|

市場調查報告書

商品編碼

1683750

蠟添加劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Wax Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

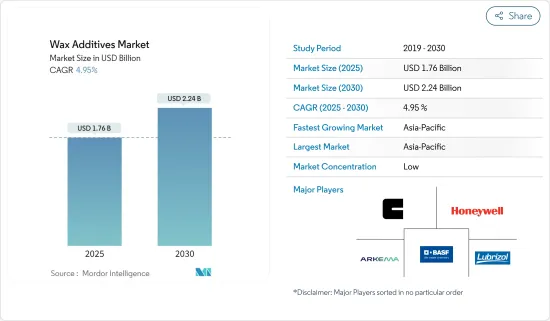

預計 2025 年蠟添加劑市場規模為 17.6 億美元,到 2030 年將達到 22.4 億美元,預測期內(2025-2030 年)的複合年成長率為 4.95%。

COVID-19 疫情爆發擾亂了建設活動。此外,汽車製造業也受到半導體晶片短缺和其他供應鏈中斷的嚴重影響。然而,蠟添加劑市場已從疫情中恢復並正在經歷強勁成長。

主要亮點

- 預計家居裝飾和健康中心對蠟燭的消費量增加將推動市場需求。此外,蠟添加劑賦予被覆劑和油墨的特性也有望推動市場成長。

- 然而,原油價格的波動可能會阻礙市場成長。

- 然而,全球生物基蠟添加劑應用的興起可能為未來的市場提供有利可圖的機會。

- 由於中國、日本和印度等國家消費量龐大,預計亞太地區將主導市場。

蠟添加劑市場趨勢

蠟添加劑預計將在塗料行業迎來高需求

- 蠟添加劑廣泛用於被覆劑,因為它們可以增強最終產品的外觀,防止運輸和搬運過程中的碰傷和刮痕,並充當活性化合物的載體。

- 由於其靈活性及其對許多配方的積極影響,它被廣泛應用於被覆劑中。您可以期待一般的耐用性、抗刮性、耐磨性甚至防滑性能。

- 根據世界塗料工業理事會預測,2022年全球油漆塗料銷售額將達1,799億美元左右,年增率為3.1%。

- 預計2022年北美市場規模為339.2億美元,歐洲市場規模為423.7億美元。這些地區的成長都是由加拿大、德國和美國的住宅改建增加所推動的。

- 預計 2022 年亞太地區油漆和塗料市場價值將達到 630 億美元。東亞地區是全球油漆和塗料市場中最利潤豐厚的市場。 2022年中國市場將進一步成長5.7%。按照目前的趨勢,2022年中國油漆和塗料的總銷售額將超過450億美元。

- 由於汽車、建築和施工行業的需求不斷成長,油漆和塗料行業多年來一直處於成長狀態。需求的成長促使全球和國內企業在多個國家開展擴建計劃,以縮小供需缺口。例如,2023 年 6 月,阿克蘇諾貝爾宣布斥資 5,500 萬美元擴建位於美國北卡羅來納州高點南部的木材塗料製造園區。

- 因此,預計上述因素將在預測期內推動塗料應用並增加對蠟添加劑的需求。

亞太地區可望引領全球市場

- 預計亞太地區的蠟添加劑市場將大幅成長,其中中國和印度等國家是被覆劑和印刷油墨的主要消費國。

- 在中國,被覆劑、印刷油墨、蠟燭和皮革塗飾等應用是蠟添加劑需求的主要驅動力。

- 根據全球油漆和塗料工業協會的數據,中國目前在該地區市場佔據主導地位,複合年成長率為 5.8%。 2022年中國油漆和塗料市場將成長5.7%。

- 根據目前的趨勢,到 2022 年,中國油漆和塗料的總銷售額將超過 450 億美元。這凸顯了中國在東亞的主導地位,擁有最大的市場佔有率(78%)。

- 印度油漆和塗料產業價值約 80 億美元。印度經濟是全球成長最快的經濟之一。印度約有 3,000 家油漆製造商。其建築塗料市場的佔有率為75%,工業塗料市場的佔有率為25%。

- 此外,在中國,點蠟燭也很流行,尤其是在假期季節。中國最重要的傳統節日是農曆新年,又稱為春節。

- 根據貿易地圖,2023年6月、7月和8月三個月,蠟燭出口額分別為77,583美元、91,034美元和98,438美元。

- 同時,2023 年 8 月,日本從世界各地進口了價值 2,495 美元的蠟燭。特別受歡迎的設計是花蠟燭,在日本佛教徒中很受歡迎,作為日常供品。此外,圖案蠟燭在喜愛蠟燭的人群中也很受歡迎。

