|

市場調查報告書

商品編碼

1698558

智慧票務市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Smart Ticketing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

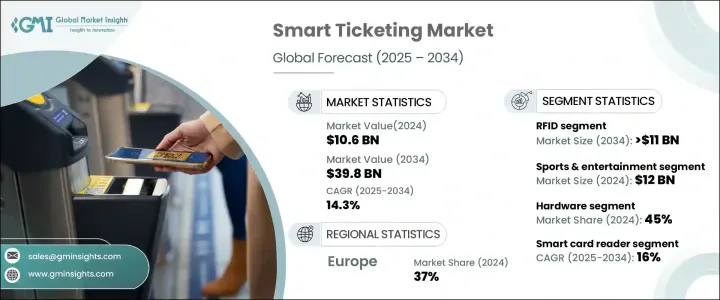

2024 年全球智慧票務市場價值為 106 億美元,預計 2025 年至 2034 年的複合年成長率為 14.3%。北美和歐洲等已開發地區採用非接觸式支付解決方案是推動市場擴張的關鍵因素。消費者現在更喜歡更快、更安全、更無縫的票務系統,增強了對智慧票務技術的信任。加密技術的廣泛採用進一步加強了支付安全性,而整合到智慧票務系統中的數位廣告則增強了用戶參與度。對政府和私人電子服務的日益依賴,加速了對智慧票務解決方案的需求。城市化也導致公共交通使用量的激增,需要先進的支付系統。新興經濟體的政府正在投資現代化公共交通,進一步刺激市場表現。

智慧票務解決方案依連線性分為條碼、RFID、蜂窩網路、Wi-Fi 和近場通訊。 RFID 領域佔了超過 30% 的市場佔有率,預計到 2034 年將超過 110 億美元。支援 RFID 的智慧卡系統和電子資訊亭等硬體組件越來越受歡迎,為交通和娛樂場所的出行提供了便捷的途徑。這些智慧卡可以充值虛擬資金,讓乘客和活動參與者輕鬆進行無現金交易。硬體和軟體解決方案的日益整合正在推動對感測器、微控制器和積體電路等基本組件的需求,這些組件在智慧票務基礎設施中發揮著至關重要的作用。此外,智慧卡業者提供的票價折扣也吸引了越來越多的客戶。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 106億美元 |

| 預測值 | 398億美元 |

| 複合年成長率 | 14.3% |

根據最終用途應用,智慧票務市場分為停車、體育和娛樂、交通和其他類別。體育和娛樂產業引領市場,2024 年創造 120 億美元的市場價值。體育場和音樂廳等娛樂場所擴大使用動態定價策略,這推動了對自動票務解決方案的需求。這些系統有助於簡化門票銷售、最佳化定價並確保活動管理順利進行。隨著線上機票預訂量的增加,安全問題正在透過提供端到端加密的創新區塊鏈支付平台得到解決。智慧體育場解決方案的採用也在加速,使活動組織者能夠透過數位工具加強票務驗證、移動入口和停車管理。

根據組成部分,市場分為硬體、軟體和服務。隨著對 RFID 讀取器和整合 IC 等攜帶式驗證設備的需求不斷成長,硬體部分將在 2024 年佔據 45% 的市場佔有率。由自助服務終端、平板電腦和支援 Wi-Fi 的裝置中的紅外線感測器提供支援的非接觸式票務解決方案在疫情後越來越受歡迎。微控制器提高了交易效率,進一步推動了硬體領域的成長。

在產品方面,市場包括請求追蹤器、票務驗證器、智慧卡讀卡機、行動售票終端、智慧售票亭和電子收費系統。預計到 2034 年,智慧卡讀卡機的複合年成長率將達到 16%,這得益於其在公共交通、門禁管制和醫療保健票務領域的廣泛應用。這些系統提高了營運效率並確保了交易安全,使其成為各行業必不可少的系統。

歐洲佔據主導地位,佔有37%的市場。德國在該地區處於領先地位,2024 年創造了 23 億美元的收入。政府支持的推廣數位票務解決方案的舉措正在鼓勵人們更多地使用公共交通,並加強智慧票務的採用。在人口密集的城市,智慧票務系統提供了可擴展的解決方案,可以有效管理客流,減少售票櫃檯擁擠並簡化交通運作。對數位交易的日益成長的偏好正在塑造城市交通的未來,使智慧票務成為現代交通系統的重要組成部分。

