|

市場調查報告書

商品編碼

1683980

亞太地區農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Asia Pacific Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

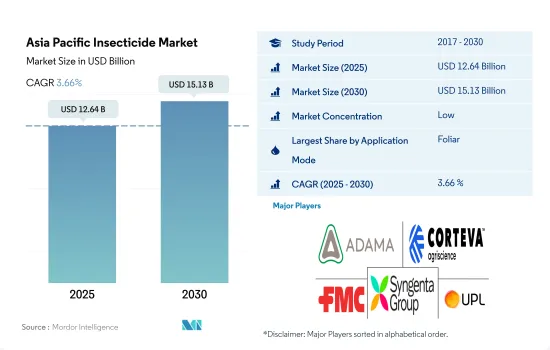

預計 2025 年亞太地區殺蟲劑市場規模為 126.4 億美元,到 2030 年將達到 151.3 億美元,預測期內(2025-2030 年)的複合年成長率為 3.66%。

由於病蟲害侵襲導致產量損失不斷增加,推動了市場的發展。

- 在該地區大多數國家中,農業發揮著至關重要的作用並對 GDP 貢獻巨大。然而,病蟲害對農作物生產的風險很大,導致產量下降、農民經濟損失和對糧食安全的擔憂。亞太地區氣候和土壤多樣,適合種植多種作物。

- 該地區採用各種噴灑方法來控制蟲害。 2022年,葉面噴布佔比最高,以金額為準計算為57.0%。作為綜合害蟲管理策略的一部分,使用Chlorantraniliprole、Emamectin benzoate和乙基多殺菌素進行葉面噴布已被證明在該地區非常有效。

- 土壤治療方法在 2022 年以以金額為準計算佔比第三高,為 9.9%。人們發現,向土壤噴灑殺蟲劑是控制昆蟲最簡單、最安全、最有效的方法。說到農業害蟲,大約 95% 的生命階段的一部分是在地下度過的,所以正如我們已經說過的,把它們留在地下是至關重要的。

- 然而,使用葉面噴布殺蟲劑對消費者、工人和環境的健康和危害有幾個。化學灌溉,即利用滴灌系統在土壤中施用殺蟲劑,可以消除葉面噴布殺蟲劑的一些通用缺點。 2022 年化學灌溉的以金額為準佔有率為 7.4%。

- 由於旨在創造最安全、最有效的噴塗方法的研究和創新不斷增加,預計市場在預測期內(2023-2029 年)的複合年成長率將達到 3.9%。

氣候變遷導致害蟲威脅加劇,推動市場成長

- 2022年,亞太地區將佔全球市場佔有率的34.8%。亞太地區農業規模龐大,害蟲數量較多,是農藥的主要市場之一。該地區廣泛使用殺蟲劑來保護作物免受昆蟲和害蟲的侵害並確保更高的產量。

- 由於廣泛採用殺蟲劑保護農作物以及人們越來越意識到昆蟲對作物產量和生產力的影響,印度、中國、日本和澳洲等國家佔據了大部分市場佔有率。

- 採用現代農業實踐和增加耕地面積等農業活動的擴大促進了市場的成長。該地區的耕地面積將從2019年的6.245億公頃增加到2022年的6.622億公頃。隨著農業的成長,需要有效的解決方案來保護作物免受病蟲害的侵害。

- 氣候變遷導致破壞作物的害蟲蔓延。因此,未來幾年對殺蟲劑的需求可能會增加。

- 中國預計將成為各地區中成長速度最快的地區,預測期內(2023-2029 年)的複合年成長率為 5.7%,因為由於病蟲害威脅加劇和農作物損失增加,預計中國農民將增加農藥使用量。

- 由於農業部門的不斷擴大、作物保護需求的不斷成長以及氣候變遷導致的農藥需求增加,預計亞太地區農藥市場在 2023 年至 2029 年期間的複合年成長率將達到 3.9%。

亞太農藥市場趨勢

氣溫升高會促進臭蟲等各種害蟲的生長,從而增加每公頃土地的殺蟲劑消費量。

- 在亞太地區,日本每公頃農藥消費量最高,從 2017 年到 2022 年增加了約 7%。這一成長可歸因於害蟲數量的顯著增加。根據農林水產省報告,臭蟲危害嚴重,近年來日益猖獗。專家表示,臭蟲等害蟲氾濫的主要因素是全球暖化。控制臭蟲和其他害蟲侵擾的主要方法是使用化學殺蟲劑,噴灑頻率和噴灑量增加是越南每公頃農藥消費量增加的主要原因。

