|

市場調查報告書

商品編碼

1683978

非洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Africa Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

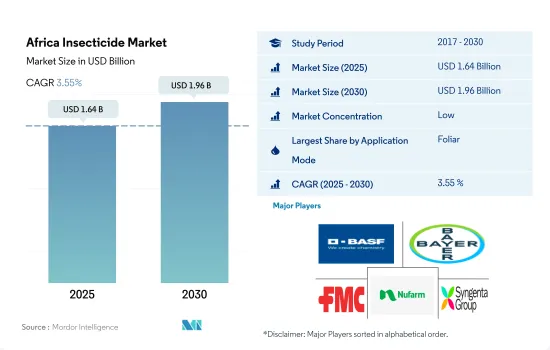

預計 2025 年非洲殺蟲劑市場規模為 16.4 億美元,到 2030 年將達到 19.6 億美元,預測期內(2025-2030 年)的複合年成長率為 3.55%。

葉面噴布因其快速起效而佔據市場主導地位

- 在非洲,農藥的使用方法多種多樣,包括化學灌溉、葉面噴布、種子處理、土壤處理和燻蒸。這些農藥施用方法正在促進整個市場的成長。

- 2022年,葉面噴布法佔據市場主導地位,佔有57.6%的佔有率。葉面噴布噴灑殺蟲劑通常是 IPM 策略的一個組成部分,可以有針對性地精準施用以控制害蟲,同時最大限度地減少對環境的影響。噻蟲胺、呋蟲胺、Imidacloprid和Thiamethoxam等殺蟲劑都是最常用作葉面噴布的系統性殺蟲劑。

- 繼葉面噴布之後,種子處理將在 2022 年佔非洲殺蟲劑市場的 16.9%。土傳昆蟲,如香蕉象鼻蟲 Cosmopolites sordidus Germar、甘薯象鼻蟲 Cylas formicarius Fabricius、豆蛆 Ophiomyia spencerella Greathead、O. phaseoli Tryon 和 O. centrosematis de Meij 經常被報道為影響東非國家(盧旺達、肯尼亞、坦桑迪利亞、烏旺達、肯亞經濟和農業作物的農業作物。這些可以透過種子處理來有效控制。

- 氣候變遷導致新型作物害蟲的大量出現,對非洲農民的糧食和經濟構成了嚴重的威脅。氣候變遷導致的乾旱和高溫為病蟲害的滋生提供了理想條件,對農作物造成了毀滅性的破壞。氣溫升高會增加植物害蟲的繁殖成功率,因為它們對溫度變化變得更加敏感。因此,預計預測期內市場複合年成長率將達到 3.7%。

氣候,特別是溫度,對害蟲族群的發展和成長有強烈而直接的影響。

- 非洲國家高度依賴農業,傳統上容易受到不可預測的氣候條件變化的影響。氣候變遷導致的氣溫上升,加上降雨減少,將對作物生產和糧食安全產生嚴重的直接和間接影響。平均而言,害蟲造成農業產量損失的30-50%。溫度對害蟲族群的發展和成長有直接而強烈的影響。蟲害日益嚴重推動了該地區殺蟲劑市場的發展。

- 2022年,南非佔非洲殺蟲劑市場的31.4%。玉米、米、小麥和高粱是該國種植的最重要的作物。在南非,主要害蟲有蚜蟲、粉蝨、紅蜘蛛、薊馬等。此外,其中一些害蟲是破壞性病毒病原體的載體。歷史時期內(2017年至2022年),南非農藥市值顯著成長,市值增加了1.47億美元。

- 殺蟲劑等農業農藥使得非洲作物產量提高成為可能。目前非洲人口約13億,預計2050年將增加一倍,將對非洲生產力低的糧食生產系統帶來巨大壓力。因此,人們對糧食生產的日益擔憂,加上氣候條件不穩定導致新害蟲的出現,將導致該地區農藥使用增加,預計在預測期內複合年成長率為 3.7%。

非洲殺蟲劑市場的趨勢

蟲害侵擾和日益成長的糧食生產需求導致該地區每公頃土地的農藥消費量不斷增加。

- 非洲每公頃農藥消費量因地區和作物不同而有很大差異。農藥的使用量受多種因素影響,包括害蟲的流行程度、作物類型、耕作方式和一個國家的農業發展水準。

- 在非洲,殺蟲劑的使用對於各種農業系統的害蟲管理至關重要,包括玉米、水稻和小麥等基本作物,以及棉花、咖啡和可可等經濟作物。農藥用於控制多種害蟲,這些害蟲會對作物造成嚴重損害、降低產量並影響糧食安全。 2017年至2022年間,非洲每公頃農藥消費量預計將增加5.3%。

- 害蟲對非洲的農業生產力構成重大威脅。非洲大陸存在各種害蟲,對作物造成嚴重破壞。由於氣候變遷、昆蟲動態變化和貿易全球化等因素,昆蟲面臨的壓力越來越大,因此必須使用殺蟲劑來有效控制昆蟲數量。例如,2019年至2021年,由於非洲之角沙漠爆發蝗蟲,埃塞俄比亞和肯亞共使用廣譜有機磷和擬除蟲菊酯殺蟲劑處理了總合萬公頃土地。

