|

市場調查報告書

商品編碼

1643132

印度智慧型電視與 OTT -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Smart TV and OTT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

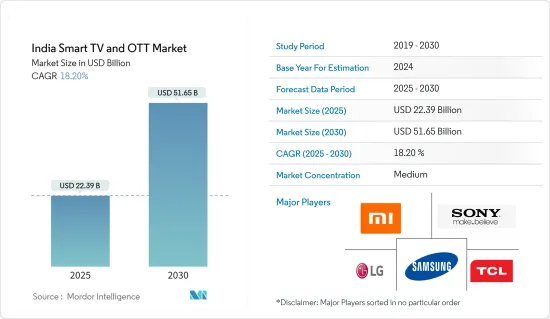

印度智慧型電視和 OTT 市場規模預計在 2025 年為 223.9 億美元,預計到 2030 年將達到 516.5 億美元,預測期內(2025-2030 年)的複合年成長率為 18.2%。

隨著高速網路的普及,熱衷於高品質內容的觀眾/聽眾開始更喜歡智慧電視而不是其他電視系統。此外,對視聽內容 OTT 串流媒體的需求日益成長,對印度的整體智慧型電視市場產生了積極影響。

關鍵亮點

- 印度大部分地區的高速網路普及以及消費者對線上內容偏好的轉變正在推動市場成長。 Netflix、Amazon Prime 和 Hotstar 等串流影片公司的大量投資帶動付費電視用戶數量的增加。

- 此外,可支配收入水準的提高和網際網路普及率的提高也促進了智慧型電視銷售的成長,從而促進了市場成長。此外,根據 IBEF 的數據,印度 OTT 視訊串流市場規模預計到 2023 年將達到 50 億美元,到 2022 年將達到 8.23 億美元,成為全球十大 OTT 市場之一。

- 印度家庭正在經歷轉型,其偏好從傳統電視轉向智慧電視。中等收入階級生活方式的改變源自於收入水準的提高、意識的增強、新技術的採用和網路普及率的提高。此外,政府措施(主要在二線和三線城市)也是預測期內推動印度智慧型電視市場成長的主要因素之一。

- 同時,線上串流媒體的需求不斷成長,為服務供應商進入 OTT 領域並透過網路提供內容提供了機會。 Netflix、亞馬遜、Hotstar、Sony Liv 等 OTT 內容參與企業以及其他幾家串流媒體服務正在增加對行銷和本地內容的支出,以擴大客戶群並吸引客戶放棄 DTH 和有線電視服務。許多此類平台也與寬頻供應商合作,透過提供免費捆綁優惠來吸引現有資料用戶。這些持續的努力加上消費行為的改變,正在幫助推動該市場的需求。

- 新冠肺炎疫情對顯示器產業帶來了不利影響,主要製造地的生產業務暫停,生產速度大幅放緩。三星、LG Display和小米等各大製造商已停止在中國、印度、韓國和歐洲的生產業務。然而,疫情期間,由於人們長時間待在家中,市場消費需求大幅增加。此外,疫情導致的電視收視率上升也預計將持續影響市場,進而推動市場成長。

印度智慧電視與 OTT 市場趨勢

物聯網生態系統中智慧型設備的普及正在推動市場成長

- 根據愛立信的《物聯網連接展望》報告,2021年,透過物聯網技術連接的設備數量將增加80%左右,達到3.3億台。這種成長可歸因於連接功能到許多設備和應用程式中的整合以及各種網路通訊協定的發展,這些發展推動了各個終端用戶行業的消費者物聯網市場的成長。

- 網路普及率的提高也促進了印度擴大採用支援物聯網的家用電子電器,例如智慧型電視。根據貝恩公司發布的《為印度解鎖數位技術:500 億美元的機會》報告,印度擁有全球第二大活躍網路用戶群,約有 3.9 億居民每月至少造訪一次網路。此外,根據愛立信連接展望報告,物聯網技術的成長將透過增加實現大規模物聯網與4G和5G共存的網路功能而得到促進。

