|

市場調查報告書

商品編碼

1683985

中國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)China Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

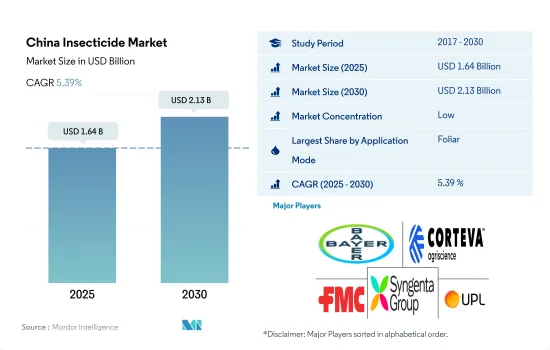

預計 2025 年中國農藥市場規模為 16.4 億美元,到 2030 年將達到 21.3 億美元,預測期內(2025-2030 年)的複合年成長率為 5.39%。

害蟲壓力的增加、農作物損失的增加以及對有效害蟲防治方法的需求正在推動對殺蟲劑的需求。

- 中國農藥市場規模不斷擴大,使用方式也日益多樣化。這種多樣化的應用技術提供了廣泛的選擇,可以有效控制害蟲並確保作物保護。

- 葉面噴布佔據中國殺蟲劑市場的主導地位。預計 2023 年至 2029 年期間,該產業的以金額為準複合年成長率將達到 5.8%。機械化、優良作物品種和先進農耕技術等現代農業實踐的快速採用是這一成長的主要驅動力。隨著農民採用這些進步,他們意識到有效的害蟲控制在最佳化作物產量方面所扮演的角色。這項認知進一步推動了對殺蟲劑(尤其是葉面噴布)的需求,使其成為中國害蟲管理策略不可或缺的一部分。

- 預計 2023 年至 2029 年間,經濟作物殺蟲劑種子處理市場將成長 450 萬美元。種子處理已成為中國大型商業種植者的標準做法。透過採用這種方法,他們實現了保護對高價值作物的投資的好處。

- 土壤處理是中國農藥市場成長最快的領域之一,預計預測期內以金額為準年成長率為 5.2%。該國農民擴大採用這種方法作為其害蟲管理策略的一部分,因為它可以長期控制害蟲,預防土壤傳播的疾病,並改善整體作物健康和生產力。因此,預計 2023 年至 2029 年中國殺蟲劑市場以金額為準的複合年成長率為 5.7%。

中國殺蟲劑市場趨勢

農藥使用量零成長和病蟲害綜合治理策略已顯著減少每公頃農藥消費量

- 由於多種因素,中國每公頃農藥消費量將從2017年到2022年下降13.1%。近年來,中國政府推出了多項政策,旨在減少農藥使用、禁止使用有害殺蟲劑產品、實現化學農藥消費量零成長。這些政策是該國促進永續農業和盡量減少農業實踐對環境影響的更廣泛努力的一部分。因此,人們開始轉向替代方案,例如使用基因改造作物和植物來源蛋白酶抑制劑。

- 基因改造作物,也稱為基因改造作物(GMO),已被開發來抵抗特定的害蟲。透過將天然抗蟲物種的基因引入作物,可以在不使用化學農藥的情況下保護作物免受某些害蟲的侵害。這種方法在中國很受歡迎,中國已經成功種植了基改棉花、玉米和其他作物。

- 除了基因改造作物外,中國還在探索使用植物來源蛋白酶抑制劑作為合成農藥的天然替代品。蛋白酶抑制劑是阻斷蛋白酶活性的物質,蛋白酶是參與昆蟲各種生理功能的酵素。透過將這些抑制劑加入作物中,可以擾亂害蟲的消化系統並減少它們對植物造成的損害。

- 由於這些政府政策的實施和替代性病蟲害防治方法的日益採用,中國每公頃土地使用的農藥量正在減少。

活性成分的價格在很大程度上受到當地氣候、疾病爆發、能源價格和人事費用等因素的影響。

- 在中國,受作物病蟲害影響的農地面積在過去50年增加了四倍,這主要是由於氣候變遷造成的。中國最常見的害蟲是鱗翅目害蟲,包括蛾和蝴蝶(還有秋粘蟲),佔受災農田的三分之一以上。接下來是同翅目昆蟲,包括蚜蟲、蟬和葉蟬。

- Cypermethrin是使用最廣泛的擬除蟲菊酯類農藥,在中國用於防治蔬菜和水果上的果蠅、紅火蟲、蟋蟀等多種害蟲。 2022 年其價格為每噸 20,900 美元。

- Malathion用於控制多種害蟲,包括蚜蟲、跳甲和許多其他吸食珍貴作物汁液的害蟲。中國廣泛種植且經常與Malathion一起使用的五種作物是櫻桃番茄、西蘭花、桑葚、蔓越莓和無花果。 2022 年的價格為每噸 12,400 美元。低毒性是Malathion最大的優勢之一,中國致力於研發低毒性高效率的農藥,並降低潛在的環境風險。這些因素可能會進一步影響中國Malathion的價格。

- Imidacloprid是一種典型的新菸鹼類殺蟲劑,2022年價格為每噸1.7萬美元。Imidacloprid主要用於防治水稻、小麥、蔬菜、棉花等作物中的飛蝨和蚜蟲。稻米是Imidacloprid最大的消費者,小麥是中國第二大作物。

- 活性成分的價格在很大程度上受到當地氣候、疾病爆發、能源價格和人事費用等因素的影響。

中國農藥產業概況

中國農藥市場較為分散,前五大企業的市佔率達37.15%。市場的主要企業是:拜耳股份公司、科迪華農業科技、FMC 公司、先正達集團和 UPL 有限公司(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 中國

- 價值鏈與通路分析

第5章 市場區隔

- 如何使用

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001687

The China Insecticide Market size is estimated at 1.64 billion USD in 2025, and is expected to reach 2.13 billion USD by 2030, growing at a CAGR of 5.39% during the forecast period (2025-2030).

