|

市場調查報告書

商品編碼

1642052

服務提供平台:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

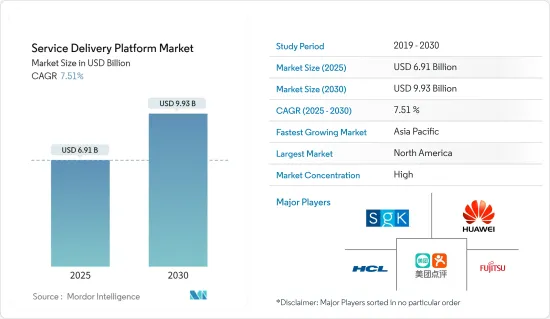

服務提供平台市場規模預計在 2025 年為 69.1 億美元,預計到 2030 年將達到 99.3 億美元,預測期內(2025-2030 年)的複合年成長率為 7.51%。

主要亮點

- 為了促進通訊業者、服務供應商者、內容提供者和使用者之間最佳化的服務交換,營運商解決方案服務配送平臺(SDP)提供了統一的中介基礎。醫療系統強化(HSS)的興起正在影響全球醫療保健趨勢並推動服務配送平臺市場的發展。 SDP 是一個支援廣泛應用程式、面向廣泛網路並為使用者提供廣泛服務的框架。 SDP需要整合IT功能,提供一個會話控制、服務創建、通訊協定實現、跨越技術和網路邊界的平台。

- 為了建立更實體的配送平台,企業正在針對不同產業客製化服務,升級配送調度系統,並增強配送基礎架構。 2022年,英特爾透過發布英特爾網路平台並加強針對5G和邊緣的新產品,維持了其作為網路矽晶圓供應商的領先地位。

- 兩家公司的目標是開發服務配送平臺,使通訊業者能夠透過行動裝置存取融合、多媒體和「Web 2.0」服務。

- 此外,2023 年 6 月,CWT 宣佈建立策略夥伴關係,將 Spotnana 的下一代旅遊即服務平台推向市場。此次合作標誌著 CWT 策略邁出的重要一步,該策略旨在利用其人才和整體的全球方法為尋求採用先進技術的客戶提供創新解決方案。

- 此外,2023 年 11 月,Indosat Ooredoo Hutchison (IOH) 和 TIMWETECH 宣布成功實施 TIMWETECH 的數位服務提供平台。 DSDP 平台整合是 Indosat 合作夥伴加入的關鍵一步。這個領先的平台簡化了整合過程,大大縮短了將服務推向市場所需的時間,並促進了與各個合作夥伴的順利合作。它在與主導通訊業數位內容和服務領域的 OTT 服務提供商合作時尤其有效。

服務提供平台市場趨勢

平台即服務 (PaaS) 的使用增加預計將推動市場成長

- 集中式服務提供平台可讓企業結合內部和外部服務並實施扣回爭議帳款機制。

- prpl高峰會2023將於2023年9月舉行,透過來自整個行業的演講者、通訊業者和行業利益相關者的主題演講以及創新的應用演示,將重點關注如何開發用於使用者端設備(CPE)的營運開放原始碼級開源相關人員來增強連網家庭體驗。

- 企業雲端採用率的提高為服務提供平台 (SDP) 創造了新的機會。 2022年10月,比利時跨國通訊服務公司BICS宣布推出其通訊平台即服務(CPaaS)平台。該平檯面向希望使用應用程式介面將語音、文字和 WhatsApp通訊等通訊服務無縫整合到現有工作流程中的企業。

- 軟體定義的資料中心利用 API主導的自動化和控制,這是增加客戶採用混合主機託管服務並增加收入的主要因素。

預計北美將佔據較大的市場佔有率

- 該地區聯網汽車日益普及,為 SDP 公司帶來了極為有利可圖的市場機會。例如,HCL Technologies 正在投資開發下一代服務平台 AGORA,該平台將為科技公司和服務供應商企業授權、提供、聚合和分發雲端和機器對機器 (M2M) 服務。 AGORA 是一個基於 SaaS 的解決方案加速器。

- 美國致力於實現基礎設施現代化,並透過投資資料中心來實現這一目標。例如,美國計劃花費高達 2.49 億美元部署私有雲端運算服務和模組化資料中心。由於 SDP 在資料中心有廣泛的應用,此類投資可能會促進服務提供平台市場的發展。

