|

市場調查報告書

商品編碼

1684572

PCR 塑膠包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測PCR Plastic Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

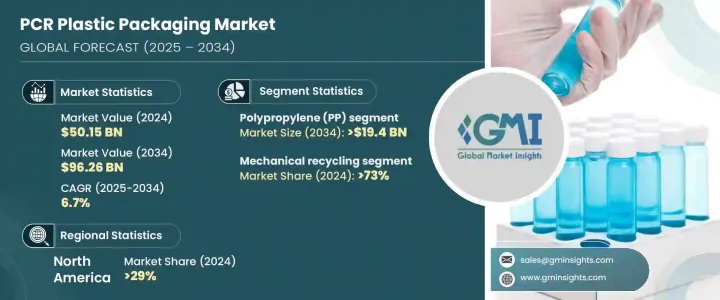

2024 年全球 PCR 塑膠包裝市場價值 501.5 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.7%。各行各業的公司擴大採用 PCR 塑膠,以符合環境目標並滿足消費者對環保產品的期望。向循環經濟的轉變和更嚴格的塑膠廢物管理法規進一步推動了市場的擴張。

市場按塑膠類型細分為聚對苯二甲酸乙二酯 (PET)、聚乙烯 (PE)、聚苯乙烯 (PS)、聚氯乙烯 (PVC)、聚丙烯 (PP) 和生物基塑膠。其中,聚丙烯 (PP) 預計將成長最快,預計複合年成長率為 8.4%,到 2034 年將達到 194 億美元。該材料的耐熱性和耐化學性使其成為需要高安全性和性能標準的包裝解決方案的可靠選擇。此外,人們對輕質耐用包裝材料的日益關注進一步推動了市場對 PP 的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 501.5億美元 |

| 預測值 | 962.6 億美元 |

| 複合年成長率 | 6.7% |

PCR塑膠包裝市場也依回收方法分為機械回收和化學回收。 2024 年,機械回收領域佔據最大佔有率,為 73%。該過程涉及對塑膠進行物理再加工而不改變其化學結構,使其適用於 PET、PP 和 PE 等常見材料。隨著回收基礎設施的改善和消費者對高回收含量包裝的需求上升,預計該領域將在未來幾年保持主導地位。化學回收雖然仍是新興事物,但因其處理混合和受污染塑膠的能力而受到關注,這可能為未來的市場成長開闢新的機會。

2024 年,北美佔據 PCR 塑膠包裝市場的 29%。越來越多的企業採用 PCR 塑膠作為其永續發展計畫的一部分,幫助減少碳足跡並促進回收。這種轉變在食品、飲料和個人護理產品等行業尤其明顯,這些行業非常重視使用在生產週期中可以輕鬆回收和再利用的包裝材料。該地區對先進回收技術的創新和投資的重視預計將進一步鞏固其在全球市場的地位。

總體而言,在不斷變化的消費者偏好、監管框架和回收技術進步的支持下,PCR 塑膠包裝市場有望大幅成長。隨著企業繼續優先考慮永續性,PCR 塑膠的採用可能會加速,為整個價值鏈的利害關係人創造新的機會。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 中斷

- 未來展望

- 製造商

- 經銷商

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 包裝解決方案中加速採用再生材料

- 擴大生產者責任延伸計畫 (EPR)

- 消費品對回收的寵物瓶的需求增加

- 寵物在推動需求和擴大回收能力方面發揮關鍵作用

- 品牌致力於循環經濟原則

- 產業陷阱與挑戰

- 多材料包裝回收的複雜性

- 高階產品中再生材料的負面看法

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按塑膠類型,2021-2034 年

- 主要趨勢

- 聚對苯二甲酸乙二醇酯(PET)

- 聚乙烯 (PE)

- 聚苯乙烯(PS)

- 聚氯乙烯(PVC)

- 聚丙烯(PP)

- 生物基塑膠

第 6 章:市場估計與預測:按回收分類,2021 年至 2034 年

- 主要趨勢

- 機械回收

- 化學回收

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 瓶子和托盤

- 袋子和麻袋

- 小袋和小袋

- 杯子和罐子

- 蛤殼

- 浴缸

- 其他

第 8 章:市場估計與預測:按最終用途產業,2021 年至 2034 年

- 主要趨勢

- 消費性電子產品

- 消費品

- 化妝品和個人護理

- 居家及清潔用品

- 其他

- 食品和飲料

- 醫療保健和製藥

- 零售

- 其他

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3plastics

- Amcor

- Berry Global

- Cambrian Packaging

- Evergreen Resources

- Glenroy

- Longdapac

- Mondi

- Proampac

- PTT Global Chemical

- Red Pack

- Regent Plast

- Sanle Plastic

- Udinc

- Winpak

The Global PCR Plastic Packaging Market was valued at USD 50.15 billion in 2024 and is expected to grow at a CAGR of 6.7% between 2025 and 2034. This market is witnessing significant growth as sustainability becomes a core focus for businesses, and the demand for alternatives to virgin plastics continues to rise. Companies across various industries are increasingly adopting PCR plastics to align with environmental goals and meet consumer expectations for eco-friendly products. The shift toward circular economies and stricter regulations on plastic waste management are further driving the market's expansion.

