|

市場調查報告書

商品編碼

1683091

歐洲建築化學品市場 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

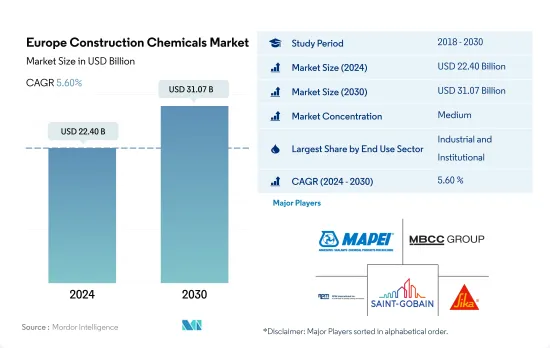

預計 2024 年歐洲建築化學品市場規模將達到 224 億美元,預計到 2030 年將達到 310.7 億美元,預測期內(2024-2030 年)的複合年成長率為 5.60%。

工業和商業領域建築投資的增加將推動建築化學品的需求

- 到 2023 年,歐洲預計將佔據全球建築化學品市場的大部分佔有率,約 24.99%。 2022 年,歐洲建築化學品市場以金額為準成長 6.15%,主要受商業和工業/機構建築業需求成長的推動。

- 工業和機構建築業在 2022 年佔比約為 35.55%,已成為該區域市場最大的建築化學品消費產業。預計該產業的新增占地面積將從 2023 年起成長至 2030 年的 2.45 億平方英尺。這一成長是由於歐洲國家對工業、教育和醫療保健建設的投資增加。受都市化和工業化等因素的推動,該地區工業和機構部門的建築化學品市場預計將從 2023 年的 74.8 億美元成長到 2030 年的 104.4 億美元。

- 該地區的商業建築業是建築化學品成長最快的消費產業,預計預測期內的複合年成長率為 6.10%。該地區的經濟擴張正在推動對商業房地產的需求,包括辦公室、酒店和零售商場。預計到 2030 年,該領域的新占地面積將比 2023 年增加 3.94 億平方英尺。受此推動,預計 2023 年至 2030 年間,歐洲該領域的建築化學品市場規模將成長 23.6 億美元。

在義大利,工業建設投資的增加預計將推動對建築化學品的需求

- 我們的建築化學品系列包括混凝土外加劑、防水解決方案、黏合劑和密封劑、錨栓和水泥漿以及地板材料樹脂,可提高建築物和結構的性能。 2022年歐洲建築化學品市場規模與前一年同期比較增6.15%。歐盟將在2022年為建築計劃撥款1.555兆美元,將使歐盟建築業主導的GDP達到15.375兆美元,較2021年成長3.5%。這些投資增強了建築業,刺激了對建築化學品的需求。預計 2023 年建築化學品市場以金額為準將成長 4.44%,延續上一年的動能。

- 2022 年,德國在建築化學品市場佔據主導地位,以以金額為準佔有 17% 的市場佔有率。該國建築業吸引了5,200億美元的投資,主要用於住宅、土木和非住宅計劃。隨著建設活動的激增,對建築化學品的需求也隨之增加,到 2022 年市場規模將達到 35 億美元。預計 2023 年市場以金額為準將成長 3.65%。

- 預計義大利建築化學品市場的複合年成長率最高,為 6.21%。這一成長的主要驅動力是工業建築領域。為了響應歐洲到2050年實現零排放的氣候目標,雷普索爾等公司已承諾在義大利投資5.5億美元用於可再生能源計劃。因此,到 2030 年,義大利工業建築新占地面積預計將比 2022 年增加 1,590 萬平方英尺,這意味著對建築化學品的需求將持續成長。

歐洲建築化學品市場趨勢

西班牙、義大利等地辦公大樓擴建計劃推動歐洲商業建築市場

- 在歐洲,由於人們更重視建造節能辦公大樓以符合 2030 年碳排放目標,新建商業建築占地面積將在 2022 年成長 12.70%。隨著員工重返辦公空間,歐洲公司也相應活性化了租賃決策,導致 2022 年新增辦公空間 570 萬平方英尺。預計 2023 年這一成長動能將持續,預計成長率為 2022 年的 2.68%。