- 此外,環境智慧和自動用戶幫助等功能使得智慧型電視在物聯網生態系統中變得越來越重要,再加上印度人民的可支配收入的增加,進一步推動了市場成長。

- 家用電子電器製造商三星印度公司最近表示,預計 LED 電視領域的成長率將接近 25%。該公司旨在透過提供具有正確提案和新技術的產品來佔據約 36% 的電視市場總量。為此,該公司於 2022 年 4 月在印度推出了超高階 2022 Neo QLED 8K 和 Neo QLED 電視。

- 此外,小米最近還增加了三家新的智慧型手機和智慧型電視合作夥伴,擴大了其在印度的生產規模。新的合作夥伴關係預計將進一步提升小米在印度的製造能力。預計這些領先供應商的發展將在預測期內推動市場成長。

網際網路通訊協定電視(IPTV)推動市場成長

- 視訊點播 (VOD) 是 IPTV 提供的動態功能之一。視訊資料透過即時串流通訊協定傳輸。 VOD 最近變得非常流行。因此,智慧型電視的普及率正在上升。此外,隨著智慧型手機普及率的提高和資料通訊資費的降低,透過 OTT 平台提供的 VoD 服務在印度呈現出良好的成長動能。

- 由於該地區寬頻普及率的提高和內容消費行為的改變,OTT 和 IPTV 正在獲得發展動力。這種影響在印度等亞洲國家尤其明顯,這些國家21會計年度的GDP成長率為8.9%。該地區的快速都市化(印度為35.39%)和不斷成長的消費能力在家庭採用 IPTV 方面發揮關鍵作用。

- 此外,印度政府在有線電視數位化、直接到戶(DTH)服務等數位轉型方面的努力也支持了IPTV在該國的普及。隨著網路服務供應商的出現,向其客戶免費提供即時 IPTV 串流服務,印度的 IPTV 格局正在改變。其他公司也紛紛效仿,預計該地區對行動 IPTV 服務的需求將會增加。

- 為了維持市場競爭力,各個供應商都在進行策略性投資。例如,2022年7月,印度政府宣布核准索尼影視網路印度公司與Zee Entertainment的合併。

印度智慧型電視和OTT產業概況

印度智慧型電視和 OTT 市場由多個參與企業組成。由於近期消費者興趣的激增,該行業被視為一個有利可圖的投資機會。公司正在投資未來技術並獲得真正的專業知識,以實現永續的競爭優勢。

- 2022 年 3 月:印度公共廣播公司DD India 與電視觀眾入口網站 OTT 平台 Yupp TV 簽署了一份合作備忘錄,以擴大 DD India 頻道的全球影響力。印度資訊廣播部表示,此舉旨在將印度對各類國際情勢的觀點投射到全球平台上,向世界展示印度文化和價值觀。

- 2022 年 1 月:Sony電子推出 BRAVIA XR 電視系列,包括 MASTER 系列 Z9K 8K、X95K 4K Mini LED 型號、MASTER 系列 A95K、MASTER 系列 A90K、A80K 4K OLED 型號和 X90K 4K LED 型號。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 調查結果

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

- 產業價值鏈分析

第5章 市場動態

- 市場促進因素

- 印度家庭數量龐大,普及率相對較低

- 消費者能力的提升和智慧型手機普及率的提高推動了對 OTT 的需求

- 較低的單價和本地參與企業的進入增強了買家的議價能力

- 市場限制

- 製造商面臨稅收挑戰和相對較高的更換率

第6章 全球智慧電視市場概述(出貨量預測、主要供應商的成長策略、市場展望、印度市場的關鍵指標)

第7章 市場區隔

- 作業系統類型(Tizen、WebOS、Android TV 等)

- 價格分佈

第8章 印度OTT情況分析

- 歷史背景和當前市場狀況

- 市場區隔-廣播公司(Hotstar 和 ZEE)、獨立公司(Alt Balaji 和 Viu)、國際參與企業(Netflix 和 Amazon Prime)、通訊業者(Jio、Airtel、Vodafone Play)

