|

市場調查報告書

商品編碼

1686579

印度電力:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)India Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

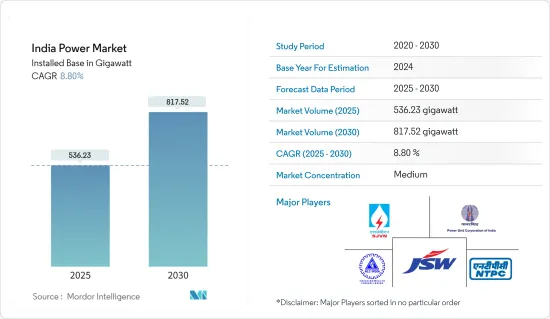

印度電力市場規模預計將從 2025 年的 536.23 吉瓦擴大到 2030 年的 817.52 吉瓦,預測期內(2025-2030 年)的複合年成長率為 8.8%。

主要亮點

- 從中期來看,政府支持政策、基礎設施建設導致的電力需求增加以及人口成長等因素將在預測期內推動市場發展。

- 同時,建立和現代化發電、輸電和配電網路需要大量投資,而私營部門投資疲軟預計將阻礙印度電力市場的成長。

- 然而,印度太陽照度充足,全年都能接收太陽能。這為利用太陽能創造了絕佳的機會,尤其是來自拉賈斯坦邦、古吉拉突邦和安得拉邦等陽光最充足的地區。上述因素加上外國投資和大型電力計劃為印度電力市場的成長提供了機會。

印度電力市場趨勢

火力發電佔市場主導地位

- 印度擁有豐富的煤炭蘊藏量,使其成為一種易於取得且相對廉價的發電燃料。印度煤炭蘊藏量豐富,既是煤炭生產大國,也是煤炭消費大國,因此火力發電廠成為滿足日益成長的電力需求的一個有吸引力的選擇。

- 此外,印度已建立起燃煤發電基礎設施。眾多煤礦、交通網和燃煤發電廠已投入運作。現有的基礎設施是支撐我們在火力發電市場佔據主導地位的基礎。

- 此外,2022年9月,印度能源部宣布,準備在2030年增加高達56吉瓦的燃煤發電能力,以滿足不斷成長的電力需求。燃煤發電能力的增加將比目前燃煤發電廠高出約 25%。

- 截至2023年11月,印度嚴重依賴火力發電,總設備容量為23,907兆瓦,佔全國總發電量的56%以上。

- 此外,火力發電廠(尤其是使用煤炭的火力發電廠)與可再生等替代能源相比具有成本競爭力。建立火力發電廠的初始資本投資通常較低,而且與波動的石油和天然氣價格相比,包括燃料成本在內的營業成本相對穩定。

- 火力發電廠非常適合滿足基本負載需求(滿足消費者日常需求所需的最低電量),因為它們可以提供穩定可靠的電力供應。能夠提供穩定的電力供應使得火力發電在市場上佔優勢。

- 因此,如上所述,火力發電部門很可能在預測期內佔據市場主導地位。

政府政策和支持可望推動市場

- 政府政策和支援是印度電力市場的主要驅動力,因為它們提供了電力產業發展所需的清晰藍圖、財政獎勵、法律規範和基礎設施發展。透過推廣可再生能源、能源效率、電網整合和數位化,政府正在創造有利環境來吸引投資、促進永續並促進印度向永續和可靠的電力市場轉型。

- 印度政府制定了雄心勃勃的再生能源目標,以增加再生能源在其整體能源結構中的佔有率。國家太陽能計劃、國家風能計劃以及各州可再生能源政策等獎勵和支持可再生能源發電計劃的發展。這些舉措旨在吸引投資、簡化監管流程、提供財務獎勵並確保為可再生能源的發展提供有利的環境。

- 為了推動國家的永續轉型,政府設定了一個雄心勃勃的目標,在 2030 年實現可再生能源裝置容量達到 500 吉瓦 (GW)。該目標包括安裝 280GW 的太陽能和 140GW 的風能,旨在推動全國範圍內的重大綠色革命。

- 截至 2022 年,印度的可再生能源裝置容量超過 162 吉瓦,而 2021 年為 147 吉瓦,這表明可再生能源的採用有所增加,從而推動了印度電力市場的發展。

