|

市場調查報告書

商品編碼

1637849

中東和非洲的無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Middle East And Africa Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

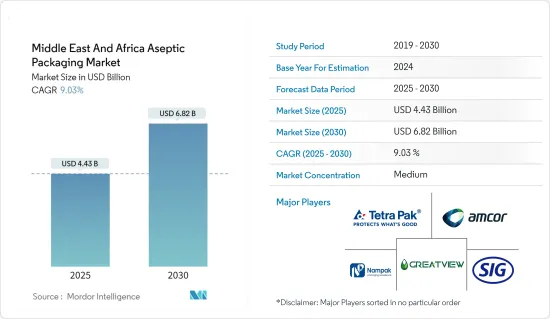

中東和非洲無菌包裝市場規模預計在 2025 年為 44.3 億美元,預計到 2030 年將達到 68.2 億美元,預測期內(2025-2030 年)的複合年成長率為 9.03%。

主要亮點

- 無菌包裝市場的主要成長動力是包裝材料滿足持續高產品品質和營養保留的需求的能力。它還可以避免其他包裝類型(如罐頭內襯)中經常出現的雙酚 A (BPA) 爭議。無菌包裝滿足了所有這些要求,並且可以在不冷藏的情況下將某些產品的保存期限延長約 6 至 12 個月。

- 快速都市化和消費品多樣化是推動無菌包裝發展的主要因素。對加工食品和一次性醫療用品的需求不斷成長也推動了該地區採用無菌包裝。

- 人們生活方式的改變導致了從家庭烹飪到已烹調產品的轉變。這些生活方式的改變以及由此導致的消費者對加工、包裝和已調理食品的依賴正在推動對無菌紙盒包裝解決方案的需求。超級市場文化的出現也改變了購物格局,增加了包裝的需求,特別是食品和飲料的包裝。

- 無菌包裝減少了產品中添加防腐劑的需要,在那些轉向天然、無防腐劑產品的消費者中越來越受歡迎。無菌包裝也有助於降低運輸和配送成本,因為在運輸和配送過程中它不需要冷藏,環境也更為寬鬆。

- 區域無菌包裝市場正處於起步階段。然而,對健康和產品保存期限的日益關注是影響該地區成長的主要因素之一。

中東和非洲無菌包裝市場的趨勢

擴大採用無菌紙盒包裝來延長產品保存期限

- 消費者正在尋找保存期限更長、使用效率更高的產品。這迫使企業想出替代傳統包裝的包裝解決方案。對於希望在不依賴複雜冷藏鏈的情況下擴大產品供應的公司來說,生產保存期限更長的包裝變得至關重要。

- 透過保護產品免受氧氣、濕氣和微生物等潛在劣化因素的影響,可以延長保存期限。公司需要具有成本效益的包裝解決方案來實現相同的目標。減少整個食品供應鏈中的浪費對於減少農業對環境的影響和滿足日益成長的糧食需求至關重要。投資高效、低成本和永續的加工和包裝解決方案來延長產品保存期限是一個可行的解決方案,從而推動了對無菌紙盒包裝的需求。

- 食品包裝不再只是起到保護食品和銷售食品的被動作用。減少防腐劑的重視也是無菌包裝的促進因素之一。無菌食品儲藏可使加工食品在打開紙箱之前無需添加防腐劑就能保存更長時間。

- 隨著非洲財富的不斷成長導致飲食習慣的改變,乳製品產業有望蓬勃發展。 IFCN酪農研究網估計,到2030年,乳品消費量將增加三分之一以上,而為滿足需求,起司和奶油的進口量預計將增加一倍以上。此外,聯合利華、雀巢和帝亞吉歐等全球巨頭都在非洲擴大業務,以利用人口激增、中產階級不斷壯大以及拉各斯、開羅和約翰內斯堡等城市日益都市化。

- 根據沙烏地阿拉伯統計總局的數據,2020 年沙烏地阿拉伯食品和飲料服務市場創造了約 144.6 億美元的銷售額。預計到 2025 年這一金額將達到約 1,603 萬美元。這種成長表明包裝食品和飲料的消費量可能會激增,這可能對無菌紙盒包裝產生積極影響。

