|

市場調查報告書

商品編碼

1644508

印度共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)India Co-working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

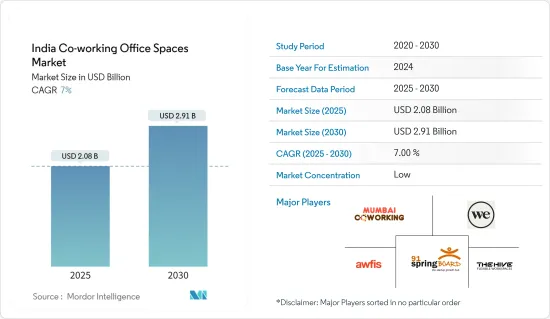

印度共享辦公空間市場規模預計在 2025 年達到 20.8 億美元,預計到 2030 年將達到 29.1 億美元,預測期內(2025-2030 年)的複合年成長率為 7%。

主要亮點

- 在傳統辦公空間面臨危機之際,疫情加速了中國共享辦公空間的成長。許多企業由於成本低廉和工作區域靈活而轉向共享辦公空間。共享辦公空間還能確保安全的工作環境。

- 該行業的發展受到自由工作者、中小型企業(SME)和新興企業日益成長的需求的推動。共享辦公空間以實惠的價格提供最好的設施,因此,即使是大型公司在意識到這一行業帶來的好處後也採用了共享辦公空間。此外,擁有大量投資流入的新興企業的增加也推動了該行業的強勁成長。

- 由於對靈活辦公空間的需求不斷成長,共享辦公空間產業去年開始呈現復甦跡象。共享辦公空間在印度企業中越來越受歡迎,過去四年需求加倍。 2023 年第一季,共享辦公空間占前七大城市 820 萬平方英尺總淨吸收量的 27%,較 2019 年第一季的 14% 大幅上升。

- 2023 年第一季,班加羅爾和國家首都地區 (NCR) 共佔共享辦公空間淨吸收總量的三分之二。同一時期,浦那和清奈共吸收了約 52 萬平方英尺的共同工作空間。排名前七位的城市的共享辦公空間淨吸收量顯著成長了 90%,從 2019 年第一季的 130 萬平方英尺擴大到 2023 年第一季的約 218 萬平方英尺。

- 班加羅爾的彈性旅遊營運商租賃佔有率最高,其次是孟買和德里國家首都轄區。在印度,新興企業最初推動了共享辦公空間的需求,隨後跨國公司和大型企業也開始增加對共享辦公空間的需求。

印度共享辦公空間市場趨勢

成本最佳化推動該產業大幅成長

在印度,共享辦公空間主要因為其成本效益而受到新興企業的青睞。使用者只需支付使用費和租金,無需任何額外費用,也沒有傳統辦公室的複雜手續或基礎設施維護、維修費用。新興企業最初的資本有限,因此具有業務成本低的優勢。在不斷變化的經濟環境中,不受限制性條款的長期租賃協議束縛的企業處於更有利的地位。共享辦公空間提供靈活的收費系統,您可以根據自己的確切需求混合搭配服務包。如果使用者需要減少或增加企劃團隊,例如如果一家公司正處於快速成長時期並需要更多的員工,那麼共享辦公空間可以隨時滿足這項要求。

企業收益是推動共享辦公空間需求的關鍵因素。與傳統辦公空間相比,共享辦公空間可節省 12-72% 的成本。傳統辦公空間的成本會迅速增加。傳統辦公空間的價格除了租賃費外,還包括水電費、網路費、技術支援和維護費。相反,共享辦公室會員資格通常包括公用設施、網路、技術支援和維護。各種規模的企業都在尋求降低共用工作空間的成本。

新興企業和自由工作者的崛起

共享辦公室生態系統最初是新興企業和自由工作者的一種選擇,現在已成為中小型企業的必需品。在潛在的1200萬至1600萬個座位容量中,有1030萬個座位已分配給大型企業。自由工作者與中小企業之間存在著150萬人的品質差距。

截至 2023 年 10 月 3 日,印度已鞏固其作為全球第三大新Start-Ups生態系統的地位,全國 763 個地區已有超過 1,12,718Start-Ups獲得 DPIIT 認可。在創新品質方面,印度在科學出版品質和大學品質方面排名世界第二,並躋身中等收入國家之列。印度的創新正在超越產業界限,新興企業正在應對 56 個不同垂直產業的挑戰。值得注意的是,13% 的新興企業從事 IT 服務業,9% 從事醫療保健和生命科學業,7% 從事教育業,5% 從事農業業,5% 從事食品和飲料業。