The market is segmented by plastic type into polyethylene terephthalate (PET), polyethylene (PE), polystyrene (PS), polyvinyl chloride (PVC), polypropylene (PP), and bio-based plastics. Among these, polypropylene (PP) is expected to see the fastest growth, projected to grow at a CAGR of 8.4%, reaching USD 19.4 billion by 2034. PP is gaining traction due to its versatility, strength, and wide range of applications, especially in packaging for food, healthcare, and consumer goods. The material's resistance to heat and chemicals makes it a reliable option for packaging solutions that require high safety and performance standards. Additionally, the growing focus on lightweight and durable packaging materials is further boosting the demand for PP in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $50.15 Billion |

| Forecast Value | $96.26 Billion |

| CAGR | 6.7% |

The PCR plastic packaging market is also divided by recycling method into mechanical recycling and chemical recycling. The mechanical recycling segment held the largest share of 73% in 2024. Mechanical recycling continues to lead due to its cost-efficiency and established methods. This process involves physically reprocessing plastics without changing their chemical structure, making them suitable for common materials such as PET, PP, and PE. As recycling infrastructure improves and consumer demand for packaging with high recycled content rises, this segment is expected to maintain its dominance in the coming years. Chemical recycling, while still emerging, is gaining attention for its ability to handle mixed and contaminated plastics, which could open new opportunities for market growth in the future.

North America accounted for a 29% share of the PCR plastic packaging market in 2024. In the United States, the market is growing rapidly, driven by increasing demand for eco-friendly products and the need to comply with state-level environmental regulations. Companies are increasingly adopting PCR plastics as part of their sustainability initiatives, helping to reduce carbon footprints and promote recycling. This shift is particularly evident in industries like food, beverages, and personal care products, where there is a strong emphasis on using packaging materials that can be easily recycled and reused in production cycles. The region's focus on innovation and investment in advanced recycling technologies is expected to further strengthen its position in the global market.

Overall, the PCR plastic packaging market is poised for substantial growth, supported by evolving consumer preferences, regulatory frameworks, and advancements in recycling technologies. As businesses continue to prioritize sustainability, the adoption of PCR plastics is likely to accelerate, creating new opportunities for stakeholders across the value chain.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Accelerated adoption of recycled content in packaging solutions

- 3.5.1.2 Expansion of extended producer responsibility (EPR) programs

- 3.5.1.3 Increased demand for recycled pet bottles in consumer goods

- 3.5.1.4 Pet's crucial role in driving demand and expanding recycling capacity

- 3.5.1.5 Brand commitment to circular economy principles

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Complexity in recycling multi-material packaging

- 3.5.2.2 Negative perceptions of recycled materials in premium products

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Plastic Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene terephthalate (PET)

- 5.3 Polyethylene (PE)

- 5.4 Polystyrene (PS)

- 5.5 Polyvinyl chloride (PVC)

- 5.6 Polypropylene (PP)

- 5.7 Bio-based plastics

Chapter 6 Market Estimates & Forecast, By Recycling, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Mechanical recycling

- 6.3 Chemical recycling

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Bottles & trays

- 7.3 Bags & sacks

- 7.4 Pouches & sachets

- 7.5 Cups & jars

- 7.6 Clamshells

- 7.7 Tubs

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Consumer goods

- 8.3.1 Cosmetics & personal care

- 8.3.2 Household & cleaning products

- 8.3.3 Others

- 8.4 Food & beverage

- 8.5 Healthcare & pharmaceutical

- 8.6 Retail

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3plastics

- 10.2 Amcor

- 10.3 Berry Global

- 10.4 Cambrian Packaging

- 10.5 Evergreen Resources

- 10.6 Glenroy

- 10.7 Longdapac

- 10.8 Mondi

- 10.9 Proampac

- 10.10 PTT Global Chemical

- 10.11 Red Pack

- 10.12 Regent Plast

- 10.13 Sanle Plastic

- 10.14 Udinc

- 10.15 Winpak

塑膠包裝:全球市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

塑膠包裝:全球市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 塑膠包裝市場按產品類型、最終用途行業和地區分類

塑膠包裝市場按產品類型、最終用途行業和地區分類 北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2030 年軟塑膠包裝市場預測:按產品類型、材料類型、最終用戶和地區進行的全球分析

2030 年軟塑膠包裝市場預測:按產品類型、材料類型、最終用戶和地區進行的全球分析 2025 年軟塑膠包裝全球市場報告

2025 年軟塑膠包裝全球市場報告 聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032

聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032 軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程

軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程 一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)