- 2023年3月,印度製定了擴大可再生能源領域的明確路線圖,為再生能源領域的發展繪製了清晰的藍圖。作為這個願景的一部分,印度正致力於在2024年3月之前建立總合發電量達到40吉瓦的超大型大規模太陽能發電廠園區。這項雄心勃勃的舉措表明了印度對擴大可再生能源基礎設施和促進永續未來的堅定承諾。

- 此外,政府也提供一系列財政獎勵和補貼,鼓勵採用可再生能源和能源效率措施。這些措施包括資本補貼、以發電為基礎的獎勵、稅收優惠、優惠融資和可行性缺口融資。這些獎勵使可再生能源計劃具有財務吸引力,並鼓勵私營部門參與電力市場。

- 因此,如上所述,預計政府支持政策將在預測期內推動市場發展。

印度電力業概況

印度電力市場是半固定的。該市場的主要企業(不分先後順序)包括 NTPC Ltd、NLC India Ltd、SJVN Ltd、JSW Group、Power Grid Corporation India Ltd 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場概述

- 介紹

- 印度2028年發電產能預測

- 各州裝置容量佔比(%)(2022年)

- 印度2028年發電量及消費量預測(單位:兆瓦時)

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 能源需求不斷成長

- 政府對電力業的支持

- 限制因素

- 財務能力

- 驅動程式

- 供應鏈分析

- PESTLE分析

第5章市場區隔

- 按電源

- 火力

- 水力發電

- 可再生能源

- 其他

- 輸配電

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Adani Group

- JSW Group

- NHPC Ltd

- NLC India Ltd.

- NTPC Ltd.

- Power Grid Corporation India Ltd.

- Reliance Power Limited

- SJVN Ltd.

- Tata Power Company Limited

- Torrent Power Ltd.

第7章 市場機會與未來趨勢

- 可再生能源的成長

簡介目錄

Product Code: 52852

The India Power Market size in terms of installed base is expected to grow from 536.23 gigawatt in 2025 to 817.52 gigawatt by 2030, at a CAGR of 8.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, factors such as supportive government policies, rising electricity demand due to infrastructural activities, and rising population are expected to drive the market during the forecasted period.

- On the other hand, huge investment is required to set up and modernize power generation, transmission & distribution networks, and weak private sector investments are expected to hinder the growth of the Indian power market.

- Nevertheless, India has abundant availability of solar irradiance and receives solar energy throughout the year. This has created enormous opportunities to exploit solar energy from the sunniest sites in the country, especially Rajasthan, Gujarat, and Andhra Pradesh. The factor above, clubbed with foreign investment and extensive power projects, provides an opportunity to grow the power market in India.

India Power Market Trends

Thermal Source for Power Generation to Dominate the Market

- India has significant coal reserves, a readily available and relatively affordable fuel source for power generation. The country's large coal reserves have made it a major producer and consumer, making thermal power plants an attractive option for meeting the growing electricity demand.

- Moreover, India has a well-established infrastructure for coal-based thermal power generation. Numerous coal mines, transportation networks, and coal-fired power plants are already operating. This existing infrastructure provides a foundation for the market's dominance of thermal power generation.

- Furthermore, in September 2022, the Ministry of Energy India announced that the country is preparing to add as much as 56 GW of coal-fired generation capacity by 2030 to meet the growing electricity demand. The increase in coal-fired capacity would represent about a 25% jump above the country's current 204 GW of coal-fueled generation from 285 coal thermal power plants.

- As of November 2023, India heavily relies on thermal power sources for generating electricity, with a total installed capacity of 239.07 GW, accounting for more than 56% of the country's electricity generation capacity.

- Additionally, thermal power plants, especially those using coal, have been cost-competitive compared to alternative sources such as renewable energy. The initial capital investment for setting up thermal power plants is often lower, and the operating costs, including fuel costs, have been relatively stable compared to volatile oil and gas prices.

- Thermal power plants can provide a consistent and reliable supply of electricity, making them suitable for meeting the base load demand, which is the minimum level of power required to meet the everyday needs of consumers. The ability to provide a stable power supply has contributed to the dominance of thermal sources in the market.

- Therefore, as mentioned above, the thermal power sector will likely dominate the market during the forecasted period.

