|

市場調查報告書

商品編碼

1636502

東協電動車電池陽極:市場佔有率分析、產業趨勢、成長預測(2025-2030)ASEAN Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

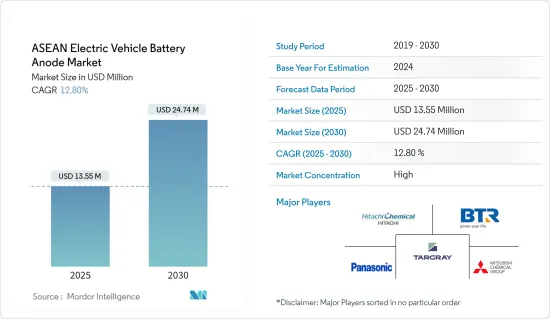

東協電動車電池陽極市場規模預計到2025年為1,355萬美元,預計2030年將達到2,474萬美元,預測期(2025-2030年)複合年成長率為12.8%。

主要亮點

- 未來幾年,由於電動車普及率提高、鋰離子電池原料成本下降以及政府支持政策等因素,東協電動車電池陽極市場預計將成長。

- 然而,原料蘊藏量有限和供應鏈差異等挑戰可能會阻礙市場擴張。

- 然而,隨著電池材料技術的進步和電動車雄心勃勃的長期目標,東協電動車電池陽極市場蘊藏著巨大的商機。

- 在東南亞國協中,印尼有望成為電動車電池陽極市場的主要企業。

東協電動車電池陽極市場趨勢

鋰離子電池領域佔市場主導地位

- 最初,東南亞的鋰離子電池產業主要針對消費性電子領域。這主要是因為該地區是大多數行業參與者和鋰離子電池必需礦物的所在地。然而,隨著時間的推移,發生了重大變化。電動車(EV)製造商已開始超越消費性電子產業,並超越鉛酸電池和其他電池類型,成為鋰離子電池的主要消費者。這項變化主要是由東南亞國協電動車銷量快速成長以及鋰離子電池及相關電動車電池陽極市場投資快速增加所推動的。

- 過去幾十年來,印尼、泰國、新加坡和越南等國家的鋰離子電池技術快速發展,特別是在汽車領域。鋰離子二次電池在東南亞國協越來越受歡迎,主要是由於其優越的容量重量比。此外,電動車中安裝的鋰電池不會排放氮氧化物、二氧化碳或其他溫室氣體,因此它們對環境的影響比傳統內燃機(ICE)汽車低得多。基於這一優勢,東南亞國協正在積極推動電動車的普及和當地電池負極製造市場的發展。

- 與2022年相比,2023年菲律賓和越南的乘用車銷量分別成長16.4%和2.8%。這對鋰離子電動車產業以及東協國家電動車電池陽極市場的參與者來說是個好兆頭。

- 2023年12月,泰國著名石油天然氣集團PTT開始生產鋰離子電池。這項舉措符合 PTT 為其電動車品牌 Neta 建立供應鏈並利用泰國不斷成長的綠色汽車市場的更廣泛策略。 PTT相關人員宣布,合資夥伴NV Gotion已在位於曼谷東南部的羅勇府建立了一條鋰離子電池生產線。該工廠目前的年產能為 2 吉瓦時,並計劃在不久的將來擴大到 8 吉瓦時。

- 2024 年 7 月,印尼慶祝首家鋰離子電動車電池工廠落成。作為東南亞最大的經濟體和全球最富有的鋰離子電池礦物生產,印尼在全球電動車供應鏈中具有戰略地位。該工廠是韓國巨頭 LG 能源解決方案公司 (LGES) 和現代汽車集團的合資企業,每年將生產 10 吉瓦時 (GWh) 的鋰離子電池。如此重大的發展對於東協電動車電池陽極市場的相關人員來說是個好兆頭。

