|

市場調查報告書

商品編碼

1636507

亞太地區電動汽車電池陽極:市場佔有率分析、產業趨勢與成長預測(2025-2030)Asia Pacific Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

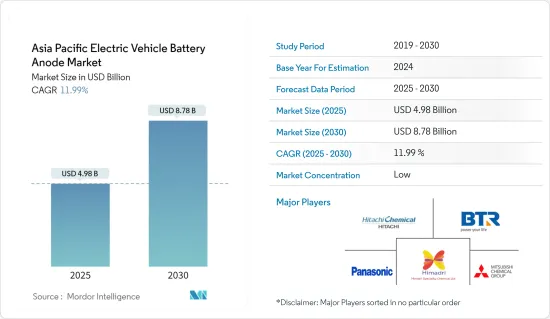

預計2025年亞太地區電動車電池負極市場規模為49.8億美元,2030年預計將達87.8億美元,預測期內(2025-2030年)複合年成長率為11.99%。

主要亮點

- 未來幾年,由於電動車採用率增加、電池原料成本下降(導致鋰離子電池價格下降)以及政府支持措施等因素,亞太電動汽車電池陽極市場預計將成長.

- 相反,蘊藏量有限和供應鏈缺口等挑戰可能會阻礙市場擴張。

- 然而,電池陽極技術的進步和雄心勃勃的長期電動車目標為市場參與企業提供了重大機會。

- 在亞太地區的主要參與企業中,印度脫穎而出,成為電動車電池負極市場成長顯著的國家。

亞太地區電動汽車電池負極市場趨勢

鋰離子電池領域佔市場主導地位

- 在鋰離子電池產業發展初期,鋰電池的主要市場是家用電子電器產品。然而,隨著歲月的流逝,發生了明顯的變化。在亞太地區電動車銷量激增的推動下,電動車 (EV) 製造商已成為鋰離子電池的主要消費者。

- 過去十年,亞太地區鋰離子電池的使用量激增,尤其是在汽車領域。在中國、印度、日本和印尼等國家,鋰離子二次電池因其優越的容量重量比而越來越受歡迎。此外,電動車中使用的鋰電池不會排放氮氧化物、二氧化碳或其他溫室氣體,因此它們對環境的影響比傳統內燃機(ICE)汽車低得多。認知到這一優勢,許多國家正在推動電動車的採用,並透過補貼和政府舉措鼓勵電動車電池負極市場的發展。

- 2023年5月,電動車電池正負極市場知名品牌Himadri Specialty Chemical Ltd.宣布對Sicona Battery Technologies Pty Ltd.進行1032萬澳元戰略投資,獲得其12.79%股權我做到了。總部位於雪梨的 Sicona 為鋰離子 (Li-ion) 電池的陽極(負極)提供必要的技術,為移動出行領域和可再生能源儲存做出了貢獻。

- 隨著電動車越來越普及,鋰離子電池正極市場可望顯著成長。此外,負極技術的進步將進一步推動這一市場的擴張。

- 根據國際能源總署(IEA)預測,2023年中國電池式電動車銷量將達540萬輛,其中95%以上依賴鋰離子電池技術,與前一年同期比較去年同期成長22.7%。考慮到純電動車領域的強勁成長,鋰離子電池因其獨特的優勢預計將在亞太電動車電池負極市場佔據重要佔有率。

- 2024年8月,貝特瑞新材料集團在印尼的鋰離子電池負極材料新廠開始運作。該公司表示,一旦全面擴建,該工廠將成為其在中國以外最大的負極材料生產基地。第一期建設投資4.78億美元,預計形成年產8萬噸負極材料的生產能力。第二階段將於 2024年終開始,將追加投資 2.99 億美元,以使該工廠的產量多樣化,並為電動車、家用電子電器電池和能源儲存系統。這些策略舉措凸顯了電動車鋰離子電池在亞太電動汽車電池負極市場中日益成長的主導地位。

- 鑑於鋰離子電池領域的這些進步,亞太地區電動車電池陽極材料市場預計在未來幾年將大幅成長。

印度主導亞太市場

- 作為《巴黎協定》和聯合國永續發展目標的一部分,印度政府正在全球平台上致力於減少溫室氣體排放。為了促進電動車 (EV) 的普及並將印度定位為全球電動車電池製造中心,政府為電動車電池和相關陽極市場的參與企業提供了回扣、獎勵和進口優惠。

- 2024 年 3 月 15 日,印度政府核准了電動車製造計畫(SMEC)。該計劃為新建待開發區車製造工廠的汽車製造商提供進口關稅優惠。根據該計劃,製造商每年可以在五年內以 15% 的減稅稅率進口最多 8,000 輛電動車。此激勵措施的條件是在獲得批准後三年內建立國內生產能力。因此,這些發展支持了電動車鋰離子電池技術的崛起,並直接刺激了印度陽極材料的成長。

- 憑藉其巨大的潛力和政府的大力支持,印度正在成為瞄準電動車市場的公司首選的製造地。例如,2024年9月,Epsilon Advanced Materials宣布計畫在美國和印度建立工廠,年產能各為3萬噸。這些工廠將成為中國以外最大的負極材料生產工廠,標誌著印度首次成為電動車電池負極材料的大型供應商。