- 此外,國際油墨製造商在中國也佔有重要地位。與東洋油墨合資的杭州東華油墨和與東洋油墨合資的天津東洋油墨是中國最大的兩家油墨製造商。 DIC、富林特集團、坂田INX、盛威科等油墨產業領導企業也在中國佔有重要地位。

- 上述因素加上政府的支持,將推動預測期內蠟添加劑市場的需求增加。

蠟添加劑產業概況

蠟添加劑市場比較分散。市場的主要企業包括(不分先後順序)路博潤、Honeywell國際、BASF、阿科瑪和科萊恩。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 家居裝飾和健康中心的蠟燭消費量增加

- 蠟添加劑在被覆劑和油墨的優勢

- 限制因素

- 原油價格波動

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 材料

- 自然的

- 半合成

- 合成

- 類型

- 分散

- 乳液

- 微粒化

- 應用

- 塗層

- 皮革飾面

- 印刷油墨

- 蠟燭

- 其他用途(塑膠加工、黏合劑、橡膠添加劑)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Arkema

- BASF SE

- BYK-CHEMIE GmbH

- Clariant

- Concentrol

- Evonik Industries AG

- Honeywell International Inc.

- Innospec

- Munzing Corporation

- Paramold Manufacturing LLC

- Shamrock Technologies, Inc.

- The Lubrizol Corporation

- Tianshi Wax

第7章 市場機會與未來趨勢

- 生物基蠟添加劑的新應用

The Wax Additives Market size is estimated at USD 1.76 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 4.95% during the forecast period (2025-2030).

The outbreak of COVID-19 resulted in hindrances in construction activities. Furthermore, due to semiconductor chip shortage and other supply chain disruptions, automotive manufacturing was also affected severely. However, the wax additives market recovered from the pandemic and is growing significantly.

Key Highlights

- The growing consumption of candles in home decor and health centers is likely to drive the demand for the market forward. Furthermore, the properties imparted by the wax additives in coatings and inks are also expected to fuel the market growth.

- However, the volatility in crude oil prices is likely to hamper the market growth.

- Nevertheless, emerging bio-based wax additive applications on a worldwide scale are likely to present lucrative opportunities for the market in the future.

- The Asia-Pacific region is expected to dominate the market with enormous consumption from countries such as China, Japan, and India.

Wax Additives Market Trends

Wax Additives Expected to find High Demand in Coatings Segment

- Wax additives are widely used in coatings to improve the appearance of finished products, help protect from bruising or scratching during the shipping and handling of goods, and act as a carrier for active compounds.

- They are used extensively in coatings because of their flexibility and significant positive impact on many formulation types. They can provide general durability, scratch and abrasion resistance, and even anti-slip properties.

- According to the World Paint and Coatings Industry Association, in 2022, the global sales volume of paints and coatings stood at around USD 179.9 billion, with an annual growth rate of 3.1%.

- The North American market value stood at USD 33.92 billion, while Europe was valued at USD 42.37 billion in 2022, respectively. The growth of these respective regions is attributed to an increase in the number of house renovation activities in Canada, Germany, and the United States.

- The Asia-Pacific paints and coatings market stood at USD 63 billion in 2022. The East Asian region is the most lucrative market for paints and coatings worldwide. The Chinese market further increased by 5.7 % in 2022. From the current trend, in 2022, China's total sales of paints and coatings exceeded USD 45 billion.

- The paint and coatings industry grew over the years due to increased demand from the automotive, building, and construction sectors. Such increased demand led to several expansion projects by global and domestic players in several countries to reduce the demand and supply gap. For instance, in June 2023, AkzoNobel unveiled the USD 55 million expansion of its wood coatings manufacturing campus in south High Point in North Carolina, United States.

- Therefore, all the above factors are expected to drive the coatings application, enhancing the demand for wax additives during the forecast period.

Asia-Pacific Region Expected to Lead the Global Market

- The Asia-Pacific region saw significant growth in the wax additives market, with countries such as China and India accounting for significant consumption of coatings and printing inks.

- In China, the major demand for wax additives is driven majorly by applications such as coatings, printing inks, candles, leather finishing, and others.

- According to the World Paint & Coatings Industry Association, China presently dominates the region market, which is growing at a CAGR of 5.8%. The Chinese paints and coatings market increased by 5.7% in 2022.

