|

市場調查報告書

商品編碼

1687724

根瘤菌:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Rhizobium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

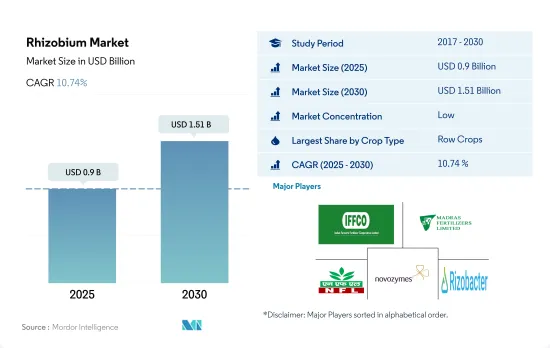

根瘤菌市場規模預計在 2025 年為 9 億美元,預計到 2030 年將達到 15.1 億美元,預測期內(2025-2030 年)的複合年成長率為 10.74%。

- 根瘤菌和豆科植物根部之間的特異性相互作用產生一種高度受調控的過程,稱為調節,將大氣中的氮轉化為可吸收的植物營養物質。這種能力是細菌接種劑在田間作物生產中使用的基礎。 2022年的菌根真菌市場以連續作物為主,約佔金額的69.7%。世界上最重要的連續作物是大麥、玉米、小麥、油菜籽、黑麥、向日葵、大豆和稻米。

- 預計 2022 年園藝作物根瘤菌生物肥料市場規模將達到 1.372 億美元,使用量為 4,900 噸。根瘤菌菌株附著在番茄和辣椒的根部,促進生產各階段的生長,提高幼苗和果實的產量和品質。它也用於番茄、辣椒和其他園藝水果的溫室栽培。

- 咖啡、茶葉、可可、棉花、甘蔗、油菜籽、向日葵和煙草是世界主要的經濟作物。 2022 年,經濟作物佔根瘤菌生物肥料市場價值的 6,870 萬美元。北美佔據經濟作物市場的主導地位,2022 年約為 5,220 萬美元。

- 根瘤菌接種可以為植物提供所需的氮,同時減少無機氮肥的需求。有效的根瘤菌接種劑可以提供提高產量所需的總氮量的50-70%。根瘤菌也會產生維生素、胺基酸、鐵載體、生長素和固氮。

- 由於上述特性和根瘤菌肥料應用的不斷增加,預計市場將在 2023 年至 2029 年間成長。

- 根瘤菌是共生植物,是棲息於豆科植物根瘤中的最重要的固氮細菌。根瘤菌是全球消費量第二大的生物肥料,到2022年將佔25.4%的市佔率。

- 據估計,根瘤菌的微生物活動在各種豆科作物中每公頃每年固定40至250公斤的氮。歐盟計畫透過擴大豆類作物種植面積,實現向永續植物蛋白生產的轉變。

- 北美在全球根瘤菌市場佔據主導地位,2022 年的市場佔有率為 52.7%。北美根瘤菌生物肥料市場以連續作物為主,約佔 2022 年市場金額的 62.4%。連續作物的主導地位是由於根瘤菌與連續作物中包含的作物共生。由於該地區連續作物種植的普及,其市場價值預計將增加,2023 年至 2029 年的複合年成長率為 13.0%。

- 非制度作物需要額外施用氮肥來提高作物的產量潛力。利用生物固氮菌可以增加穀物、水果和蔬菜等非反芻作物的產量。根瘤菌生物肥料市場以耕作作物為主,田間作物佔據了大面積的種植面積,約佔2022年金額的69.8%。已知將根瘤菌生物肥料施用於果蔬作物可以增加養分的利用率並產生必要的植物激素。

全球根瘤菌市場趨勢

在北美和歐洲,由於人們認知的不斷提高和政府的舉措,有機產量達到了歷史最高水準。

- 有機農業已成為永續糧食系統的主要貢獻者,並已在全球 187 個國家實踐。截至2021年,全球有機農地面積為7,230萬公頃,2018年至2021年間各地區平均成長2.9%。有機種植面積為1,440萬公頃,佔有機農地總面積的19.9%。

