|

市場調查報告書

商品編碼

1629770

中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)Middle East And Africa Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

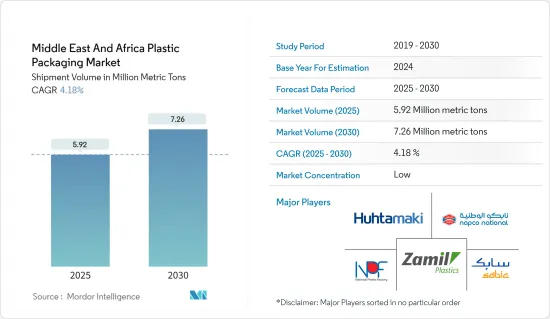

以出貨量為準,中東和非洲塑膠包裝市場規模預計將從2025年的592萬噸擴大到2030年的726萬噸,預測期間(2025-2030年)複合年成長率為4.18%。

主要亮點

- 隨著消費者的健康偏好和永續發展意識日益增強,以及中東和非洲法規的不斷發展,塑膠包裝專業人士感受到了創新的壓力。我們調整我們的材料、設計和技術來滿足這些不斷變化的需求。

- 在瓶裝水和軟性飲料消費量增加的支持下,飲料行業已成為塑膠包裝的主要最終用戶。阿拉伯聯合大公國和埃及的研究人員最近的一項研究揭示了一個驚人的趨勢。儘管阿拉伯聯合大公國有嚴格的市政水質標準,但仍有超過 80% 的參與者選擇普通瓶裝水。

- 可氧化可分解塑膠正在興起。中東和非洲國家,如阿拉伯聯合大公國、沙烏地阿拉伯、葉門、象牙海岸共和國、南非、加納和多哥等,不僅在推廣Oxo可分解塑膠。

- 隨著東非和西非國內經濟的蓬勃發展、消費市場的迅速擴大、收入的增加和年輕人口的增加,該大陸正在成為塑膠包裝產業的樞紐。

- 地方政府機構正在支持旨在減少碳排放和能源消耗的計劃,這表明了市場的積極前景。例如,2024 年 2 月,卡達市政部 (MoM) 開始向當地回收工廠免費提供可回收材料,強調其對永續性和循環經濟的承諾。

- 另一項舉措是,2023 年 12 月,終結塑膠廢棄物聯盟與沙烏地阿拉伯投資回收公司 (SIRC) 在杜拜簽署了一份合作備忘錄。這項戰略合作夥伴關係旨在在沙烏地阿拉伯部署有效的廢棄物管理解決方案,並專門解決與某些塑膠相關的挑戰。

- 新材料正在逐漸取代傳統塑膠,為市場供應商帶來了挑戰。此外,日益嚴重的環境問題和對永續包裝(例如紙質包裝)的需求不斷增加,可能會阻礙市場成長。

中東和非洲塑膠包裝市場趨勢

軟包裝預計將顯著成長

- 在中東和非洲,沙烏地阿拉伯、阿拉伯聯合大公國和埃及等國家主要推動藥品包裝的需求。各行業對軟塑膠解決方案(尤其是袋子)的關注和不斷成長的需求正在推動市場擴張。

- 由於對結構化包裝的需求不斷成長,預計該領域的銷量在預測期內將顯著成長。此外,隨著肉類和乳製品消費的增加,對塑膠包裝的需求也將增加。所有這些因素都促進了軟質塑膠包裝市場的快速成長。

- 中東的塑膠袋和小袋製造商具有獲得具成本效益原料和原油、聚丙烯等原料的優勢。這一優勢支持塑膠袋的本地生產及其在電子商務中的使用。

- 阿拉伯聯合大公國消費者食品偏好的變化正在為包裝行業,特別是食品和飲料行業創造巨大的成長機會。根據阿拉伯聯合大公國金融機構 Alpen Capital 的報告,由於其戰略定位和該地區不斷成長的人口,中東和非洲的食品工業預計將成長。疫情後線上食品宅配的激增增加了對包裝、套袋和標籤等軟包裝的需求,推動了產業成長。

- 此外,國內食品加工業的成長正在推動對塑膠包裝的需求。阿拉伯聯合大公國約有 568 家食品和飲料加工商,每年生產 596 萬噸,推動了該國對塑膠包裝的需求。此外,由於遊客數量的增加、消費者偏好的變化以及人們消費能力的提高,該國的食品服務業正在成長,這可能會在未來幾年推動市場成長。

