|

市場調查報告書

商品編碼

1639534

印尼塑膠包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Indonesia Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

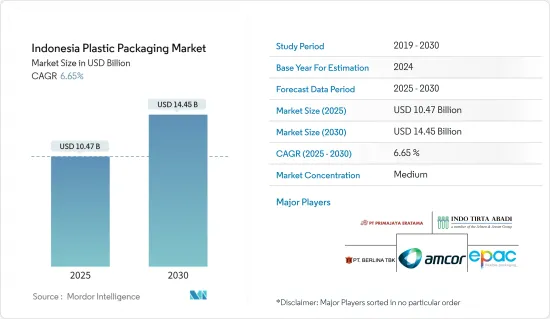

印尼塑膠包裝市場規模預計在 2025 年為 104.7 億美元,預計到 2030 年將達到 144.5 億美元,預測期內(2025-2030 年)的複合年成長率為 6.65%。

主要亮點

- 技術的進步和終端用戶行業中包裝應用的不斷擴大是推動印尼包裝市場成長的關鍵因素。該國不斷成長的人口和不斷增加的人均包裝消費量對這一趨勢貢獻巨大。消費行為的轉變,例如對便利產品的需求不斷增加以及擴大使用塑膠作為傳統包裝材料的替代品,進一步推動了市場擴張。

- 塑膠包裝為包裝行業的運作開闢了新的方式。耐用、輕巧和舒適的包裝解決方案正在推動整個全部區域塑膠作為包裝材料的使用增加。

- 經濟成長以及對方便、一次性食品的需求推動了印尼軟包裝產量的成長。在軟包裝產品類型中,由於人們生活節奏快、勞動人口眾多,印度的即食食品市場正在不斷擴大,因此預計小袋包裝將佔據主要佔有率。受訪的市場預計將選擇低成本的替代品來包裝液體和飲料,因此軟包裝很可能會被廣泛使用,因為它比其他類型的包裝更便宜。

- 目前該地區的 LDPE 包裝價格較低,這意味著使用這種材料的額外成本對商家的影響很小。由聚丙烯、聚異戊二烯和聚氨酯製成的外科口罩的需求也在增加。

- 塑膠污染已成為全球性環境問題,許多研究都強調了其對生態系統的負面影響。作為回應,印尼實施了限制塑膠使用的法規。由於塑膠樹脂價格上漲,印尼塑膠包裝市場目前面臨重大挑戰。這一趨勢導致樹脂成本上漲的恢復延遲,並降低了現有本地製造商的盈利。

印尼塑膠包裝市場趨勢

聚對苯二甲酸乙二醇酯(PET)佔據最大市場佔有率

- 由於重量輕且耐用, 寶特瓶擴大被用來代替玻璃瓶。這一轉變使得運輸瓶裝水和其他飲料變得更加經濟高效。 PET 的透明度和固有的二氧化碳阻隔性能使其適用於各種應用。該材料可輕鬆製成瓶子和其他形狀,並且可以透過色素、紫外線防護和氧氣阻隔等添加劑來增強其性能,以滿足特定品牌的要求。

- 在硬質包裝方面,PET 可用於生產各種產品的微波食品托盤和瓶子,包括軟性飲料、水、果汁、運動飲料、啤酒、調味品和食品容器。家庭護理、飲料和個人護理等多個領域對寶特瓶的需求都在成長。這種成長主要受消費者偏好以及 PET 的關鍵屬性(如重量輕、可回收性高)的推動。

- 隨著牛奶需求的增加,包裝的生產也隨之增加。這種成長帶動了對新製造設施的投資、生產能力的擴大和 PET 包裝技術的發展。

- 經濟合作暨發展組織預測,未來幾年印尼的原料乳製品消費量將會增加。經濟合作暨發展組織預測,未來幾年印尼原乳消費量將成長,年均成長率約為人均1公斤(+24.88%),2031年將達到人均1.2公斤消費量。

- 預計新鮮乳製品消費量的增加將對印尼寶特瓶包裝市場產生正面影響。 寶特瓶是包裝各種產品(包括乳製品)的常用材料。

食品板塊呈現顯著成長

- 快速的都市化以及超級市場、大賣場、雜貨店、便利商店和購物中心的興起正在擴大袋和袋子的市場。食品和飲料行業的成長也將對市場產生積極影響。此外,消費者對環保產品的偏好轉變也推動了對非生物分解塑膠袋和袋子的需求。

- 根據美國農業部(USDA)的報告,印尼為美國原料供應商滿足食品加工產業的原料需求提供了絕佳機會。美國是印尼第三大農產品供應國,市場佔有率11%。到2023年,大豆和乳製品將占美國對印尼農產品出口的一半左右。

