|

市場調查報告書

商品編碼

1644870

英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)UK Co-Working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

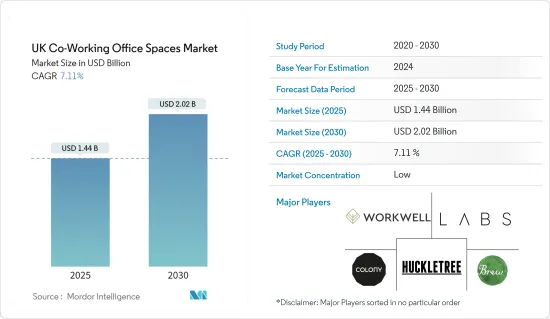

英國共享辦公空間市場規模預計在 2025 年為 14.4 億美元,預計到 2030 年將達到 20.2 億美元,預測期內(2025-2030 年)的複合年成長率為 7.11%。

共享辦公空間很快就成為企業的理想選擇。傳統的工作方式不再適合我們的生活方式。世界正在迅速走向共享辦公空間,它提供了靈活性和成長空間。

一項針對 1,000 名企業領導人的調查發現,在家工作帶來的自由可能會永久改變我們的工作方式。近一半(45%)擁有辦公空間的公司計劃在 2025年終縮小規模,七分之一(18%)的公司自疫情開始以來已經縮小規模。研究顯示,未來五年內,約有1,800萬平方英尺的辦公空間將被淘汰,佔目前已佔用空間的18%。

英國企業也尋求更短、更靈活的租約,並轉向 WeWork 等共享辦公空間,12% 的企業打算比「自有」辦公室更頻繁地使用這些空間。在計劃繼續使用辦公室的公司中,13%的公司將尋找人均辦公桌空間較小的住宿設施。

在這個新環境中,靈活性是改變的驅動力,將辦公空間轉變為充滿可能性的空間。例如,倫敦郊區的一個小型辦公空間為團隊提供的費用不到每人每天 265 歐元(287.51 美元)。這種靈活的空間回應了現代工作空間不斷發展的特性,不僅具有實用性,而且還能滿足現代職業生活不斷變化的需求。

英國共享辦公空間市場趨勢

成本上升、空置率下降導致辦公空間租賃需求激增

裝修和融資成本的上漲,以及開發完工時間的延遲,推動了租戶對靈活、對業主友善的辦公空間的需求。這些選擇有助於減輕這些風險,並為租戶提供靈活性和便利性。此外,黃金位置的彈性辦公空間短缺也推動了對業主安裝辦公空間的需求。許多地方的運轉率升至滿員。

然而,我們看到 5,000 至 10,000 平方英尺範圍內的裝修辦公空間交易量有所增加。這在金融城尤其明顯,2022 年由房東主導的裝修交易數量增加了一倍。

此外,2022 年,業主裝修佔該市面積少於 10,000 平方英尺的辦公室租賃交易的 42%(而 2021 年僅為 21%)。人們對全託管空間的興趣也日益濃厚,由業主提供軟服務。小型租戶青睞健身空間的趨勢預計將持續下去,尤其是隨著包含軟服務的「套餐交易」的興起。

倫敦共享辦公室的需求正在推動市場

當地調查顯示,倫敦是設立聯合辦公室的最佳地點。該研究調查了全球 53 個地點,考慮了共享辦公室的供需情況、平均每月成本、網路速度等。

結果,倫敦擊敗其他城市,奪得靈活辦公空間的頭把交椅。除了混合工作之外,對共享辦公室的需求也在上升。

Instant Group 報告稱,去年英國的運轉率達到了 83%,為疫情爆發前的最高水平。預計這一趨勢將持續到 2024 年,企業將考慮搬遷至服務式辦公室,以度過經濟衰退並降低管理成本。

倫敦擁有世界上最多的共享辦公空間,整個英國首都共有 1,400 個房間。巴黎是世界第二大城市,擁有 1,000 多個共享辦公空間。倫敦共享辦公空間每月平均搜尋次數為 4,400 次,顯示共享辦公空間的需求很高。最近的報告顯示,美國各地的企業正在將共享辦公作為租用全職辦公空間的經濟高效的替代方案。

