|

市場調查報告書

商品編碼

1640360

陸地應用中的慣性系統:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Inertial Systems in Land-based Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

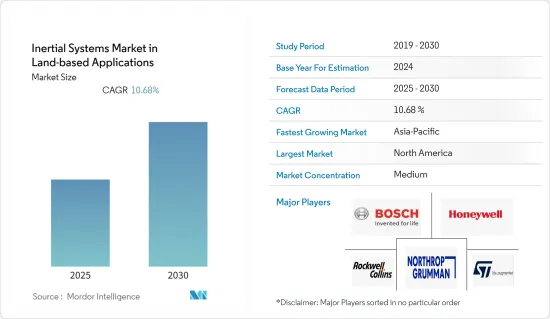

預測期內,陸地應用慣性系統市場預計將以 10.68% 的複合年成長率成長。

微機電系統 (MEMS) 技術的出現使得感測器和半導體領域的機械和電子機械元件透過微製造和微加工技術得以小型化。因此,MEMS有望成為未來導航系統不可爭議的一部分,推動慣性系統市場的成長。

此外,高階慣性系統由配備高性能感測器(陀螺儀、地磁感測器、加速感應器)的IMU組成,透過相對運動提供有關周圍環境的高精度資訊。因此,對導航系統更高精度的需求日益增加,從而推動了對先進慣性系統的需求。

此外,這些慣性系統擴大被應用於深海鑽井平台來執行先進的操作。 Sonardyne International 開發了一種新型 DP-INS(慣性導航系統),該系統結合了長基線、極短基線 (LUSBL) 定位技術的互補屬性與 Lodestar AHRS/INS 平台的高精度慣性測量。陀螺儀感測器是一種用於偵測高度角和角速度的慣性感測器。它具有體積小、功耗低、重量輕、成本低、可量產等特點,因此比傳統陀螺儀更廣泛的採用。

此外,由於新冠疫情,中國已停止包括半導體產業在內的所有主要生產活動。預計這將對2020年全球工業慣性系統市場的供應鏈產生重大影響,此後市場可望復甦。中國的生產中斷可能會對全球企業以及電子價值鏈上下游產生重大影響,並直接衝擊感測器市場。

陸地應用慣性系統的市場趨勢

精度需求不斷成長推動市場

高精度和高可靠性是導航系統最重要的特性。慣性導航系統與其他形式的導航系統相比具有明顯的優勢,因為它們不依賴外部輔助來確定運動物體的旋轉和加速度。這些系統使用陀螺儀、加速計和磁力計的組合來確定車輛或移動物體的向量變數。

導航系統本質上適合用於具有挑戰性的環境中車輛的綜合導航、控制和引導。與GPS和其他導航系統不同,慣性系統即使在惡劣的條件下也能保持其性能。慣性測量單元 (IMU) 非常適合導航系統計算多個指標。這些系統不受輻射和干擾的影響。慣性導航系統比萬向節系統更常使用捷聯系統。此外,由於採用了 MEMS 技術,因此它還具有成本效益。

隨著人工智慧和機器學習等先進技術得到越來越廣泛的應用,可使用感測器技術進行遠端控制的先進無人駕駛汽車變得越來越普遍。無人水下航行器、無人飛行器和無人地面航行器都正在採用這項新技術。因此,戰術級裝備的高度和方向等精確的位置參數在當今的戰鬥場景中至關重要。

慣性導航系統目前已商業性民航機、無人機、軍事和防禦部隊使用。慣性導航系統是導航和控制系統不可或缺的一部分,隨著系統處理能力的不斷提高,能夠與其他導航系統互動。某些形式的慣性系統,例如磁力儀,廣泛與其他形式的慣性系統結合使用,以確定方向和磁場的存在。

北美佔有最大市場佔有率

由於領先的 MEMS 供應商的存在,該地區很可能成為技術創新的源頭,因此預計會佔據相當大的市場佔有率。北美是世界上最大的海上油氣通訊市場之一。預計美國新發現的頁岩資源和加拿大石油和天然氣計劃的增加將推動該地區對通訊設備的需求。

美國內政部 (DoI) 計劃允許在約 90% 的外大陸棚(OCS) 面積上進行近海探勘。該地區的石油和天然氣產業預計將在2019-2024年國家外大陸棚石油和天然氣租賃計畫(國家OCS計畫)下創造新的機會。

