|

市場調查報告書

商品編碼

1644920

亞太地區抽水蓄能:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Asia-Pacific Pumped Hydro Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

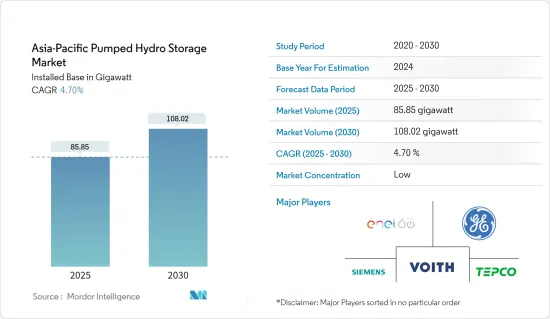

亞太地區抽水蓄能發電市場預計將從 2025 年的 85.85 GW 擴大到 2030 年的 108.02 GW,預測期內(2025-2030 年)的複合年成長率為 4.7%。

關鍵亮點

- 從中期來看,受可再生能源日益普及以及政府支持政策等因素影響,亞太地區抽水蓄能發電市場預計將實現成長。

- 另一方面,其他能源儲存技術的競爭預計將威脅該地區抽水蓄能市場的成長。

- 預計抽水蓄能技術的不斷進步將在預測期內為市場創造重大機會。

- 由於政府努力增加抽水蓄能容量,預計未來幾年中國將佔據最大的市場佔有率。儘管如此,抽水蓄能技術的不斷進步預計將在預測期內為市場創造重大機會。

- 由於政府努力增加抽水蓄能容量,預計未來幾年中國將佔據最大的市場佔有率。

亞太地區抽水蓄能電力市場趨勢

閉合迴路部分預計將顯著成長

- 在閉合迴路系統中,抽水蓄能電站的建造方式是,一個或兩個水庫都是人工建造的,並且沒有自然的水流入。封閉回路型抽水蓄能具有高度的靈活性、可靠性和高功率。閉合迴路蓄能系統對環境的影響比開放回路抽水蓄能系統小,因為它們不與現有的河流系統相連。此外,它們可以安裝在需要電網支援的位置。

- 根據國際可再生能源機構預測,2022年亞洲純抽水蓄能裝置容量將達80,988兆瓦,為全球最高。由於該地區對封閉回路型蓄能電站的需求不斷成長,過去五年來其容量一直在穩步增加。

- 例如,2023 年 5 月,Rewa Ultra Mega Solar Ltd (RUMSL) 啟動了一項提案請求 (RFP) 流程,為中央邦總合13.8 吉瓦的抽水蓄能 (PHS)計分類配場地。該提案總合涉及 12 個站點,開發商可以在這些站點安裝 600MW 至 2GW 的 PHS 容量。

- 澳洲調查團隊得出結論,封閉回路型抽水蓄能電站有可能在不久的將來超越開放回路型PSH電站,因為它們克服了為抽水蓄能電站尋找合適位置的難題,並且具有對水資源沒有環境影響等優勢。

- 此外,閉合迴路蓄能具有高度的靈活性、可靠性和電力輸出。選擇這種方式的另一個主要原因是它不會干擾現有的河流系統或水流,從而更容易獲得經營許可證和許可證。

- 這些因素為預測期內封閉回路型抽水蓄能發電市場明顯發展動能鋪平了道路。

中國可望主導市場

- 中國引領全球水力發電市場,截至 2022 年,可再生水力發電裝置容量約 3,677 萬千瓦。水力發電約佔總發電量的16%。中國也正在努力發展抽水蓄能水力發電,特別是製定了新的政策和計劃目標。

- 2022年,全國淨抽水蓄能發電裝置容量約4,579萬千瓦,位居亞洲國家之首。在政府和民間組織的努力下,這項技術將在中國進一步蓬勃發展。

- 例如,2022年6月,中國電力建設集團宣布,已開工興建200座抽水蓄能電站,至2025年新增抽水蓄能容量2,700萬千瓦。預計將使中國的儲能裝置容量增加約10%,全球能源儲存裝置容量增加約170%。

