|

市場調查報告書

商品編碼

1639465

泰國石油和天然氣下游市場 -市場佔有率分析、行業趨勢、成長預測(2025-2030)Thailand Oil and Gas Downstream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

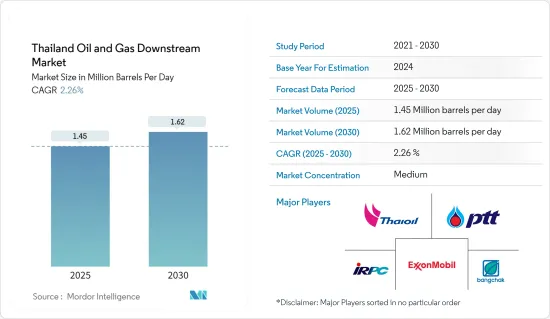

泰國石油和天然氣下游市場規模預計2025年為145萬桶/日,預計2030年將達到162萬桶/日,預測期間(2025-2030年)複合年成長率為2.26%。

受訪的市場在 2020 年受到了 COVID-19 的負面影響,但現在已恢復並達到疫情前的水平。隨著各種精製產品的需求不斷成長,該國正在重點發展煉油產能,預計這將在預測期內推動所研究市場的成長。然而,清潔替代能源的趨勢,例如電動車的日益普及,預計將阻礙最終用戶行業對精製油的需求並抑制市場成長。

安達曼海發現了天然氣田,這讓人們對減少對進口天然氣的依賴和天然氣運輸成本的樂觀增加。這一因素為這一領域的參與企業創造了機會。

泰國油氣下游市場走勢

煉油精製能確認成長

儘管泰國消耗的大部分石油都是自己生產的,但它仍然依賴進口來滿足不斷成長的需求。據泰國能源和工程部稱,2020年汽油需求量每天超過3000萬升,但2021年前10個月燃料(柴油和汽油)消費量下降4.4%,日均1.31億升,同年與COVID-19 之前的水平相同。

就精製和加工能力而言,泰國的煉油業是東南亞第二大煉油業,僅次於新加坡。在泰國,2016年至2019年煉油產能保持相對穩定,從2016年的1,234,500桶/日增加到2021年的1,244,500桶/日。近年來,煉油廠加工能力不斷增加。該國擁有六座煉油廠,其中大部分由該國國有石油和天然氣集團 PTT 部分或全部擁有。該國正在積極提高精製能力,以滿足不斷成長的國內和地區需求。例如,泰國石油公司的是是拉差香甜辣椒醬煉油廠擴建計劃是該公司無污染燃料計劃(CFP)的一部分,預計到2023年終竣工後總產能將達到40萬桶/日。

由於煉油廠擴建和精製油需求增加,泰國精製能力預計在預測期內略有增加。

石油和天然氣產量下降抑制市場

泰國正在轉型為“泰國4.0”,工業向技術進步和先進服務邁進。政府已將「下一代汽車」的發展指定為最重要的目標產業,並正在支持旨在從內燃機汽車(ICE)轉向東南亞電動車生產中心的電動車相關企業。

在泰國政府為促進電動車市場成長而採取的有利措施的支持下,電動車 (EV) 產業正在引起人們的興趣。例如,泰國政府制定了電動車獎勵制度,包括稅收減免和補貼,以促進該國電動車市場的發展。

2020 年國家電動車政策委員會推出了藍圖,制定了 2021 年至 2035 年泰國電動車發展框架,改造泰國現有的零排放車 (ZEV) 生產汽車供應鏈,建立現代化出行的技術能力。藍圖不僅涵蓋了電動車的生產和使用,還包括電池製造和供應的發展、充電站和電網管理等配套基礎設施以及相關安全標準和法規的規劃,以實現全面、一體化的實施。總體規劃中的電動車涵蓋了各種車輛,包括摩托車、三輪車、巴士、卡車和渡輪。

泰國消費稅部宣布,投資委員會(BOI)推廣的10人座及以下電動乘用車將從2020年1月1日至2022年12月31日以及2023年1月1日至2025年享受0%的稅收。

該國新登記的純電動車從2019年的724輛增加到2021年的2079輛。隨著電動車數量的增加,該國公共和私營部門的投資都在增加,充電站的數量也迅速增加。根據EVAT統計,2021年6月,全國10家開發商提供了2224個充電樁,安裝充電站超過664個。泰國政府的目標是到2036年在全國擁有690個充電站和120萬輛電動車。

交通運輸業在泰國下游油氣經濟中扮演重要角色。因此,電動車的引入預計將阻礙泰國石油和天然氣下游市場的成長。

泰國油氣下游產業概況

泰國的石油和天然氣下游市場本質上是部分一體化的。市場主要企業(排名不分先後)包括埃克森美孚公司、PTT Public Company Limited、Thai Oil PCL、IRPC PCL、Bangchak Petroleum Public Company 等。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 至2027年精製能力及預測(單位:千桶/日)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- PESTLE分析

第5章市場區隔

- 透過煉油廠

- 概述

- 現有、興建及規劃計劃

- 由石化廠

- 概述

- 現有、興建及規劃計劃

- 燃料零售/銷售

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- PTT Public Company Limited

- Esso Thailand PLC

- Bangchak Corporation PCL

- Royal Dutch Shell PLC

- Caltex(Chevron Corporation)

- SCG Chemicals Co. Ltd(Siam Cement Group)

- IRPC Public Company Limited

- Total SA

- ExxonMobil Corp.