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 硬體供應商

- 軟體供應商

- 技術提供者

- 最終用途

- 利潤率分析

- 供應商格局

- 技術與創新格局

- 專利分析

- 監管格局

- 價格趨勢

- 衝擊力

- 成長動力

- 非接觸式支付解決方案的採用日益增多

- 對公共交通的依賴日益增加

- 提高交通系統的技術整合度

- 票務平台高度證券化

- 票務系統數位化

- 產業陷阱與挑戰

- 與舊平台的兼容性問題

- 開發成本高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 軟體

- 服務

第6章:市場估計與預測:依發行量,2021 - 2034 年

- 主要趨勢

- 智慧卡讀卡器

- 驗票機

- 售票行動終端

- 請求追蹤器

- 售票機/智慧售票亭

- 電子收費

第7章:市場估計與預測:依連結性,2021 - 2034 年

- 主要趨勢

- 射頻識別

- 條碼

- 近場通訊 (NFC)

- 蜂窩網路

- 無線上網

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 停車處

- 體育與娛樂

- 運輸

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Atos

- Confidex (Now Beontag)

- Chengdu Monkey Software

- Conduent

- CPI Card Group

- Cubic Corporation

- ETICKETS.HK

- Fujitsu

- Giesecke & Devrient

- HID Global

- Indra Systemas

- Infineon Technologies

- NXP Semiconductors

- Oberthur Technologies

- Scheidt & Bachman

- Siemens

- Telvent GIT

- Thales Group (formerly Gemalto)

- Vix Technology

- Xerox Corporation

The Global Smart Ticketing Market was valued at USD 10.6 billion in 2024 and is projected to grow at a CAGR of 14.3% from 2025 to 2034. The adoption of contactless payment solutions across developed regions like North America and Europe is a key factor driving market expansion. Consumers now prefer faster, secure, and seamless ticketing systems, enhancing trust in smart ticketing technologies. Increased adoption of encryption further strengthens payment security, while digital advertising integrated into smart ticketing systems enhances user engagement. The growing reliance on electronic services, both governmental and private, is accelerating the demand for intelligent ticketing solutions. Urbanization is also leading to a surge in public transport usage, necessitating advanced payment systems. Governments in emerging economies are investing in modernizing public transportation, further stimulating market performance.

Smart ticketing solutions are categorized based on connectivity into barcode, RFID, cellular networks, Wi-Fi, and near-field communications. The RFID segment held over 30% market share and is expected to exceed USD 11 billion by 2034. Hardware components such as smart card systems enabled with RFID and E-kiosks are gaining traction, offering easy access to transportation and entertainment venues. These smart cards can be reloaded with virtual funds, allowing passengers and event attendees to make cashless transactions effortlessly. The growing integration of hardware and software solutions is fueling demand for essential components like sensors, microcontrollers, and ICs, which play a crucial role in smart ticketing infrastructure. Additionally, fare discounts offered by smart card operators are attracting a larger customer base.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.6 Billion |

| Forecast Value | $39.8 Billion |

| CAGR | 14.3% |

Based on end-use applications, the smart ticketing market is segmented into parking, sports & entertainment, transportation, and other categories. The sports & entertainment sector led the market, generating USD 12 billion in 2024. The increasing use of dynamic pricing strategies by entertainment venues, including stadiums and concert halls, is driving demand for automated ticketing solutions. These systems help streamline ticket sales, optimize pricing, and ensure smooth event management. As online ticket bookings rise, security concerns are being addressed through innovative blockchain-based payment platforms that offer end-to-end encryption. The adoption of smart stadium solutions is also accelerating, enabling event organizers to enhance ticket validation, mobile entry, and parking management through digital tools.

By component, the market is divided into hardware, software, and services. The hardware segment accounted for 45% market share in 2024, with the growing demand for portable validation devices like RFID readers and integrated ICs. Touch-free ticketing solutions, powered by IR sensors in kiosks, tablets, and Wi-Fi-enabled devices, are gaining popularity post-pandemic. Microcontrollers improve transaction efficiency, further driving the hardware segment growth.

In terms of offerings, the market includes request trackers, ticket validators, smart card readers, mobile ticketing terminals, smart ticketing kiosks, and E-tolling systems. Smart card readers are projected to grow at a CAGR of 16% through 2034, driven by their widespread use in public transport, access control, and healthcare ticketing. These systems enhance operational efficiency and ensure secure transactions, making them essential in various industries.

