|

市場調查報告書

商品編碼

1683867

電動商用車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)Electric Commercial Vehicle Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

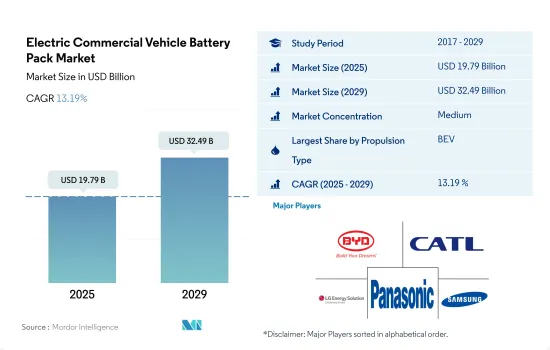

2025 年電動商用車電池組市場規模預估為 197.9 億美元,預計到 2029 年將達到 324.9 億美元,預測期內(2025-2029 年)的複合年成長率為 13.19%。

人們對小型電動送貨車的興趣日益濃厚,推動了電池產能的擴張

- 近年來,商用車越來越受歡迎,但它們也對污染和氣候變遷產生了重大影響。因此,近年來,世界許多地方對電動商用車及其動力來源電池的需求不斷成長。中國不僅是電池生產大國,也引領全球電動車熱潮,2021年全電動卡車銷量佔90.24%。電動商用車需求的增加將推動電池產業的發展,導致全球對包括LFP和NMC在內的各種電動商用車電池組的需求在2021年比2017年成長34.38%。

- 全球對電動卡車的需求不斷增加,影響了全球各種電池市場。 NMC、NCM 和 LFP 電池正在多個地區迅速擴張。多種電動商用車電池市場的 90% 以上都來自中國,中國是全球電動商用車和電池生產的領導者。因此,2022 年全球對所有類型商用車電池的需求與 2021 年相比成長了 32.11%。

- 考慮到由於電子商務、物流和基礎設施用戶等各個行業的成長而導致對電動車的需求不斷成長,預計預測期內世界各國對 BEV 和 PHEV 等電動商用車的需求將顯著成長。

受中國、日本和韓國的推動,亞太地區將主導電動商用車電池組市場

- 電動商用車電池組市場在各個地區呈現出蓬勃發展的動能。亞太地區的電池組市場正在經歷顯著的成長。中國、日本和韓國等國家電動車日益普及,推動了對電池組的需求。中國電動車市場的大幅成長,推動亞洲地區成為全球電動車電池組市場的領導者。

- 歐洲市場出現了巨大的成長。這是由於汽車電氣化的大力推動、嚴格的排放法規和政府的支持政策。該地區已成為電動車生產的中心,導致對電池組的需求增加。對電池研發和充電基礎設施建設的投資進一步推動了市場成長。過去幾年,北美電池組市場穩定成長。推動這一成長的因素包括消費者對電動車的需求不斷增加、政府鼓勵和監管清潔能源的政策以及電池技術的進步。電池組製造產能和投資的增加反映了該地區對永續交通和能源儲存解決方案的承諾。

- 電池組市場的成長歸因於多種因素,例如對電動車的需求不斷增加、政府的支持性政策、技術進步以及對永續能源儲存解決方案的需求。隨著世界各國逐步轉向更清潔的交通和能源系統,市場可望持續成長和創新。

電動商用車電池組市場趨勢

比亞迪和特斯拉引領電動車市場並塑造未來

- 2022年,比亞迪在電動車銷量方面領先市場,佔13.3%的佔有率。比亞迪的主導地位得益於幾個因素。比亞迪專注於生產電動車及相關技術,是電動車產業的早期和主要參與者。作為一個較早進入該市場的品牌,比亞迪已經贏得了廣大消費者的認可。比亞迪也積極進行全球擴張、建立夥伴關係以及投資研發,所有這些都有助於鞏固主導地位。

- 特斯拉一直處於電動車創新的前沿,並在電動車的全球普及中發揮了關鍵作用。 2022 年,特斯拉是電動車產業的重要參與者,市場佔有率為 12.2%。特斯拉強大的品牌形象、最尖端科技和廣泛的超級充電網路為其成功做出了貢獻。

- 在電動車市場的其他主要企業中,還有其他幾家公司佔有相當大的市場佔有率。 BMW在汽車產業享有盛譽,並且正在不斷擴大其市場佔有率,同時也透過其子品牌 BMW i 致力於電動車的發展。同樣,大眾汽車在 2022 年的市場佔有率為 3.9%,在「大眾汽車集團」的保護下,正在積極投資電動車。這些公司與梅賽德斯·奔馳、起亞和現代等其他公司一起,利用現有的品牌知名度,推出引人注目的電動車車型,並投資於提高電動車續航里程和性能的技術,重新佔領電動車行業。