- 自 2024 年 10 月 17 日起,印尼的許多食品、原料、添加劑和所有加工食品都必須獲得清真認證。

- 隨著對清真認證食品的需求增加,對符合清真標準的包裝的需求也可能隨之成長。這可能會導致經過認證或專門設計用於處理清真產品的塑膠包裝的需求增加。

- 有機食品產業經常強調永續性和環境責任。這一趨勢可能會刺激更環保的塑膠包裝解決方案的開發和採用,例如生物分解性塑膠和可回收的塑膠。公司可能會投資創造符合有機市場價值的包裝。

- 據有機貿易協會稱,2022 年印尼有機包裝食品消費約 1,570 萬美元。預計到 2025 年將成長至 1,900 萬美元。

印尼塑膠包裝產業概況

市場處於半靜態狀態並由少數主要企業推動。 Amcor Group、Prima Jaya Eratama、PT ePac Flexibles Indonesia、PT Berlina Tbk 和 PT Indo Tirta Abadi 在滿足日益成長的包裝解決方案需求方面發揮著至關重要的作用。這些公司不僅正在擺脫傳統的塑膠包裝,而且還在跟上消費者對永續塑膠替代品日益成長的偏好。為了加強市場地位,這些公司正在調整策略,擴大產品供應,並積極尋求以永續性為重點的合作夥伴關係和收購。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 擴大採用輕量化包裝方法

- 增加環保包裝和再生塑膠

- 市場挑戰

- 原料(塑膠樹脂)價格上漲

- 政府法規和環境問題

第6章 市場細分

- 硬質塑膠包裝

- 材料類型

- 聚乙烯 (PE)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚苯乙烯 (PS) 和發泡聚苯乙烯 (EPS)

- 聚氯乙烯(PVC)

- 其他材料

- 產品類型

- 瓶子和罐子

- 托盤和容器

- 其他產品類型

- 材料類型

- 軟質塑膠包裝

- 材料類型

- 聚乙烯 (PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 聚氯乙烯(PVC)

- 乙烯 - 乙烯醇(EVOH)

- 其他材料

- 產品類型

- 小袋

- 包包

- 薄膜和包裝

- 其他產品類型

- 材料類型

- 最終用戶產業

- 食物

- 飲料

- 衛生保健

- 化妝品和個人護理

- 其他最終用戶產業

第7章 競爭格局

- 公司簡介

- Amcor Group

- Prima Jaya Eratama

- PT ePac Flexibles Indonesia

- PT Berlina Tbk

- PT Indo Tirta Abadi

- Sonoco Products Company

- PT Solusi Prima Packaging

- PT Hasil Raya Industries

- PT Indonesia Toppan Printing

第8章投資分析

第9章:市場的未來

The Indonesia Plastic Packaging Market size is estimated at USD 10.47 billion in 2025, and is expected to reach USD 14.45 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Key Highlights

- Technological advancements and expanding end-user industry packaging applications are key factors driving the growth of Indonesia's packaging market. The country's increasing population and rising per capita packaging consumption contribute significantly to this trend. Consumer behavior shifts, including the growing demand for convenience products and the increased adoption of plastic as an alternative to traditional packaging materials, further propel market expansion.

- Plastic packaging has implemented new ways for the packaging industry to function. Durable, lightweight, and comfortable packaging solutions have augmented the use of plastics as a packaging material across the region.

- Economic growth and the need for single-serve, on-the-go convenience foods in Indonesia have increased flexible packaging production. Among flexible packaging product types, pouches are expected to hold a significant share due to the country's increasing market for Ready-to-Eat (RTE) foods, owing to the busy lifestyle and many working populations. The studied market is anticipated to opt for a low-cost alternative for liquid and beverage packaging and hence see wide usage of flexible packaging as it is cheaper than other types of packaging.

- The price of LDPE packaging is currently low in the region, which means that the additional cost of using the material will have minimal impact on sellers. The demand for surgical masks made of polypropylene, polyisoprene, and polyurethane has also increased.

- Plastic pollution has emerged as a global environmental concern, with numerous studies highlighting its detrimental effects on ecosystems. In response, Indonesia has implemented regulations to curb plastic usage. The Indonesian plastic packaging market now faces significant challenges due to rising plastic resin prices. This trend has resulted in delays in recovering increased resin costs and diminished profitability for established local manufacturers.

Indonesia Plastic Packaging Market Trends

Polyethylene Terephthalate (PET) Occupies the Largest Market Share

- Due to their lightweight and durable nature, PET bottles are increasingly replacing glass bottles. This shift allows for more cost-effective transportation of mineral water and other beverages. PET's transparency and inherent CO2 barrier properties suit it for various applications. The material can be easily moulded into bottles or other shapes, and its properties can be enhanced with additives such as colourants, UV blockers, and oxygen barriers to meet specific brand requirements.

- In rigid packaging, PET produces microwavable food trays and bottles for various products, including soft drinks, water, juices, sports drinks, beer, condiments, and food containers. The demand for PET bottles is growing across multiple sectors, including home care, beverages, and personal care. This growth is primarily driven by consumer preferences and PET's key attributes, such as its lightweight nature and high recyclability.