沙烏地阿拉伯預計將經歷顯著成長

- 沙烏地阿拉伯在中東包裝產業佔據主導地位。除了著名的石油和天然氣行業外,它還擁有多樣化的工業活動,推動塑膠包裝的年度需求激增。

- 隨著全球油價下跌,沙烏地阿拉伯意識到迫切需要加強其非石油部門。為此,沙烏地阿拉伯推出了多項旨在擴大工業生產的措施和監管改革,包括國家工業發展和物流計畫(NIDLP)和2030年願景。

- 沙烏地阿拉伯的塑膠消費量在海灣合作理事會中處於領先地位。 GPCA 最近估計該國的人均塑膠消費量超過 95 公斤,突顯其為海灣合作理事會最大的塑膠消費國。此外,出於旅遊和教育目的,人們越來越接受西方文化,這將進一步提振市場。美食廣場和美食廣場的人氣飆升進一步強調了這種成長軌跡。

- 此外,已調理食品和冷凍食品部分描述了食用前需要最少準備或無需準備的已調理食品。由於快節奏的城市生活和多元文化的影響,這個細分市場在中東國家越來越受歡迎,特別是在阿拉伯聯合大公國和沙烏地阿拉伯。

- 沙烏地阿拉伯的加工肉品、水產品和肉類替代品市場正在成長。 2023年市場規模約為1,499.10噸。預計到 2027 年將增加至約 1,839.50 噸,反映了消費者對加工肉品偏好的變化和增加。

中東和非洲塑膠包裝產業概況

中東和非洲的塑膠包裝市場較為分散,有多家公司按地區營運。市場上的主要供應商正在採取產品創新和夥伴關係等策略來擴大市場範圍並保持競爭力。該市場的主要參與企業包括 SABIC、Zamil Plastic Industries Co、HuhtamakiFlexibles UAE (Huhtamaki Oyj)、National Plastic Factory LLC 和 Napco Group (Napco National)。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 回收和永續性景觀

- 行業法規、政策和標準

- 進出口分析

第5章市場動態

- 市場促進因素

- 對氧化可分解塑膠的需求

- 加工食品需求穩定成長

- 市場問題

- 有關回收和安全處置的環境問題

- 原料成本高且回收基礎設施有限

第6章 市場細分

- 硬質塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 聚對苯二甲酸乙二酯 (PET)

- 聚丙烯(PP)

- 聚苯乙烯 (PS) 和發泡聚苯乙烯 (EPS)

- 聚氯乙烯(PVC)

- 其他

- 依產品類型

- 瓶子和罐子

- 托盤/容器

- 蓋子與封口裝置

- 其他

- 按最終用戶產業

- 食物

- 飲料

- 醫療保健

- 化妝品/個人護理

- 居家護理

- 其他最終用戶產業(工業、電子商務等)

- 依材料類型

- 軟質塑膠包裝

- 依材料類型

- 聚乙烯(PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯 (CPP)

- 聚氯乙烯(PVC)

- 乙烯 - 乙烯醇(EVOH)

- 其他

- 依產品類型

- 小袋

- 包包

- 薄膜和包裝

- 其他

- 按最終用戶產業

- 食物

- 飲料

- 醫療保健

- 化妝品/個人護理

- 居家護理

- 其他最終用戶產業(工業、電子商務等)

- 依材料類型

- 按國家/地區

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 埃及

- 南非

第7章 競爭格局

- 公司簡介

- Zamil Plastic Industries Co.

- Takween Advanced Industries

- Packaging Products Company(PPC)

- PrimePak Industries Nigeria Ltd(Enpee Group)

- Constantia Flexibles Afripack

- Huhtamaki South Africa(Pty)Ltd

- Al Bayader International(H&H Group of Companies)

- Napco National

- Falcon Pack

- Arabian Flexible Packaging LLC

- Hotpack Packaging Industries LLC

- ENPI Group

- Gulf East Paper and Plastic Industries LLC

- 熱圖分析

第8章投資分析

第9章 市場機會及未來趨勢

The Middle East And Africa Plastic Packaging Market size in terms of shipment volume is expected to grow from 5.92 million metric tons in 2025 to 7.26 million metric tons by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Key Highlights

- As consumer preferences increasingly lean towards health-conscious and sustainable products, and with evolving regulations in the Middle East and Africa, professionals in plastic packaging are feeling the pressure to innovate. They are adjusting materials, designs, and technologies to align with these shifting demands.