- 以每公頃農藥使用量來看,越南是該地區第二大國家。每公頃農藥使用量將大幅增加,從 2017 年的 750 克增加到 2022 年的 1,200 克。這一成長可歸因於採用集約化作物生產技術來提高生產力和控制害蟲。越南屬於熱帶氣候,高溫、高濕、降雨頻繁,為農業生產提供了有利條件,但也促進了害蟲的快速繁殖。因此,該國每公頃土地的農藥消費量正在增加。

- 整體來看,亞太地區其他國家每公頃農藥消費量與前一年同期比較也有所增加。氣候變遷導致害蟲數量增加是造成此趨勢的主要原因。

甘蔗、棉花、水果和蔬菜等主要作物對殺蟲劑的需求不斷增加,有利於有效成分價格上漲。

- 除了氣候變遷之外,害蟲對該地區的農業部門構成了重大威脅,造成平均產量損失高達 73% 至 100%。為了有效對抗這些害蟲,農民嚴重依賴化學農藥。

- 該地區使用最廣泛的殺蟲劑是Cypermethrin,它具有合成除蟲菊酯的特性,可以有效控制多種害蟲,包括鱗翅目、鞘翅目、雙翅目和半翅目。在印度、中國和越南等國家,Cypermethrin主要用於防治各種作物的害蟲。中國和越南是Cypermethrin的主要進口國。截至2022年,該有效成分的價格已上漲至每噸21,037.7美元,自2017年以來大幅上漲了21.1%。此次價格大幅上漲主要是因為甘蔗、棉花、水果和蔬菜等作物對Cypermethrin的需求增加。

- Imidacloprid是一種新菸鹼類殺蟲劑,用於多種作物的種子披衣、土壤處理和葉面處理,包括棉花、水稻、油籽、水果、蔬菜和種植作物,如茶、咖啡和豆蔻。其主要目的是消滅吸食汁液的害蟲。中國是Imidacloprid的主要出口國,而印度和越南則是該殺蟲劑的主要進口國。活性成分價格為每噸17,105.7美元,較2017年大幅上漲21.2%。

- 需求增加、進口關稅和外匯波動等各種因素導致活性成分價格波動。

亞太農藥產業概況

亞太地區殺蟲劑市場較為分散,前五大公司佔了21.92%的市場。該市場的主要企業是:ADAMA Agricultural Solutions Ltd、Corteva Agriscience、FMC Corporation、Syngenta Group 和 UPL Limited(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 價值鏈與通路分析

第5章 市場區隔

- 如何使用

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001682

The Asia Pacific Insecticide Market size is estimated at 12.64 billion USD in 2025, and is expected to reach 15.13 billion USD by 2030, growing at a CAGR of 3.66% during the forecast period (2025-2030).

The market is being driven by growing yield losses due to increasing pest infestations

- In most of the countries in the region, agriculture has a key role to play and contributes substantially to GDP. Nevertheless, there is a significant risk to crop production due to the infestations of insects that result in reduced yields, financial losses for farmers, and concerns about food security. The diversity of climate and soil in Asia-Pacific allows for the cultivation of different crops.

- Various application methods are adopted in the region to manage insect infestation. The foliar application method occupied the highest share of 57.0% by value in 2022. It has been observed that the use of foliar spraying with chlorantraniliprole, emamectin benzoate, and spinetoram as part of an integrated pest management strategy has been quite effective in the region.

- The soil treatment method occupied the third highest share of 9.9% by value in 2022. It has been observed that insecticide application on soil appeared to be the easiest, safest, and most efficient way of controlling insects. In terms of agricultural pests, approximately 95% have passed some portion of their lives in the soil, and therefore, it is essential for them to be held underground, as already mentioned.

- Nevertheless, there are several drawbacks to the health of consumers, workers, and the environment from using foliar pesticides. Chemigation uses pesticides in soil with drip irrigation systems and may remove several drawbacks common to foliar insecticide applications. Chemigation occupied a share of 7.4% by value in 2022.

- Owing to the increase in research and innovation, which are aimed to bring out the safest and most effective method of application, the market is anticipated to register a CAGR of 3.9% during the forecast period (2023-2029).

The rising threat of pests with changing climate is contributing to the growth of the market

- Asia-Pacific accounted for 34.8% of the market share of the global insecticide market in 2022. Asia-Pacific is one of the important markets for insecticides due to its large agricultural sector and the prevalence of pests in the region. Insecticides are widely used in the region to protect crops from insects and pests, ensuring higher yields.

- Countries such as India, China, Japan, and Australia hold a substantial share of the market due to the wide adoption of insecticides to protect crops and the rise in awareness about the effects of insects on crop yield and productivity.