Europe holds a dominant market position, with a 37% share. Germany led the region, generating USD 2.3 billion in 2024. Government-backed initiatives promoting digital ticketing solutions are encouraging greater public transport use and reinforcing smart ticketing adoption. In densely populated cities, smart ticketing systems offer a scalable solution to manage passenger flow efficiently, reducing ticket counter congestion and streamlining transit operations. The increasing preference for digital transactions is shaping the future of urban mobility, positioning smart ticketing as a critical component of modern transportation systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Hardware suppliers

- 3.1.1.2 Software providers

- 3.1.1.3 Technology providers

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Price trend

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing adoption of contactless payment solutions

- 3.6.1.2 Growing reliance on public transportation

- 3.6.1.3 Increasing technological integration in transit systems

- 3.6.1.4 High securitization of ticketing platforms

- 3.6.1.5 Digitization of ticketing systems

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Compatibility issues with legacy platforms

- 3.6.2.2 High development costs

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Offerings, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Smart card reader

- 6.3 Ticket validators

- 6.4 Ticketing mobile terminals

- 6.5 Request tracker

- 6.6 Ticketing machine / smart ticketing Kiosk

- 6.7 E-toll

Chapter 7 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 RFID

- 7.3 Barcode

- 7.4 Near-field Communication (NFC)

- 7.5 Cellular network

- 7.6 Wi-Fi

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Parking

- 8.3 Sports & Entertainment

- 8.4 Transportation

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Atos

- 10.2 Confidex (Now Beontag)

- 10.3 Chengdu Monkey Software

- 10.4 Conduent

- 10.5 CPI Card Group

- 10.6 Cubic Corporation

- 10.7 ETICKETS.HK

- 10.8 Fujitsu

- 10.9 Giesecke & Devrient

- 10.10 HID Global

- 10.11 Indra Systemas

- 10.12 Infineon Technologies

- 10.13 NXP Semiconductors

- 10.14 Oberthur Technologies

- 10.15 Scheidt & Bachman

- 10.16 Siemens

- 10.17 Telvent GIT

- 10.18 Thales Group (formerly Gemalto)

- 10.19 Vix Technology

- 10.20 Xerox Corporation

線上活動票務市場規模、佔有率及成長分析(按平台、活動類型和地區)-2025 年至 2032 年產業預測

線上活動票務市場規模、佔有率及成長分析(按平台、活動類型和地區)-2025 年至 2032 年產業預測 2025-2029 年全球智慧票務市場智慧票務市場規模、佔有率及成長分析(按組件、產品、應用、組織規模和地區)-2025 年至 2032 年產業預測

2025-2029 年全球智慧票務市場智慧票務市場規模、佔有率及成長分析(按組件、產品、應用、組織規模和地區)-2025 年至 2032 年產業預測 2025-2033 年按產品、組件、系統、應用程式和地區分類的智慧票務市場報告線上電影票務服務市場規模、佔有率和成長分析(按服務類型、付款方式、螢幕類型、類型、應用和地區)- 產業預測 2025-2032

2025-2033 年按產品、組件、系統、應用程式和地區分類的智慧票務市場報告線上電影票務服務市場規模、佔有率和成長分析(按服務類型、付款方式、螢幕類型、類型、應用和地區)- 產業預測 2025-2032 2031 年北美智慧票務市場預測 - 區域分析 - 按組件、支付系統和最終用戶

2031 年北美智慧票務市場預測 - 區域分析 - 按組件、支付系統和最終用戶 2031 年亞太地區智慧票務市場預測 - 區域分析 - 按組件、支付系統和最終用戶

2031 年亞太地區智慧票務市場預測 - 區域分析 - 按組件、支付系統和最終用戶 歐洲智慧票務市場預測至 2031 年 - 區域分析 - 按組件(硬體、軟體和服務)、支付系統(開放支付系統、智慧卡和 NFC)和最終用戶(交通、體育和娛樂、停車等)

歐洲智慧票務市場預測至 2031 年 - 區域分析 - 按組件(硬體、軟體和服務)、支付系統(開放支付系統、智慧卡和 NFC)和最終用戶(交通、體育和娛樂、停車等) 線上電影票務服務市場:預測(2025-2030)

線上電影票務服務市場:預測(2025-2030) 線上活動門票市場報告:至2030年的趨勢、預測和競爭分析

線上活動門票市場報告:至2030年的趨勢、預測和競爭分析