Government Policies and Support are Expected to Drive the Market

- Government policies and support are crucial drivers of the Indian power market as they provide a clear roadmap, financial incentives, regulatory frameworks, and infrastructure development necessary for the sector's growth. By promoting renewable energy, energy efficiency, grid integration, and digitalization, the government creates an enabling environment that attracts investments, fosters innovation, and facilitates the transition toward a sustainable and reliable power market in India.

- The Indian government has set ambitious renewable energy targets to increase the share of renewables in the overall energy mix. Policies such as the National Solar Mission, National Wind Energy Mission, and various state-level renewable energy policies provide incentives and support for developing renewable power projects. These initiatives aim to attract investments, streamline regulatory processes, provide financial incentives, and ensure a favorable environment for renewable energy growth.

- To catalyze a sustainable transformation in the nation, the government has established a formidable objective of achieving 500 gigawatts (GW) of installed renewable energy capacity by 2030. This target encompasses the installation of 280 GW from solar power and 140 GW from wind power sources, aiming to drive a significant green revolution across the country.

- As of 2022, the country has more than 162 GW of installed renewable energy capacity compared to 147 GW in 2021, signifying the increasing adaption of renewable energy in the country, consequently driving the power market in India.

- In March 2023, India charted a definitive path for expanding its renewable energy sector, outlining a clear roadmap for its growth. As part of this vision, the country is committed to establishing Ultra Mega Solar Parks with a combined generation capacity of 40 gigawatts by March 2024. This ambitious initiative demonstrates India's steadfast dedication to scaling up its renewable energy infrastructure and fostering a sustainable future.

- Additionally, the government offers various financial incentives and subsidies to promote renewable energy deployment and energy efficiency measures. These include capital subsidies, generation-based incentives, tax benefits, concessional financing, and viability gap funding. Such incentives make renewable projects financially attractive and encourage private sector participation in the power market.

- Therefore as per the above mentioned point, supportive government policies are expected to drive the market during the forecasted period.

India Power Industry Overview

The Indian power market is semi-consolidated. Some key players in this market (not in a particular order) include NTPC Ltd, NLC India Ltd, SJVN Ltd, JSW Group, and Power Grid Corporation India Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 India Installed Power Generating Capacity Forecast, till 2028

- 4.3 Share of Installed Power Generation Capacity (%), by State, India, 2022

- 4.4 Electricity Generation and Consumption Forecast, in Terawatt Hours, India, till 2028

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Increasing Energy Demand

- 4.7.1.2 Government Support for Power Sector

- 4.7.2 Restraints

- 4.7.2.1 Financial Viability

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Generation

- 5.1.1 Thermal

- 5.1.2 Hydro

- 5.1.3 Renewable

- 5.1.4 Others

- 5.2 Transmission and Distribution

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Adani Group

- 6.3.2 JSW Group

- 6.3.3 NHPC Ltd

- 6.3.4 NLC India Ltd.

- 6.3.5 NTPC Ltd.

- 6.3.6 Power Grid Corporation India Ltd.

- 6.3.7 Reliance Power Limited

- 6.3.8 SJVN Ltd.

- 6.3.9 Tata Power Company Limited

- 6.3.10 Torrent Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Renewable Energy Growth

02-2729-4219

+886-2-2729-4219

再生能源 PPA 概況和公平價格展望:2025 年 3 月

再生能源 PPA 概況和公平價格展望:2025 年 3 月 英國容量市場展望:對本週的T-4拍賣有何期待?

英國容量市場展望:對本週的T-4拍賣有何期待? 2025年能源與電力領域人工智慧(AI)全球市場報告

2025年能源與電力領域人工智慧(AI)全球市場報告 2025 年至 2029 年全球電力交易市場

2025 年至 2029 年全球電力交易市場 電力零售 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

電力零售 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 歐洲電力:回顧 2024 年

歐洲電力:回顧 2024 年 歐洲的電力與再生能源:2025 年值得關注的事情中國發電:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)亞太電力 -市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電力:市場佔有率分析、產業趨勢與成長預測(2025-2030)

歐洲的電力與再生能源:2025 年值得關注的事情中國發電:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)亞太電力 -市場佔有率分析、產業趨勢、成長預測(2025-2030)北美電力:市場佔有率分析、產業趨勢與成長預測(2025-2030)

▼