最小的是擁有10萬個座位的新興企業。隨著從傳統辦公室向靈活工作空間的重大轉變越來越被廣泛接受,越來越多的中小型企業開始採用聯合辦公,因為它具有成本效益、靈活性、技術整合、卓越的基礎設施、更高的生產力、即插即用解決方案、網路機會等。這使得中小型企業可以省去管理財產的麻煩,並專注於核心業務。

印度共享辦公空間產業概況

印度的共同工作空間市場分散,既有全球參與者,也有本地參與者。該市場的一些主要企業包括 91 Springboard、Awfis、WeWork 和 Mumbai Coworking。越來越多的企業正在加緊努力,滿足人們對休閒辦公環境日益成長的需求。印度共享辦公空間市場中的公司正在採取策略聯盟、合併和收購等多種成長和擴大策略,以獲得競爭優勢。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 市場動態

- 市場促進因素

- Start-Ups公司的崛起

- 開發永續的共享工作空間

- 市場限制

- 遠距工作增加

- 印度傳統的工作文化與共享辦公空間的開放、協作環境並不相容。

- 市場機會

- 增強技術整合

- 市場促進因素

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者/購買者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 政府法規和舉措

- 產業價值鏈分析

- 市場技術趨勢

- 洞察印度共享辦公新興企業

- 新冠肺炎疫情對市場的影響

第5章 市場區隔

- 按類型

- 靈活管理辦公室

- 服務式辦公室

- 按應用

- 資訊科技(IT 和 ITES)

- 法律服務

- BFSI(銀行、金融服務、保險)

- 諮詢

- 其他服務

- 按最終用戶

- 個人用戶

- 小型企業

- 大型企業

- 其他最終用戶

- 按主要城市

- 德里

- 孟買

- 班加羅爾

- 其他城市

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Mumbai Coworking

- We Work-BKC

- Innov8-Vikhroli

- 91 springboard

- Spring House Coworking

- Indi Qube

- Skootr

- Awfis CBD

- Smartworks

- Goodworks

- Cowrks

- Hive

- 其他公司

第7章:市場的未來

第 8 章 附錄

The India Co-working Office Spaces Market size is estimated at USD 2.08 billion in 2025, and is expected to reach USD 2.91 billion by 2030, at a CAGR of 7% during the forecast period (2025-2030).

Key Highlights

- The pandemic accelerated the growth of co-working spaces in the country, as traditional workspaces faced challenges during the crisis. Many enterprises moved toward co-working spaces because of affordable prices and flexibility in working areas. Also, co-working spaces ensure to provide a safe working environment.

- The sector is driven by increasing demand from freelancers, small and medium-scale enterprises (SMEs), and startups. Because the industry provides top facilities at affordable prices, large-scale enterprises are also adopting co-working spaces after realizing the benefits offered by the industry. Also, the increasing number of startups with high investment flow rates has resulted in robust sector growth.

- The previous year has seen a rebound in the co-working space industry, driven by the increased demand for flexible office space. Co-working spaces have grown in popularity among businesses in India, with demand doubling over the past four years. In the first quarter of 2023, co-working spaces accounted for 27% of the net absorption of 8.2 million sq. ft. across the top seven cities, marking a substantial rise from 14% in Q1 2019.

- Bengaluru and the National Capital Region (NCR) together comprised two-thirds of the net absorption of co-working spaces during Q1 2023. Pune and Chennai collectively absorbed about 0.52 million sq. ft. of co-working spaces in the same period. The top seven cities experienced a remarkable 90% growth in net absorption of co-working spaces, escalating from 1.3 million sq. ft. in Q1 2019 to approximately 2.18 million sq. ft. in Q1 2023.

- Bengaluru accounted for the highest share of leasing by Flexi operators, followed by Mumbai and Delhi-NCR. Startups first led the demand for co-working office spaces in India before MNCs and large enterprises took the plunge by taking up space in co-working office spaces.

India Co-working Office Spaces Market Trends

Cost Optimization is Driving the Significant Growth in the Sector

In India, startups mainly prefer co-working spaces for cost-effectiveness. Users only pay for what they use and rent, nothing extra, and there are no hassles or spending on infrastructure maintenance and repair, which conventional offices include. Since startups initially function on limited capital, lower costs of performing work are in their favor. Companies not bound by long-term lease contracts with strict terms in a regularly changing economic environment will be better positioned. Co-working spaces offer flexible tariffs that can combine service packages, such as choosing precisely what suits users' needs. In case users need to reduce or, on the contrary, increase the project team, for example, if companies enter a period of rapid growth and need more employees, using co-working spaces can always do it.

