|

市場調查報告書

商品編碼

1687474

鉛酸電池-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Lead-acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

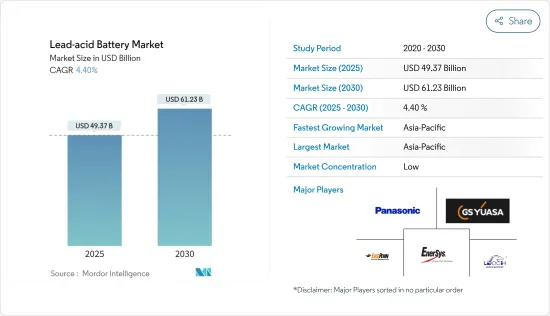

預計 2025 年鉛酸電池市場規模為 493.7 億美元,到 2030 年將達到 612.3 億美元,預測期內(2025-2030 年)的複合年成長率為 4.4%。

儘管2020年新冠疫情對市場產生了負面影響,但目前已恢復至疫情前的水準。

主要亮點

- 從中期來看,汽車銷售的成長預計將刺激鉛酸電池市場的成長。

- 然而,預計成本下降和鋰離子電池採用率的提高將阻礙預測期內的市場成長。

- 鉛酸電池市場正在經歷多項技術發展,如吸收式玻璃纖維隔板 (AGM) 電池和增強型富液電池 (EFB) 技術,預計這些技術將在預測期內為市場提供重大機會。

- 預計亞太地區將主導鉛酸電池市場,大部分需求來自中國、日本和印度。

鉛酸電池市場趨勢

SLI電池領域佔據市場主導地位

- SLI 電池專為汽車使用而設計,並始終安裝在汽車的充電系統中,這意味著汽車使用時電池會不斷充電和放電。 50 多年來,12V 電池一直是最常用的電池。但其平均電壓(在汽車中使用並由交流發電機充電時)接近 14 伏特。

- 2021 年,SLI 電池的市場佔有率為 75.32%。由於全球汽車產業的成長,預計該細分市場的佔有率在預測期內將會擴大。OEM和售後市場不斷成長的需求正在推動汽車行業的發展。

- SLI 電池市場成長的主要驅動力是對電池的需求不斷成長,用於為啟動馬達、照明、點火系統和其他內燃機供電,同時確保高性能、長壽命和成本效益。

- 鉛酸電池是全球所有傳統內燃機車輛(例如汽車和卡車)中 SLI 電池應用的首選技術。

- 國際汽車工業組織 (OICA) 表示,全球汽車銷售在 2020 年下滑後正在復甦。 2021年全球汽車銷量較2020年成長4.96%。

- 雖然未來 30 至 40 年內傳統內燃機市場預計將萎縮,但替代汽車技術預計將繼續使用 SLI 鉛酸電池為各種車載電子設備和安全功能供電。

亞太地區佔市場主導地位

- 預計亞太地區將主導鉛酸電池市場,大部分需求來自中國、日本和印度。

- 截至2021年,中國是最大的電動車市場,銷量約330萬輛。

- 電動車的普及與清潔能源政策相吻合。中國政府計劃放寬汽車製造商的進口限制,以縮小供需缺口。目前,外國汽車製造商需繳納25%的進口關稅,或必須在中國建廠,且在中國的持股比例上限為50%。預計電動車製造商將率先從這些變化中受益。

- 此外,印度汽車產業的成長、太陽能發電工程數量的增加以及通訊基礎設施的持續擴張預計將推動對鉛酸電池的需求。

- 電訊業仍然是印度鉛酸電池最有前景的終端用戶之一。過去十年,印度通訊業實現了強勁成長。例如,根據印度電訊監管局的數據,2022 年 3 月無線和行動電話用戶總數達到 11.4208 億。

- 然而,印度鉛酸電池市場正面臨鋰離子電池技術的挑戰,這導致人們更加關注鉛酸電池的研發活動。為了保持與鋰離子電池的競爭力,製造商面臨著提供更高品質、壽命更長、維護更少的電池的壓力。

鉛酸電池產業概況

鉛酸電池市場比較分散。該市場的主要企業(不分先後順序)包括Panasonic Corporation、GS Yuasa 有限公司、EnerSys、East Penn Manufacturing Co. 和 Leoch International Technology Limited。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 2027 年市場規模與需求預測

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 限制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場區隔

- 按應用

- SLI(啟動、照明、點火)電池

- 固定電池(電訊、UPS、能源儲存系統(ESS)等)

- 可攜式電池(用於家用電器等)

- 其他用途

- 依技術

- 沈水式

- VRLA(閥控鉛酸蓄電池)

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 俄羅斯聯邦

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Johnson Controls International PLC

- Exide Technologies Inc.

- GS Yuasa Corporation

- EnerSys

- East Penn Manufacturing Co.

- C&D Technologies Inc.

- Amara Raja Batteries Ltd

- Leoch International Technology Limited

- Panasonic Corporation

第7章 市場機會與未來趨勢

The Lead-acid Battery Market size is estimated at USD 49.37 billion in 2025, and is expected to reach USD 61.23 billion by 2030, at a CAGR of 4.4% during the forecast period (2025-2030).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Over the medium term, the increasing sales of automobiles are expected to stimulate the growth of the lead-acid battery market.

- On the other hand, declining costs and increasing adoption of lithium-ion batteries are expected to hinder the growth of the market during the forecast period.