- 各國政府正在探索透過新的數位方法、使用虛擬助理和第三方應用程式為公民提供更順暢、更有效率的服務提供的方案。這為該地區的 SDP 提供者提供了潛在的機會。例如,加拿大正在探索使用 Alexa、Google Home 和其他平台來提供政府服務。

- 2023 年 8 月,面向客戶的計劃管理解決方案產業領導者之一 Rocketlane 宣布向專業服務自動化 (PSA) 策略擴張。透過此次嘗試,Rocketlane 將幫助 PS 組織實現前所未有的計劃盈利、效率和客戶滿意度。

服務提供平台產業概覽

服務提供平台市場由華為技術有限公司、HCL科技有限公司、富士通有限公司、SGK國際公司和美團點評公司等主要企業主導。這些參與者透過不斷的產品創新來獲得競爭優勢。大量投資於研發、策略聯盟和併購使這些公司提高了盈利和市場佔有率。

- 2023年10月-富士通為食品流通產業開發EDI共用操作平台。富士通為加強食品流通產業非競爭領域的協作與合作,建構了EDI(電子資料交換)共用營運平台,支援食品流通企業之間的業務標準化。 JII 已開始經營富士通為參與該計劃的國內食品分銷公司開發的新平台。

- 2022 年 2 月—德勤宣布擴展其數位服務提供平台,以幫助政府機構從雲端轉型中獲得目標收益並應對多重雲端挑戰。這些全面、可擴展的計劃旨在滿足各政府機構的特定需求,包括建立具有客製化服務產品和功能的可攜式、可互通的多重雲端設定的能力。

- 2022 年 4 月-Quantum Corporation 宣布推出新的服務配送平臺: MyQuantum。安全的入口網站為 Quantum 客戶提供對關鍵資源的單一登入 (SSO) 訪問,提供管理支援問題、搜尋Quantum 知識庫和文件、下載軟體以及使用基於雲端的分析 (CBA) AIOps 軟體監控 Quantum 資產的單一入口點。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素與限制因素簡介

- 市場促進因素

- 對資料和內容相關服務的需求不斷增加

- 對高性能智慧型手機的需求不斷增加

- 平台即服務 (PaaS) 的使用日益增多

- 市場限制

- 初期投資高

第5章 市場區隔

- 按類型

- 軟體

- 服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 世界其他地區

- 北美洲

第6章 競爭格局

- 公司簡介

- Huawei Technologies Co. Ltd

- HCL Technologies Ltd

- Fujitsu Ltd

- SGK International Inc.

- Meituan Dianping Inc.

- QTS Realty Trust Inc.

- Accenture PLC

- Telenity Inc.

第7章投資分析

第8章 市場機會與未來趨勢

The Service Delivery Platform Market size is estimated at USD 6.91 billion in 2025, and is expected to reach USD 9.93 billion by 2030, at a CAGR of 7.51% during the forecast period (2025-2030).

Key Highlights

- To facilitate the exchange of optimized services among operators, service and content providers, and users, service delivery platforms (SDPs) - which are operator solutions - provide a unified middle ground. The rising trend of "health system strengthening" (HSS) has become influential in global health circles, boosting the service delivery platform market. SDPs are a framework that supports a wide range of applications, targets different networks, and offers users extensive services. To provide a platform for session control, service development, protocol execution, and technology and network boundary crossing, SDPs require the integration of IT capabilities.

- To establish more physical delivery platforms, companies are customizing services for different industries, upgrading the delivery dispatch system, and enhancing delivery infrastructure. In 2022, Intel maintained its position as the top network silicon vendor by introducing the Intel Network Platform, as well as new product enhancements for 5G and Edge.

- Companies are aiming to develop a service delivery platform that allows telecom operators to access convergent, multimedia, and "Web 2.0" services on their mobile devices

- Furthermore, In June 2023, CWT announced a strategic partnership to provide Spotnana's next-generation Travel-as-a-Service platform to the market. This collaboration is an important step in CWT's strategy to bring innovative solutions to customers looking to deploy pioneering technology, driven by the strength of CWT's people and holistic, global approach.

- Moreover, in November 2023, Indosat Ooredoo Hutchison (IOH) and TIMWETECH announced the successful deployment of TIMWETECH's Digital Service Delivery Platform. Integrating the DSDP platform is a significant step for Indosat's partner onboarding. This advanced platform facilitates integration processes, significantly reducing the time required to bring services to the market and fostering smooth collaboration with various partners. It is especially effective in engaging with OTT service providers, who dominate the telco industry's digital content and service sector.