此外,無人機數量的不斷成長和國防支出的增加是美國大量採用這些系統的主要原因。此外,根據美國高級研究計劃局(DARPA)的美國,美國國防部正在向美國提供先進工具,以擴大水下感測器的覆蓋範圍和有效性。 ),以幫助其潛艇探測並攻擊敵方潛艇。因此,政府措施和研發支出預計將進一步刺激該地區的市場成長。

陸地應用慣性系統產業概況

由於有各種慣性系統解決方案供應商,陸地應用慣性系統市場的競爭格局相當分散。然而,供應商始終專注於產品開發,以提高其知名度和全球影響力。此外,各公司正在建立策略聯盟和進行收購以獲得市場吸引力並擴大市場佔有率。

2021年10月,美國從諾斯羅普·格魯曼公司接受了第500套WSN-7環形雷射陀螺儀慣性導航系統(INS)。諾斯羅普·格魯曼公司繼續為美國和北約在世界各地的水面和潛艇海軍資產提供支持,這些資產分佈在美國艦隊的各個角落。

2021年4月,慣性實驗室宣布發布其下一代GPS輔助系統:INS-DH- OEM、IMU-NAV-100和INS-U。這些 INS 適用於無人機、直升機和機載LiDAR勘測。其中包括MEMS加速計和MEMS陀螺儀。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- MEMS技術的出現

- 基於運動感應的應用日益增多

- 市場限制

- 積分漂移誤差

第6章 市場細分

- 按組件

- 加速計

- IMU

- 陀螺儀

- 磁力儀

- 姿勢航向

- 參考系統

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第7章 競爭格局

- 公司簡介

- Honeywell International Inc.

- Northrop Grumman Corporation

- Rockwell Collins

- Bosch Sensortec GmbH

- ST Microelectronics

- Safran Group

- SBG Systems

- Raytheon Anschtz GmbH

- KVH Industries Inc.

- Silicon Sensing Systems Ltd

- Vector NAV

第8章投資分析

第9章:未來展望

The Inertial Systems Market in Land-based Applications Industry is expected to register a CAGR of 10.68% during the forecast period.

The emergence of Micro Electro Mechanical Systems (MEMS) technology resulted in the miniaturization of mechanical and electro-mechanical elements in the field of sensors and semiconductors through the use of micro-fabrication and micro-machining techniques. Hence, MEMS has become an indisputable part of future navigation systems and is expected to propel the inertial systems market's growth.

Additionally, high-end inertial systems are comprised of IMU with high-performance sensors (gyroscopes, magnetometers, accelerometers), which provide high accuracy information about the surrounding environment through relative movement. Hence, the need for higher accuracy in navigation systems is increasing, thus, increasing the demand for advanced inertial systems.

Moreover, these inertial systems are increasingly used in deep-water drilling units for advanced operations. Sonardyne International came up with a new DP-INS (inertial navigation system) that combined the complementary characteristics of its long and ultra-short baseline (LUSBL) positioning technology with high-integrity inertial measurements from its Lodestar AHRS/INS platform. Further, a gyroscope is a kind of inertial sensor used to detect the altitude angle and angular rate. Characteristics such as small size, low power consumption, lightweight, low cost, and the possibility of batch fabrication drive their adoption over conventional gyroscopes.

Further, due to the COVID-19 pandemic, China has stopped all major production activities, including its semiconductor industry. This is expected to significantly influence the global industrial inertial systems market supply chain in 2020, and the market is expected to pick up afterward. Disruption in China may significantly impact companies worldwide and up and down the electronics value chain, directly impacting the sensor market.

Land-based Applications Inertial Systems Market Trends

Increasing Demand for Accuracy to Drive the Market

A high level of accuracy and reliability is a navigational system's prime feature. Inertial navigational systems have a distinct advantage over other forms of navigation systems in terms of their lack of dependence on external aids to determine the rotation and acceleration of a moving object. These systems use a combination of gyroscopes, accelerometers, and magnetometers to determine the vector variables of a vehicle or a moving object.

Navigational systems are inherently suited for use in integrated navigation, control, and guidance of vehicles in challenging environs. Unlike GPS and other navigation systems, inertial systems can retain their performance even under challenging conditions. Inertial measurement units (IMU) are well suited for navigational systems to calculate several metrics. These systems remain unaffected by radiation and jamming problems. Strapdown inertial systems find more usage in inertial navigation systems than gimbaled systems, as they are strapped to the moving object and offer better reliability and performance. Moreover, they provide cost-effectiveness as they are incorporated with MEMS techniques.