- The lead-acid battery market has witnessed several developments in technologies like AGM (Absorbed Glass Mat) batteries and EFB (Enhanced Flooded Battery) technology, which are expected to provide great opportunities for the market during the forecast period.

- Asia-Pacific is expected to dominate the lead-acid battery market, with most of the demand coming from China, Japan, and India.

Lead Acid Battery Market Trends

SLI Battery Segment to Dominate the Market

- SLI batteries are designed for automobiles and are always installed with the vehicle's charging system, which means there is a continuous cycle of charge and discharge in the battery whenever the vehicle is in use. The 12-volt batteries have been the most commonly used for over 50 years. However, their average voltage (while in use in the car and being charged by the alternator) is close to 14 volts.

- The SLI batteries segment held a 75.32% market share in 2021. Its share is expected to grow during the forecast period, owing to worldwide growth in the automotive sector. The growing demand from OEMs and aftermarkets has boosted the automotive sector.

- The major factors attributed to the growth of the SLI battery market are the increasing demand for these batteries to power start motors, lights, ignition systems, or other internal combustion engines while ensuring high performance, long life, and cost-efficiency.

- The lead-acid battery is the technology of choice for all SLI battery applications in conventional combustion engine vehicles, such as cars and trucks worldwide.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), motor vehicle sales globally have been recovering after a downfall in 2020. In 2021, the world witnessed a 4.96% rise in motor vehicle sales compared to 2020.

- Although the conventional combustion engine market is expected to decline over the next 30-40 years, replacement car technologies are expected to continue using SLI-type lead-acid batteries to provide power for various electronics and safety features within the vehicle.

Asia-Pacific to Dominate the Market

- The Asia-Pacific is expected to dominate the lead-acid battery market, with most demand coming from China, Japan, and India.

- As of 2021, China is the largest electric vehicle market, selling around 3.3 million vehicles.

- The increasing adoption of electric vehicles aligns with the clean energy policy. The Chinese government plans to ease restrictions on automakers importing cars into the country to reduce the demand-supply gap. Currently, foreign automakers face a 25% import tariff or have to build a factory in China with a cap of 50% ownership. Electric vehicle makers are expected to be the first to benefit from this change.

- Moreover, in India, the growing automobile sector, the increasing number of solar power projects, and the continuous expansion of telecommunication infrastructure are expected to drive the demand for lead-acid batteries in the country.

- The telecom sector remains one of India's most promising end users for lead-acid battery use. The Indian telecommunication sector has registered strong growth over the past decade. For instance, according to the Telecom Regulatory Authority of India, the total wireless or mobile telephone subscriber base reached 1142.08 million in March 2022.

- However, the lead-acid battery market in India faces challenges from lithium-ion battery technology, which has led to an increased focus on research and development activities pertaining to lead-acid batteries. Manufacturers are being forced to offer high-quality, long-lasting batteries with low maintenance to sustain the competition from lithium-ion batteries.

Lead Acid Battery Industry Overview

The lead-acid battery market is fragmented. Some of the key players in this market (in no particular order) include Panasonic Corporation, GS Yuasa Corporation, EnerSys, East Penn Manufacturing Co., and Leoch International Technology Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 SLI (Starting, Lighting, Ignition) Batteries

- 5.1.2 Stationary Batteries (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.1.3 Portable Batteries (Consumer Electronics, etc.)

- 5.1.4 Other Applications

- 5.2 By Technology

- 5.2.1 Flooded

- 5.2.2 VRLA (Valve Regulated Lead-acid)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 Italy

- 5.3.2.4 United Kingdom

- 5.3.2.5 Russian Federation

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 South Africa

- 5.3.4.4 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies Inc.

- 6.3.3 GS Yuasa Corporation

- 6.3.4 EnerSys

- 6.3.5 East Penn Manufacturing Co.

- 6.3.6 C&D Technologies Inc.

- 6.3.7 Amara Raja Batteries Ltd

- 6.3.8 Leoch International Technology Limited

- 6.3.9 Panasonic Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年鉛酸電池市場報告(按產品、製造方法(富液式、閥控式密封鉛酸電池)、銷售管道、應用和地區分類)

2025 年至 2033 年鉛酸電池市場報告(按產品、製造方法(富液式、閥控式密封鉛酸電池)、銷售管道、應用和地區分類) 北美鉛酸電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

北美鉛酸電池:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 2025年鉛酸電池全球市場報告

2025年鉛酸電池全球市場報告 全球鉛酸電池市場報告 - 行業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年全球先進鉛酸電池市場報告印度的電動三輪車用鉛蓄電池市場評估:各類型,極板類型,按容量(安培時間),各流通管道,各地區,機會,預測,2018~2032年

全球鉛酸電池市場報告 - 行業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年全球先進鉛酸電池市場報告印度的電動三輪車用鉛蓄電池市場評估:各類型,極板類型,按容量(安培時間),各流通管道,各地區,機會,預測,2018~2032年 按產品類型、製造方法、最終用途和地區分類的鉛酸電池市場

按產品類型、製造方法、最終用途和地區分類的鉛酸電池市場 鉛酸電池回收市場 2025-2029

鉛酸電池回收市場 2025-2029 鉛酸電池回收市場機會、成長動力、產業趨勢分析與預測 2025 - 2034SLI用鉛酸電池-市場佔有率分析、產業趨勢、成長預測(2025-2030)

鉛酸電池回收市場機會、成長動力、產業趨勢分析與預測 2025 - 2034SLI用鉛酸電池-市場佔有率分析、產業趨勢、成長預測(2025-2030)