- 主要OTT參與企業用戶規模(單位:10萬)

- OTT參與企業採用的關鍵策略——內容在地化、可負擔性、策略合作夥伴關係、個人化以及利用數位轉型吸引觀眾

- 印度OTT與DTH用戶群比較研究

- 各大供應商重點客戶獲取策略

- 服務捆綁和通訊業者合作

- 優質化和內容驅動計劃

- 針對年輕人的經濟實惠的訂閱計劃

- 目前 OTT 供應商確定的其他關鍵策略主題

- 在對本地內容的強勁需求的支持下,預計本地參與企業將崛起

第9章 供應商市場佔有率分析-印度智慧電視(小米、三星、LG、索尼等)

第10章 競爭格局

- 公司簡介

- Xiaomi Corporation

- Samsung Electronics

- LG Corporation

- Sony Corporation

- TCL Technology

- Vu Technologies

- Honor

- Panasonic Corporation

- Haier

- OnePlus

- Sansui

第11章 投資展望

第12章 市場展望市場展望

The India Smart TV and OTT Market size is estimated at USD 22.39 billion in 2025, and is expected to reach USD 51.65 billion by 2030, at a CAGR of 18.2% during the forecast period (2025-2030).

As high-speed internet has become easily affordable, viewers/audiences that prefer good quality content prefer smart TVs over other television systems. Also, the increasing admiration for OTT streaming in audiovisual content is impacting the overall smart TV market in a positive manner in India.

Key Highlights

- The shifting consumer preferences toward online content due to the increasing proliferation of high-speed internet in most parts of India provides an impetus to market growth. Substantial investment flows by video streaming media companies, like Netflix, Amazon Prime, and Hotstar, led to an increase in Pay-TV subscribers.

- Furthermore, a rise in disposable income levels and growing internet penetration in the country also contribute to an increase in sales of smart TVs and hence fuelling the market growth. Moreover, according to IBEF, the market size of the OTT video streaming market of India is forecasted to reach USD 5 billion by 2023, and India is projected to become one of the top 10 global OTT markets to reach USD 823 million by 2022.

- Households in India are at a cusp of transition, and a shift in preference has been witnessed from conventional TV sets to smart TV sets. Changing the lifestyle of the middle-income population is attributed to rising income levels, increasing awareness, adoption of new technology, and growing internet penetration. Additionally, government initiatives, primarily in tier-II and tier-III cities, are some of the key factors likely to bolster the growth of the Indian smart TV market during the forecast period.

- On the other hand, the growing demand for online streaming has opened opportunities for service providers to venture into the OTT space and distribute content via the internet. OTT content players, such as Netflix, Amazon, Hotstar, Sony Liv, and several other streaming services, are increasing their spending on marketing and local content to expand their customer base by luring them away from DTH and TV Cable services. Many of these platforms also partner with broadband providers to get the existing data users onboard by offering free bundled subscriptions. These continued efforts, coupled with changing consumer behavior, are driving the increased demand for the market.

- The COVID-19 outbreak affected the display industry negatively, with manufacturing operations temporarily suspended across major manufacturing hubs, leading to a substantial slowdown in production. Various key manufacturers, including Samsung, LG Display, and Xiaomi, suspended their manufacturing operations in China, India, South Korea, and Europe. However, the market has witnessed considerable growth in consumer demand during the pandemic as people stayed at their homes for extended periods. Further, the increased tendency to watch television due to the pandemic is also expected to continue impacting the market, resulting in its growth.

India Smart TV & OTT Market Trends

Increasing Adoption of Smart Devices Across IoT Ecosystem to Drive the Market Growth

- According to Ericsson's IoT Connections Outlook report, the number of devices connected by IoT technologies increased by approximately 80% and reached 330 million in 2021. The growth can be attributed to the integration of connectivity competence in many devices and applications, along with the development of various networking protocols that have advanced the growth of the consumer IoT market across various end-user industries.