The rising pest pressure, increasing crop losses, and the need for effective pest control methods are driving the demand for insecticides

- The Chinese insecticide market is experiencing growth across various application methods. These diverse application techniques offer a wide range of options to effectively control insect pests and ensure crop protection.

- The foliar application method dominates the insecticide market in China. This segment is projected to register a CAGR of 5.8% in terms of value from 2023 to 2029. The rapid adoption of modern agricultural practices, such as mechanization, enhanced crop varieties, and advanced farming techniques, has been a key driver of this growth. As farmers adopt these advancements, they are increasingly realizing the role of effective pest control in optimizing crop yields. This recognition has further fueled the demand for insecticides, specifically through foliar application, as an essential part of pest management strategies in China.

- Between 2023 and 2029, the insecticide seed treatment market in commercial crops is projected to grow by USD 4.5 million. Large-scale commercial growers in China are adopting seed treatment as standard practice. By adopting this method, they are recognizing the advantages of protecting their investments in highly valuable crops.

- Soil treatment is one of the fastest-growing segments in the insecticide market in China, which is expected to register a CAGR of 5.2% in terms of value during the forecast period. Farmers in the country are increasingly incorporating this method into their pest management strategies due to its effectiveness in long-term pest control, prevention of soil-borne diseases, and enhancement of overall crop health and productivity. Therefore, the Chinese insecticide market is forecast to register a CAGR of 5.7% in terms of value during 2023-2029.

China Insecticide Market Trends

Zero growth in pesticide usage and IPM strategies have contributed to a significant reduction in the per hectare insecticide consumption

- The consumption of insecticides in China per hectare decreased by 13.1% from 2017 to 2022, attributed to several factors. In recent years, China has implemented several government policies aimed at reducing the usage of insecticides, banning harmful insecticidal products, and achieving zero growth in chemical pesticide consumption. These policies are part of the country's broader efforts to promote sustainable agriculture and minimize the environmental impact of agricultural practices. As a result, there has been a shift toward alternative methods of pest control, including the use of transgenic crops and plant-derived protease inhibitors.

- Transgenic crops, also known as genetically modified organisms (GMOs), have been developed with built-in resistance to certain pests. Introducing genes from naturally pest-resistant species into crops can help them defend themselves against specific insects without the need for chemical insecticides. This approach has gained traction in China, where genetically modified cotton, maize, and other crops have been successfully cultivated.

- In addition to transgenic crops, China has been exploring the use of plant-derived protease inhibitors as a natural alternative to synthetic insecticides. Protease inhibitors are substances that inhibit the activity of proteases, which are enzymes involved in various physiological processes of insects. Incorporating these inhibitors into crops can aim to disrupt the digestive systems of insect pests, rendering them less harmful to plants.

- The implementation of the above-mentioned government policies and the rising adoption of alternative pest control methods have contributed to a reduction in the usage of insecticides per hectare in China.

Active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country

- The amount of farmland hit by crop pests in China has quadrupled in the past 50 years, mainly due to climate change. The most prevalent pests in China are lepidoptera, the order that includes moths and butterflies (and fall armyworms), which accounted for more than a third of the affected cropland. This was followed by homoptera, which includes aphids, cicadas, and leafhoppers.

- Cypermethrin is the most widely used pyrethroid pesticide to control many pests, such as fruit flies, borers, and mealy bugs in vegetables and fruits in China. It was valued at a price of USD 20.9 thousand per metric ton in 2022.

- Malathion is used to control a wide range of pests, including aphids, fleas, and other sucking pests on a number of valuable crops. Five crops that are extensively grown in China that use malathion frequently are cherry tomato, broccoli, mulberry, cranberry, and fig. It was valued at a price of USD 12.4 thousand per metric ton in 2022. Low toxicity is one of malathion's largest advantages, as China is dedicated to developing low-toxic and highly efficient pesticides to reduce potential environmental risks. Such factors will further influence the price of malathion in China.

- Imidacloprid is a typical neonicotinoid insecticide, priced at USD 17.0 thousand per metric ton in 2022. Imidacloprid is mainly used in the control of planthoppers and aphids on crops like rice, wheat, vegetables, and cotton. Rice is the largest consumer of imidacloprid, and wheat ranks second among crops cultivated in China.

- The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Insecticide Industry Overview

The China Insecticide Market is fragmented, with the top five companies occupying 37.15%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

家用殺蟲劑市場-全球產業規模、佔有率、趨勢、機會及預測(按昆蟲類型、化學類型、形態、地區和競爭情況細分,2020-2030 年)

家用殺蟲劑市場-全球產業規模、佔有率、趨勢、機會及預測(按昆蟲類型、化學類型、形態、地區和競爭情況細分,2020-2030 年) 2025-2029年全球電子殺蟲器市場

2025-2029年全球電子殺蟲器市場 亞太地區農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)儲糧殺蟲劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)儲糧殺蟲劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