|

市場調查報告書

商品編碼

1636485

中國電動汽車電池陽極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)China Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

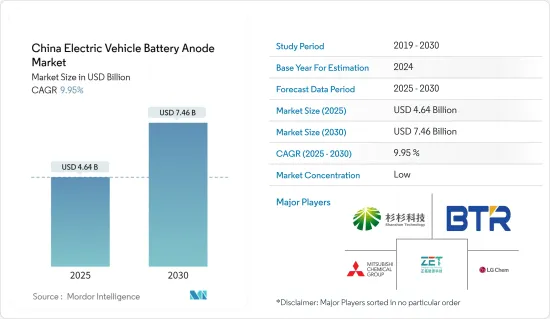

預計2025年中國電動車電池陽極市場規模為46.4億美元,2030年將達74.6億美元,預測期間(2025-2030年)複合年成長率為9.95%。

主要亮點

- 從中期來看,政府對電池製造的支持政策和投資以及鋰離子電池價格的下降預計將在預測期內推動市場。

- 另一方面,陽極材料的高製造成本預計將抑制未來市場的成長。

- 然而,陽極材料和高效電解質的持續研究和進步可能會提供市場成長的機會。

中國電動汽車動力電池陽極市場趨勢

鋰離子電池類型預計將佔據較大佔有率

- 最初,鋰離子電池主要為行動電話、電腦等家用電器提供動力。然而,鋰離子電池的使用已顯著擴大,成為中國混合動力汽車和純電動車(EV)的主要動力來源。這種轉變主要是由電動車的環境效益所推動的,電動車不排放二氧化碳和氮氧化物等溫室氣體。

- 鋰離子電池具有高能量密度、經濟高效且高效的特點,使其成為電動車(EV)的首選。這種採用的增加推動了製造過程中對陽極材料的需求增加。

- 此外,鋰離子材料成本的下降也是電動車鋰離子電池製造需求增加的主要原因。 2023年,鋰離子電池組的價格將與前一年同期比較%,達到139美元/kWh。隨著電池價格下降,電動車將變得更加便宜,從而提高其採用率和市場佔有率。需求的激增推動了包括負極在內的電池組件消費量的增加,並推動了提高電池性能的技術進步。

- 未來,技術創新可望提高電動車用鋰離子電池的效率,同時對負極材料的需求將會增加。

- 例如,2024年4月,中國電動車製造商寧德時代新能源科技有限公司推出了電動車的磷酸鋰鐵鋰(LFP)電池。這種新型電池的能量密度為205Wh/kg,比目前此類電池的技術水準高出近8%。預計此類發展將增加預測期內對電動車鋰離子陽極材料的需求。

- 此外,根據中國工業監督製定的《汽車產業綠色低碳發展藍圖1.0》,到2025年,中國乘用車新能源汽車銷售將成長。這樣的藍圖也有望為中國電動車負極製造帶來未來的機會。

- 因此,由於電動車中鋰離子電池的使用量增加和價格下降,預計鋰離子電池陽極細分市場在預測期內將大幅成長。

政府對電池製造的政策和投資預計將推動市場

- 政府的支持政策和對電池製造的大量投資正在推動中國電動車電池製造的發展,預計這將增加對電動車電池陽極的需求。政府提供直接財政支援、稅收減免和補貼,以降低製造商的成本並鼓勵對先進設備的投資。中國電動車製造商受惠於政府補貼。例如,一輛續航里程超過400公里的純電動插電式汽車將獲得12,600元人民幣(約2,000美元)的補貼。同時,續航里程為300-400公里的汽車將獲得9,100元人民幣(約1,400美元)的補貼。

- 此外,中國對電動車日益成長的需求正在推動電動車電池製造計劃的投資,並創造了對電動車電池陽極材料的潛在需求。根據國際能源總署(IEA)預測,2023年中國電動車電池需求量將為417GWh,高於去年的314GWh。

- 此外,電動車銷量的不斷成長正促使電池製造商加大對電動車電池生產的投資,從而創造了對電動車電池陽極材料的需求。根據國際能源總署 (IEA) 預測,2023 年電動車銷量將達到 810 萬輛,超過 2022 年的 590 萬輛。

- 未來,隨著國內電動車生產的快速發展以及電動車電池製造投資的增加,電動車電池負極材料的需求預計將增加。例如,2024年5月,中國宣布將投資8.45億美元開發下一代電池技術,為電動車提供動力。此類投資可能會在預測期內刺激電動車電池製造的需求。

- 因此,政府的支持政策和對電池製造的投資預計將推動市場。

中國電動汽車動力電池陽極產業概況

中國電動車電池陽極市場呈現半分割狀態。該市場的主要企業(排名不分先後)包括上海杉杉科技、貝特瑞新材料集團、江西鄭都新能源科技、三菱化學集團和LG化學集團。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 電池製造的政府政策和投資

- 降低電池原物料成本

- 抑制因素

- 負極材料製造成本高

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 依電池類型

- 鋰離子

- 鉛酸電池

- 其他電池類型

- 按材質

- 鋰

- 石墨

- 矽

- 其他

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Shanghai Shanshan Technology Co., Ltd.

- BTR New Material Group Co., Ltd.

