|

市場調查報告書

商品編碼

1644516

印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Flexible Office Space - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

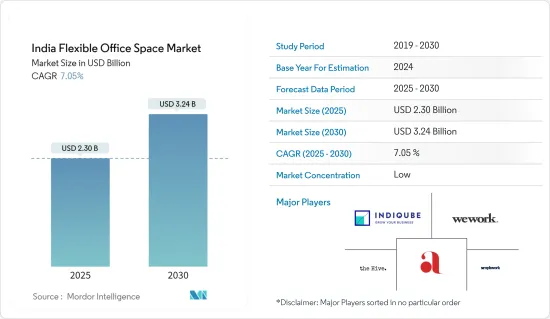

印度靈活辦公空間市場規模預計在 2025 年為 23 億美元,預計到 2030 年將達到 32.4 億美元,預測期內(2025-2030 年)的複合年成長率為 7.05%。

關鍵亮點

- 在混合工作模式興起、靈活租賃需求和不斷發展的工作文化的推動下,印度明顯轉向靈活的辦公空間。這一趨勢吸引了各種各樣的客戶,包括新興企業、中小型企業和大型企業。其在總辦公室租賃中的佔有率將從 2019 年的 10.2% 上升至 2024 年上半年的 12.7%。 2024 年 9 月《商業標準》的一份報告預測,彈性辦公席位將從 2021 年的 85,234 個飆升至 2023 年的 155,000 個,僅 2024 年上半年就租賃了 106,554 個席位。

- 根據產業機構關於彈性空間產業發展的報告,截至 2024 年上半年,印度前八大城市的彈性工作空間將達到 5,800 萬平方英尺(MSF),佔全國甲級辦公室總供應量的 7-8%。光是 2024 年上半年,彈性辦公空間供應量就將增加 500 萬平方英尺以上,每年成長 8 億-900 萬平方英尺,延續過去兩年的勢頭,2022 年的成長率為 23%,2023 年的成長率為 18%。

- 在過去三年半中,彈性工作空間領域每年都享有35-37%的驚人成長率。值得注意的是,2024 年已經步入正軌,實現了 2023 年租賃量的近 70%。該行業機構的報告《從靈活到託管—靈活空間產業的演變,2024 年 9 月》也詳細介紹了前八大城市的靈活空間庫存分佈。班加羅爾佔總數的 31%,其次是德里國家首都轄區(16%)、浦那(14%)、海得拉巴(14%)和孟買(11%)。此外,勞動力日益分散以及對工作與生活平衡的重視,推動了二線和三線城市對彈性工作空間的需求激增。在全國範圍內,彈性空間佔辦公空間總需求的 11-13%。

- 採用託管辦公室解決方案 (MOS) 模型的企業可享有客製化服務套件,從而能夠控制完全客製化的辦公室和工作空間的各個方面。在這個擁有 300 多家營運商的市場中,排名前 5% 的營運商持有超過 50% 的 A 級彈性庫存,其中大多數提供以託管辦公室解決方案 (MOS) 為中心的服務。

- 資訊科技(尤其是業務流程管理)將佔據主導地位,到 2024 年將佔靈活工作空間吸收量的 50%。其次是工程和製造業,佔 18%,以及銀行、金融服務和保險 (BFSI),佔 12%。成本的上升和疫情後遠距辦公的可行性,促使這些產業走向靈活的辦公室解決方案。

印度彈性辦公市場趨勢

市場因 IT 和通訊產業的需求而蓬勃發展

印度靈活辦公空間市場正在經歷顯著成長,主要由 IT 和通訊業推動。這些適應性工作空間的需求激增,凸顯了它們對於企業轉型為混合工作模式的重要性。根據《商業標準》報道,IT 產業將主導市場,佔 2024 年上半年彈性辦公空間吸收量的 50%。靈活的辦公室解決方案越來越有吸引力,尤其是對於熱衷於最佳化房地產策略的 IT 公司。

這一趨勢並不局限於 IT 領域,也受到了業務流程管理 (BPM) 領域的推動,該領域是通訊領域的主要企業。隨著工作性質的演變,企業越來越意識到敏捷的必要性,從而對靈活辦公空間的需求顯著增加。根據產業協會報告,就季度租賃交易而言,IT-BPM 領域佔約 32% 的佔有率,其次是彈性工作空間(15%)和 BFSI 領域(14%)。這種轉變意味著靈活的工作安排正得到越來越廣泛的接受,而 IT 和 BPM 則走在了最前沿,能夠快速適應不斷變化的勞動力動態。