- The beverage sector, buoyed by a rise in bottled water and soft drink consumption, emerges as the dominant end-user of plastic packaging. A recent study by researchers from the UAE and Egypt unveiled a striking trend: even with the UAE's stringent municipal water quality standards, over 80% of participants opted for bottled plain drinking water.

- Oxo-degradable plastics are on the rise. Countries in the Middle East and Africa, such as the UAE, Saudi Arabia, Yemen, Ivory Coast, South Africa, Ghana, and Togo, are not only endorsing oxo-degradable plastics but some have even made their use mandatory.

- With East and West Africa witnessing booming domestic economies, a surge in consumer markets, rising incomes, and a youthful demographic, the continent is emerging as a pivotal hub for the plastic packaging industry.

- Regional government agencies are backing projects aimed at curbing carbon emissions and energy consumption, signaling a positive outlook for the market. For example, in February 2024, Qatar's Ministry of Municipality (MoM) began offering recyclable materials at no cost to local recycling factories, underscoring their commitment to sustainability and a circular economy.

- In another move, December 2023 saw the Alliance to End Plastic Waste ink a Memorandum of Understanding (MoU) with Saudi Investment Recycling Company (SIRC) in Dubai. This strategic collaboration is set to roll out effective waste management solutions in Saudi Arabia, specifically addressing challenges linked to certain plastics.

- New materials, set to gradually take the place of conventional plastics, present a challenge for market vendors. Furthermore, growing environmental concerns and a rising demand for sustainable packaging, such as those crafted from paper, could pose hurdles to the market's growth.

Middle East And Africa Plastic Packaging Market Trends

Flexible Packaging is Expected to Witness Significant Growth

- Countries like Saudi Arabia, the United Arab Emirates and Egypt are primarily fueling the rising demand for pharmaceutical packaging in the Middle East and Africa. This emphasis and a growing demand for flexible plastic solutions, particularly pouches across various industries, propel the market's expansion.

- With a rising demand for structured packaging, the sector is poised for significant volume growth during the forecast period. Furthermore, as meat and dairy consumption increases, so will the demand for plastic packaging. All these factors contribute to the burgeoning market for flexible plastic packaging.

- Middle Eastern manufacturers of plastic bags and pouches are expected to benefit from access to cost-effective feedstock and raw materials, such as crude oil and polypropylene. This advantage bolsters the local production of plastic pouches and their use in e-commerce.

- The changing consumer food preferences in the United Arab Emirates have created significant growth opportunities in the packaging industry, especially for the food and beverage industry. According to report by Alpen Capital, a financial institute in United Arab Emirates, the food industry in the Middle East and African region is estimated to grow due to its strategic location and region's growing population. Post-pandemic, the surge in online food delivery has enhanced the demand for flexible packaging such as wraps, sleeves , labels and others, which is driving industry growth.

- Additionally, growth in the food processing industry in the country drives the demand for plastic packaging. Around 568 food and beverage processors operate across the United Arab Emirates, producing 5.96 million metric tonnes annually, boosting the demand for plastic packaging in the country. Also, the rise in the food service industry in the country due to a boost in tourism, changing consumer preferences, and the growing spending capacity of the population is likely to boost the market growth in the coming years.

Saudi Arabia is Expected to Witness Significant Growth

- Saudi Arabia stands out as a dominant player in the Middle Eastern packaging industry. Beyond its renowned oil and gas sector, the nation boasts a diverse array of industrial activities, fueling a surging annual demand for plastic packaging.

- In light of declining global crude oil prices, Saudi Arabia recognizes the imperative to bolster its non-oil sector. To this end, the nation has rolled out several initiatives and regulatory reforms, including the National Industrial Development and Logistics Program (NIDLP) and Vision 2030, aiming to amplify industrial production.

- Saudi Arabia leads the GCC in plastic consumption. Recent GPCA estimates highlight a per capita plastic consumption exceeding 95 kg, underscoring its position as the GCC's top plastic consumer. Additionally, a growing embrace of Western culture, spurred by tourism and educational pursuits, is poised to further energize the market. The burgeoning popularity of food malls and courts further underscores this growth trajectory.