- PTG Energy PCL

第7章 市場機會及未來趨勢

The Thailand Oil and Gas Downstream Market size is estimated at 1.45 million barrels per day in 2025, and is expected to reach 1.62 million barrels per day by 2030, at a CAGR of 2.26% during the forecast period (2025-2030).

Although the market studied was negatively impacted by COVID-19 in 2020, it has recovered and reached pre-pandemic levels. With the growing demand for various refined products, the country is focused on developing its refinery capacity, which is expected to drive the growth of the market studied during the forecast period. However, the shifting trend toward cleaner alternatives, such as the increasing adoption of electric vehicles, is expected to hinder the demand for refined products from end-user industries, which is expected to restrain the market's growth.

Gas fields have been discovered in the Andaman Sea, increasing optimism about reducing the dependence on imported gas and the cost of natural gas transportation. This factor is creating an opportunity for the players in the sector.

Thailand Oil and Gas Downstream Market Trends

Oil Refining Capacity to Witness Growth

Thailand produces a large share of the petroleum it consumes but still relies on imports to meet the increasing demand. Demand for gasoline stood above 30 million liters a day in 2020, while fuel (diesel and gasoline) consumption took a plunge of 4.4% in the first ten months of 2021 to a daily average of 131 million liters, the same level as before COVID-19 level, according to Department of Energy Business, Thailand.

The refinery sector of Thailand is the second largest in Southeast Asia in refining capacity and throughput, just after Singapore. In Thailand, the refineries' capacity has remained relatively stable during 2016-2019, at 1,234,500 barrels per day in 2016, which increased to 1,244,500 barrels per day in 2021. The refinery throughput has been increasing in recent years. The country has six refinery complexes, the majority of which are owned partially or fully by the country's national oil and gas conglomerate PTT. The country has been actively increasing its refining capacity to meet its growing domestic and regional demand. For instance, the expansion project of Thai Oil's Sriracha refinery, a part of the company's Clean Fuel Project (CFP), is expected to have a total capacity of 400,000 b/d when completed at the end of 2023.

Thailand's oil refining capacity is expected to grow slightly during the forecast period due to the expansion of refineries and increased demand for refined oil.

Decreasing Oil and Gas Production to Restrain the Market

Thailand is trying to transform into 'Thailand 4.0,' whose industries transition to technological advances and high-level services. The government designated 'next-generation automotive' development among the top targeted industries and supported EV-related businesses to transform from internal combustion engine (ICE) vehicles to an EV production hub in Southeast Asia.

The electric vehicle (EV) industry is gaining interest in Thailand, supported by favorable government policies to push the EV market's growth. For example, the government of Thailand rolled out EV incentive schemes, i.e., tax benefits and subsidy systems, to propel the development of the EV market in the country.

The National Electric Vehicles Policy Committee 2020 introduced a roadmap that lays out a framework for Thailand's EV development from 2021-2035 to transform the country's well-established automotive supply chain for the production of zero-emission vehicles (ZEVs) and build the technological capacity for modern mobility. The roadmap covers not only EV production and usage but also developing plans for battery manufacturing and supplies, supporting infrastructure, including charging stations and power grid management, and the development of related safety standards and regulations to enable comprehensive and integrated implementation. EVs in the master plan covers various vehicles, including motorcycles, tricycles, buses, trucks, and ferry boats.

The Excise Department of Thailand has been applying an excise tax rate of 0% from 1 January 2020 to 31 December 2022 and 2% from 1 January 2023 to 31 December 2025 to electric-powered passenger vehicles with seating not exceeding ten seats which are promoted by the Board of Investment (BOI).

The country's newly registered battery electric vehicles grew from 724 in 2019 to 2,079 in 2021. With an increase in the number of EVs, the country is also witnessing a surge in the number of charging stations with rising investments from both the public and private sectors. According to EVAT, the country had over 664 charging stations with 2,224 chargers from 10 developers nationwide in June 2021. By 2036, the Thai government aims to have 690 charging stations and 1.2 million electric vehicles nationwide.

The transportation sector plays a vital role in Thailand's downstream oil and gas economy. Therefore, the adoption of EVs is expected to hamper the growth of the downstream oil and gas market in Thailand.

Thailand Oil and Gas Downstream Industry Overview

The Thailand oil and gas downstream market is partially consolidated in nature. Some of the major players in the market (in no particular order) include Exxon Mobil Corporation, PTT Public Company Limited, Thai Oil PCL, IRPC PCL, and Bangchak Petroleum Public Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Refining Capacity and Forecast, in thousand barrels per day, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 By Refineries

- 5.1.1 Overview

- 5.1.2 Existing, Under Construction, and Planned Projects

- 5.2 By Petrochemical Plants

- 5.2.1 Overview

- 5.2.2 Existing, Under Construction, and Planned Projects

- 5.3 By Fuel Retail and Marketing

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 PTT Public Company Limited

- 6.3.2 Esso Thailand PLC

- 6.3.3 Bangchak Corporation PCL

- 6.3.4 Royal Dutch Shell PLC

- 6.3.5 Caltex (Chevron Corporation)

- 6.3.6 SCG Chemicals Co. Ltd (Siam Cement Group)

- 6.3.7 IRPC Public Company Limited

- 6.3.8 Total SA

- 6.3.9 ExxonMobil Corp.

- 6.3.10 PTG Energy PCL