預測期內,醫藥和醫療保健領域預計將大幅成長

- 預灌封注射器克服了非腸道給藥方式缺乏便利性、價格、準確性、無菌性和安全性等缺點。這些注射器可以更容易管理糖尿病和類風濕性關節炎等慢性疾病,從而在預測期內增加自動注射器和筆式注射器的使用量。預計預測期內中東和非洲糖尿病和其他慢性病盛行率的不斷上升將導致市場需求增加。

- 隨著製藥業尋求新的、更便捷的藥物輸送方法,預填充式注射器成為快速成長的單位劑量分配選擇。它還使製藥公司能夠最大限度地減少藥物浪費,延長產品壽命,並允許患者在家中而不是在醫院自行注射藥物。

- 大約80%的管瓶和安瓿瓶都是由玻璃製成的,因為它們適用於多種藥物組合,但它們面臨剝落和破損等挑戰。環狀烯烴聚合物(COP)和環狀烯烴共聚物(COC)等替代塑膠管瓶預計將在未來五年內獲得顯著的市場佔有率。 Schott AG 和 Amcor Group GmbH 等領先公司在製藥應用的 COC 方面擁有專業知識。這些發展推動了該地區對無菌包裝的需求。

- 此外,根據國際糖尿病聯盟中東和北非地區預測,2021年約有7,300萬人(20-79歲)將罹患糖尿病,到2045年將有1.36億成年人罹患糖尿病。 2021年至2045年間,非洲20至79歲糖尿病患者數量預計將增加134%。同時,中東和非洲預計將出現87%的激增。因此,胰島素產業的成長有望推動預灌封注射器市場的發展,並進一步促進無菌包裝市場的發展。

中東和非洲無菌包裝產業概況

中東和非洲的無菌包裝市場已呈現半固體,已有多家本地和國際供應商進入該市場。市場的主要參與者包括 Tetra Pak International SA、Amcor Group GmbH、SIG Group AG、Mondi PLC、Nampak Ltd、Greatview Aseptic Packaging Company 和 International Aseptic Paperboard Mfg LLC。參與者採用產品創新、併購等各種策略,主要是為了擴大影響力並保持競爭優勢。

- 2023年11月,領先的無菌包裝系統和解決方案供應商SIG Group AG宣佈為阿拉伯聯合大公國的餐飲業領導者和新興企業推出一款灌裝機。 SIG SmileSmall 24 無菌填充機和 SIG CleanPouch 25 無菌填充機可在位於杜拜矽谷的 SIG 技術中心購買。這些灌裝機為食品和飲料創新者提供了一系列好處和可能性,包括產品測試和創新、性能、容量靈活性和 SIG 的 Drinksplus 功能。

- 2023 年 11 月,利樂國際公司 (Tetra Pak International SA) 與食品製造商 Lactogal 合作推出了“Tetra Brik 200 Slim Leaf”,這是一款帶有紙質屏障的無菌紙盒。為了將包裝中可再生材料的使用率提高到90%,紙箱由大約80%的紙板製成。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 技術簡介

- 評估地緣政治情勢對產業的影響

第5章 市場動態

- 市場促進因素

- 低溫運輸物流成本降低需求日益增加

- 長期產品儲存需求快速成長

- 市場挑戰

- 環境和回收問題

- 製造複雜性增加(例如原料成本上升)和投資回報率降低

第6章 市場細分

- 按包裝材質

- 金屬

- 玻璃

- 紙和紙板

- 塑膠

- 其他包裝材料

- 按包裝類型

- 紙盒

- 袋子和小袋

- 杯子和托盤

- 瓶子和罐子

- 能

- 其他包裝類型

- 按最終用戶產業

- 食物

- 飲料

- 製藥和醫療

- 其他最終用戶產業

- 按國家

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第7章 競爭格局

- 公司簡介

- Tetra Pak International SA

- Amcor Group GmbH

- Nampak Ltd

- DS Smith PLC

- SIG Group AG

- Uflex Limited

- Mondi PLC

- Greatview Aseptic Packaging Company

- International Aseptic Paperboard Mfg. LLC

- Smurfit Kappa Group PLC

第8章投資分析

第9章:市場的未來

The Middle East And Africa Aseptic Packaging Market size is estimated at USD 4.43 billion in 2025, and is expected to reach USD 6.82 billion by 2030, at a CAGR of 9.03% during the forecast period (2025-2030).