- 新冠疫情造成嚴重的勞動力和材料短缺,導致多個商務用建築計劃被取消或延遲。然而,隨著關閉措施的放鬆和建設活動的恢復,歐洲 2021 年新建商業占地面積強勁成長 16.60%,其中西班牙以 105.05% 的成長率領先。

- 歐洲商業建築業預計將經歷顯著成長,預測期內新占地面積預計複合年成長率為 3.88%。一些著名計劃預計將增強該地區的商業建設格局,例如位於義大利米蘭的美國總領事館綜合體(耗資 6,500 萬美元,預計於 2025 年完工)和位於西班牙的 Arteixo 辦公大樓擴建項目(耗資 2.6 億美元,佔地 180 萬平方英尺,預計於 2024 年運作)。隨著消費者偏好從線上零售轉向線下零售,到 2030 年,歐洲新零售商場占地面積預計將比 2022 年增加 4.283 億平方英尺。

英國和歐洲各地經濟適用住宅計劃和已完工住宅計劃的增加預計將推動新建住宅占地面積的成長。

- 在歐洲住宅建築領域,2022年新屋占地面積較去年與前一年同期比較成長2.71%。其背景是都市化的上升,城市人口預計將從 2020 年的 73.5% 上升到 2022 年的 75%。預計這一趨勢將持續到 2023 年,與 2022 年相比成長率為 3.21%。根據 EURO CONSTRUCT 網路的數據,預計 2023 年歐洲已完工住宅計劃數量將增加 2.7%,匈牙利、愛爾蘭、挪威和波蘭的數量將顯著增加。

- 新冠疫情導致景氣衰退,許多住宅建築計劃被取消或推遲。因此,2020年歐洲新建住宅占地面積與前一年同期比較下降了9.40%。然而,隨著封鎖限制的放鬆和建設活動的恢復,該行業強勁復甦,2021 年的新占地面積與 2020 年相比飆升了 18.28%。西班牙的成長顯著,增幅為 40.23%,其次是義大利,增幅為 25.07%。

- 預測期內,歐洲新建住宅占地面積預計複合年成長率為 3.89%。英國將引領這一成長,複合年成長率為 5.94%。這種成長是由對經濟適用住宅的需求不斷成長所推動的,特別是在人口成長和住宅供應有限的都市區。英國政府的經濟適用房計畫旨在2026年提供13萬套住宅,擴大全國的住宅占地面積,投資額為80億美元。

歐洲建築化學品產業概況

歐洲建築化學品市場適度整合,前五大公司佔49.49%的市佔率。該市場的主要企業是 MAPEI SpA、MBCC Group、RPM International Inc.、Saint-Gobain 和 Sika AG。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用途細分趨勢

- 商業的

- 業/設施

- 基礎設施

- 住宅

- 重大基礎設施計劃(目前和已宣布)

- 法律規範

- 價值鏈與通路分析

第 5 章。市場區隔(包括市場規模、2030 年預測、成長前景分析)

- 最終用途領域

- 商業的

- 業/設施

- 基礎設施

- 住宅

- 產品

- 膠水

- 按子產品

- 熱熔膠

- 反應性

- 溶劑型

- 水性

- 錨固和水泥漿

- 按子產品

- 水泥基固定材料

- 樹脂固定

- 其他

- 混凝土外加劑

- 按子產品

- 加速器

- 引氣劑

- 高效減水劑(塑化劑)

- 阻燃

- 減縮劑

- 黏度調節劑

- 減水劑(塑化劑)

- 其他

- 混凝土保護漆

- 按子產品

- 丙烯酸纖維

- 醇酸

- 環氧樹脂

- 聚氨酯

- 其他

- 地板樹脂

- 按子產品

- 丙烯酸纖維

- 環氧樹脂

- 聚天冬醯胺

- 聚氨酯

- 其他

- 修復和再生化學品

- 按子產品

- 光纖纏繞系統

- 水泥漿材料

- 微混凝土砂漿

- 改質砂漿

- 鋼筋保護材料

- 密封材料

- 按子產品

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽膠

- 其他

- 表面處理化學品

- 按子產品

- 硬化劑

- 脫模劑

- 其他

- 防水解決方案

- 按子產品

- 化學產品

- 膜

- 膠水

- 國家名稱

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 歐洲其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介

- Ardex Group

- Arkema

- Atlas

- CEMEX, SAB de CV

- Fosroc, Inc.