越來越多的新興企業和小型企業選擇靈活的工作空間,這也使 IT 和通訊產業受益。在過去兩年(2022 年和 2023 年)中,該行業一直出現持續的新租賃需求,總計總合1000 萬平方英尺,主要受到跨國公司、新興企業、獨角獸、新創公司和海灣合作理事會衛星辦公室的需求推動。根據《印度快報》報道,預計這一勢頭將持續到 2024 年和 2025 年,每年成長 1,000 萬至 1,200 萬平方英尺。共享辦公環境使 IT 和通訊公司能夠享受最先進的基礎設施,而無需承擔傳統租賃的長期沉重承諾。這種轉變不僅將使這些產業受益,還將促進不同企業之間的合作和交流。

總之,IT 和通訊業對於塑造印度靈活辦公市場的成長軌跡至關重要。對適應性工作空間的日益依賴反映了產業向靈活性和創新性的廣泛轉變,確保這些產業將繼續處於工作場所轉型的前沿。

班加羅爾辦公室租賃激增推動市場發展

根據行業機構的資料,被稱為印度科技之都的班加羅爾在 2024 年的辦公室租賃活動中處於領先地位,從 1 月到 9 月吸收了驚人的 1640 萬平方英尺的面積。需求激增的一個關鍵促進因素是在班加羅爾強大的高科技環境中蓬勃發展的科技公司和全球能力中心 (GCC)。高科技產業佔總租賃量的 23%,這些公司尋求擁有最先進基礎設施和設施的空間。

根據《建築周刊》的報道,光是 2024 年第三季度,班加羅爾的房屋吸收量就達到 620 萬平方英尺,比去年同期顯著成長了 48%。超過 100,000 平方英尺的大型交易佔據了市場主導地位,佔租賃活動的 67%。預計到年終,總吸收量將達到創紀錄的約 2,000 萬平方英尺。雖然 IT-BPM 產業以 46% 的租賃佔有率處於領先地位,但 BFSI 產業在 24 年第三季也為該市的租賃活動貢獻了 23%。

班加羅爾、孟買、德里國家首都轄區和海得拉巴等主要城市活性化新空間收購,涉及 IT-BPM 和 BFSI 到工程、製造和靈活營運商等各個行業。 2024 年第三季度,需求繼續超過供應,儘管全國各地的供應量都有所增加,主要原因是班加羅爾和海得拉巴的竣工。這種差異凸顯了加快主要城市竣工的迫切需要,特別是在對優質甲級辦公空間的需求不斷增加的情況下。

根據該行業機構的關鍵要點,2024 年第三季將有 1,000 萬平方英尺的新建築竣工,其中班加羅爾和海得拉巴分別佔 50% 和 24%。班加羅爾處於領先地位,擁有 2020 萬平方英尺的靈活空間。值得注意的是,孟買、班加羅爾和德里國家首都轄區等一線城市的主要微型市場的平均辦公桌成本比其他地區高出 50%。據報道,到 2024 年 9 月,班加羅爾超過 80% 的租戶打算在未來幾年內透過靈活的空間擴大其投資組合。

總之,班加羅爾在辦公室租賃方面的主導地位及其強勁的靈活空間市場凸顯了其在推動印度靈活辦公市場方面的關鍵作用。班加羅爾能夠滿足不同行業的需求並專注於優質的基礎設施,這使其能夠很好地滿足不斷變化的佔用者的需求。

印度彈性辦公產業概況

印度彈性辦公市場的競爭格局由主要企業主導。由於技術進步降低了新參與企業的進入門檻,市場競爭日益激烈。為了確保競爭優勢,印度靈活辦公空間領域的公司正在推行包括策略夥伴關係、合併和收購在內的成長策略。主要參與企業包括 WeWork、Awfis、IndiQube、Simpliwork、The Hive、91 Springboard、Redbrics 和 Mumbai Co-working。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 當前市場狀況

- 科技趨勢

- 政府法規和舉措

- 辦公室租金洞察

- 深入了解印度推出彈性辦公室

- 洞察總體經濟和房地產貸款利率制度

- 地緣政治與疫情將如何影響市場

第5章 市場動態

- 市場促進因素

- 新興企業和小型企業的崛起

- 增加外國投資

- 市場限制

- 競爭激烈、飽和狀態

- 租賃靈活性

- 市場機會

- 正在崛起的二線城市

- 永續性與綠色計劃

- 波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 按類型

- 私人辦公室

- 聯合辦公室

- 虛擬辦公室

- 按最終用戶

- 資訊科技/通訊

- 媒體娛樂

- 零售和消費品

- 其他

- 按城市

- 德里

- 孟買

- 班加羅爾

- 海得拉巴

- 普納

- 印度其他地區

第7章 競爭格局

- 市場集中度概覽

- 公司簡介

- WeWork

- Mumbai Coworking

- Simpliwork

- The Hive

- Innov8

- 91Springboard

- IndiQube

- Skootr

- Awfis

- Smartworks

- Goodworks

- Spring House Coworking*

第 8 章:市場的未來

第 9 章 附錄

The India Flexible Office Space Market size is estimated at USD 2.30 billion in 2025, and is expected to reach USD 3.24 billion by 2030, at a CAGR of 7.05% during the forecast period (2025-2030).