As advanced technologies such as AI and Machine Learning become more widely adopted, advanced robotic cars that can be controlled remotely via sensor technology are becoming more common. Unmanned Underwater Vehicles, Unmanned Aerial Vehicles, and Unmanned Ground Vehicles are all being updated owing to this new technology. As a result, accurate position parameters, such as altitude and orientation of tactical grade equipment, are important in today's battle scenario.

Inertial navigation systems are now being made available for commercial use in private aircraft, UAVs, military, and defense units. They form an integral part of the navigational control systems and can interact with other navigational systems due to incremental advancements in the processing ability of the systems. Several forms of inertial systems like magnetometers are widely used for determining the orientation and presence of a magnetic field in conjunction with other forms of inertial systems.

North America to Hold the Largest Market Share

The presence of prominent vendors offering MEMS in the region is likely to emerge as a source for innovation, and it is estimated to hold a significant market share. North America is one of the largest markets for offshore oil and gas communication globally. New-found shale resources in the US and an increasing number of oil and gas projects in Canada are expected to drive the demand for communication equipment in the region.

The US Department of the Interior (DoI) plans to allow offshore exploratory drilling in about 90% of the Outer Continental Shelf (OCS) acreage. The region's oil and gas sector is expected to create new opportunities under the National Outer Continental Shelf Oil and Gas Leasing Program (National OCS Program) for 2019-2024.

Moreover, the rising number of unmanned aerial vehicles and rising defense spending are the key reasons for the high adoption of these systems in the US. Besides, under the US Defense Advanced Research Projects Agency (DARPA) program, to provide the US Navy with advanced tools to expand the reach and effectiveness of its underwater sensors, the US defense sector has invested in the development of small unmanned underwater vehicles (UUV) to help US submarines detect and engage adversary submarines. Hence, government initiatives and spending on R&D are expected to further stimulate the growth of the market in the region.

Land-based Applications Inertial Systems Industry Overview

The competitive landscape of the inertial systems market in land-based applications is fragmented moderately due to the presence of various inertial systems solution providers. However, vendors are consistently focusing on product development to enhance their visibility and global presence. Companies are also undergoing strategic partnerships and acquisitions to gain traction and increase their market share.

In October 2021, the US Navy received the 500th WSN-7 ring laser gyroscope inertial navigation system (INS) from Northrop Grumman Corporation. Northrop Grumman continues to support the US and NATO surface and submarine naval assets worldwide, with installations across the US Navy Fleet.

In April 2021, Inertial Labs announced the release of INS-DH-OEM, IMU-NAV-100, and INS-U, the next generation of GPS-assisted systems. These INS are intended for use with UAVs, helicopters, and LiDAR surveys from the air. MEMS accelerometers and MEMS gyroscopes are among them.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of MEMS Technology

- 5.1.2 Increasing Applications Based on Motion Sensing

- 5.2 Market Restraints

- 5.2.1 Integration Drift Error

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Accelerometers

- 6.1.2 IMUs

- 6.1.3 Gyroscopes

- 6.1.4 Magnetometers

- 6.1.5 Attitude Heading

- 6.1.6 Reference Systems

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 Northrop Grumman Corporation

- 7.1.3 Rockwell Collins

- 7.1.4 Bosch Sensortec GmbH

- 7.1.5 ST Microelectronics

- 7.1.6 Safran Group

- 7.1.7 SBG Systems

- 7.1.8 Raytheon Anschtz GmbH

- 7.1.9 KVH Industries Inc.

- 7.1.10 Silicon Sensing Systems Ltd

- 7.1.11 Vector NAV

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

汽車慣性系統市場-全球產業規模、佔有率、趨勢、機會和預測(按車型、零件、地區和競爭細分,2020-2030 年)

汽車慣性系統市場-全球產業規模、佔有率、趨勢、機會和預測(按車型、零件、地區和競爭細分,2020-2030 年) 亞太慣性系統市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)交通運輸中的慣性系統:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美慣性系統:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)戰術慣性系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)拉丁美洲慣性系統:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲慣性系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太慣性系統市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)交通運輸中的慣性系統:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美慣性系統:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)戰術慣性系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)拉丁美洲慣性系統:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲慣性系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 慣性系統市場:按組件、類型和應用分類 - 2025-2030 年全球預測高階慣性系統市場:按組件、按應用分類 - 2025-2030 年全球預測

慣性系統市場:按組件、類型和應用分類 - 2025-2030 年全球預測高階慣性系統市場:按組件、按應用分類 - 2025-2030 年全球預測 高階慣性系統市場報告:2030 年趨勢、預測與競爭分析

高階慣性系統市場報告:2030 年趨勢、預測與競爭分析