特斯拉和比亞迪在 2022 年最暢銷的電動車車型中佔據主導地位

- 2022 年最暢銷的電動車車型由兩大原始OEM製造商主導:特斯拉和比亞迪。特斯拉以兩款車型Model Y和Model 3分別佔據第一和第三的位置,確立了市場強勢地位。特斯拉的Model Y是最受歡迎的插電式電動車,2022年全球銷量約77.13萬輛。同年,特斯拉Model 3和Model Y的銷量突破120萬輛,成為特斯拉最暢銷的車型,與前一年同期比較成長36.77%。最暢銷的五款插電式電動車 (PEV) 車型中有兩款是特斯拉品牌,但這家電池電動車製造商在 2022 年面臨亞洲品牌的競爭。由於其豐富的插電式混合動力電動車車型陣容,總部位於中國的比亞迪將在 2022 年超越特斯拉成為最暢銷的 PEV 品牌。緊接在特斯拉Model Y之後的是比亞迪宋Plus(BEV+PHEV),以477,090輛的銷量位居第二。比亞迪在中國市場佔有重要地位,以生產可靠、技術先進的電動車而聞名,這可能促成了宋 Plus 車型的強勁銷售表現。

- VolkswagenID.4是唯一一款進入前十名的歐洲PEV(插電式電動車),並在最暢銷的電動車車型中脫穎而出。 ID.4 在 2022 年的銷量為 174,090 輛,彰顯了大眾汽車對電動車的承諾及其在電動車市場日益成長的影響力。

- 總體而言,特斯拉和比亞迪的這些頂級電動車車型,以及五菱宏光 MINI EV 和大眾 ID.4 等其他知名競爭對手,都顯示消費者對電動車的需求日益成長。

電動商用車電池組產業概況

電動商用車電池組市場格局適度整合,前五大企業佔59.48%。該市場的主要企業為:比亞迪股份有限公司、寧德時代新能源科技股份有限公司(CATL)、LG 能源解決方案有限公司、松下控股股份有限公司和三星 SDI(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 電動商用車銷售

- 電動商用車銷量(OEM)

- 最暢銷的電動車車型

- 具有首選電池化學成分的OEM

- 電池組價格

- 電池材料成本

- 每種電池化學成分的價格表

- 誰供給誰?

- 電動車電池容量和效率

- 發布的電動車車型數量

- 法律規範

- 比利時

- 巴西

- 加拿大

- 中國

- 哥倫比亞

- 法國

- 德國

- 匈牙利

- 印度

- 印尼

- 日本

- 墨西哥

- 波蘭

- 泰國

- 英國

- 美國

- 價值鏈與通路分析

第5章 市場區隔

- 體型

- 公車

- LCV

- M&HDT

- 推進類型

- BEV

- PHEV

- 電池化學

- LFP

- NCA

- NCM

- NMC

- 其他

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 超過80度

- 少於15千瓦時

- 電池形狀

- 圓柱形

- 小袋

- 方塊

- 方法

- 雷射

- 金屬絲

- 成分

- 陽極

- 陰極

- 電解

- 分隔符

- 材料類型

- 鈷

- 鋰

- 錳

- 天然石墨

- 鎳

- 其他材料

- 地區

- 亞太地區

- 按國家

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 其他亞太地區

- 歐洲

- 按國家

- 法國

- 德國

- 匈牙利

- 義大利

- 波蘭

- 瑞典

- 英國

- 其他歐洲國家

- 中東和非洲

- 北美洲

- 按國家

- 加拿大

- 美國

- 南美洲

- 亞太地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介

- A123 Systems LLC

- BYD Company Ltd.

- China Aviation Battery Co. Ltd.(CALB)

- Contemporary Amperex Technology Co. Ltd.(CATL)

- EVE Energy Co. Ltd.

- Farasis Energy(Ganzhou)Co. Ltd.

- Guoxuan High-tech Co. Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- Sunwoda Electric Vehicle Battery Co. Ltd.(Sunwoda)

- Tata Autocomp Systems Ltd.

- Tianjin Lishen Battery Joint-Stock Co., Ltd.(Lishen Battery)

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The Electric Commercial Vehicle Battery Pack Market size is estimated at 19.79 billion USD in 2025, and is expected to reach 32.49 billion USD by 2029, growing at a CAGR of 13.19% during the forecast period (2025-2029).