- 2024 年 9 月,主要企業Epsilon Advanced Materials 宣布有意在卡納塔克邦建立最先進的電動車電池陽極製造工廠。計畫投資900億印度盧比(約106億美元),年產能目標為9萬噸。投資策略將分兩個階段製定。根據Epsilon集團執行董事詳細介紹,初始投資將為400億印度盧比(約47億美元),隨後追加投資500億印度盧比(約美元)。

- 2024 年 1 月,HEG Limited 的子公司、LNJ Bhilwara 集團旗下的 Advanced Carbons Company (TACC) 在中央邦 Dewas 區 Sarsoda 村推出了石墨陽極製造工廠。該公司於 2022 年在這個待開發區計劃上投資了約 1850 億印度盧比(約 21 億美元)。該工廠佔地 100 英畝,每年將生產 20,000 噸陽極材料,以滿足快速成長的能源儲存和移動需求。

- 印度政府指出,2023年電動車(EV)電池組的平均價格較前一年大幅下降13%至139美元/kWh。隨著技術進步和製造效率提高,電池組價格預計將進一步下降,2025年降至113美元/kWh,2030年降至80美元/kWh。這些趨勢支撐了印度鋰離子電動車電池負極市場日益成長的重要性。

- 透過開發這些新興市場,印度預計在未來幾年內確立在鋰離子電池負極市場的主導地位。

亞太電動車負極產業概況

亞太地區電動車電池負極市場適度細分。市場主要企業(排名不分先後)包括BTR新材料集團、Himadri Specialty Chemical Ltd.、Hitachi Chemical Company Ltd.、Panasonic Holdings Corporation、Epsilon Advanced Materials Pvt. Ltd.等。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車的擴張

- 政府有利措施

- 鋰離子電池價格下降

- 抑制因素

- 供應鏈缺口

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 依電池類型

- 鋰離子

- 鉛酸電池

- 其他

- 依材料類型

- 矽

- 石墨

- 鋰

- 其他

- 按地區

- 中國

- 印度

- 日本

- 馬來西亞

- 印尼

- 泰國

- 越南

- 其他亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BTR New Material Group Co., Ltd

- Shenzhen Dynanonic Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Northern Graphite Corporation

- Panasonic Corporation

- Targray Technology International Inc.

- Epsilon Advanced Materials Pvt. Ltd.

- Himadri Speciality Chemical Ltd

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 負極材料的持續研究和進展

The Asia Pacific Electric Vehicle Battery Anode Market size is estimated at USD 4.98 billion in 2025, and is expected to reach USD 8.78 billion by 2030, at a CAGR of 11.99% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the Asia Pacific Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of battery raw materials (leading to lower prices for Li-ion batteries), and supportive government policies.

- Conversely, challenges like limited raw material reserves and gaps in the supply chain may hinder the market's expansion.

- However, advancements in battery anode technologies and ambitious long-term electric vehicle targets present significant opportunities for market players.

- Among the key players in the Asia-Pacific region, India stands out as a country poised for notable growth in the electric vehicle battery anode market.

Asia Pacific Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

- In the early decades of the lithium-ion battery industry, the primary market for lithium batteries was consumer electronics. However, over the years, a notable shift took place. Electric vehicle (EV) manufacturers emerged as the leading consumers of lithium-ion batteries, driven by surging EV sales in the Asia-Pacific region.

- Over the past decade, the Asia-Pacific has seen a meteoric rise in the adoption of lithium-ion batteries, especially in the automotive sector. Countries like China, India, Japan, and Indonesia are increasingly favoring lithium-ion rechargeable batteries due to their superior capacity-to-weight ratio. Moreover, lithium batteries used in EVs do not emit NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing this advantage, numerous countries are promoting EV adoption and fostering the development of the Electric Vehicle Battery anode Market through subsidies and government initiatives.

- In May 2023, Himadri Speciality Chemical Ltd., a prominent player in the EV Battery Cathode and Anode market, announced a strategic investment of AUD 10.32 million in Sicona Battery Technologies Pty Ltd, securing a 12.79 percent stake. Sicona, based in Sydney, offers technology crucial for the anodes (negative electrodes) of lithium-ion (Li-ion) batteries, serving both the mobility sector and renewable energy storage.

- As electric vehicle adoption continues to rise, the lithium-ion battery cathode market is poised for substantial growth. Additionally, advancements in anode technologies are set to further propel this market expansion.

- According to the International Energy Agency (IEA), battery electric vehicle sales in China hit 5.4 million in 2023, with over 95% relying on Li-ion battery technology, marking a 22.7% increase from the previous year. Given this robust growth in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are projected to capture a significant share of the Asia-Pacific Electric Vehicle Battery Anode Market.