Key Highlights

- Driven by the rise of hybrid work models, a demand for flexible leases, and evolving work cultures, India is witnessing a pronounced shift towards flexible office spaces. This trend has attracted a diverse clientele, spanning start-ups, SMEs, and major corporations. Their share of total office leasing has risen from 10.2% in 2019 to 12.7% in the first half of 2024. The uptake of flexible office seats surged from 85,234 in 2021 to 155,000 in 2023, with 106,554 seats leased in just the first half of 2024, as per the reports by Business Standard on September 2024.

- Reported by Industry Associations on Evolution on the Flex Space Industry, as of H1 2024, flexible workspaces across India's top eight cities spanned 58 Million Square Feet (MSF), representing 7-8% of the nation's total Grade A office supply. The first half of 2024 alone saw an addition of over 5 MSF to the flex supply, building on the previous two years' momentum, which saw increases of 8-9 MSF each year, with growth rates of 23% in 2022 and 18% in 2023.

- Over the past 3.5 years, the flexible workspace sector has enjoyed an impressive annual growth rate of 35-37%. Notably, 2024 is already on track, achieving nearly 70% of 2023's leasing figures. From Flex to Managed - Evolution of the Flex Space Industry, September 2024, a report from Industry Associations also details the distribution of flex space inventory in the top 8 cities: Bangalore dominates with 31% of the total stock, trailed by Delhi NCR (16%), Pune (14%), Hyderabad (14%), and Mumbai (11%). Moreover, there's a burgeoning demand for flexible workspaces in Tier II and III cities, spurred by workforce decentralization and a heightened focus on work-life balance. Nationwide, flexible spaces now represent 11-13% of total office space demand.

- Enterprises leveraging the Managed Office Solutions (MOS) model enjoy a suite of tailored services, allowing for a fully custom-built office and control over every aspect of their workspace. Among the 300+ operators in the market, the top 5% dominate, holding over 50% of the Grade A flex stock, with most centering their offerings around Managed Office Solutions (MOS).

- Information Technology (specifically business process management) leads the charge, making up 50% of 2024 absorption in flexible workspaces. They are followed by engineering and manufacturing at 18%, and banking, financial services, and insurance (BFSI) at 12%. Post-pandemic, rising costs and the feasibility of remote work have nudged these sectors towards flexible office solutions.

India Flexible Office Space Market Trends

Market Thrives on IT and Communication Sector Demand

India's flexible office space market is witnessing significant growth, primarily driven by the IT and Communication sectors. The surge in demand for these adaptable workspaces underscores their importance for companies transitioning to hybrid work models. Business Standard reports that in the first half of 2024, the IT sector was responsible for a substantial 50% of the total absorption of flexible office spaces, underscoring its dominant influence on the market. As businesses adapt to the post-pandemic landscape, the allure of flexible office solutions has intensified, especially for IT firms keen on optimizing their real estate strategies.

Beyond the IT realm, the Business Process Management (BPM) segment, a key player in the communication sector, is also fueling this trend. As the nature of work evolves, companies increasingly recognize the need for agility, leading to a marked uptick in demand for flexible office spaces. Reports from Industry Association, indicate that in quarterly leasing, IT-BPM segments commanded the lion's share at ~32%, trailed by flexible workspaces at 15% and the BFSI sector at 14%. This evolution signifies a wider acceptance of flexible work arrangements, with IT and BPM at the forefront, adapting swiftly to the changing workforce dynamics.

The IT and Communication sectors are also benefiting from the rise of startups and small-to-medium enterprises (SMEs) that are increasingly opting for flexible workspaces. Over the past two years, 2022 and 2023, the sector has consistently witnessed new leasing activities totaling around 10 million square feet, driven largely by demand from satellite offices of MNCs, MSMEs, unicorns, startups, and GCCs. This momentum is set to continue into 2024 and 2025, with projections of an annual growth of 10-12 million square feet as reported by India Breifing. By embracing coworking environments, IT and Communication companies gain access to state-of-the-art infrastructure without the burdensome long-term commitments of traditional leases. This shift not only serves the interests of these sectors but also fosters enhanced collaboration and networking among diverse enterprises.