- Increasing internet penetration can also contribute to India's widespread expansion of IoT-enabled consumer electronics, such as smart TV. According to Bain and Company's, Unlocking Digital for Bharat: USD 50 billion Opportunity, the report stated India has the second-highest number of active internet users, with about 390 million residents who use the web at least once a month. Further, the Ericsson connection outlook report stated that the growth of IoT technologies is enhanced by an added network capability that enables massive IoT co-existence with 4G and 5G.

- Additionally, the increasing significance of smart TV in the IoT ecosystem, due to the features like ambient intelligence and automatic user assistance, along with the rising disposable income of the people in India, is further boosting the market growth.

- Samsung India, a consumer electronics firm, has recently announced that it expects a nearly 25% growth in the LED TV segment. The company aims to capture around 36% share of the overall TV market by bringing products with the right proposition and new technologies. Owing to this, the company, in April 2022, launched its ultra-premium 2022 Neo QLED 8K and Neo QLED TVs in India.

- Moreover, recently, Xiaomi expanded its manufacturing in India by adding three new partners for smartphones and smart TVs. The new partnerships are expected further to increase Mi India's manufacturing capacity in India. Such developments by the major vendors are expected to boost market growth over the forecast period.

Internet Protocol Television (IPTV) to Boost the Market Growth

- Video on demand (VOD) is one of the dynamic features offered by IPTV. The video data is transmitted via Real-Time Streaming Protocol. VOD has gained a tremendous amount of popularity in the recent past. This has resulted in the increased adoption rates of Smart TVs. Moreover, with growing smartphone penetration and lower data tariffs, VoD services through OTT platforms show promising growth in India.

- OTT and IPTV are gaining traction driven by increasing broadband penetration and changing content consumption behaviors in the region. The effect can be significantly observed in Asian countries, like India, which represented an 8.9% GDP growth rate in FY 2021. Rapid urbanization in the region, standing at 35.39% in India, and the increase in spending power play a significant role in adopting IPTV in households.

- Moreover, the Government of India's initiatives toward digital transformation, such as digitization of cable TV and direct-to-home (DTH) services, are also favoring the adoption of IPTV in the country. The IPTV scenario in India is witnessing change owing to the advent of the network services provider, with the company providing free IPTV live subscriptions to its customers. With other companies following suit, the demand for mobile-based IPTV services is expected to increase in the region.

- The market is witnessing strategic investments from various vendors to remain competitive. For instance, in July 2022, the Government of India announced the approval of the merger between Sony Pictures Networks India and Zee Entertainment.

India Smart TV & OTT Industry Overview

The Indian smart TV and OTT market consists of several players. This industry is viewed as a lucrative investment opportunity due to the recent huge consumer interest. The companies are investing in future technologies to gain substantial expertise, enabling them to achieve sustainable competitive advantage.

- March 2022: India's public broadcaster, DD India, signed an MoU with Yupp TV, an OTT platform that is a gateway for television viewers, to expand the global reach of the DD India channel. According to the Ministry of Information and Broadcasting, this is an attempt to put forth India's perspective on various international developments on global platforms and to showcase India's culture and values to the world.

- January 2022: Sony Electronics announced a Bravia XR television series, including MASTER Series Z9K 8K and X95K 4K Mini LED models, MASTER Series A95K, MASTER Series A90K and A80K 4K OLED models, and X90K 4K LED model.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Study Deliverables

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the market

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Large Volume of the Indian Households and Relative Less Levels of Penetration

- 5.1.2 Growing Spending Power and Growth in Smartphone Adoption to boost OTT Demand

- 5.1.3 Declining Unit Prices Coupled with Entry of Several Regional Players to Drive Bargaining Leverage of Buyers

- 5.2 Market Restraints

- 5.2.1 Manufacturers Faced with Taxation Challenges and Relatively Higher Replacement Rate

6 GLOBAL SMART TV MARKET SNAPSHOT (Unit Shipment Forecasts, Growth Strategies Adopted by Key Vendors, Market Outlook, and Major Cues for the Indian Market)

7 MARKET SEGMENTATION

- 7.1 OS Type (Tizen, WebOS, Android TV, etc.)