The growing interest in light electric delivery vans is driving battery capacity expansion

- Commercial vehicles have been more popular in recent years but have also greatly contributed to pollution and climate change. Therefore, in recent years, there has been a rise in demand for electric commercial vehicles and the batteries that power them in numerous regions worldwide. China is not just a major producer of batteries but also a driving force behind the global boom in demand for electric vehicles, with 90.24% of all-electric trucks sold in 2021. The increasing demand for electric CVs has boosted the battery sector, resulting in a 34.38% increase in the global demand for electric CV battery packs of different kinds, including LFP and NMC, in 2021 compared to 2017.

- Demand for electric trucks has increased worldwide, impacting the market for various battery types in different parts of the world. NMC, NCM, and LFP batteries are rapidly expanding in several regions. Over 90% of the market for several types of electric CV batteries comes from China, a global leader in producing electric CVs and batteries. As a result, worldwide demand for commercial vehicle batteries of all varieties expanded by 32.11% in 2022 compared to 2021.

- Considering the growing demand for electric vehicles due to the rise in various industries, such as e-commerce, logistics, and infrastructure users, the demand for electric commercial vehicles, such as BEV and PHEV, is expected to show significant growth during the forecast period in various countries globally.

The APAC region takes the lead in the electric CV battery pack market, driven by adoption in China, Japan, and South Korea

- The electric CV battery pack market is experiencing dynamic growth across different regions. The APAC region has experienced remarkable growth in the battery pack market. The rising adoption of electric vehicles in countries like China, Japan, and South Korea has fueled the demand for battery packs. China's massive growth in the EV market has propelled the Asian region to the forefront of the global electric CV battery pack market.

- Europe witnessed a significant surge in the market. This can be attributed to the strong push toward the electrification of vehicles, stringent emission regulations, and supportive government policies. The region has become a hub for electric vehicle production, leading to increased demand for battery packs. Investments in battery research and development, coupled with the establishment of charging infrastructure, further drive the growth of the market. The battery pack market in North America has been steadily growing over the years. Factors driving this growth include rising consumer demand for electric vehicles, government incentives and regulations promoting clean energy, and advancements in battery technology. The increasing capacity and investments in battery pack manufacturing reflect the region's commitment to sustainable transportation and energy storage solutions.

- The growth of the battery pack market can be attributed to several factors, including the growing demand for electric vehicles, supportive government policies, technological advancements, and the need for sustainable energy storage solutions. As countries worldwide strive for cleaner transportation and energy systems, the market is poised for continued growth and innovation.

Electric Commercial Vehicle Battery Pack Market Trends

BYD AND TESLA ARE LEADING THE CHARGE IN THE EV MARKET AND SHAPING THE FUTURE

- In 2022, BYD was the market leader in electric vehicle sales and held a share of 13.3%. BYD's leading position can be attributed to several factors. It has been an early and prominent player in the EV industry, with a strong focus on producing electric vehicles and related technologies. The company's early entry into the market allowed it to establish a solid foundation and gain recognition among consumers. BYD has also been actively expanding its operations globally, forging partnerships, and investing in research and development, all of which contribute to its leading position.

- Tesla has been at the forefront of electric vehicle innovation and has played a crucial role in popularizing EVs worldwide. Tesla was a significant player in the EV industry in 2022, with a market share of 12.2%. Tesla's strong brand image, cutting-edge technology, and extensive Supercharger network have contributed to its success.

- Among the other players in the EV market, there are several notable companies that hold significant market shares. BMW's established reputation in the automotive industry, coupled with its commitment to electric mobility through its "BMW i" sub-brand, has contributed to its market presence. Similarly, Volkswagen, which held a market share of 3.9% in 2022, has been actively investing in electric mobility under its "Volkswagen Group" umbrella. These companies, along with others like Mercedes-Benz, Kia, and Hyundai, are recolonizing the EV industry by leveraging their existing brand recognition, introducing compelling electric vehicle models, and investing in technology to enhance the range and performance of their electric offerings.

TESLA AND BYD DOMINATED THE BEST-SELLING EV MODELS OF 2022

- The best-selling EV models in 2022 were dominated by two key OEMs: Tesla and BYD. Tesla held a strong market position with two of its models, the Model Y and Model 3, capturing the first and third spots, respectively. The Tesla Model Y was the most popular plug-in electric vehicle, with global unit sales of roughly 771,300 in 2022. That year, deliveries of Tesla's Model 3 and Model Y surpassed 1.2 million, a Y-o-Y increase of 36.77% for Tesla's best-selling models. While two of the five best-selling plug-in electric vehicle (PEV) models were Tesla-branded, the battery electric vehicle manufacturer faced competition from Asian brands in 2022. China-based BYD overtook Tesla as the best-selling PEV brand in 2022, relying on a large offering of plug-in hybrid electric models. Following closely behind the Tesla Model Y, the BYD Song Plus (BEV + PHEV) secured the second spot, with sales reaching 477,090 units. BYD's established presence in the Chinese market, along with its reputation for producing reliable and technologically advanced electric vehicles, likely contributed to the strong sales performance of the Song Plus models.

