|

市場調查報告書

商品編碼

1645034

美國藥品倉儲:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)US Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

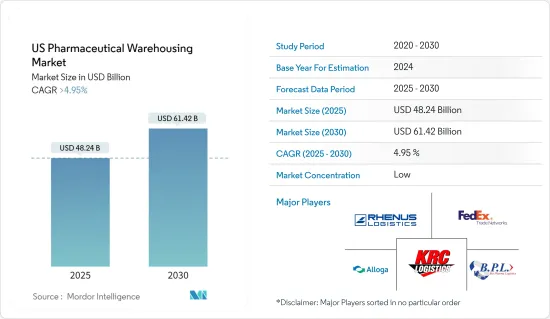

美國醫藥倉儲市場規模預計在 2025 年為 482.4 億美元,預計到 2030 年將達到 614.2 億美元,預測期內(2025-2030 年)的複合年成長率將超過 4.95%。

美國製藥業以開發突破性藥物而聞名,在推動醫療保健產業成長方面發揮關鍵作用。然而,許多高成本藥物的推出導致醫療成本上升,影響私人組織和聯邦政府。

作為回應,政策制定者正在積極尋求控制藥品價格和減少聯邦藥品支出的策略。此類支出涵蓋一系列活動,從新藥研發和測試到產品擴展、安全性和啟動臨床試驗等漸進式創新。

在強大的專科藥物管道和越來越多的品牌製造商的支持下,到 2023 年美國醫藥市場將成長 7.8%,達到 2,325 家公司。

FDA 在 2023 年核准了55 種新藥,預示著核准的復甦。這一成長與一些公司在專利到期前為增強其投資組合而進行的策略性收購相吻合。全球疫苗接種運動和持續的治療需求支撐了該行業強勁的生產和銷售。

到 2028 年,藥品淨支出預計將比 2023 年的水準激增 1,270 億美元,這主要得益於產量成長。雖然採用技術創新將成為關鍵驅動力,但它也會受到通常導致價格下降的因素(例如專利到期和立法影響)的限制。

隨著加速創新和藥物引進的壓力越來越大,製藥公司正在利用新的機會。科學突破正在推動製造業新一輪創新浪潮,而美國食品藥物管理局(FDA)務實的監管立場則加速了這一進程。這次合作加速了救命藥物和療法進入市場。

由於對高效儲存和配送解決方案的需求不斷增加,美國醫藥倉儲市場也正在經歷顯著成長。隨著製藥業的擴張,對確保藥品安全合規儲存的先進倉儲設施的需求變得至關重要。

這些設施配備了最尖端科技,以保持藥品處於最佳狀態,從而支援整個行業供應鏈。預計市場將繼續保持上升趨勢,與製藥行業的整體成長趨勢保持一致。

美國醫藥倉儲市場趨勢

受控物流包裝的興起

由於對溫度敏感的藥品和疫苗的重要性日益增加,製藥公司、醫療機構和物流供應商越來越重視低溫運輸物流包裝。生技藥品和某些疫苗的有效性取決於精確溫度下的儲存和運輸。轉向受控物流包裝對於避免產品劣化至關重要,鞏固低溫運輸包裝作為製藥行業的重要組成部分的地位。

網路藥品訂購系統的普及進一步刺激了低溫運輸物流包裝的擴張。隨著越來越多的消費者和醫療保健提供者轉向線上平台和直接面向患者的運輸,對高效溫控包裝解決方案的需求日益成長。利用低溫運輸物流進行安全可靠的運送,使供應商能夠接觸到更廣泛的市場,同時保護醫藥產品的完整性。

2023年11月,Cryopak Eco GelTM推出了低溫運輸物流領域的突破性解決方案,為傳統冷媒提供了一種永續的、環保的替代品。白皮書深入探討了該產品的顯著屬性,包括 FDA核准、生物分解性和可回收性,強調了其在不同行業中推動永續實踐的潛力。