In conclusion, the IT and Communication sectors are pivotal in shaping the growth trajectory of India's flexible office space market. Their increasing reliance on adaptable workspaces reflects a broader industry shift towards flexibility and innovation, ensuring these sectors remain at the forefront of workplace transformation in the years to come.

Bengaluru's Surge in Office Leasing Sets the Pace for Market

Bengaluru, often dubbed India's tech capital, spearheaded office leasing activities in 2024, absorbing a staggering 16.4 million square feet from January to September, as per Industry Association's data. This surge in demand predominantly stems from technology firms and Global Capability Centres (GCCs), both flourishing in Bengaluru's robust tech landscape. With the tech sector accounting for 23% of total leasing, companies are on the lookout for spaces boasting cutting-edge infrastructure and amenities, pivotal for high-stakes operations like R&D and data analytics.

As per reports from Construction Week, in Q3 2024 alone, Bengaluru witnessed an absorption of 6.2 million square feet, marking a notable 48% year-on-year uptick. Large transactions, each spanning 100,000 square feet or more, dominated the scene, making up 67% of the leasing activity. Projections suggest the city is on track to hit a record gross absorption of approximately 20 million square feet by year's end. While the IT-BPM sector remained the frontrunner with a 46% leasing share, the BFSI sector made its mark, contributing 23% to the city's leasing activities in Q3 2024.

Major cities, including Bengaluru, Mumbai, Delhi NCR, and Hyderabad, experienced heightened fresh space take-ups across diverse sectors, from IT-BPM and BFSI to engineering, manufacturing, and flexible operators. While Q3 2024 saw a nationwide uptick in supply, primarily fueled by completions in Bengaluru and Hyderabad, demand outpaced this supply. This disparity underscores the urgency for accelerated completions in major cities, especially as inquiries for premium Grade A spaces intensify.

Key highlights from Industry Associations, reveal that Q3 2024 witnessed 10 million square feet of new completions, with Bengaluru and Hyderabad claiming 50% and 24% shares, respectively. Leading the charge, Bengaluru boasts a flex space availability of 20.2 million square feet. Notably, the average desk cost in Tier I cities like Mumbai, Bengaluru, and Delhi NCR is 50% steeper in prime micro-markets than in other locales. By September 2024, reports indicate that over 80% of occupiers in Bengaluru are inclined to expand their portfolios with flexible spaces in the coming years.

In conclusion, Bengaluru's dominance in office leasing and its robust flex space market highlight its pivotal role in driving India's flexible office space market. The city's ability to cater to diverse sectors and its focus on quality infrastructure position it as a key player in meeting the evolving demands of occupiers.

India Flexible Office Space Industry Overview

Major international and domestic players populate the competitive landscape of India's flexible office space market. High competition characterizes this market, fueled by technological advancements that lower entry barriers for newcomers. To secure a competitive edge, companies in India's flexible office space arena pursue growth strategies, including strategic partnerships, mergers, and acquisitions. Some of the major players include WeWork, Awfis, IndiQube, Simpliwork, The Hive, 91 Springboard, Redbrics, Mumbai Co-working, etc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Government Regulations and Initiatives

- 4.4 Insights on Office Rents

- 4.5 Insights on Flexible Office Space Startups in India

- 4.6 Insights into Interest Rate Regime for General Economy and Real Estate Lending

- 4.7 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise of Startups and SMEs

- 5.1.2 Increase in Foreign Investment

- 5.2 Market Restraints

- 5.2.1 High Competition and Saturation

- 5.2.2 Lease Flexibility

- 5.3 Market Opportunities

- 5.3.1 Growing Tier - 2 Cities

- 5.3.2 Sustainability and Green Initiatives

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Private Officees

- 6.1.2 Coworking Offices

- 6.1.3 Virtual Offices

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.2.4 Other End Users

- 6.3 By City

- 6.3.1 Delhi

- 6.3.2 Mumbai

- 6.3.3 Bangalore

- 6.3.4 Hyderabad

- 6.3.5 Pune

- 6.3.6 Rest of India

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 WeWork

- 7.2.2 Mumbai Coworking

- 7.2.3 Simpliwork

- 7.2.4 The Hive

- 7.2.5 Innov8

- 7.2.6 91Springboard

- 7.2.7 IndiQube

- 7.2.8 Skootr

- 7.2.9 Awfis

- 7.2.10 Smartworks

- 7.2.11 Goodworks

- 7.2.12 Spring House Coworking*

8 FUTURE OF THE MARKET

9 APPENDIX

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年 共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年)

共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年) 亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F

共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F 共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測

共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測