- The Volkswagen ID.4 stood out among the best-selling EV models as the only European PEV (Plug-in Electric Vehicle) in the top ten. With a sales volume of 174,090 units in 2022, the ID.4 demonstrated Volkswagen's commitment to electric mobility and its growing presence in the EV market.

- Overall, these top-performing EV models from Tesla and BYD, along with other notable contenders like the Wuling Hong Guang MINI EV and Volkswagen ID.4, demonstrate the increasing consumer demand for electric vehicles.

Electric Commercial Vehicle Battery Pack Industry Overview

The Electric Commercial Vehicle Battery Pack Market is moderately consolidated, with the top five companies occupying 59.48%. The major players in this market are BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), LG Energy Solution Ltd., Panasonic Holdings Corporation and Samsung SDI Co. Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Commercial Vehicle Sales

- 4.2 Electric Commercial Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 Belgium

- 4.11.2 Brazil

- 4.11.3 Canada

- 4.11.4 China

- 4.11.5 Colombia

- 4.11.6 France

- 4.11.7 Germany

- 4.11.8 Hungary

- 4.11.9 India

- 4.11.10 Indonesia

- 4.11.11 Japan

- 4.11.12 Mexico

- 4.11.13 Poland

- 4.11.14 Thailand

- 4.11.15 UK

- 4.11.16 US

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Battery Chemistry

- 5.3.1 LFP

- 5.3.2 NCA

- 5.3.3 NCM

- 5.3.4 NMC

- 5.3.5 Others

- 5.4 Capacity

- 5.4.1 15 kWh to 40 kWh

- 5.4.2 40 kWh to 80 kWh

- 5.4.3 Above 80 kWh

- 5.4.4 Less than 15 kWh

- 5.5 Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 Method

- 5.6.1 Laser

- 5.6.2 Wire

- 5.7 Component

- 5.7.1 Anode

- 5.7.2 Cathode

- 5.7.3 Electrolyte

- 5.7.4 Separator

- 5.8 Material Type

- 5.8.1 Cobalt

- 5.8.2 Lithium

- 5.8.3 Manganese

- 5.8.4 Natural Graphite

- 5.8.5 Nickel

- 5.8.6 Other Materials

- 5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.1.1 By Country

- 5.9.1.1.1 China

- 5.9.1.1.2 India

- 5.9.1.1.3 Japan

- 5.9.1.1.4 South Korea

- 5.9.1.1.5 Thailand

- 5.9.1.1.6 Rest-of-Asia-Pacific

- 5.9.2 Europe

- 5.9.2.1 By Country

- 5.9.2.1.1 France

- 5.9.2.1.2 Germany

- 5.9.2.1.3 Hungary

- 5.9.2.1.4 Italy

- 5.9.2.1.5 Poland

- 5.9.2.1.6 Sweden

- 5.9.2.1.7 UK

- 5.9.2.1.8 Rest-of-Europe

- 5.9.3 Middle East & Africa

- 5.9.4 North America

- 5.9.4.1 By Country

- 5.9.4.1.1 Canada

- 5.9.4.1.2 US

- 5.9.5 South America

- 5.9.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A123 Systems LLC

- 6.4.2 BYD Company Ltd.

- 6.4.3 China Aviation Battery Co. Ltd. (CALB)

- 6.4.4 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.5 EVE Energy Co. Ltd.

- 6.4.6 Farasis Energy (Ganzhou) Co. Ltd.

- 6.4.7 Guoxuan High-tech Co. Ltd.

- 6.4.8 LG Energy Solution Ltd.

- 6.4.9 Panasonic Holdings Corporation

- 6.4.10 Samsung SDI Co. Ltd.

- 6.4.11 SK Innovation Co. Ltd.

- 6.4.12 Sunwoda Electric Vehicle Battery Co. Ltd. (Sunwoda)

- 6.4.13 Tata Autocomp Systems Ltd.

- 6.4.14 Tianjin Lishen Battery Joint-Stock Co., Ltd. (Lishen Battery)

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動汽車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)北美電動車鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)南美洲電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2023-2029 年)印度電動車電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)德國電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)德國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)日本電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)東協電動車電池組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

中國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動汽車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)北美電動車鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)南美洲電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2023-2029 年)印度電動車電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)德國電動公車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)德國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)日本電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)東協電動車電池組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)