- 隨著非洲糧食需求的增加,非洲正不斷努力提高農業產量。殺蟲劑透過保護植物免受抑制生產的昆蟲侵害,在提高農業產量發揮著至關重要的作用。滿足人口的食物需求導致了對殺蟲劑的依賴增加。

蟲害日益增多導致對Cypermethrin和Imidacloprid等活性成分的需求增加,而有限的生產能力則推高了價格。

- 氣候變遷對非洲農業生產有重大影響,為粉蝨等各類害蟲的滋生創造了有利條件。如果不加以控制,這些害蟲平均會導致25-40%的作物損失。為了解決這個問題,農民嚴重依賴殺蟲劑來更好地控制這些有害昆蟲。因此,農藥的使用是該地區農業實踐的重要組成部分。

- 與其他活性成分相比,Cypermethrin是較昂貴的活性成分之一。 2022 年的價格為每噸 21,023 美元。過去一段時間,Cypermethrin的價格大幅上漲,2022 年的價格與 2017 年的價格相比每公噸上漲了 3,186.2 美元。這種價格上漲趨勢主要是由於它廣泛用於各種作物上以控制介殼蟲、甘藍夜蛾、甘藍夜蛾、粘蟲蛾、果蠅、毛蟲、介殼蟲和莖蟲等害蟲。該地區Cypermethrin產量有限也是造成價格高漲的原因之一。

- Imidacloprid屬於新菸鹼類系統性殺蟲劑,可有效控制多種害蟲。這些害蟲包括吸食汁液的昆蟲、土壤昆蟲甚至白蟻,這使它成為一種可應用於多種作物的多功能解決方案。 2022年Imidacloprid價格為每噸17,120.8美元。

- 活性成分的價格波動主要受原物料成本上漲的影響,是推動市場成長的主要因素之一。

非洲農藥產業概況

非洲農藥市場較為分散,前五大企業佔比為24.69%。市場的主要企業是:BASF公司、拜耳公司、FMC 公司、Nufarm 有限公司和先正達集團(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 南非

- 價值鏈與通路分析

第5章 市場區隔

- 如何使用

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 南非

- 非洲其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001680

The Africa Insecticide Market size is estimated at 1.64 billion USD in 2025, and is expected to reach 1.96 billion USD by 2030, growing at a CAGR of 3.55% during the forecast period (2025-2030).

The foliar method of application dominates the market due to its quick action

- Insecticides are applied through multiple methods in Africa, including chemigation, foliar application, seed treatment, soil treatment, and fumigation. These methods of pesticide application are contributing to the overall expansion of the market.

- The foliar method of application dominated the market in 2022, accounting for a share of 57.6%. The foliar application of insecticides is often a component of IPM strategies, allowing for targeted and precise application to manage pests while minimizing environmental impact. Insecticides like clothianidin, dinotefuran, imidacloprid, and thiamethoxam are the most commonly used systemic insecticides applied through the foliar method.

- Following the foliar application, seed treatment accounted for 16.9% of the African insecticide market in 2022. Soil-borne insects like the banana weevil Cosmopolites sordidus Germar, the sweet potato weevil Cylas formicarius Fabricius, the bean maggots Ophiomyia spencerella Greathead, O. phaseoli Tryon, and O. centrosematis de Meij are frequently reported as common agricultural pests impacting economic crops in countries across East Africa (Rwanda, Kenya, Tanzania, Uganda, and Burundi). These can be effectively controlled by seed treatment.

- Climate change is encouraging the proliferation of new insect pests affecting crops that pose a serious food and financial threat to African farmers. Climate change-induced droughts and high temperatures have provided optimal conditions for pests and diseases to thrive, unleashing destruction on crops. As temperatures rise, the reproduction success of plant pests increases as they are sensitive to temperature changes. Owing to this, the market is anticipated to register a CAGR of 3.7% during the forecast period.

Climate, especially temperature, has a strong and direct influence on the development and growth of insect pest populations

- Countries in Africa are highly dependent on agriculture, an activity traditionally vulnerable to unpredictable changes in climatic conditions. Any increase in temperature caused by climate change, coupled with a decline in rainfall, will have direct and indirect drastic effects on crop production and food security. On average, 30-50% of the yield losses in crops are caused by pests. Temperature has a strong and direct influence on the development and growth of insect pest populations. An increase in pest infestation is driving the insecticide market in the region.

- South Africa accounted for 31.4% of the African insecticides market in 2022. Maize, rice, wheat, and sorghum are the most important food crops grown in the country. In South Africa, the major pest outbreaks were aphids, whiteflies, red spider mites, and thrips. Moreover, some of these pests are vectors of destructive viral pathogens. There has been significant growth observed in the South African insecticide market value during the historical period (between 2017 and 2022), and the market value increased by USD 147.0 million.