- 泰國汽車研究所(TAI)的資料顯示,泰國電動車註冊數量大幅增加。 2023年登記車輛數量達17萬輛,較2022年的84,570輛大幅增加。考慮到這些車輛中超過 95% 由鋰離子技術動力來源,這一成長凸顯了鋰離子產業在泰國電動車電池陽極市場的主導地位。

- 總之,市場細分強烈表明鋰離子電池領域在電動車電池陽極市場中佔據主導地位。

印尼主導市場

- 印尼的目標是到 2030 年將二氧化碳排放減少 29%,相當於約 3.03 億噸。隨著人們對碳排放和對石化燃料的依賴日益關注,印尼將電動車 (EV) 的引入視為可行的解決方案。這一轉變將為該國的電動車電池陽極市場創造重大機會。

- 此外,印尼政府也積極鼓勵全球主要電動車製造商在該國投資。例如,2024年5月在峇里島舉行的世界水論壇上,印尼海洋事務和投資協調部長透露,特斯拉執行長正在向印尼政府提案建立電動車電池工廠。此舉預計將大大增強雅加達成為電動車負極材料生產主導者的雄心壯志。

- 2023 年 11 月,美國和印尼舉行了討論,重點討論建立關鍵礦物的夥伴關係,重點是電動車 (EV) 電池必需的金屬貿易。

- 2024 年 9 月,印尼外交部宣布打算擴大在生產電動車 (EV) 電池所需的關鍵礦物方面的合作,這次是與非洲國家。該部秘書長在印尼-非洲論壇(IAF)上發表演說時強調,不僅電動車電池,而且正極和負極等相關零件對關鍵礦物的需求龐大。該部也指出在鋰方面的積極合作,特別是與印尼礦業公司(MIND ID)和坦尚尼亞的合作。這些努力顯示印尼電動車電池陽極市場具有強勁的成長潛力。

- 根據聯合國COMTRADE資料顯示,儘管印尼是電池礦產豐富的國家,但其鋰離子電池進口量卻激增並保持在高位。 2023年,鋰離子電池進口額達2,759萬美元,略高於2022年的2,757萬美元。這項發展凸顯了印尼電動車產業對鋰離子電池的強勁需求,並突顯了印尼電動車電池陽極製造能力的快速成長。

- 2024年5月,澳洲席勒資源集團從莫三比克巴拉馬石墨礦運1萬噸精細天然石墨粉。該批貨物是為貝特瑞新能源材料位於印尼的新工廠出貨。印尼正在推進電動汽車電池生產和相關負極材料的基礎設施開發,這批貨物是繼 3 月試運的貨櫃之後出貨的。此舉不僅是席勒多元化策略的關鍵時刻,也鞏固了其在天然石墨和活性陽極材料(AAM)供應領域的全球領先地位。

- 從這些發展來看,印尼顯然正在東協電動車電池陽極市場站穩腳步。

東協電動車電池陽極產業概況

東協電動車電池陽極市場正在變得半固體。市場主要企業(排名不分先後)包括貝特瑞新材料集團、特銳科技國際有限公司、三菱化學集團、工業、Panasonic等。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 電動車的擴張

- 有利的政府政策

- 鋰離子電池價格下降

- 抑制因素

- 供應鏈缺口

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 依電池類型

- 鋰離子

- 鉛酸電池

- 其他技術

- 依材料類型

- 矽

- 石墨

- 鋰

- 其他材料

- 按地區

- 馬來西亞

- 印尼

- 泰國

- 越南

- 其他東南亞國協

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BTR New Material Group Co., Ltd

- Shenzhen Dynanonic Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Northern Graphite Corporation

- Panasonic Corporation

- Targray Technology International Inc.

- Epsilon Advanced Materials Pvt. Ltd.