- 有機農業最強大的市場是北美和歐洲,這兩個地區佔世界有機種植面積的 41.0%。 2022年,歐洲將擁有650萬公頃有機耕地,佔總有機耕地面積的44.1%。北美和歐洲最重要的有機種植作物是蘋果、草莓、穀物和橄欖。

- 亞太地區的新興國家也正在加入有機農業運動,並在生產和供應新鮮有機農產品方面實現自給自足,以滿足國內需求。有機農業趨勢在亞太地區日益興起,2017 年至 2022 年間,該地區的有機土地面積將增加 18.8%。該地區政府的主要措施也在有機農業擴張趨勢中發揮了關鍵作用。例如,日本的食品、農業和農村基本計畫旨在2030年將有機農場和有機農地的數量增加兩倍。

- 有機農業的成長源於人們對其益處的認知不斷提高,例如促進土壤健康、減少環境影響和生產更健康的食品。

人均有機食品支出的成長主要出現在美國和德國,這是由消費者對更健康、更永續食品的需求所推動的。

- 過去幾年,有機食品市場經歷了顯著成長,全球銷售額預計將從 2012 年的 708 億美元成長到 2020 年的 1,206 億美元。有機食品的趨勢受到多種因素的推動,包括消費者對更健康、更永續的食品選擇的需求不斷成長,以及對傳統農業對環境影響的認知不斷提高。預計未來幾年全球有機食品市場將持續維持成長趨勢。

- 根據有機貿易協會 2021 年的一項調查,當年有機水果和蔬菜的銷售額成長了約 4.5%,佔有機產品總銷售額的 15%。北美在有機產品平均支出方面佔據市場主導地位,2021年美國的人均支出達到186.7美元,是北美國家中最高的。歐洲有機食品市場預計也將強勁成長,其中德國 2021 年的人均有機食品支出最高,達到 75.6 美元。

- 有機食品市場仍由消費者可支配收入較高的已開發國家主導,但有機食品市場在新興國家預計也將成長。例如,亞太地區的工人階級不斷壯大,這使得有機食品更容易取得且價格更便宜,有助於擴大市場。

根瘤菌產業概況

根瘤菌市場較為分散,前五大公司的市佔率為28.14%。市場的主要企業是:印度農民化肥合作社有限公司、馬德拉斯化肥有限公司、國家化肥有限公司、諾維信和 Rizobacter(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機栽培面積

- 有機產品人均支出

- 法律規範

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中國

- 埃及

- 法國

- 德國

- 印度

- 印尼

- 義大利

- 日本

- 墨西哥

- 荷蘭

- 奈及利亞

- 菲律賓

- 俄羅斯

- 南非

- 西班牙

- 泰國

- 土耳其

- 英國

- 美國

- 越南

- 價值鏈與通路分析

第5章 市場區隔

- 作物類型

- 經濟作物

- 園藝作物

- 耕作作物

- 地區

- 非洲

- 按國家

- 埃及

- 奈及利亞

- 南非

- 非洲其他地區

- 亞太地區

- 按國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 按國家

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲國家

- 中東

- 按國家

- 伊朗

- 沙烏地阿拉伯

- 其他中東地區

- 北美洲

- 按國家

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 按國家

- 阿根廷

- 巴西

- 南美洲其他地區

- 非洲

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介.

- Indian Farmers Fertiliser Cooperative Limited

- Indogulf BioAg LLC(Biotech Division of Indogulf Company)

- IPL Biologicals Limited

- Lallemand Inc.

- Madras Fertilizers Limited

- National Fertilizers Limited

- Novozymes

- Rizobacter

- T Stanes and Company Limited

- Vittia Group

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 64662

The Rhizobium Market size is estimated at 0.9 billion USD in 2025, and is expected to reach 1.51 billion USD by 2030, growing at a CAGR of 10.74% during the forecast period (2025-2030).

- The specific interaction between rhizobia and legume roots results in the formation of a highly regulated process termed modulation, which converts atmospheric nitrogen into an assimilable plant nutrient. This ability provides the basis for the use of bacterial inoculants in field crop production. Row crops dominated the mycorrhiza market in 2022, accounting for around 69.7% of market value. Globally, the most important row crops are barley, maize, wheat, rapeseed, rye, sunflower, soybean, and rice.