- From the current trend, in 2022, China's total sales of paints and coatings exceeded USD 45 billion. It is, thereby, depicting the country's dominance with the largest market share (78%) in East Asia.

- The Indian Paint and Coating Industry accounts for around USD 8 billion. It is considered one of the fastest-growing economies globally. India comprises around 3,000 paint manufacturers. The country exhibits a 75% share of architectural and a 25% share of industrial paints.

- Further, the usage of candles in China is very popular, particularly during the holiday season. The most important of all traditional Chinese holidays is Chinese New Year, also known as Spring Festival.

- As per the trade map, the country exported candles with a value of USD 77,583, 91,034, and 98,438 in the June, July, and August months of 2023.

- Japan, on the other hand, imported USD 2,495 worth of candles from all around the world in August 2023. A particularly popular design is a candle with flower patterns that became popular amongst Buddhists as a daily offering in the country. Moreover, painted wax candles are used by people who love candles.

- Furthermore, international ink manufacturers also hold a major presence in China. Hangzhou Toka Ink, a joint venture with T&K Toka, and Tianjin Toyo Ink Co. Ltd, a joint venture with Toyo Ink, are China's two largest ink manufacturers. DIC, Flint Group, Sakata INX, Siegwerk, and other ink industry leaders also include a sizable presence in China.

- The factors above, coupled with government support, are contributing to the increasing demand for the wax additives market during the forecast period.

Wax Additives Industry Overview

The market for wax additives is fragmented in nature. Some of the major players in the market include The Lubrizol Corporation, Honeywell International Inc., BASF SE, Arkema, and Clariant (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Consumption of Candles in Home Decor and Health Centers

- 4.1.2 Wax Additives Benefits in Coatings and Inks

- 4.2 Restraints

- 4.2.1 Volatility in Crude Oil Price

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material

- 5.1.1 Natural

- 5.1.2 Semi-synthetic

- 5.1.3 Synthetic

- 5.2 Type

- 5.2.1 Dispersion

- 5.2.2 Emulsion

- 5.2.3 Micronized

- 5.3 Application

- 5.3.1 Coatings

- 5.3.2 Leather Finishing

- 5.3.3 Printing Ink

- 5.3.4 Candles

- 5.3.5 Other Applications (Plastic Processing, Adhesives, and Rubber Additive)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 BYK-CHEMIE GmbH

- 6.4.4 Clariant

- 6.4.5 Concentrol

- 6.4.6 Evonik Industries AG

- 6.4.7 Honeywell International Inc.

- 6.4.8 Innospec

- 6.4.9 Munzing Corporation

- 6.4.10 Paramold Manufacturing LLC

- 6.4.11 Shamrock Technologies, Inc.

- 6.4.12 The Lubrizol Corporation

- 6.4.13 Tianshi Wax

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Bio-based Wax Additives Applications

蜂蠟:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

蜂蠟:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球合成蠟市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球合成蠟市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 蜂蠟市場機會、成長動力、產業趨勢分析及 2025-2034 年預測北美香薰蠟熔體市場規模、佔有率、趨勢分析報告:按熔體類型、香味、形式、應用、包裝、國家、細分市場預測,2025-2030 年Wax -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)微晶蠟:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

蜂蠟市場機會、成長動力、產業趨勢分析及 2025-2034 年預測北美香薰蠟熔體市場規模、佔有率、趨勢分析報告:按熔體類型、香味、形式、應用、包裝、國家、細分市場預測,2025-2030 年Wax -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)微晶蠟:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 合成聚合物蠟市場規模、佔有率、成長分析,按類型、按應用、按最終用途行業、按地區 - 行業預測,2025-2032 年蠟熔體市場規模、佔有率、成長分析、按產品類型、按香料類型、按分銷管道、按應用、按地區 - 行業預測,2025-2032 年全球蠟市場規模、佔有率和成長分析:按產品、應用和地區分類 - 產業預測(2024-2031)蠟乳液市場規模、佔有率、成長分析,按產地、按產品、按應用、按地區 - 行業預測,2024-2031 年

合成聚合物蠟市場規模、佔有率、成長分析,按類型、按應用、按最終用途行業、按地區 - 行業預測,2025-2032 年蠟熔體市場規模、佔有率、成長分析、按產品類型、按香料類型、按分銷管道、按應用、按地區 - 行業預測,2025-2032 年全球蠟市場規模、佔有率和成長分析:按產品、應用和地區分類 - 產業預測(2024-2031)蠟乳液市場規模、佔有率、成長分析,按產地、按產品、按應用、按地區 - 行業預測,2024-2031 年