Key Highlights

- The main growth drivers in the aseptic packaging market are the packaging material's ability to meet the demands for high, consistent product quality and nutrient retention. Also, the capacity to avoid the bisphenol A (BPA) controversy is frequently found in other packaging types, such as can liners. Aseptic packaging has met all these requirements and extends the shelf life of some products by an estimated six to twelve months without refrigeration.

- Rapid urbanization and the variety of consumer goods are key factors promoting the development of aseptic packaging. The rising demand for processed foods and disposable medical supplies also drives the adoption of aseptic packaging in the region.

- The altering lifestyles of people have resulted in the shift from home-cooked to ready-to-eat products. These lifestyle changes and consumers' consequent dependence on processed, packaged, and pre-cooked food are increasing the demand for aseptic carton packaging solutions. The advent of supermarket culture has also altered the shopping landscape and increased the need for packaging, especially in food and beverage products.

- Aseptic packaging reduces the need to add preservatives to the product, which is gaining attention among consumers who are focusing on natural and no-preservative products. Also, aseptic packaging helps reduce shipping and distribution costs by eliminating the need for refrigerated, more relaxed environments during shipping and distribution.

- The regional aseptic packaging market is in its early stages. However, increasing concerns regarding health and product shelf life are some of the major factors affecting its growth in the region.

Middle East And Africa Aseptic Packaging Market Trends

Increasing Adoption of Aseptic Carton Packaging to Increase the Shelf-life of Products

- Consumers have been demanding products with a longer shelf life and more efficient usage. This has necessitated the companies to devise alternative packaging solutions to traditional packaging. With companies seeking to expand their product offerings with less dependence on sophisticated cold storage chains, producing packages that provide longer shelf life has become crucial.

- Protecting products from potential deteriorating agents, such as oxygen, moisture, and microbes, can increase shelf life. Companies need a cost-effective packaging solution to achieve the same. Reducing wastage throughout the food supply chain is likely a crucial activity to reduce the environmental impact of agriculture and serve the increasing food demand. Investing in efficient, low-cost, and sustainable processing and packaging solutions to increase product shelf life is a viable solution, thus increasing the demand for aseptic carton packaging.

- Food packaging is no longer just a passive role in protecting and marketing a food product. The emphasis on decreasing preservatives is also a driving factor for aseptic packaging, as aseptic food preservation methods enable processed food to be kept longer without preservatives until the carton is opened.

- The dairy industry is expected to prosper as Africa's growing wealth translates to evolving diets. The IFCN Dairy Research Network estimates intake will increase by more than a third by 2030, in which time imports of cheese and butter are expected to more than double to meet that demand. Furthermore, global giants like Unilever, Nestle, and Diageo are all running massive operations across Africa as they seek to capitalize on surging population growth, a rising middle class, and increasing urbanization in cities such as Lagos, Cairo, and Johannesburg.

- According to the General Authority for Statistics, the revenue of the food and beverage service activities market in Saudi Arabia was worth about USD 14.46 billion in 2020. This amount is anticipated to reach around USD 16.03 million in 2025. This growth indicates a potential surge in the consumption of packaged foods and beverages, which can positively impact aseptic carton packaging.

The Pharmaceutical and Medical Segment is Expected to Witness Significant Growth During the Forecast Period

- Prefillable syringes overcome the disadvantages of parenteral drug delivery, such as lack of convenience, affordability, accuracy, sterility, and safety. These syringes enable easy management of chronic diseases, such as diabetes and rheumatoid arthritis, thereby increasing the use of auto-injectors and pen injectors over the forecast period. The growing prevalence of diabetes and other chronic diseases in the Middle East and Africa is expected to lead to market demand over the forecast period.

- Prefilled syringes are emerging as one of the fastest-growing choices for unit-dose medication as the pharmaceutical industry seeks new and more convenient drug delivery methods. Also, pharmaceutical companies minimize drug waste and increase product life span, while patients can self-administer injectable drugs in their homes instead of the hospital.

- Around 80% of the vials and ampoules are made from glass, owing to their suitability with varied drug combinations, but they face challenges like delamination, breakage, etc. Alternative plastic vials, like cycle olefin polymer (COP) and cycle olefin copolymer (COC) formats, are expected to gain significant market share over the next five years. Major players such as Schott AG and Amcor Group GmbH possess expertise in COC for pharmaceutical applications. Such developments are driving the need for aseptic packaging in the region.