- Henkel AG & Co. KGaA

- Kingspan Group

- MAPEI SpA

- MBCC Group

- MC-Bauchemie

- RPM International Inc.

- Saint-Gobain

- Schomburg

- Selena Group

- Sika AG

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 46762

The Europe Construction Chemicals Market size is estimated at 22.40 billion USD in 2024, and is expected to reach 31.07 billion USD by 2030, growing at a CAGR of 5.60% during the forecast period (2024-2030).

Increase in investments for constructions in the industrial and commercial sectors to drive the demand for construction chemicals

- By 2023, Europe was expected to hold a significant share, amounting to approximately 24.99% of the global construction chemicals market. In 2022, the construction chemicals market in Europe saw a 6.15% growth in value, driven primarily by rising demand from the commercial and industrial & institutional construction sectors.

- Accounting for a share of about 35.55% in 2022, the industrial and institutional construction sector emerged as the largest consumer of construction chemicals in the regional market. The sector's projected new floor area is set to rise and reach 245 million sq. ft by 2030 compared to 2023. This surge is attributed to increased investments in industrial, education, and healthcare construction across European countries. The region's construction chemicals market for the industrial and institutional sector is forecast to grow from USD 7.48 billion in 2023 to USD 10.44 billion in 2030, driven by factors like urbanization and industrialization.

- The commercial construction sector in the region is poised to be the fastest-growing consumer of construction chemicals, with a projected CAGR of 6.10% during the forecast period. The region's expanding economy is fueling demand for commercial properties, including offices, hotels, and retail malls. The sector's new floor area is anticipated to rise by 394 million sq. ft by 2030 compared to 2023. Driven by such developments, the European construction chemicals market for this sector is expected to witness a USD 2.36 billion increase from 2023 to 2030.

Construction chemicals are expected to witness high demand in Italy due to rising investments in industrial construction

- Construction Chemicals, including concrete admixtures, waterproofing solutions, adhesives & sealants, anchors & grouts, and flooring resins, enhance the functionality of buildings and structures. In 2022, the value of Europe's construction chemicals market grew by 6.15% from the previous year. The European Union (EU) allocated USD 1555 billion to construction projects in 2022, contributing to the EU's construction-driven GDP of USD 15375 billion, a 3.5% increase from 2021. These investments bolstered the construction sector and fueled the demand for construction chemicals. The construction chemicals market was projected to grow by 4.44% in value in 2023, building on the momentum of the previous year.

- Germany dominated the construction chemicals market in 2022, capturing a 17% market share by value. The country's construction sector attracted investments of USD 520 billion, primarily directed toward residential, civil engineering, and non-residential projects. As construction activities surged, the demand for construction chemicals followed suit, resulting in a market worth USD 3.5 billion in 2022. This market was anticipated to grow by 3.65% in value in 2023.

- Italy is poised to witness the highest compound annual growth rate (CAGR) of 6.21% in the construction chemicals market. This growth is largely driven by the industrial construction segment. In line with Europe's climate goals of achieving zero emissions by 2050, companies like Repsol have committed to investing USD 550 million in renewable energy projects in Italy. Consequently, the projected new floor area for industrial construction in Italy is set to increase by 15.9 million square feet by 2030 compared to 2022, signaling a rising demand for construction chemicals.

Europe Construction Chemicals Market Trends

Office building expansion projects in countries such as Spain and Italy are boosting the commercial construction market in Europe

- Europe witnessed a 12.70% surge in the new floor area for commercial construction in 2022, driven by an increased focus on constructing energy-efficient office buildings, which aligns with the region's 2030 carbon emission targets. As employees returned to office spaces, European companies, in turn, ramped up their leasing decisions, resulting in the addition of 5.7 million square feet of new office space in 2022. This growth was expected to persist in 2023, with a projected growth rate of 2.68% over 2022.