因此,美國醫藥倉儲市場對受控物流包裝的需求正在顯著增加。此舉體現了業界對維持產品功效和滿足對溫度敏感藥物和疫苗日益成長的需求的承諾。 Cryopak Eco GelTM 等先進低溫運輸解決方案的採用進一步推動了這一成長,凸顯了市場向更永續、更可靠的包裝實踐的轉變。

醫院和診所發展加快

美國擁有約 6,120 家醫院,包括學術醫療中心和教學醫院,擁有各種各樣的非聯邦短期醫療設施。這些醫院在美國各地的藥品消費中發揮著至關重要的作用。美國有 6,200 多所醫院和 400 個醫療系統發揮至關重要的作用,並對醫療保健的提供產生了重大影響。

作為急性和專科護理的主要提供者,這些組織決定了藥品採購和使用的趨勢。醫療機構的強烈需求表明醫療保健領域將繼續進行合作和策略性舉措,以改善患者治療效果並簡化業務。

在美國,有 31,748 家診所提供醫療保健框架,包括醫療、心理健康和婦女服務。這些診所不僅提供全面的醫療服務,也加強了該國對優質醫療保健的奉獻精神。

德克薩斯州擁有 4,661 家診所,凸顯了其強大的醫療保健基礎設施。包括華盛頓州、密蘇裡州和明尼蘇達州在內的其他州也強調了滿足居民醫療需求的承諾。此次擴建凸顯了日益成長的醫療服務需求以及該診所在整個醫療保健體系中的戰略重要性。

美國醫院和診所數量的不斷增加對醫藥倉儲市場產生了重大影響。隨著這些醫療設施的擴大,對高效能藥品儲存和分銷解決方案的需求也日益成長。

這項發展凸顯了醫藥倉庫在支持醫療保健基礎設施、確保及時安全地運送藥品以滿足全國各地醫院和診所日益成長的需求方面的重要作用。

美國藥品倉儲產業概況

美國藥品倉儲市場競爭激烈,既有多家大型企業,也有中小型公司。一些主要參與者將透過擴大其地理影響力、增強其服務產品以及投資新技術和自動化來保持相關性。

主要參與者包括 Alloga、BioPharma Logisics、Rhenus SE and Co.KG、ADAllen Pharma、WH BOWKER LTD、Pulleyn Transport Ltd、TIBA、Schenker AG、CEVA Logistics 和 DACHSER Group SE and Co.KG。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態與洞察

- 市場概況

- 市場促進因素

- 製藥業的成長

- 溫控儲存需求不斷成長

- 市場限制

- FDA 對藥品倉庫的嚴格規定

- 市場機會

- 政府推出新措施加強醫藥倉庫

- 電子商務日益普及

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 地緣政治與疫情將如何影響市場

第5章 市場區隔

- 按服務類型

- 貯存

- 分配

- 庫存管理

- 包裝

- 其他

- 按模式

- 低溫運輸倉庫

- 非低溫運輸倉庫

- 按最終用戶

- 製藥公司

- 醫院和診所

- 研究和政府組織

- 其他

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Alloga

- Bio Pharma Logistics

- Rhenus SE and Co. KG

- ADAllen Pharma

- DB Schenker

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Hellmann Worldwide Logistics SE and Co KG

- KRC Logistics

- Kuehne Nagel Management AG

- United Parcel Service Inc.

- XPO Logistics Inc.*

- 其他公司

第7章:市場的未來

第 8 章 附錄

- 宏觀經濟指標(GDP分佈,依活動分類)

- 經濟統計 - 運輸及倉儲業對經濟的貢獻

- 相關藥品進出口統計

The US Pharmaceutical Warehousing Market size is estimated at USD 48.24 billion in 2025, and is expected to reach USD 61.42 billion by 2030, at a CAGR of greater than 4.95% during the forecast period (2025-2030).

The U.S. pharmaceutical industry, celebrated for its groundbreaking drug developments, plays a pivotal role in propelling the healthcare sector's growth. However, the introduction of many high-priced medications has led to surging healthcare costs, impacting both private entities and the federal government.