The companies' bottom lines are a crucial factor driving demand for co-working space. Based on locations nationwide, co-working offers a 12-72% cost reduction compared to traditional office space. The cost of traditional office space quickly adds up. In addition to lease payments, prices for conventional office space include utilities, internet, and tech support and maintenance. Conversely, utilities, internet, tech support, and maintenance are typically included in co-working memberships. Businesses of all sizes have caught on to the cost savings of shared workspace.

Increasing Number of Startups and Freelancers in the Country

Co-working ecosystem, initially the go-to option for startups and freelancers, has become a prerequisite for SMEs. The biggest chunk of 10.3 million seats out of the total 12-16 million potential seats is ascribed to large companies. There is a quality divide of 1.5 million each among freelancers and SMEs.

As of October 3, 2023, India cemented its position as the third-largest startup ecosystem globally, boasting over 112,718 startups recognized by DPIIT across 763 districts nationwide. Regarding innovation quality, India ranks second globally, excelling particularly in the quality of scientific publications and the caliber of its universities among middle-income economies. Innovation in India transcends specific sectors, with startups addressing challenges across 56 diverse industrial domains. Notably, 13% of these startups operate in IT services, 9% in healthcare and life sciences, 7% in education, 5% in agriculture, and 5% in food and beverages.

The most minor lot is formed by startups at 100,000 seats. With a substantial shift from traditional offices to flexible workspaces attaining widespread acceptance, more SMEs are embracing coworking due to cost efficiency, flexibility, tech integrations, superior infrastructure, enhanced productivity, plug-and-play solutions, and networking opportunities. Thus, they can concentrate on their fundamental business minus the hassle of managing real estate.

India Co-working Office Spaces Industry Overview

The Indian co-working office space market is fragmented, with global and local co-working market players. Some of the key players in the market are 91 Springboard, Awfis, WeWork, and Mumbai Coworking. Also, many more are entering the need to fulfill the rapid demand for casual environment offices. Companies in the Indian co-working office space market are involved in several growth and expansion strategies, such as strategic partnerships, mergers, and acquisitions, to gain a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increase in Number of Startups

- 4.2.1.2 The Development of Sustainable Co-working Spaces

- 4.2.2 Market Restraints

- 4.2.2.1 A Rise in Remote Work

- 4.2.2.2 Traditional Work Culture in India, Which May Not Align Well With the Open and Collaborative Environment of Co-working Spaces

- 4.2.3 Market Opportunities

- 4.2.3.1 Enhanced Technology Integration

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers/Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain Analysis

- 4.6 Technology Trends in the Market

- 4.7 Insights on Co-working Startups in India

- 4.8 Impact of the COVID - 19 Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Flexible Managed Office

- 5.1.2 Serviced Office

- 5.2 ByApplication

- 5.2.1 Information Technology (IT and ITES)

- 5.2.2 Legal Services

- 5.2.3 BFSI (Banking, Financial Services, and Insurance)

- 5.2.4 Consulting

- 5.2.5 Other Services

- 5.3 By End User

- 5.3.1 Personal User

- 5.3.2 Small Scale Company

- 5.3.3 Large Scale Company

- 5.3.4 Other End Users

- 5.4 By Key Cities

- 5.4.1 Delhi

- 5.4.2 Mumbai

- 5.4.3 Bangalore

- 5.4.4 Other Cities

6 Competitive Land Scape

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Mumbai Coworking

- 6.2.2 We Work-BKC

- 6.2.3 Innov8-Vikhroli

- 6.2.4 91 springboard

- 6.2.5 Spring House Coworking

- 6.2.6 Indi Qube

- 6.2.7 Skootr

- 6.2.8 Awfis CBD

- 6.2.9 Smartworks

- 6.2.10 Goodworks

- 6.2.11 Cowrks

- 6.2.12 Hive*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年

印度的共享辦公空間市場評估:各類型,各行業,各終端用戶,不同商業模式,各地區,機會,機會及預測,2018~2032年 共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年)

共享辦公空間管理軟體市場報告:趨勢、預測和競爭分析(至 2031 年) 亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球辦公空間 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

印度彈性辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

拉丁美洲共享辦公空間:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

歐洲的共同工作空間 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

英國共享辦公室:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F

共享辦公空間市場 - 全球產業規模、佔有率、趨勢、機會和預測,按設施、目標受眾、增值服務、地區和競爭細分,2019-2029F 共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測

共享辦公空間市場:按業務類型、最終用戶分類 - 2025-2030 年全球預測