- Furthermore, the ready-to-eat meals and frozen food segment offers prepared food that requires minimal or no preparation before consumption. This segment is gaining popularity in Middle Eastern countries, particularly in the United Arab Emirates and Saudi Arabia, due to the fast-paced urban lifestyle and diverse cultural influences.

- The Saudi Arabian market for processed meat, seafood, and meat alternatives is experiencing growth. In 2023, the market volume was approximately 1,499.10 metric tons. Projections indicate an increase to about 1,839.50 metric tons by 2027, reflecting the country's changing and growing consumer preferences for processed meat.

Middle East And Africa Plastic Packaging Industry Overview

The Middle East and Africa Plastic Packaging Market is fragmented in nature, with multiple players in the market operating regionally. The major vendors in the market adopt strategies such as product innovation and partnerships, among others, to expand their reach and stay competitive in the market. Some of the major players in the market are SABIC, Zamil Plastic Industries Co., and Huhtamaki Flexibles UAE (Huhtamaki Oyj), National Plastic Factory LLC, Napco Group (Napco National), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Recycling and Sustainability Landscape

- 4.5 Industry Regulation, Policy and Standards

- 4.6 Import-Export Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Oxo-Degradable Plastics

- 5.1.2 Steady Rise in Demand for Processing Food

- 5.2 Market Challenges

- 5.2.1 Environmental Concerns over Recycling and Safe Disposal

- 5.2.2 High Raw Material Costs and Limited Recycling Infrastructure

6 MARKET SEGMENTATION

- 6.1 Rigid Plastic Packaging

- 6.1.1 By Material Type

- 6.1.1.1 Polyethylene (PE)

- 6.1.1.2 Polyethylene Terephthalate (PET)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 6.1.1.5 Polyvinyl Chloride (PVC)

- 6.1.1.6 Other Material Types

- 6.1.2 By Product Type

- 6.1.2.1 Bottles and Jars

- 6.1.2.2 Trays and containers

- 6.1.2.3 Caps and Closures

- 6.1.2.4 Other Product Types

- 6.1.3 By End-User Industry

- 6.1.3.1 Food

- 6.1.3.2 Beverage

- 6.1.3.3 Healthcare

- 6.1.3.4 Cosmetics and Personal Care

- 6.1.3.5 Household Care

- 6.1.3.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 6.1.1 By Material Type

- 6.2 Flexible Plastic Packaging

- 6.2.1 By Material Type

- 6.2.1.1 Polyethylene (PE)

- 6.2.1.2 Bi-Orientated Polypropylene (BOPP)

- 6.2.1.3 Cast Polypropylene (CPP)

- 6.2.1.4 Polyvinyl Chloride (PVC)

- 6.2.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.2.1.6 Other Material Types

- 6.2.2 By Product Type

- 6.2.2.1 Pouches

- 6.2.2.2 Bags

- 6.2.2.3 Films & Wraps

- 6.2.2.4 Other Product Types

- 6.2.3 By End-User Industry

- 6.2.3.1 Food

- 6.2.3.2 Beverage

- 6.2.3.3 Healthcare

- 6.2.3.4 Cosmetics and Personal Care

- 6.2.3.5 Household Care

- 6.2.3.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 6.2.1 By Material Type

- 6.3 By Country

- 6.3.1 United Arab Emirates

- 6.3.2 Saudi Arabia

- 6.3.3 Egypt

- 6.3.4 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Zamil Plastic Industries Co.

- 7.1.2 Takween Advanced Industries

- 7.1.3 Packaging Products Company (PPC)

- 7.1.4 PrimePak Industries Nigeria Ltd (Enpee Group)

- 7.1.5 Constantia Flexibles Afripack

- 7.1.6 Huhtamaki South Africa (Pty) Ltd

- 7.1.7 Al Bayader International (H&H Group of Companies

- 7.1.8 Napco National

- 7.1.9 Falcon Pack

- 7.1.10 Arabian Flexible Packaging LLC

- 7.1.11 Hotpack Packaging Industries LLC

- 7.1.12 ENPI Group

- 7.1.13 Gulf East Paper and Plastic Industries LLC

- 7.2 Heat Map Analysis

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025 年軟塑膠包裝全球市場報告

2025 年軟塑膠包裝全球市場報告 聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032

聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032 軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程

軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程 一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印尼塑膠包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

印尼塑膠包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 德國塑膠包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

德國塑膠包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)