根據 Google Trends 的資料,截至 2023 年 3 月 31 日,搜尋共享辦公室的企業數量激增。搜尋的突然增加可能是由於 2023 年 4 月 1 日生效的小型企業稅率上調。政府表示,透過引入新稅率,將使營業稅與市場規模保持一致。本月初辦公大樓價格平均漲幅約10%。

英國共享辦公空間產業概況

英國共享辦公空間市場較為分散,參與者眾多。開發商正在嘗試提供新的、成本更低的產品來滿足當前的需求。不斷發展的技術進步(例如新的房地產科技解決方案)正在推動市場在增加交易和更好地管理房地產服務方面的發展。英國領先的公司包括 Work Well Offices、Labs、The Brew、Huckle Tree 和 Jactin House。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 市場動態

- 驅動程式

- 共享辦公空間日益普及推動市場發展

- 人們對永續性的興趣日益濃厚,推動市場

- 限制因素

- 經濟不確定性影響市場

- 機會

- 對協作工作環境的需求不斷成長推動了市場

- 驅動程式

- 科技趨勢

- 產業價值鏈分析

- 政府法規和舉措

- 深入了解英國共享辦公室Start-Ups

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 新冠肺炎疫情的影響

第5章 市場區隔

- 按最終用戶

- 個人用戶

- 小型企業

- 大型企業

- 其他

- 按地區

- 倫敦

- 曼徹斯特

- 伯明罕

- 利茲

- 其他城市

- 按類型

- 靈活管理辦公室

- 服務式辦公室

- 按應用

- 資訊科技(IT 和 ITES)

- 法律服務

- BFSI(銀行、金融服務、保險)

- 諮詢

- 其他

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Work Well Offices

- Labs

- The Brew

- Huckle Tree

- Jactin House

- The Skiff

- Icon Offices

- Wimbletech CIC

- Regus

- Creative Works

- The Office Group

- Foyles

- Soho Works

- The Hoxton

- Mare Street Market

- Southbank Centre*

- 其他公司

第7章:市場的未來

第 8 章 附錄

The UK Co-Working Office Spaces Market size is estimated at USD 1.44 billion in 2025, and is expected to reach USD 2.02 billion by 2030, at a CAGR of 7.11% during the forecast period (2025-2030).

Co-working spaces are fast becoming the perfect fit for businesses. Traditional ways of working do not fit the way we live anymore. The world is rapidly moving towards co-working spaces that offer flexibility and space to grow.

The freedom afforded by working from home, according to the research of 1,000 business leaders, is set to alter the way they work permanently. Nearly half of the enterprises with office space (45%) plan to downsize by the end of 2025, and one in seven (18%) have already done so since the pandemic began. According to the study, about 18 million sq. ft of office space will become obsolete in the next five years, accounting for 18% of all currently occupied square footage, significantly impacting how cities in the United Kingdom appear and feel.

Businesses in the United Kingdom will also be looking for shorter, flexible leases and utilizing co-working spaces such as WeWork, with 12% intending to use these locations more often than an 'owned' office. For those businesses planning to stick to the office, 13% will look for accommodation with less desk space per head as the office's main function is set to shift with more space for collaboration, such as break-out areas and meeting rooms.

In this new landscape, flexibility is the driving force for change, transforming office spaces into spaces of possibility. For example, small office spaces outside of London are attracting teams for under EUR 265 (USD 287.51) per person per day. These are flexible spaces that respond to the ever-evolving nature of modern workspaces that not only function but also respond to the evolving needs of contemporary professional life.

UK Co-Working Office Space Market Trends

The Demand for Landlord-Fitted Office Space Surges Amid Rising Costs and Shrinking Availability

Occupants' demand for flexible and landlord-fitted office space is on the rise due to increasing fit-out and finance costs, as well as delayed development completion dates. These options help to mitigate these risks and offer flexibility and convenience for occupiers. The prime flexible office space shortage in key locations also drives demand for landlord-fitted office space. Occupancy rates are increasing to full capacity in many centers.