- The expansion of agriculture activities, such as adapting modern agriculture practices and increasing the area under agricultural cultivation, contributes to the market's growth. The region witnessed an increase in acreage under cultivation to 662.2 million hectares in 2022 from 624.5 million hectares in 2019. As agriculture increases, effective solutions are needed to protect crops from pests.

- The changing climate is leading to the spread of insect pests that can damage crops. Due to this, the demand for insecticides may increase in the coming years.

- China is expected to grow fastest in the region at a CAGR of 5.7% during the forecast period (2023-2029) because the farmers in the country are expected to increase the usage of insecticide owing to the rising threat of pests and increasing crop losses.

- The Asia-Pacific insecticide market is forecasted to record a CAGR of 3.9% during 2023-2029 due to the increasing demand for insecticides due to the expansion of the agriculture sector, the rising need to protect crops, and the changing climate.

Asia Pacific Insecticide Market Trends

The rise in climate temperatures favors various insect pests like stink bugs to grow, increasing insecticide consumption per hectare

- In Asia-Pacific, Japan exhibits higher per-hectare consumption of insecticide, which witnessed approximately a 7% increase from 2017 to 2022. This rise may be attributed to the substantial growth in the population of insect pests. The Ministry of Agriculture, Forestry, and Fisheries reports that stink bugs, which pose significant threats to agricultural crops, have been increasingly prevalent in recent years. According to experts, the primary factor driving the proliferation of stink bugs and other pests is attributed to global warming. The principal approach to managing infestations of stink bugs and other pests involves the use of chemical insecticides, with the intensified frequency and dosages of the application being the primary factors contributing to the augmented consumption of insecticides per hectare in the country.

- Vietnam is the second country in the region in terms of insecticide usage per hectare. The amount of insecticide used per hectare significantly increased from 750 g in 2017 to 1,200 g in 2022. This rise may be attributed to the adoption of intensive crop production techniques aimed at improving productivity and pest control. Vietnam's tropical climate, characterized by high temperatures, humidity, and frequent rainfall, provides favorable conditions for agriculture but also promotes the rapid proliferation of insect pests. As a result, insecticide consumption per hectare has increased in the country.

- In overall, other countries in Asia-Pacific are also experiencing a YoY increase in insecticide consumption per hectare. Climate changes leading to an increase in the population of insect pests' infestations are primary reasons for this trend.

Increased demand for insecticides in major crops like sugarcane, cotton, and fruits and vegetables favors the active ingredient price growth

- In addition to climate changes, insect pests present a significant threat to the agriculture sector in the region, causing average yield losses of up to 73% to 100%. To combat these insect pests effectively, farmers are heavily relying on chemical insecticides.

- Cypermethrin holds a dominant position as the most widely used insecticide in the region, known for its synthetic pyrethroid properties that effectively control various insect pests, including Lepidoptera, Coleoptera, Diptera, and Hemiptera. Countries like India, China, and Vietnam predominantly rely on cypermethrin for pest control across various crops. China and Vietnam are the primary importers of cypermethrin. As of 2022, the price of the active ingredient increased to USD 21,037.7 per metric ton, reflecting a significant rise of 21.1% since 2017. This notable price increase was primarily attributed to the escalating demand for cypermethrin in crops such as sugarcane, cotton, and fruits and vegetables.

- Imidacloprid, a neonicotinoid insecticide, finds application as a seed dressing, soil treatment, and foliar treatment in various crops, including cotton, rice, oilseeds, fruits, and vegetables, and plantation crops like tea, coffee, and cardamom. Its primary purpose is to control sucking insect pests. China serves as the major exporter of Imidacloprid, while India and Vietnam are the main importing countries for this insecticide. The price of the active ingredient stood at USD 17,105.7 per metric ton, representing a significant increase of 21.2% compared to 2017.

- Various factors, such as rising demand, import tariffs, and fluctuations in exchange rates, contribute to the fluctuation in the price of the active ingredients.

Asia Pacific Insecticide Industry Overview

The Asia Pacific Insecticide Market is fragmented, with the top five companies occupying 21.92%. The major players in this market are ADAMA Agricultural Solutions Ltd, Corteva Agriscience, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

家用殺蟲劑市場-全球產業規模、佔有率、趨勢、機會及預測(按昆蟲類型、化學類型、形態、地區和競爭情況細分,2020-2030 年)

家用殺蟲劑市場-全球產業規模、佔有率、趨勢、機會及預測(按昆蟲類型、化學類型、形態、地區和競爭情況細分,2020-2030 年) 2025-2029年全球電子殺蟲器市場

2025-2029年全球電子殺蟲器市場 中國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)儲糧殺蟲劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)儲糧殺蟲劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印尼農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農藥:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