- 此外,2022年1月,中國在河北省運作世界上最大的抽水蓄能電站。 360千萬瓦抽水蓄能電站由12台30萬千瓦可逆式水泵發電機組組成,總儲能發電量為66億千瓦時。

- 2023年11月,國家電網公司位於中國西北新疆維吾爾自治區的阜康抽水蓄能電廠完工投產。該計劃將採用三台30萬千瓦風力渦輪機,總發電量為120萬千瓦。這是中國西北地區第一座此類發電廠。

- 預計此類發展將在不久的將來推動該國抽水蓄能電力市場的發展。

亞太抽水蓄能產業概況

亞太地區抽水蓄能電力市場呈現細分化。主要企業(不分先後順序)包括 Enel SpA、通用電氣公司、西門子股份公司、Voith GmBH & Co. KGAa 和東京電力公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場概況

- 介紹

- 至2028年裝置容量及預測(單位:GW)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 可再生能源整合

- 政府支持措施和政策

- 限制因素

- 與其他能源儲存技術的競爭

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 類型

- 開放回路

- 閉合迴路

- 2028 年市場規模與需求預測(按地區)

- 中國

- 韓國

- 印度

- 日本

- 其他亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Enel SpA

- General Electric Company

- Siemens AG

- Voith GmBH & Co. KGaA

- Tokyo Electric & Power Company

- Stantec

- Black & Veatch Holding Company

- Andritz AG

第7章 市場機會與未來趨勢

- 不斷提高的技術進步

簡介目錄

Product Code: 93141

The Asia-Pacific Pumped Hydro Storage Market size in terms of installed base is expected to grow from 85.85 gigawatt in 2025 to 108.02 gigawatt by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing adoption of renewable energy coupled with supportive government policies are projected to thrive in the Asia-Pacific pumped hydro storage market.

- On the other hand, the competition from other energy storage technologies is expected to threaten the growth of the pumped hydro storage market in the region.

- Nevertheless, the growing technological advancements in pumped hydro storage technology are expected to create significant opportunities for the market during the forecasted period.

- China is predicted to capture the largest market share in the coming years due to government initiatives to increase the pumped hydro storage capacity.Nevertheless, the growing technological advancements in pumped hydro storage technology are expected to create significant opportunities for the market during the forecasted period.

- China is predicted to capture the largest market share in the coming years due to government initiatives to increase the pumped hydro storage capacity.

Asia-Pacific Pumped Hydro Storage Market Trends

Closed-loop Segment is Expected to Witness Significant Growth

- In closed-loop systems, pumped hydro storage plants are created so that one or both the reservoirs are artificially built, and no natural water inflow is involved with either of them. Closed-loop pumped hydro storage offers high flexibility, reliability, and high-power output. Since the closed-loop pumped-hydro systems are not connected to existing river systems, their impact on the environment is less compared to open-loop pumped hydro storage systems. Moreover, they can be positioned where support for the grid is required.

- According to the International Renewable Energy Agency, the capacity of installed pure pumped hydro storage in Asia was recorded at 80,988 MW in 2022, the highest among all the regions across the world. The capacity grew consistently in the last five years due to the growing demand for closed-loop pumped hydro storage plants in the region.

- For instance, in May 2023, Rewa Ultra Mega Solar Ltd (RUMSL) initiated a Request for Proposal (RFP) process to allocate locations for a combined 13.8 GW of pumped hydro storage (PHS) projects in Madhya Pradesh. The offering includes a total of 12 sites where developers can establish PHS capacities ranging from 600 MW to 2 GW.

- A research team from Australia has concluded through a research study that the closed-loop pumped hydro storage plants may overshadow the open-loop PSH plants in the near future due to the benefits they provide, like overcoming the problem of finding suitable sites for pumped hydro storage plant location, and no environmental effects on water resources.