- Jiangxi Zhengtuo New Energy Technology

- Mitsubishi Chemical Group.

- Shanghai Putailai New Energy Technology

- Targray Industries Inc.

- Ningbo Shanshan Co., Ltd.

- LG Chemical Group

- Tokai Carbon Co., Ltd.

- Resonac Holdings Corporation.

- List of Other Prominent Companies

- 市場排名分析

第7章 市場機會及未來趨勢

- 加大其他陽極材料的研發力度

簡介目錄

Product Code: 50003754

The China Electric Vehicle Battery Anode Market size is estimated at USD 4.64 billion in 2025, and is expected to reach USD 7.46 billion by 2030, at a CAGR of 9.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies and investments in battery manufacturing and the decreasing price of lithium-ion batteries are expected to drive the market in the forecast period.

- On the other hand, high production cost for anode materials is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in anode material and efficient electrolytes may offer opportunities for market growth.

China Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Initially, lithium-ion batteries primarily powered consumer electronics, including mobile phones and personal computers. However, their application has broadened significantly, making them the dominant power source for hybrid and fully electric vehicles (EVs) in China. This transition is primarily driven by the environmental advantages of EVs, which emit no CO2, nitrogen oxides, or other greenhouse gases.

- Due to their high energy density, cost-effectiveness, and efficiency, lithium-ion batteries have become the preferred choice for electric vehicles (EVs). This growing adoption has spurred a rising demand for anode materials during the manufacturing process.

- Further, the decreasing cost of lithium-ion materials is also a significant reason for the increasing demand for lithium-ion battery manufacturing for electric vehicles. In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, increasing adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, as technological innovations enhance the efficiency of lithium-ion batteries in electric vehicles, the demand for anode materials is projected to rise simultaneously.

- For instance, in April 2024, Contemporary Amperex Technology Co., a Chinese electric vehicle manufacturer, launched a lithium iron phosphate (LFP) battery for electric vehicles. The new battery has an energy density of 205 Wh per kg, almost 8% higher than the current state of the art for such batteries. Such developments are expected to boost the demand for EV lithium-ion anode materials in the forecast period.

- Additionally, as per Automotive Industry Green and Low-Carbon Development Roadmap 1.0 developed under the supervision of China's Ministry of Industry and Information Technology, electric car sales in China for passenger new energy vehicle (NEV) is expected to reach a 50% share by 2025. Such roadmaps are expected to raise a futuristic oppotunity for EV anode manufacturing too in China.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- A combination of supportive government policies and significant investment in battery production drives China's EV battery manufacturing, which, in turn, is expected to boost the demand for electric vehicle battery anodes. The government offers direct financial support, tax incentives, and subsidies, reducing manufacturers' costs and encouraging investment in advanced equipment. Manufacturers of electric vehicles in China benefit from government subsidies. For instance, all-electric plug-in cars boasting a range exceeding 400 km qualify for a subsidy of RMB 12,600 (around USD 2,000). Meanwhile, those ranging between 300 to 400 km receive a subsidy of RMB 9,100 (approximately USD 1,400).

- Further, the country's increasing demand for electric vehicles is fueling investment in electric vehicle battery manufacturing projects, thereby creating a potential need for electric vehicle battery anode materials. According to the International Energy Agency, in 2023, the demand for electric vehicle batteries in China accounted for 417 GWh, up from 314 GWh last year.

- Moreover, rising electric vehicle sales are motivating battery manufacturing companies to invest more in EV battery production, thereby creating demand for EV battery anode materials. According to the International Energy Agency, in 2023, the country's total EV car sales accounted for 8.1 million, higher than 5.9 million in 2022.

- In the future, the demand for EV battery anode materials is expected to increase as the country rushes towards manufacturing electric vehicles, and investments are expected to grow in EV battery manufacturing. For instance, in May 2024, China announced to invest 845 USD million to develop next-generation battery technology powering electricl vehicles. Such investments will boost the demand for electric vehicle battery manufacturing in the forecast period.

- Thus, supportive government policies and investments in battery manufacturing are expected to drive the market.

China Electric Vehicle Battery Anode Industry Overview

The China electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include Shanghai Shanshan Technology Co., Ltd., BTR New Material Group Co., Ltd., Jiangxi Zhengtuo New Energy Technology, Mitsubishi Chemical Group., and LG Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost for Anode Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Shanshan Technology Co., Ltd.

- 6.3.2 BTR New Material Group Co., Ltd.

- 6.3.3 Jiangxi Zhengtuo New Energy Technology

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Shanghai Putailai New Energy Technology

- 6.3.6 Targray Industries Inc.

- 6.3.7 Ningbo Shanshan Co., Ltd.

- 6.3.8 LG Chemical Group

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Resonac Holdings Corporation.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials

02-2729-4219

+886-2-2729-4219

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析 2025年全球正極材料市場報告

2025年全球正極材料市場報告 全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告

全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告 電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年)

電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年) 亞太地區電動汽車電池陽極:市場佔有率分析、產業趨勢與成長預測(2025-2030)東協電動車電池陽極:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區電動汽車電池陽極:市場佔有率分析、產業趨勢與成長預測(2025-2030)東協電動車電池陽極:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

▼