- The COVID-19 pandemic caused a significant labor and material shortage, leading to the cancellation or postponement of several commercial construction projects. However, as lockdowns eased and construction activities resumed, Europe witnessed a robust 16.60% growth in new floor area for commercial construction in 2021, with Spain being the leader with a 105.05% growth rate.

- The commercial construction sector in Europe is poised for substantial growth, with the new floor area anticipated to register a CAGR of 3.88% during the forecast period. Noteworthy projects, such as the USD 65 million Milan US Consulate General Complex in Italy, slated for completion by 2025, and the USD 260 million Arteixo Office Building Expansion in Spain, spanning 1.8 million square feet and set to be operational in 2024, are expected to bolster the region's commercial construction landscape. As consumer preferences shift from online to in-person retail experiences, the new floor area is expected to increase by 428.3 million square feet for retail shopping malls in Europe by 2030 compared to 2022.

Affordable housing schemes in the UK and Europe and growth in housing project completions are expected to increase the new floor area for residential construction

- Europe's residential construction sector witnessed a 2.71% growth in new floor area in 2022 compared to the previous year. This can be attributed to the escalating urbanization rate, with the urban population accounting for 75% of the total in 2022, up from 73.5% in 2020. This trend was expected to persist in 2023, with a projected growth rate of 3.21% over 2022. According to the EURO CONSTRUCT network, Europe witnessed a 2.7% rise in housing project completions in 2023, with notable increases in Hungary, Ireland, Norway, and Poland.

- The COVID-19 pandemic led to an economic downturn, resulting in the cancellation or postponement of numerous residential construction projects. Consequently, the new floor area for residential construction in Europe plummeted by 9.40% in 2020 compared to the preceding year. However, as lockdown restrictions eased and construction activities resumed, the sector rebounded strongly, with an 18.28% surge in new floor area in 2021 compared to 2020. Spain led the growth with a remarkable 40.23% increase, followed by Italy at 25.07%.

- The new floor area for residential construction in Europe is projected to witness a CAGR of 3.89% during the forecast period. The United Kingdom is poised to lead this growth, recording a CAGR of 5.94%. This growth can be attributed to factors such as a mounting demand for affordable housing, particularly in urban centers grappling with population growth and limited housing supply. The UK government's Affordable Homes Programme, backed by an investment of USD 8 billion, aims to deliver 130,000 housing units by 2026, bolstering the nation's residential construction floor area.

Europe Construction Chemicals Industry Overview

The Europe Construction Chemicals Market is moderately consolidated, with the top five companies occupying 49.49%. The major players in this market are MAPEI S.p.A., MBCC Group, RPM International Inc., Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Arkema

- 6.4.3 Atlas

- 6.4.4 CEMEX, S.A.B. de C.V.

- 6.4.5 Fosroc, Inc.

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Kingspan Group

- 6.4.8 MAPEI S.p.A.

- 6.4.9 MBCC Group

- 6.4.10 MC-Bauchemie

- 6.4.11 RPM International Inc.

- 6.4.12 Saint-Gobain

- 6.4.13 Schomburg

- 6.4.14 Selena Group

- 6.4.15 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

建築化學品市場規模、佔有率及成長分析(混凝土外加劑、防水劑、防護被覆劑、黏合劑及密封劑、修補劑及修復劑及地區)- 2025-2032 年產業預測

建築化學品市場規模、佔有率及成長分析(混凝土外加劑、防水劑、防護被覆劑、黏合劑及密封劑、修補劑及修復劑及地區)- 2025-2032 年產業預測 中東和非洲的建築化學品:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美建築化學品:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)南美洲建築化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度建築化學品-市場佔有率分析、產業趨勢與統計、2025-2030 年成長預測建築修復和維修化學品-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國建築化學品-市場佔有率分析、產業趨勢與成長預測(2025-2030年)美國建築化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

中東和非洲的建築化學品:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美建築化學品:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)南美洲建築化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度建築化學品-市場佔有率分析、產業趨勢與統計、2025-2030 年成長預測建築修復和維修化學品-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國建築化學品-市場佔有率分析、產業趨勢與成長預測(2025-2030年)美國建築化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

▼