- Furthermore, closed-loop pumped hydro storage offers high flexibility, reliability, and power output. The other major factor for their preference is the certainty of gaining an operating license or permit since they do not interfere with the existing river systems or any water streams.

- Such factors pave the way for an explicitly visible momentum for the closed-loop pumped hydro storage market during the forecast period.

China is Expected to Dominate the Market

- China led the global hydropower market with around 36.77 GW of renewable hydropower capacity as of 2022. Hydro sources constitute about 16% of the total electricity generation mix. The country is also strenuously working on a lucid pumped hydro storage development, particularly with new policies and project goals.

- In 2022, the country's pure pumped hydro storage installed capacity was around 45.79 GW, the highest among all the Asian countries. The technology is set to bloom even more in China due to the efforts made by the government and private entities.

- For example, in June 2022, the Power Construction Corporation of China announced that it had started working on the new 270 GW of pumped hydro storage capacity to be added to the country's electricity mix, with the installation of 200 pumped hydro storage plants by 2025. It is expected to raise China's installed capacity by around 10% and the world's energy storage capacity by about 170%.

- Furthermore, in January 2022, the country commissioned the world's largest pumped hydro storage plant in China's Hebei province. The 3.6 GW pumped hydro storage facility consists of 12 reversible pumps generating sets with 300 MW each and possesses a power generation capacity from storage of 6.6 billion kWh.

- In November 2023, the State Grid Corporation of China inaugurated the Fukang pumped-storage power station in northwest China's Xinjiang region. The project features three 300 MW turbines with a total capacity of 1.2 GW. The facility is the first of its kind in northwestern China.

- Such developments are projected to drive the pumped hydro storage market in the country in the near future.

Asia-Pacific Pumped Hydro Storage Industry Overview

The Asia-Pacific pumped hydro storage market is fragmented. Some of the key players (in no particular order) include Enel SpA, General Electric Company, Siemens AG, Voith GmBH & Co. KGAa, and Tokyo Electric & Power Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Renewable Energy Integration

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Competition with Other Energy Storage Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Open Loop

- 5.1.2 Closed Loop

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 China

- 5.2.2 South Korea

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Enel SpA

- 6.3.2 General Electric Company

- 6.3.3 Siemens AG

- 6.3.4 Voith GmBH & Co. KGaA

- 6.3.5 Tokyo Electric & Power Company

- 6.3.6 Stantec

- 6.3.7 Black & Veatch Holding Company

- 6.3.8 Andritz AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Advancements

02-2729-4219

+886-2-2729-4219

抽水蓄能發電:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

抽水蓄能發電:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2025年全球抽水蓄能市場報告北美抽水蓄能能源:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲抽水蓄能儲能:市場佔有率分析、產業趨勢與成長預測(2025-2030)

2025年全球抽水蓄能市場報告北美抽水蓄能能源:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美洲抽水蓄能儲能:市場佔有率分析、產業趨勢與成長預測(2025-2030) 抽水蓄能能源市場:按類型、應用和最終用途分類-2025-2030 年全球預測

抽水蓄能能源市場:按類型、應用和最終用途分類-2025-2030 年全球預測 抽水蓄能市場規模 - 按系統類型(開迴路、閉迴路、創新)、區域展望和預測,2024 年至 2032 年

抽水蓄能市場規模 - 按系統類型(開迴路、閉迴路、創新)、區域展望和預測,2024 年至 2032 年 全球抽水蓄能發電市場:市場規模與佔有率分析(依類型(開環、閉環))、工業需求預測(截至2030年)

全球抽水蓄能發電市場:市場規模與佔有率分析(依類型(開環、閉環))、工業需求預測(截至2030年) 抽水蓄能發電市場:按類型和地區分類

抽水蓄能發電市場:按類型和地區分類