Service Delivery Platform Market Trends

Increasing Use of Platform-as-a-service (PaaS) is Expected to Drive the Market Growth

- A centralized service delivery platform allows enterprises to combine internal and external services and implement a chargeback mechanism, enabling them to charge business units for the services they use.

- In September 2023, The prpl Summit 2023 would focus on how developments in carrier-grade, open-source middleware for customer premises equipment (CPE) would enhance the connected home experience by featuring speakers from across the industry, keynotes from operators and industry stakeholders, and innovative application demonstrations.

- The rise in cloud adoption by companies presents new opportunities for the Service Delivery Platform (SDP). In October 2022, BICS, a Belgian multinational telecom services firm, launched its Communications Platform as a Service (CPaaS) platform, which is aimed at businesses that want to seamlessly integrate communication services like voice, text, and WhatsApp messaging into their existing workflows by utilizing Application Programming Interfaces.

- Software-defined data centers are taking advantage of API-driven automation and control, which is a significant factor contributing to the increased usage and sales of hybrid colocation services among customers.

North America is Expected to Hold Significant Market Share

- With connected cars gaining popularity in the region, they present a very lucrative opportunity for the SDP offering companies to tap the market. For instance, HCL Technologies has invested in developing AGORA, a next-generation services platform that allows, provides, aggregates, and distributes cloud and Machine to Machine (M2M) services for technology and service provider firms. AGORA is a SaaS-based solution accelerator.

- The United States was instrumental in modernizing its infrastructure, and the country aims to achieve this by investing in data centers. For instance, the US Army is planning to spend up to USD 249 million to deploy private cloud computing services and modular data centers. As SDP has a great application in the data centers, such investments may, in turn, boost the service delivery platform market.

- The governments are looking for options to ensure smooth and efficient service delivery to the public in new digital ways, either through virtual assistants or third-party applications. This offers a potential opportunity for the SDP offering firms in the region. For instance, Canada is looking to explore its government service delivery with Alexa, Google Home, or any other platforms.

- In August 2023, Rocketlane, one of the industry leaders in customer-facing project management solutions, announced its strategic expansion into Professional Services automation (PSA). With this foray, Rocketlane empowers PS organizations to achieve unprecedented project profitability, efficiency, and client satisfaction.

Service Delivery Platform Industry Overview

The service delivery platform market is consolidated with several major players, such as Huawei Technologies Co. Ltd, HCL Technologies Ltd, Fujitsu Ltd, SGK International Inc., and Meituan Dianping Inc. These players have gained a competitive advantage by continuously innovating their products. Significant investments in research and development, strategic partnerships, and mergers and acquisitions have enabled these companies to increase their profitability and market share.

- October 2023 - Fujitsu develops EDI shared operating platform for the food distribution industry. As part of this initiative that focuses on improving cooperation and collaboration in non-competitive areas in the food distribution industry, Fujitsu constructed an Electronic Data Interchange (EDI) shared operating platform to support food distributors in standardizing operations. JII started operations of the new platform developed by Fujitsu for food distribution companies in Japan participating in the initiative.

- February 2022 - Deloitte announced the expansion of its digital service delivery platform to assist government agencies in gaining targeted advantages from cloud transformation and navigating multi-cloud difficulties. This comprehensive and scalable plan is designed to meet the specific demands of various government entities, including the ability to build portable, interoperable multi-cloud setups with customized service offers and capabilities.

- April 2022 - Quantum Corporation announced the launch of its new service delivery platform, MyQuantum. This secure web portal provides Quantum clients with single sign-on (SSO) access to key resources, enabling them to manage support issues, explore the Quantum knowledge base and documentation, download software, and monitor their Quantum assets using Cloud-Based Analytics (CBA) AIOps software from a single point of entry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Rise in Demand for Data and Content-related Services

- 4.3.2 Rising Demand for High Performance Smartphones

- 4.3.3 Increasing Use of Platform-as-a-service (PaaS)

- 4.4 Market Restraints

- 4.4.1 High Initial Investments

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Software

- 5.1.2 Services

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Rest of the Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Huawei Technologies Co. Ltd

- 6.1.2 HCL Technologies Ltd

- 6.1.3 Fujitsu Ltd

- 6.1.4 SGK International Inc.

- 6.1.5 Meituan Dianping Inc.

- 6.1.6 QTS Realty Trust Inc.

- 6.1.7 Accenture PLC

- 6.1.8 Telenity Inc.