- Volt14 Solutions Pte Ltd

- List of Other Prominent Companies

- Market Ranking/Share(%)Analysis

第7章 市場機會及未來趨勢

- 負極材料的持續研究和進展

簡介目錄

Product Code: 50003831

The ASEAN Electric Vehicle Battery Anode Market size is estimated at USD 13.55 million in 2025, and is expected to reach USD 24.74 million by 2030, at a CAGR of 12.8% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the ASEAN Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of Li-ion battery raw materials, and supportive government policies.

- However, challenges like limited raw material reserves and supply chain gaps may hinder the market's expansion.

- Yet, with ongoing technological advancements in battery materials and ambitious long-term targets for electric vehicles, significant opportunities await players in the ASEAN Electric Vehicle Battery Anode Market.

- Among the ASEAN nations, Indonesia is set to emerge as a leading player in the electric vehicle battery anode landscape.

ASEAN Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

- Initially, the lithium-ion battery industry in Southeast Asia primarily served the consumer electronics sector. This was largely due to the region being home to both a majority of industry players and the minerals essential for Li-ion batteries. However, a significant transformation occurred over time. Electric vehicle (EV) manufacturers began to eclipse the consumer electronics sector, emerging as the primary consumers of lithium-ion batteries, outpacing lead-acid and other battery types. This shift was predominantly fueled by surging EV sales in ASEAN countries and escalating investments in Li-ion batteries and the associated Electric Vehicle Battery Anode Market.

- In nations such as Indonesia, Thailand, Singapore, and Vietnam, the past few decades have seen a meteoric rise of lithium-ion battery technology, especially in the automotive sector. ASEAN nations are increasingly favoring lithium-ion rechargeable batteries, primarily due to their superior capacity-to-weight ratio. Furthermore, lithium batteries in EVs do not emit NOX, CO2, or any other greenhouse gases, resulting in a significantly lower environmental impact compared to conventional internal combustion engine (ICE) vehicles. Given this advantage, ASEAN nations are actively promoting EV adoption and the development of local battery anode manufacturing markets.

- Data from the Organisation Internationale des Constructeurs d'Automobiles highlights a positive trend: both the Philippines and Vietnam saw passenger vehicle sales grow by 16.4% and 2.8% respectively in 2023 compared to 2022. This bodes well for players in the Li-ion Electric Vehicle sector and, by extension, those in the Electric Vehicle Battery Anode Market across ASEAN countries.

- In December 2023, PTT, a prominent oil and gas conglomerate from Thailand, ventured into lithium-ion battery production. This initiative aligns with PTT's broader strategy to create a supply chain for its electric vehicle brand, Neta, and capitalize on Thailand's expanding green car market. PTT officials announced that their joint venture partner, NV Gotion, has established a lithium-ion battery production line in Rayong province, southeast of Bangkok. The facility currently boasts a production capacity of 2 gigawatt-hours per year, with ambitious plans to scale up to 8 gigawatt-hours in the near future, directly catering to the surging demand and subsequently fueling the nation's EV Battery Anode Market.

- In July 2024, Indonesia celebrated the inauguration of its first Li-ion EV battery plant. As the largest economy in Southeast Asia and home to the world's richest Li-ion battery minerals, Indonesia is strategically positioning itself in the global electric vehicle supply chain. This plant, a joint venture between South Korean titans LG Energy Solution (LGES) and Hyundai Motor Group, is set to produce a staggering 10 Gigawatt hours (GWh) of Li-ion battery cells annually. Such a significant development augurs well for stakeholders in the ASEAN Electric Vehicle Battery Anode Market.

- Data from the Thailand Automotive Institute (TAI) reveals a remarkable surge in electric vehicle registrations in Thailand. In 2023, registrations reached 170,000, a significant jump from 84,570 in 2022. Given that over 95% of these vehicles are powered by Li-ion technology, this growth underscores the dominance of the Li-ion segment in Thailand's Electric Vehicle Battery Anode Market.

- In conclusion, the evidence strongly indicates that the lithium-ion battery segment is poised to dominate the ASEAN Electric Vehicle Battery Anode Market.

