|

市場調查報告書

商品編碼

1644495

全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Global Office Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

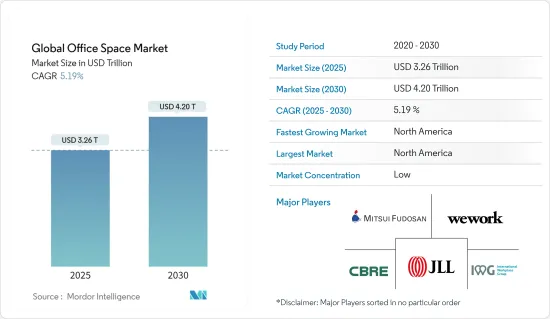

2025 年全球辦公空間市場規模估計為 3.26 兆美元,預計到 2030 年將達到 4.2 兆美元,預測期內(2025-2030 年)的複合年成長率為 5.19%。

尤其是規模較大的公司仍依賴採用長期合約的傳統辦公空間租賃模式。靈活工作安排的增加推動了共享辦公空間和服務式辦公室等靈活工作空間解決方案的發展以及會議室的需求。在英國,《僱傭關係軟工作法案》已於2023年7月獲議會通過並獲得御准。

共享辦公空間提供共用工作空間和靈活的租賃條款,深受自由工作者、新興企業和成熟企業的歡迎。這樣的空間通常提供協作環境、交流機會和便利設施,吸引尋求靈活性的企業。

科技在辦公空間中扮演越來越重要的角色。物聯網設備、居住感測器和整合通訊工具等智慧辦公室解決方案正在提高效率、安全性和工作場所體驗。 2023年1月,Global IT Corporation與柯尼卡美能達公司宣布成立合資企業柯尼卡美能達解決方案實驗室公司,以加強軟體開發能力並推動辦公空間市場的成長。柯尼卡美能達也瞄準了市場的其他外圍領域,例如智慧辦公室解決方案和尚未開發的軟體解決方案潛力。

全球辦公空間市場趨勢

彈性辦公空間愈發受歡迎

彈性工作空間市場的成熟(尤其是在某些城市)以及疫情防範需求的增加,導致辦公空間需求大幅增加。這一趨勢受到新興企業的崛起以及成熟公司對提供靈活工作空間作為房地產策略的認可度提高的支持。隨著科技公司尋求建立具有靈活模式的全球能力中心,以便在嚴峻的經濟環境下更好地控制成本,對軟辦公空間的需求可能會成長。預計疫情和景氣衰退的影響將導致租戶對更大靈活性和更短租賃期限的需求。他們在分配資本和營運成本時也可能更加謹慎。預計這一趨勢將持續下去,企業辦公室可能會尋求設備更好的空間、更短的租賃期限或平均鎖定期為 36 個月或更短的私人營運空間。根據產業報告顯示,到2024年,彈性工作空間辦公桌的數量預計將從254萬張增加到310萬張。

然而,隨著運轉率和需求的增加,主要的微型市場營運商正在尋求提高定價。私人辦公室彈性合約的運轉率率已恢復至疫情前的水平(超過 80%),共用空間的入住率也已恢復至 65% 以上。彈性業者對私人辦公室的辦公桌收取了更高的價格,2022 年 10 月歐洲的價格平均上漲了 9%。

印度城市優質辦公大樓租金漲幅高居亞太地區首位

在印度,孟買大都會區在 2023 年上半年的租金最高,其次是國家首都地區 (NCR) 和班加羅爾。由於空間有限,孟買的租金增約 16%,其次是德里國家首都轄區和浦那,分別較去年同期小幅上漲 3% 和 2%。

在班加羅爾和海德拉巴,辦公空間的流入速度持續超過租賃速度,導致空置率上升。印度商業房地產行業並未完全免受全球經濟成長放緩的不利影響,這導致一些公司裁員,並有幾個城市出現技術性衰退。第一季需求明顯放緩,年減14%,第二季年減9%。

由於許多科技公司鼓勵員工重返辦公室,該市的租賃活動明顯改善。 2023 年上半年,IT 產業佔清奈租賃交易的 46%,顯示其在該市辦公大樓市場中持續發揮重要工作 用。繼IT-BPM領域之後,彈性工作空間租賃活躍,貢獻率為21%,租賃面積約90萬平方英尺。能源和化學產業的佔用者也表現活躍,從 2022 年上半年的少數佔有率上升到 2023 年上半年的 19%。

全球辦公空間產業概覽

全球辦公空間市場競爭激烈,參與企業眾多。該市場的知名參與企業包括世邦魏理仕集團、三井不動產、仲量聯行公司、IWG PLC 和 WeWork。這些公司正在利用策略合作措施來增加市場佔有率和盈利。供應商依靠連續的併購、研發、地理擴張和新產品引進策略來進一步擴大業務並實現成長。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場洞察

- 市場概況

- 政府法規和舉措

- 產業技術趨勢

- 辦公室租金洞察

- 辦公空間規劃洞察

- COVID-19 對市場的影響

- 價值鏈/供應鏈分析

第5章 市場動態

- 市場促進因素

- 彈性的工作安排與共享辦公空間

- 市場限制

- 遠距工作趨勢

- 市場機會

- 科技融合與智慧辦公室

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 依建築類型

- 維修

- 新建築

- 按最終用戶

- 資訊科技/通訊

- 媒體娛樂

- 零售和消費品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 埃及

- 其他中東和非洲地區

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲國家

- 北美洲

第7章 競爭格局

- 市場集中度概覽

- 公司簡介

- CBRE Group Inc.

- Mitsui Fudosan Co. Ltd

- Jones Lang LaSalle Incorporated

- IWG PLC

- WeWork

- Knotel Inc.