- Agricultural pesticides like insecticides have made it possible to increase production in crop yields in Africa. Africa's population, currently estimated at 1.3 billion people, is expected to double by 2050, placing enormous pressure on African food production systems that are plagued by low productivity. Therefore, the increasing concerns over food production, coupled with the emergence of new pests due to erratic climatic conditions, is expected to boost the usage of insecticides in the region, and the market is anticipated to register a CAGR of 3.7% during the forecast period.

Africa Insecticide Market Trends

Growing insect pest infestations and the need for higher food production are raising the consumption of insecticides per hectare in the region

- The consumption of insecticides per hectare in Africa can vary significantly across different regions and crops. Insecticide usage is influenced by several factors, such as the prevalence of insect pests, crop types, farming practices, and the level of agricultural development in each country.

- In Africa, the use of insecticides is critical for managing insects in a variety of agricultural systems, including basic food crops like maize, rice, and wheat, as well as cash crops like cotton, coffee, and cocoa. Insecticides are used to manage a wide variety of insect pests that can cause considerable crop damage, lower yields, and have an impact on food security. Between 2017 and 2022, insecticide consumption per hectare in Africa witnessed a growth of 5.3%.

- Insect pests pose a significant threat to agricultural productivity in Africa. The continent is home to a diverse range of insect pests that can cause extensive damage to crops. The increasing insect pressure, driven by factors such as climate change, changing insect dynamics, and globalization of trade, has necessitated the use of insecticides to manage insect populations effectively. For instance, a total of 1.6 million hectares in Ethiopia and Kenya were treated with broad-spectrum organophosphate and pyrethroid insecticides as a result of the locust outbreak in the Horn of Africa's desert between 2019 and 2021.

- The increasing demand for food in Africa has led to a concerted effort to enhance agricultural output. Insecticides serve an important role in increasing agricultural yields by protecting plants from insects that might disrupt output. The necessity to fulfill the population's food requirements drives the reliance on insecticides.

Increasing pest infestations resulted in high demand for active ingredients like cypermethrin and imidacloprid, and their limited production capacities are raising the prices

- Climate change is significantly impacting agricultural production in Africa, providing favorable conditions for the proliferation of various insect pests like whiteflies. If left unmanaged, these pests can lead to an average crop loss of 25-40%. To combat this issue, farmers heavily rely on insecticides to gain better control over these harmful insects. As a result, the use of insecticides has become a crucial component of agricultural practices in the region.

- Cypermethrin stands out as one of the pricier active ingredients compared to others. In 2022, it recorded a price of USD 21,023.0 per metric ton. Over the historical period, the price of cypermethrin has seen a substantial increase, surging by USD 3,186.2 per metric ton in 2022 compared to its price in 2017. This escalating price trend can be primarily attributed to its extensive usage across various crops to control a wide range of insect pests, such as American bollworms, weevils, codling moths, leafrollers, fruit flies, caterpillars, cutworms, stalk borers, and more. The limited production of cypermethrin within the region also contributes to the upward price trajectory.

- Imidacloprid, classified as a systemic insecticide within the neonicotinoid family, effectively controls an extensive array of insect pests. These pests encompass sucking insects, soil insects, and even termites, making it a versatile solution applicable to various crops. The price of imidacloprid stood at USD 17,120.8 per metric ton in 2022.

- The fluctuations in the prices of active ingredients are primarily influenced by the rising costs of raw materials, which constitutes one of the significant contributing factors to the growth of the market.

Africa Insecticide Industry Overview

The Africa Insecticide Market is fragmented, with the top five companies occupying 24.69%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 South Africa

- 5.3.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球農藥市場報告(2026 年)

全球農藥市場報告(2026 年) 農藥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

農藥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 技術級多殺菌素市場依製劑類型、作物類型、害蟲類型和應用方法分類-2026-2032年全球預測殺蟲劑種子處理市場-2026-2031年預測

技術級多殺菌素市場依製劑類型、作物類型、害蟲類型和應用方法分類-2026-2032年全球預測殺蟲劑種子處理市場-2026-2031年預測 按類型、作物、劑型和地區分類的農藥市場規模、佔有率和成長分析 - 2026-2033 年行業預測按劑型、作物類型、應用方法、最終用戶和銷售管道的Buprofezin市場—2025-2032年全球預測氯蟲苯甲醯胺市場按作物類型、製劑類型、應用方法、最終用戶和作用機制分類-2025-2032年全球預測殺蟲劑種子處理市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、作物類型、形態、應用方法、地區及競爭情況分類,2020-2030 年)

按類型、作物、劑型和地區分類的農藥市場規模、佔有率和成長分析 - 2026-2033 年行業預測按劑型、作物類型、應用方法、最終用戶和銷售管道的Buprofezin市場—2025-2032年全球預測氯蟲苯甲醯胺市場按作物類型、製劑類型、應用方法、最終用戶和作用機制分類-2025-2032年全球預測殺蟲劑種子處理市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、作物類型、形態、應用方法、地區及競爭情況分類,2020-2030 年)

▼