- The market for rhizobium-based biofertilizers in horticultural crops is expected to be worth USD 137.2 million, with 4.9 thousand metric tons used in 2022. Rhizobium strains colonize the roots of tomato and pepper plants to encourage growth at various stages of production, increasing seedling and fruit yield and quality. It is also utilized in greenhouse culture, such as tomato and capsicum farming, as well as other horticultural fruit growing.

- Coffee, tea, cocoa, cotton, sugarcane, rapeseed, sunflower, and tobacco are some of the major cash crops grown globally. Cash crops accounted for USD 68.7 million in the market value of rhizobium-based biofertilizers in 2022. North America dominated the market for cash crops and accounted for about USD 52.2 million in 2022.

- Rhizobium inoculation can provide plant nitrogen requirements while decreasing the demand for inorganic nitrogen fertilizer. Effective rhizobium inoculation can deliver up to 50-70% of the total nitrogen required to boost yields. Rhizobium also generates vitamins, amino acids, siderophores, auxins, and nitrogen fixation.

- Owing to the above-mentioned characteristics and the increase in the application of rhizobium-based fertilizers, the market is anticipated to grow between 2023 and 2029.

- Rhizobium is the most important nitrogen-fixing bacterium that exists in a symbiotic relationship with plants and lives in the root nodules of leguminous plants. Rhizobium is the second most consumed among biofertilizers globally and accounted for a share of 25.4% in the year 2022.

- It has been estimated that 40-250 kg of nitrogen per hectare per year is fixed by different legume crops by the microbial activities of rhizobium. The European Union is planning to make the transition toward sustainable plant protein production through the expansion of the area under leguminous crop cultivation.

- North America dominated the global rhizobium market with a market share of 52.7% in 2022. Row crops dominate the rhizobium biofertilizer market in North America, and they accounted for about 62.4% of the market value in 2022. The dominance of row crops is due to rhizobium's symbiotic association with leguminous crops, which come under row crops. Due to the large cultivation of row crops in the region, their market value is anticipated to increase, registering a CAGR of 13.0% between 2023 and 2029.

- The requirement for additional application of nitrogen in non-leguminous crops is high in order to enhance the yield potential of the crops. The usage of biological nitrogen-fixing bacteria can increase the production of non-leguminous crops like cereals, fruits, and vegetables. Row crops dominate the rhizobium biofertilizer market and accounted for about 69.8% of the market value in 2022, owing to the large area under the cultivation of field crops. The application of rhizobium biofertilizers in fruit and vegetable crops is known to increase nutrient availability and produce required plant hormones.

Global Rhizobium Market Trends

Organic production is at an all-time high in North America and Europe, due to the increasing awareness and Government initiatives.

- Organic agriculture has emerged as a significant contributor to sustainable food systems, with 187 countries practicing it globally. As of 2021, there was 72.3 million ha of organic agricultural land worldwide, with an average increase of 2.9% across all regions from 2018 to 2021. Organic arable land accounted for 14.4 million ha, representing 19.9% of the total organic agricultural land.

- The strongest markets for organic farming are North America and Europe, accounting for 41.0% of the global organic arable land. In 2022, Europe had 6.5 million ha of organic arable land, equivalent to 44.1% of the overall organic arable agricultural area. The most significant crops grown organically in North America and Europe are apples, strawberries, cereals, and olives.

- Developing countries in Asia-Pacific are also joining the organic agriculture movement and becoming self-sufficient in producing and providing fresh organic produce to meet their domestic demand. The trend of organic farming is gaining momentum in Asia-Pacific, with the region recording an 18.8% increase in organic arable land from 2017 to 2022. The major initiatives by governments in the region also play a vital role in the growing trend of organic farming. For example, Japan's Basic Plan for Food, Agriculture, and Rural Areas aims to triple the number of organic farmers and lands by 2030.

- The growth of organic agriculture is driven by the rising awareness of the benefits of organic farming, such as promoting soil health, reducing environmental impacts, and producing healthier food.

Per capita spending of organic food majorly observed in United States and Germany, attributed to the consumer demand for healthier and sustainable food

- The organic food market experienced significant growth in the past few years, with global sales reaching USD 120.6 billion in 2020, up from USD 70.8 billion in 2012. The trend toward organic food is being driven by several factors, such as increasing consumer demand for healthier, more sustainable food options and a growing awareness of the environmental impact of conventional agriculture. The global organic food market is expected to continue its growth trend over the coming years.