- Increased demand for milk will necessitate more packaging production. This growth can lead to investment in new manufacturing facilities, expanded production capabilities, and technological advancements in PET packaging.

- The Organisation for Economic Cooperation and Development forecasts that Indonesia's consumption of fresh milk products will increase over the coming years. They project a compound annual growth rate of approximately one kilogram per capita (+24.88%) and estimate that by 2031, the consumption per capita will reach 5.01 kg.

- This anticipated rise in fresh dairy product consumption is expected to impact Indonesia's PET bottle packaging market positively. PET bottles are a commonly used material for packaging various products, including dairy items.

Food Segment to Show Significant Growth

- Rapid urbanization and the growing number of supermarkets, hypermarkets, grocery stores, convenience stores, and shopping centers increase the market for pouches and bags. The growth of the food and beverage industry also positively impacts the market. Futhermore, the changing consumer preferences towards eco-friendly products also drive the need for non-biodegradable plastic pouches and bags.

- The United States Department of Agriculture (USDA) reports that Indonesia presents substantial opportunities for United States ingredient suppliers to meet the raw material needs of its food processing industry. The United States ranks as the third-largest agricultural supplier to Indonesia, holding an 11% market share. In 2023, soybeans and dairy products constituted approximately half of all US agricultural exports to Indonesia.

- Starting October 17, 2024, halal certification will become mandatory for numerous foods, ingredients, additives, and all processed food products in Indonesia.

- As the demand for halal-certified food products rises, there will be a parallel need for packaging that meets halal standards. This could lead to increased demand for plastic packaging that is certified or specifically designed to handle halal products.

- The organic food sector often emphasizes sustainability and environmental responsibility. This trend can drive the development and adoption of more eco-friendly plastic packaging solutions, such as biodegradable or recyclable plastics. Companies will likely invest in creating packaging that aligns with the organic market's values.

- According to the Organic Trade Association, in 2022, the consumption value of organic packaged food in Indonesia amounted to around USD 15.7 million. The value was forecast to increase to USD 19 million in 2025.

Indonesia Plastic Packaging Industry Overview

The market is semi-consolidated and driven by several key players. Amcor Group, Prima Jaya Eratama, PT ePac Flexibles Indonesia, PT Berlina Tbk, and PT Indo Tirta Abadi are pivotal in addressing the surging demand for packaging solutions. These companies are not only moving away from conventional plastic packaging but are also aligning with the growing consumer preference for sustainable plastic alternatives. To bolster their market presence, these firms are fine-tuning their strategies, broadening their product offerings, and actively seeking collaborations and acquisitions, with a pronounced focus on sustainability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging Methods

- 5.1.2 Increased Eco-friendly Packaging and Recycled Plastic

- 5.2 Market Challenges

- 5.2.1 High Price of Raw Material (Plastic Resin)

- 5.2.2 Government Regulations and Environmental Concerns

6 MARKET SEGMENTATION

- 6.1 Rigid Plastic Packaging

- 6.1.1 Material Type

- 6.1.1.1 Polyethylene (PE)

- 6.1.1.2 Polyethylene terephthalate (PET)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Polystyrene (PS) and Expanded polystyrene (EPS)

- 6.1.1.5 Polyvinyl chloride (PVC)

- 6.1.1.6 Other Material Types

- 6.1.2 Product Type

- 6.1.2.1 Bottles and Jars

- 6.1.2.2 Trays and containers

- 6.1.2.3 Other Product Types

- 6.1.1 Material Type

- 6.2 Flexible Plastic Packaging

- 6.2.1 Material Type

- 6.2.1.1 Polyethene (PE)

- 6.2.1.2 Bi-orientated Polypropylene (BOPP)

- 6.2.1.3 Cast polypropylene (CPP)

- 6.2.1.4 Polyvinyl Chloride (PVC)

- 6.2.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.2.1.6 Other Material Types

- 6.2.2 Product Type

- 6.2.2.1 Pouches

- 6.2.2.2 Bags

- 6.2.2.3 Films & Wraps

- 6.2.2.4 Other Product Types

- 6.2.1 Material Type

- 6.3 End-user Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Healthcare

- 6.3.4 Cosmetics and Personal Care

- 6.3.5 Other End-user Industry

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group

- 7.1.2 Prima Jaya Eratama

- 7.1.3 PT ePac Flexibles Indonesia

- 7.1.4 PT Berlina Tbk

- 7.1.5 PT Indo Tirta Abadi

- 7.1.6 Sonoco Products Company

- 7.1.7 PT Solusi Prima Packaging

- 7.1.8 PT Hasil Raya Industries

- 7.1.9 PT Indonesia Toppan Printing

8 INVESTMENT ANLAYSIS

9 FUTURE OF THE MARKET

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025 年軟塑膠包裝全球市場報告

2025 年軟塑膠包裝全球市場報告 聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032

聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032 軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程

軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程 一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 德國塑膠包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

德國塑膠包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)