Indonesia to Dominate the Market

- Indonesia aims to cut CO2 emissions by 29%, equating to approximately 303 million tons, by the year 2030. With rising concerns over carbon emissions and reliance on fossil fuels, Indonesia views the introduction of electric vehicles (EVs) as a viable solution. This shift is poised to unlock substantial opportunities for the Electric Vehicle Battery Anode Market in the nation.

- Moreover, the Indonesian government is actively courting major global EV players to invest domestically. For instance, in May 2024, at the World Water Forum in Bali, Indonesia's coordinating minister for maritime affairs and investment revealed that Tesla's CEO is contemplating a proposal from the Indonesian government to set up an EV battery plant in the nation. This move would significantly bolster Jakarta's ambition to emerge as a dominant player in EV anode production.

- In November 2023, discussions between the U.S. and Indonesia centered on forging a partnership focused on critical minerals, with an emphasis on trading metals essential for electric vehicle (EV) batteries.

- In September 2024, the Indonesian Foreign Affairs Ministry expressed its intent to expand collaborations on critical minerals for EV battery production, this time engaging with African nations. At the Indonesia-Africa Forum (IAF), the ministry's Director General underscored Indonesia's vast demand for critical minerals, not only for EV batteries but also for related components like cathodes and anodes. The ministry also pointed out an active collaboration in lithium, especially between Mining Industry Indonesia (MIND ID) and Tanzania. These endeavors hint at a robust growth potential for Indonesia's Electric Vehicle Battery Anode Market.

- Data from the United Nations COMTRADE reveals that even as a nation rich in battery minerals, Indonesia's imports of Li-ion batteries have surged and remained elevated. In 2023, the value of imported Li-ion batteries reached USD 27.59 million, a slight uptick from USD 27.57 million in 2022. This trend underscores a strong demand for Li-ion batteries in Indonesia's EV sector and highlights the nation's burgeoning capacity for Electric Vehicle Battery Anode manufacturing.

- In May 2024, Australia's Syrah Resources Group dispatched 10,000 metric tons of natural graphite fines from its Balama graphite operation in Mozambique. The shipment was destined for BTR New Energy Materials' new plant in Indonesia. As Indonesia ramps up its infrastructure for EV battery production and associated anode materials, this shipment follows a trial container sent in March. This move not only marks a pivotal moment in Syrah's diversification strategy but also cements its position as a global leader in supplying natural graphite and active anode materials (AAM).

- Given these developments, it's evident that Indonesia is solidifying its foothold in the ASEAN Electric Vehicle Battery Anode Market.

ASEAN Electric Vehicle Battery Anode Industry Overview

The ASEAN Electric Vehicle Battery Anode Market is semi-consolidated. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Targray Technology International Inc., Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, and Panasonic Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Favorable Government Policies

- 4.5.1.3 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other technology

- 5.2 By Material Type

- 5.2.1 Silicon

- 5.2.2 Graphite

- 5.2.3 Lithium

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 Malaysia

- 5.3.2 Indonesia

- 5.3.3 Thailand

- 5.3.4 Vietnam

- 5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BTR New Material Group Co., Ltd

- 6.3.2 Shenzhen Dynanonic Co., Ltd.

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Hitachi Chemical Company Ltd

- 6.3.5 Northern Graphite Corporation

- 6.3.6 Panasonic Corporation

- 6.3.7 Targray Technology International Inc.

- 6.3.8 Epsilon Advanced Materials Pvt. Ltd.

- 6.3.9 Volt14 Solutions Pte Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Anode Material

02-2729-4219

+886-2-2729-4219

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析 2025年全球正極材料市場報告

2025年全球正極材料市場報告 全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告

全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告 電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年)

電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年) 中國電動汽車電池陽極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)亞太地區電動汽車電池陽極:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

中國電動汽車電池陽極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)亞太地區電動汽車電池陽極:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

▼