸器市場規模、佔有率和成長分析(按接觸器類型、額定電壓、額定功率、冷卻類型、應用和地區)- 產業預測 2025-2032

電動汽車電池接觸器市場規模、佔有率和成長分析(按接觸器類型、額定電壓、額定功率、冷卻類型、應用和地區)- 產業預測 2025-2032

▼