- Furthermore, according to the International Diabetes Federation in the Middle East and North Africa, in 2021, around 73 million people (20-79) had diabetes, and it is projected that 136 million adults will have diabetes by 2045. People with diabetes are expected to grow by 134% in Africa among those aged 20 to 79 between 2021 and 2045. At the same time, there is projected to be an 87% surge across the Middle East and Africa. Thus, the growing insulin industry is expected to drive the prefillable syringes market, which would further aid the development of the aseptic packaging market.

Middle East And Africa Aseptic Packaging Industry Overview

The Middle East and Africa aseptic packaging market is semi-consolidated, as a few domestic and international vendors operate in the market. Some of the major players in the market include Tetra Pak International SA, Amcor Group GmbH, SIG Group AG, Mondi PLC, Nampak Ltd, Greatview Aseptic Packaging Company, and International Aseptic Paperboard Mfg LLC. Players are adopting various strategies, such as product innovation, mergers, and acquisitions, primarily to expand their reach and stay competitive.

- In November 2023, SIG Group AG, a leading systems and solutions provider for aseptic packaging, announced the launch of filling machines for F&B leaders and startups in the United Arab Emirates. The SIG SmileSmall 24 Aseptic and SIG CleanPouch 25 Aseptic filling machines are available in SIG's Technology Center at Dubai Silicon Oasis. They offer F&B innovators various benefits and possibilities for product testing and innovation, performance, volume flexibility, and SIG's Drinksplus capability.

- In November 2023, Tetra Pak International SA launched the Tetra Brik 200 Slim Leaf aseptic carton, which contains paper-based barriers, in collaboration with food products producer Lactogal. To increase the use of renewable content in the packaging to 90%, the carton is made from approximately 80% paperboard.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Assessment of the Geopolitical Scenario's Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand to Reduce Cost of Cold Chain Logistics

- 5.1.2 Surge in Need for Longer Shelf Life of Products

- 5.2 Market Challenges

- 5.2.1 Concerns over Environment Problems and Recycling

- 5.2.2 Manufacturing Complications (For Example Increasing Cost of Raw Materials) and Lower ROI

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Metal

- 6.1.2 Glass

- 6.1.3 Paper & Paperboard

- 6.1.4 Plastics

- 6.1.5 Other Packaging Material

- 6.2 By Packaging Type

- 6.2.1 Cartons

- 6.2.2 Bags and Pouches

- 6.2.3 Cups and Trays

- 6.2.4 Bottles and Jars

- 6.2.5 Cans

- 6.2.6 Other Packaging Type

- 6.3 By End-User Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Other End-User Industries

- 6.4 By Country

- 6.4.1 Saudi Arabia

- 6.4.2 South Africa

- 6.4.3 United Arab Emirates

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tetra Pak International SA

- 7.1.2 Amcor Group GmbH

- 7.1.3 Nampak Ltd

- 7.1.4 DS Smith PLC

- 7.1.5 SIG Group AG

- 7.1.6 Uflex Limited

- 7.1.7 Mondi PLC

- 7.1.8 Greatview Aseptic Packaging Company

- 7.1.9 International Aseptic Paperboard Mfg. LLC

- 7.1.10 Smurfit Kappa Group PLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球無菌包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

全球無菌包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 2025年無菌包裝全球市場報告

2025年無菌包裝全球市場報告 滅菌包裝市場:按包裝類型、材料、應用和地區分類醫療植入無菌包裝市場:依產品類型、依材料類型、依應用、按地區亞太無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲的無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

滅菌包裝市場:按包裝類型、材料、應用和地區分類醫療植入無菌包裝市場:依產品類型、依材料類型、依應用、按地區亞太無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲的無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 無菌包裝市場報告:趨勢、預測和競爭分析(至 2030 年)2030 年乳製品無菌包裝市場預測:按產品類型、材料、技術、應用和地區進行的全球分析

無菌包裝市場報告:趨勢、預測和競爭分析(至 2030 年)2030 年乳製品無菌包裝市場預測:按產品類型、材料、技術、應用和地區進行的全球分析