- In August 2024, BTR New Material Group inaugurated its new anode materials plant for lithium-ion batteries in Indonesia. The company claims that, once fully expanded, this facility will be the largest anode production site outside of China. The first construction phase, supported by a USD 478 million investment, is designed for an annual production capacity of 80,000 tons of anode material. A second phase, commencing at the end of 2024 with an additional USD 299 million investment, aims to diversify the facility's output, supplying anode materials for electric vehicles, appliance batteries, and energy storage systems. Such strategic moves underscore the growing dominance of EV Li-ion batteries in the Asia-Pacific EV Battery Anode Market.

- Given these advancements in the lithium-ion battery sector, the market for anode materials in the Asia-Pacific region's electric vehicle battery market is set for significant growth in the coming years.

India to Dominate the Market in Asia Pacific

- As part of the Paris Agreement and the United Nations SDGs, the Government of India has committed to reducing GHG emissions on global platforms. To bolster the adoption of Electric Vehicles (EVs) and position India as a global hub for EV battery manufacturing, the government has introduced rebates, incentives, and import concessions for players in the electric vehicle batteries and associated anode markets.

- On March 15, 2024, the Indian government approved the Scheme for Manufacturing of Electric Cars (SMEC). This initiative offers concessional import duties to automakers establishing new greenfield electric vehicle manufacturing plants. Under the scheme, manufacturers can import up to 8,000 EVs annually at a reduced duty of 15% for five years. This concession is granted on the condition that they establish domestic production capabilities within three years of receiving approval. Consequently, these developments are bolstering the rise of Li-ion battery technology for EVs, directly fueling the growth of anode materials in India.

- Given its vast potential and robust government backing, India is emerging as a prime manufacturing hub for companies eyeing the electric vehicle market. For instance, in September 2024, Epsilon Advanced Materials announced plans to set up two plants, each boasting a capacity of 30,000 tonnes per annum-one in the United States and the other in India. These facilities are poised to be the largest producers of anode material outside of China, marking India's debut as a large-scale supplier of electric vehicle battery anode material.

- In September 2024, Epsilon Advanced Materials, a key player in battery materials, disclosed its intent to set up another cutting-edge EV battery anode material manufacturing unit in Karnataka. With a projected investment of INR 9,000 crore (~USD 10.6 billion), the facility targets an annual production capacity of 90,000 tonnes. The investment strategy unfolds in two phases: an initial INR 4,000 crore (~USD 4.7 billion) infusion, followed by an additional INR 5,000 crore (~USD 5.9 billion) in the second phase, as detailed by Epsilon Group's Managing Director.

- In January 2024, the Advanced Carbons Company (TACC), a HEG Limited subsidiary and part of the LNJ Bhilwara group, launched its graphite anode manufacturing unit in Sirsoda village, Dewas district, Madhya Pradesh. The company had earmarked approximately INR 1850 crores (~USD 2.1 billion) for this greenfield project back in 2022. Spread over 100 acres, the facility is poised to churn out 20,000 metric tonnes of anode material annually, meeting the surging demands of energy storage and mobility.

- In 2023, the Government of India noted a significant 13% drop in average battery pack prices for electric vehicles (EVs), bringing them down to USD 139/kWh from the previous year. With ongoing technological advancements and enhanced manufacturing efficiencies, projections indicate a further decline in battery pack prices, forecasting USD 113/kWh by 2025 and an ambitious drop to USD 80/kWh by 2030. Such trends underscore the growing significance of the Lithium-ion Electric Vehicle Battery Anode Market in India.

- Given these developments, India is poised to emerge as a dominant player in the studied market in the coming years.

Asia Pacific Electric Vehicle Battery Anode Industry Overview

The Asia Pacific Electric Vehicle Battery Anode Market is moderately fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Himadri Speciality Chemical Ltd., Hitachi Chemical Company Ltd, Panasonic Holdings Corporation, and Epsilon Advanced Materials Pvt. Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Favorable Government Policies

- 4.5.1.3 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Battery type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other Technologies

- 5.2 By Material Type

- 5.2.1 Silicon

- 5.2.2 Graphite

- 5.2.3 Lithium

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Malaysia

- 5.3.5 Indonesia

- 5.3.6 Thailand

- 5.3.7 Vietnam

- 5.3.8 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BTR New Material Group Co., Ltd

- 6.3.2 Shenzhen Dynanonic Co., Ltd.

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Hitachi Chemical Company Ltd

- 6.3.5 Northern Graphite Corporation

- 6.3.6 Panasonic Corporation

- 6.3.7 Targray Technology International Inc.

- 6.3.8 Epsilon Advanced Materials Pvt. Ltd.

- 6.3.9 Himadri Speciality Chemical Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Anode Material

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析

硬碳陽極前驅體市場報告:至2031年的趨勢、預測與競爭分析 2025年全球正極材料市場報告

2025年全球正極材料市場報告 全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告

全球下一代陽極材料市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年2025 年電池材料全球市場報告 電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年)

電池材料市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032 年) 中國電動汽車電池陽極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)東協電動車電池陽極:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

中國電動汽車電池陽極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)東協電動車電池陽極:市場佔有率分析、產業趨勢、成長預測(2025-2030)歐洲電動車電池負極:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)美國電動汽車電池負極:市場佔有率分析、產業趨勢及成長預測(2025-2030)義大利電動汽車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)