- Servcorp

- The Office Group

- WOJO

- Mindspace*

- 其他公司

第8章 市場機會與未來趨勢

第 9 章 附錄

The Global Office Space Market size is estimated at USD 3.26 trillion in 2025, and is expected to reach USD 4.20 trillion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

In particular, larger companies still use a classic leasing model for office space on long-term agreements. Nevertheless, the development of flexible workspace solutions, such as coworking spaces and service offices, and the demand for meeting rooms are fueled by the increasing flexibility in working arrangements. The Employment Relations Flexible Working Bill was adopted by Parliament in July 2023 and received royal assent in the United Kingdom.

Coworking spaces, offering shared workspaces with flexible lease terms, have gained popularity among freelancers, start-ups, and even established enterprises. These spaces often provide a collaborative environment, networking opportunities, and amenities, attracting businesses seeking flexibility.

Technology is playing an increasingly significant role in office spaces. Smart office solutions, including IoT devices, occupancy sensors, and integrated communication tools, enhance efficiency, security, and workplace experience. In January 2023, Global IT Corporation and Konica Minolta Inc. announced the establishment of a joint venture, Konica Minolta Solution Labs Inc., to fortify software development capabilities and boost the growth of the office space market. Konica Minolta also targets other peripheral areas of the market, such as smart office solutions and the potential for untapped software solutions.

Global Office Space Market Trends

The Popularity Of Flexible Office Spaces is Increasing

The demand for office spaces increased significantly due to the maturity of the flexible workspace market, particularly in some cities, and the need for pandemic preparedness. The emergence of several start-ups and greater appreciation for existing market players offering flexible workspaces as real estate strategies underpinned this trend. As technology companies seek to set up global capability centers with a flexible model that allows them to control costs successfully in an economically challenging environment, demand for flexible office space will increase. Increased flexibility and shorter lease periods are expected to be requested by occupiers due to the effects of the pandemic and recession. They will be more careful when allocating capital and operational costs. This trend is expected to continue, and enterprise corporate offices may look for fitted-out spaces, shorter leases, or privately operated spaces with an average lock-in period of 36 months or less. According to industry reports, by 2024, the number of flexible workspace desks is expected to increase from 2.54 million to 3.1 million.

However, with increased occupancy levels and demand, vital micro-market operators are looking to improve their prices. The occupancy rate of flex contracts in private offices returned to a pre-pandemic level of more than 80% and more than 65% for shared space. Flex operators charged higher prices for private office desks, as recorded by an average 9% increase in October 2022 in Europe.

Indian Cities Recorded Highest Prime Office Rental Growth in Asia-Pacific

In India, the Mumbai Metropolitan Region recorded the highest office rental, followed by the National Capital Region (NCR) and Bengaluru, in the first half of 2023. The highest rental growth of approximately 16% Y-o-Y was recorded in Mumbai owing to limited availability of space, followed by Delhi-NCR and Pune, which noted a marginal rise of 3% and 2% Y-o-Y, respectively.

Bengaluru and Hyderabad saw a rise in vacancy levels due to a consistent infusion of space outpacing the leasing momentum. The Indian commercial real estate sector was not completely insulated from headwinds of slowing global economic growth, with select organizations reducing headcount and a few cities undergoing a technical recession. There was a visible slowdown in demand in the first quarter, with a 14% decline compared to the previous year, which continued in the second quarter, with demand contracting by 9% Y-o-Y.

With quite a few tech companies encouraging employees to return to the office, leasing activity saw a marked improvement in the city. The IT sector accounted for 46% of the leasing activity in Chennai in H1 2023, demonstrating its continued importance to the city's office market. Following the IT-BPM sector, flexible workspaces were leased aggressively, with a contribution of 21% and nearly 0.9 million sq. ft of leased area. The energy and chemicals sector occupiers were also active, with a substantial 19% share in leasing activity in H1 2023, up from a negligible share in H1 2022.

Global Office Space Industry Overview

The global office space market is highly competitive and consists of several players. Some prominent players in the market include CBRE Group, Mitsui Fudosan, Jones Lang LaSalle Incorporated, IWG PLC, and WeWork. These companies leverage strategic collaborative initiatives to increase their market share and profitability. Vendors depend on successive merger and acquisition strategies, research and development, geographic expansion, and new product introduction strategies to execute further business expansion and growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends in the Industry

- 4.4 Insights into Office Rents

- 4.5 Insights into Office Space Planning

- 4.6 Impact of Covid-19 on the Market

- 4.7 Value Chain / Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Flexible Work Arrangements and Coworking Spaces

- 5.2 Market Restraints

- 5.2.1 Remote Work Trends

- 5.3 Market Opportunities

- 5.3.1 Technology Integration and Smart Offices

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Building Type

- 6.1.1 Retrofits

- 6.1.2 New Buildings

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.2.4 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of the Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of the Asia-Pacific

- 6.3.4 Middle East and Africa

- 6.3.4.1 South Africa

- 6.3.4.2 United Arab Emirates

- 6.3.4.3 Saudi Arabia

- 6.3.4.4 Egypt

- 6.3.4.5 Rest of the Middle East and Africa

- 6.3.5 Latin America

- 6.3.5.1 Mexico

- 6.3.5.2 Brazil

- 6.3.5.3 Argentina

- 6.3.5.4 Rest of the Latin America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CBRE Group Inc.

- 7.2.2 Mitsui Fudosan Co. Ltd

- 7.2.3 Jones Lang LaSalle Incorporated

- 7.2.4 IWG PLC

- 7.2.5 WeWork

- 7.2.6 Knotel Inc.

- 7.2.7 Servcorp

- 7.2.8 The Office Group

- 7.2.9 WOJO

- 7.2.10 Mindspace*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年 共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年)

共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年) 亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F

共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F 共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測

共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測