- According to a survey conducted by the Organic Trade Association in 2021, sales of organic fruits and vegetables increased by around 4.5% in the same year, accounting for 15% of the overall organic sales. North America dominates the market in terms of average spending on organic products, with per capita spending in the United States reaching USD 186.7 in 2021, the highest among all North American countries. Europe is also expected to experience significant growth in the organic food market, with Germany accounting for the highest per capita spending of USD 75.6 in 2021.

- While the organic food market is still dominated by developed countries with high consumer disposable incomes, it is also expected to grow in developing nations. For example, the increasing number of working-class people in the Asia-Pacific region may contribute to the market's expansion due to the growing availability and affordability of organic food products.

Rhizobium Industry Overview

The Rhizobium Market is fragmented, with the top five companies occupying 28.14%. The major players in this market are Indian Farmers Fertiliser Cooperative Limited, Madras Fertilizers Limited, National Fertilizers Limited, Novozymes and Rizobacter (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 Egypt

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Netherlands

- 4.3.15 Nigeria

- 4.3.16 Philippines

- 4.3.17 Russia

- 4.3.18 South Africa

- 4.3.19 Spain

- 4.3.20 Thailand

- 4.3.21 Turkey

- 4.3.22 United Kingdom

- 4.3.23 United States

- 4.3.24 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Crop Type

- 5.1.1 Cash Crops

- 5.1.2 Horticultural Crops

- 5.1.3 Row Crops

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Country

- 5.2.1.1.1 Egypt

- 5.2.1.1.2 Nigeria

- 5.2.1.1.3 South Africa

- 5.2.1.1.4 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Country

- 5.2.2.1.1 Australia

- 5.2.2.1.2 China

- 5.2.2.1.3 India

- 5.2.2.1.4 Indonesia

- 5.2.2.1.5 Japan

- 5.2.2.1.6 Philippines

- 5.2.2.1.7 Thailand

- 5.2.2.1.8 Vietnam

- 5.2.2.1.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Country

- 5.2.3.1.1 France

- 5.2.3.1.2 Germany

- 5.2.3.1.3 Italy

- 5.2.3.1.4 Netherlands

- 5.2.3.1.5 Russia

- 5.2.3.1.6 Spain

- 5.2.3.1.7 Turkey

- 5.2.3.1.8 United Kingdom

- 5.2.3.1.9 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Country

- 5.2.4.1.1 Iran

- 5.2.4.1.2 Saudi Arabia

- 5.2.4.1.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Country

- 5.2.5.1.1 Canada

- 5.2.5.1.2 Mexico

- 5.2.5.1.3 United States

- 5.2.5.1.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Country

- 5.2.6.1.1 Argentina

- 5.2.6.1.2 Brazil

- 5.2.6.1.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Indian Farmers Fertiliser Cooperative Limited

- 6.4.2 Indogulf BioAg LLC (Biotech Division of Indogulf Company)

- 6.4.3 IPL Biologicals Limited

- 6.4.4 Lallemand Inc.

- 6.4.5 Madras Fertilizers Limited

- 6.4.6 National Fertilizers Limited

- 6.4.7 Novozymes

- 6.4.8 Rizobacter

- 6.4.9 T Stanes and Company Limited

- 6.4.10 Vittia Group

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國生物肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物有機肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)美國生物肥料市場:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

中國生物肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物有機肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)生物肥料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)美國生物肥料市場:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 2025年全球生物肥料市場報告

2025年全球生物肥料市場報告 全球生物肥料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年全球根瘤菌肥料市場報告

全球生物肥料市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年全球根瘤菌肥料市場報告 2025 年至 2033 年生物肥料市場報告(按類型、作物、微生物、應用方式和地區分類)根瘤菌生物肥料市場評估,依配方、作物類型、應用、最終用途、地區、機會和預測,2018-2032 年生物有機肥料市場 - 2025 年至 2030 年預測

2025 年至 2033 年生物肥料市場報告(按類型、作物、微生物、應用方式和地區分類)根瘤菌生物肥料市場評估,依配方、作物類型、應用、最終用途、地區、機會和預測,2018-2032 年生物有機肥料市場 - 2025 年至 2030 年預測

▼