- 7.2 Price Range

8 ANALYSIS OF THE OTT LANDSCAPE IN INDIA

- 8.1 Historical Context and Current Market Scenario

- 8.2 Market Categorization - Broadcaster (Hotstar and ZEE), Independent (Alt Balaji and Viu), International Players (Netflix and Amazon Prime), and Telco (Jio, Airtel, and Vodafone Play)

- 8.3 Subscriber Base of Key OTT Players (in million)

- 8.4 Key strategies adopted by OTT players -Localization of Content, Affordable Pricing, Strategic Collaborations, Personalization and Use of Digital Transformation for View Engagement

- 8.5 A comparative Study of OTT and DTH User Base in India

- 8.6 Key Customer Acquisition Strategies of Major Vendors

- 8.6.1 Bundling of Services and collaboration with Telcos

- 8.6.2 Premiumization and Emphasis on Content-driven Programs

- 8.6.3 Affordable Subscription Plans Targeted at Young Populace

- 8.6.4 Other Key Strategic Themes Identified from the Current OTT Vendors

- 8.7 Local Players expected to Catch Ground Aided by Strong Demand for Regional Content

9 VENDOR MARKET SHARE ANALYSIS - INDIA SMART TV (Xiaomi, Samsung, LG, Sony, etc.)

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles

- 10.1.1 Xiaomi Corporation

- 10.1.2 Samsung Electronics

- 10.1.3 LG Corporation

- 10.1.4 Sony Corporation

- 10.1.5 TCL Technology

- 10.1.6 Vu Technologies

- 10.1.7 Honor

- 10.1.8 Panasonic Corporation

- 10.1.9 Haier

- 10.1.10 OnePlus

- 10.1.11 Sansui

11 INVESTMENT OUTLOOK

12 MARKET OUTLOOK

網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類)

網路電視市場:2026年至2032年全球預測(依顯示技術、解析度、螢幕大小、作業系統和應用程式分類) 2026年全球體育賽事線上影片市場報告

2026年全球體育賽事線上影片市場報告 智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類

智慧電視市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、功能、安裝類型、最終用戶及模式分類 美國智慧電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國智慧電視:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年

智慧電視市場規模、佔有率、趨勢和預測(按解析度類型、螢幕大小、螢幕類型、技術、平台、分銷管道、應用和地區分類),2026-2034年 智慧電視市場規模、佔有率和趨勢分析報告:按解析度、螢幕尺寸、作業系統、分銷管道、技術、地區和細分市場預測(2026-2033 年)2026年全球智慧電視市場報告

智慧電視市場規模、佔有率和趨勢分析報告:按解析度、螢幕尺寸、作業系統、分銷管道、技術、地區和細分市場預測(2026-2033 年)2026年全球智慧電視市場報告 智慧電視市場-全球產業規模、佔有率、趨勢、機會、預測:按解析度類型、螢幕大小、螢幕類型、分銷管道、地區和競爭格局分類,2021-2031年智慧電視棒市場 - 全球產業規模、佔有率、趨勢、機會及預測(按影片支援類型、銷售管道、地區和競爭格局分類,2021-2031年)日本智慧電視市場報告(按解析度類型、螢幕尺寸、螢幕類型、技術、平台、配銷通路、應用和地區分類,2026-2034年)

智慧電視市場-全球產業規模、佔有率、趨勢、機會、預測:按解析度類型、螢幕大小、螢幕類型、分銷管道、地區和競爭格局分類,2021-2031年智慧電視棒市場 - 全球產業規模、佔有率、趨勢、機會及預測(按影片支援類型、銷售管道、地區和競爭格局分類,2021-2031年)日本智慧電視市場報告(按解析度類型、螢幕尺寸、螢幕類型、技術、平台、配銷通路、應用和地區分類,2026-2034年)