Fitted space has traditionally been more attractive to smaller tenants, with most transactions being under 5,000 sq. ft. However, there is an increasing number of fit-out office space deals in the 5,000-10,000 sq. ft range. This is especially true in the City, where the number of landlord-fitted transactions doubled in 2022.

Landlord-fitted office space also made up 42% of the total City of London office leasing transactions under 10,000 sq. ft in 2022, compared to just 21% in 2021. There is also a growing interest in fully managed space, where landlords offer soft services. A preference for fitted space among smaller tenants is anticipated to persist, particularly with the rise of 'package deals' where soft services are included as an offer.

The Demand for Co-working Office Space in London is Driving the Market

According to a local survey, London is said to be the best place to open a coworking office. The study looked at 53 locations around the world, taking into account the supply and demand of coworking, average monthly costs, and internet speeds.

The results showed that London outperformed all other cities, taking the number one spot for flexible office spaces. In addition to hybrid working, demand for coworking has been on the rise.

The Instant Group reported last year that occupancy rates in the United Kingdom stood at 83%, the highest level since before the pandemic. This trend is expected to continue in 2024 as companies look to move to serviced offices to weather the economic downturn and reduce overhead costs.

London has the most coworking spaces in the world, with 1,400 available across the UK capital. That's more than 1,000 coworking spaces in Paris, the second-largest city in the world. The average monthly search for coworking spaces in London was 4,400, demonstrating the high demand for coworking spaces. According to recent reports, organizations across the country are turning to coworking as a cost-effective alternative to renting full-time office workspace.

According to Google Trends data, the number of companies searching for coworking offices soared as of March 31, 2023. The spike in searches is likely due to the increase in small business rates, which entered into force on April 1, 2023. The government has said that the new rates will align business premises fees with their market value. Office properties had an average increase in rateable values of around 10% at the start of this month.

UK Co-Working Office Space Industry Overview

The UK co-working spaces market is fragmented, with many companies in the industry. Developers are trying to bring new and lower-cost products to meet the current demand. Evolving technological advancements such as new proptech solutions drive the market in terms of increased transactions and better management of real estate services. Some of the major players in the United Kingdom are Work Well Offices, Labs, The Brew, Huckle Tree, and Jactin House.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Shift Toward Co-working Spaces is Driving the Market

- 4.2.1.2 Increasing Focus on Sustainability is Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Economic Uncertainty is Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Increasing Demand for Collaborative Work Environments is Driving the Market

- 4.2.1 Drivers

- 4.3 Technological Trends

- 4.4 Industry Value Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Insights on Co-working Startups in the United Kingdom

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of the COVID-19 Pandemic

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Personal User

- 5.1.2 Small Scale Company

- 5.1.3 Large Scale Company

- 5.1.4 Other End Users

- 5.2 By Geography

- 5.2.1 London

- 5.2.2 Manchester

- 5.2.3 Birmingham

- 5.2.4 Leeds

- 5.2.5 Other UK Cities

- 5.3 By Type

- 5.3.1 Flexible Managed Office

- 5.3.2 Serviced Office

- 5.4 By Application

- 5.4.1 Information Technology (IT and ITES)

- 5.4.2 Legal Services

- 5.4.3 BFSI (Banking, Financial Services, and Insurance)

- 5.4.4 Consulting

- 5.4.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Work Well Offices

- 6.2.2 Labs

- 6.2.3 The Brew

- 6.2.4 Huckle Tree

- 6.2.5 Jactin House

- 6.2.6 The Skiff

- 6.2.7 Icon Offices

- 6.2.8 Wimbletech CIC

- 6.2.9 Regus

- 6.2.10 Creative Works

- 6.2.11 The Office Group

- 6.2.12 Foyles

- 6.2.13 Soho Works

- 6.2.14 The Hoxton

- 6.2.15 Mare Street Market

- 6.2.16 Southbank Centre*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年 共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年)

共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年) 亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F

共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F 共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測

共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測