In response, policymakers are actively seeking strategies to curtail drug prices and diminish federal drug-related expenditures. These expenditures span a spectrum of activities, from the discovery and testing of novel drugs to incremental innovations like product extensions and clinical testing for safety and marketing.

Bolstered by a strong pipeline of specialty drugs and a rising count of brand-name manufacturers, the U.S. pharmaceutical market witnessed a 7.8% growth, reaching 2,325 businesses in 2023.

The FDA granted approvals to 55 new drugs in 2023, signaling a resurgence in approvals. This uptick coincides with strategic acquisitions by companies aiming to bolster their portfolios in anticipation of patent expirations. The sector's robust output and sales are buoyed by a global vaccination drive and a consistent demand for medical treatments.

By 2028, net spending on medicines is projected to surge by USD 127 billion from 2023 levels, driven primarily by volume growth. While the adoption of innovations will be a key growth driver, it will be tempered by factors like patent expirations and legislative impacts, which typically lead to lower prices.

Amidst pressures to hasten innovation and drug introductions, pharmaceutical manufacturers are capitalizing on emerging opportunities. Scientific breakthroughs are ushering in a fresh wave of innovations in manufacturing, a momentum further bolstered by the U.S. Food and Drug Administration's (FDA) pragmatic regulatory stance. This collaboration is expediting the market entry of lifesaving medicines and therapeutics.

The United States pharmaceutical warehousing market is also experiencing significant growth, driven by the increasing demand for efficient storage and distribution solutions. As the pharmaceutical industry expands, the need for advanced warehousing facilities that ensure the safe and compliant storage of drugs becomes paramount.

These facilities are equipped with state-of-the-art technology to maintain optimal conditions for pharmaceuticals, thereby supporting the industry's overall supply chain. The market is expected to continue its upward trajectory, aligning with the broader growth trends in the pharmaceutical sector.

US Pharmaceutical Warehousing Market Trends

Increase in Controlled Logistics Packaging

Pharmaceutical companies, healthcare facilities, and logistics providers are increasingly prioritizing cold chain logistics packaging due to a heightened emphasis on temperature-sensitive medications and vaccines. The efficacy of biologics and certain vaccines hinges on their storage and transportation at precise temperatures. This pivot towards controlled logistics packaging is vital to avert product degradation, solidifying cold chain packaging as an essential component of the pharmaceutical industry.

The surge in online medication ordering systems has further fueled the expansion of cold chain logistics packaging. With a growing number of consumers and healthcare providers turning to online platforms and direct-to-patient deliveries, the need for efficient temperature-controlled packaging solutions has escalated. By leveraging cold chain logistics for safe and reliable deliveries, providers can tap into a wider market while safeguarding the integrity of pharmaceutical products.

In November 2023, Cryopak Eco GelTM introduced a groundbreaking solution in cold chain logistics, presenting a sustainable and eco-friendly alternative to conventional refrigerants. This white paper delves into the product's standout attributes, including FDA approval, biodegradability, and recyclability, and underscores its potential to propel sustainable practices across diverse industries.

As a result, the United States pharmaceutical warehousing market has seen a significant increase in controlled logistics packaging. This trend reflects the industry's commitment to maintaining product efficacy and meeting the growing demand for temperature-sensitive medications and vaccines. The adoption of advanced cold chain solutions like Cryopak Eco GelTM further supports this growth, highlighting the market's shift towards more sustainable and reliable packaging methods.

The Rise in Development of Hospitals and Clinics

With around 6,120 hospitals, including academic medical centers and teaching hospitals, the U.S. boasts a diverse array of nonfederal, short-term facilities. These hospitals play a pivotal role in the nation's pharmaceutical consumption. Over 6,200 hospitals and 400 health systems across the country are key players, significantly influencing healthcare delivery.

As primary providers of acute and specialized care, these institutions shape trends in pharmaceutical procurement and usage. Their strong demand signals ongoing collaborations and strategic moves within the healthcare sector, all aimed at boosting patient outcomes and streamlining operations.

In the U.S., 31,748 clinics, spanning medical, mental health, and women's health services, are integral to the healthcare framework. These clinics not only deliver comprehensive medical care but also reinforce the nation's dedication to healthcare excellence.

Texas tops the list with 4,661 clinics, highlighting its robust healthcare infrastructure, while California closely follows with 4,584. Other states like Washington, Missouri, and Minnesota also stand out, emphasizing their commitment to meeting the healthcare needs of their residents. This expansion underscores the rising demand for medical services and the strategic significance of clinics in the broader healthcare delivery system.

The rise in the development of hospitals and clinics in the United States has significantly impacted the pharmaceutical warehousing market. As these healthcare facilities expand, the demand for efficient pharmaceutical storage and distribution solutions has grown.

This trend highlights the critical role of pharmaceutical warehousing in supporting the healthcare infrastructure, ensuring timely and safe delivery of medications to meet the increasing needs of hospitals and clinics nationwide.

US Pharmaceutical Warehousing Industry Overview

The United States Pharmaceutical Warehousing Market is a highly competitive market with the presence of several large players as well as small and medium-sized companies. Some of the key players are focusing on expanding their geographic presence, enhancing their service offerings, and investing in new technologies and automation to remain in the market.

Some of the major players are Alloga, BioPharma Logisics, Rhenus SE and Co. KG, ADAllen Pharma, WH BOWKER LTD, Pulleyn Transport Ltd, TIBA, Schenker AG, CEVA Logistics and DACHSER Group SE and Co. KG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of the pharmaceutical industry

- 4.2.2 Increasing demand for temperature-controlled storage

- 4.3 Market Restraints

- 4.3.1 Stringent FDA rules & regulations towards Pharmaceutical Warehousing

- 4.4 Market Opportunities

- 4.4.1 Rise in government initiatives to enhance Pharmaceutical Warehousing

- 4.4.2 Growing popularity of e-commerce

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution

- 5.1.3 Inventory Management

- 5.1.4 Packaging

- 5.1.5 Others

- 5.2 By Mode

- 5.2.1 Cold Chain Warehouse

- 5.2.2 Non-Cold Chain Warehouse

- 5.3 By End User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Hospital and Clinics

- 5.3.3 Research Institiutes and Government Agencies

- 5.3.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Alloga

- 6.2.2 Bio Pharma Logistics

- 6.2.3 Rhenus SE and Co. KG

- 6.2.4 ADAllen Pharma

- 6.2.5 DB Schenker

- 6.2.6 FedEx Corp.

- 6.2.7 GEODIS SA

- 6.2.8 CEVA Logistics

- 6.2.9 Hellmann Worldwide Logistics SE and Co KG

- 6.2.10 KRC Logistics

- 6.2.11 Kuehne Nagel Management AG

- 6.2.12 United Parcel Service Inc.

- 6.2.13 XPO Logistics Inc.*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, By Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 Export and Import Statistics of Related Pharmaceutical Products

2025 年至 2033 年化學品倉儲和儲存市場報告,按類型(一般倉庫、專業倉庫)、應用(大宗化學品、特種化學品)和地區分類

2025 年至 2033 年化學品倉儲和儲存市場報告,按類型(一般倉庫、專業倉庫)、應用(大宗化學品、特種化學品)和地區分類 2025-2029 年全球食品飲料倉儲市場

2025-2029 年全球食品飲料倉儲市場 全球醫藥倉儲市場(2025-2029)

全球醫藥倉儲市場(2025-2029) 2025-2033 年按倉庫類型、所有權、最終用途和地區分類的倉儲市場報告

2025-2033 年按倉庫類型、所有權、最終用途和地區分類的倉儲市場報告 智慧倉庫市場分析及預測(截至 2033 年),按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類

智慧倉庫市場分析及預測(截至 2033 年),按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類 中國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 德國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

德國醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

歐洲醫藥倉儲:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 2025-2029年全球倉儲市場

2025-2029年全球倉儲市場 倉儲市場:按類型、所有者、技術、最終用戶產業分類 - 2025-2030 年全球預測

倉儲市場:按類型、所有者、技術、最終用戶產業分類 - 2025-2030 年全球預測