|

市場調查報告書

商品編碼

1627174

東南亞黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030)Southeast Asia Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

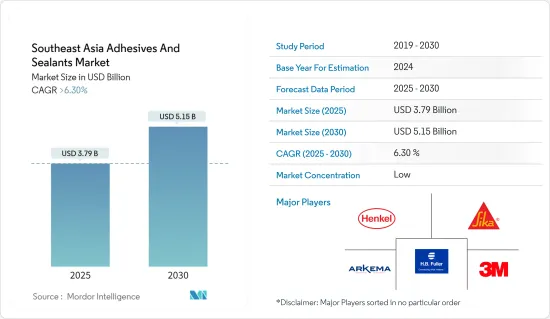

東南亞黏合劑和密封劑市場規模預計到2025年為37.9億美元,預計到2030年將達到51.5億美元,預測期內(2025-2030年)複合年成長率為6.3%。

由於 COVID-19,東南亞黏合劑和密封劑市場面臨挫折。全球封鎖和嚴格的政府監管導致生產基地大規模關閉。然而,市場於 2021 年復甦,預計未來幾年將顯著成長。

主要亮點

- 從短期來看,建築業不斷成長的需求和包裝行業不斷成長的採用是推動所研究市場需求的關鍵因素。

- 然而,黏合劑和密封劑嚴格的揮發性有機化合物排放法規預計將阻礙市場成長。

- 生物基黏合劑的創新和發展以及複合材料黏合的轉變預計將在所研究的市場中創造新的機會。

- 預計印尼將主導市場並在預測期內實現最高成長。

東南亞黏合劑和密封劑市場趨勢

建築業成長迅速

- 由於其獨特的性能和物理特性,黏合劑和密封劑在建築行業中發揮著至關重要的作用,使其成為市場的關鍵最終用戶部分。

- 黏合劑和密封劑的關鍵性能包括強內聚力、黏合力和彈性,以及高內聚力和柔韌性。它還具有高彈性模量,抗熱膨脹,並能承受紫外線、腐蝕、鹽水、雨水和其他風化條件等環境挑戰。

- 常見應用包括暖通空調系統、混凝土建築、接縫水泥、彈性地板材料、屋頂和固定窗框。

- 在東南亞,印尼、菲律賓、馬來西亞、越南和泰國等國家的建設活動不斷增加,增加了對黏合劑和密封劑的需求。

- 在政府的大力支持下,馬來西亞的建築業正迅速現代化和擴張。根據馬來西亞工業發展金融公司(MIDF)的數據,該產業已連續第六個季度實現成長。

- 2023 年最後一個季度,賽城資料中心開始建設,這是位於馬來西亞雪蘭莪州賽城的一座 17,000平方公尺的七層資料中心。賽城資料中心由 1,830 個機櫃組成,容量為 12MW。施工預計將於 2025 年第二季完成,從而增加所研究市場的需求。

- 據預算和管理部稱,2023年菲律賓政府將在基礎設施和資本支出上支出12,046億披索(約220億美元),與前一年同期比較增加19%。

- 根據建設局的資料,2023 年新加坡的建築合約預計價值在 270 億新元(約 206 億美元)至 320 億新元(約 244 億美元)之間。公共部門計劃預計將佔這一需求的 60% 左右,住宅和發展委員會 (HDB) 正在大力開展公共住宅建設。此外,隨著水處理廠和教育設施等計劃的激增,新加坡對黏合劑和密封劑的需求預計將增加。

- 政府舉措以及許多正在進行和計劃中的基礎設施計劃可能會影響預測期內東南亞對黏合劑和密封劑的需求。例如,在泰國普吉島,作為卡圖芭東高速公路計劃一部分的卡圖芭東隧道計劃將建造一條1.85公里的隧道。建設總成本為146.7億泰銖(約4.3億美元),預計2027年完工。

- 作為旅遊中心,泰國大力投資購物中心和豪華酒店。芭堤雅馬奎斯萬豪酒店擁有 900 多間客房,是一個備受矚目的計劃,計劃於 2024 年開業。這兩棟建築的開發項目還包括擁有 398 間客房的 JW 萬豪酒店和芭堤雅海灘水療度假村。萬豪計劃在 2027 年之前在曼谷和芭堤雅推出三個品牌下的四家新酒店,加入其在泰國現有 45 家酒店和度假村的投資組合。

- 根據越南統計局資料,2023年,越南建築業將為GDP貢獻超過640.72兆越南盾(約300億美元),為國家貢獻總額約1.2兆越南盾(約4億美元)佔GDP的6.27%。

- 鑑於這些動態,上述因素可能會影響未來幾年黏合劑和密封劑的需求軌跡。

印尼主導市場

- 印尼在黏合劑和密封劑消費方面領先東南亞。這一成長的主要促進因素包括建設活動的增加、電子產品生產的蓬勃發展以及鞋類、皮革和醫療領域需求的不斷成長。

- 在鞋類和皮革行業,黏合劑和密封劑對於將材料黏合在一起、確保耐用性並提高產品性能至關重要。隨著印尼鞋類和皮革工業的擴張,對黏合劑和密封劑的需求也不斷成長。

- 印尼統計局資料顯示,2023年皮革鞋類製造業GDP達約49.24兆印度盧比(約30億美元),比前一年成長2%。這一成長證實了印尼作為全球製造業強國的崛起。

- 在醫療領域,黏合劑和密封劑對於將材料黏合在一起、確保耐用性並增強醫療設備的功能至關重要。隨著醫療產業的成長,預計未來幾年對黏合劑和密封劑的需求將會增加。

- 過去一年,印尼透過重大國內和國際投資加強了衛生部門。 2023 年第 17 號衛生法廢除了強制性衛生支出,並引入基於績效的預算(PBBS)以鼓勵有針對性的支出。該法律還提供了六大支柱的醫療保健轉型大綱,強調了政府加強印尼醫療保健服務的承諾。

- 根據印尼衛生署預計,2023年印尼醫療設備出口額將達到約33.4億美元,與前一年同期比較成長22%,進一步拉動醫療產業成長,支持受訪者市場成長。

- 東南亞最大的建築市場印尼正在加大政府在基礎設施和都市化的支出,以滿足住宅和商業設施需求的激增,從而導致對黏合劑和密封劑的需求增加。

- 建築業對印尼的國內生產毛額至關重要。財政部將從2024年預算中向公共工程和住宅部撥款35兆印尼幣(約20億美元)資金,用於增加公務員的基礎設施和住宅。西爪哇茂物佔地 95 公頃的 Sequoia Hills Sentul住宅開發計劃將於 2023 年第四季開始施工,預計 2027 年完工。

- 印尼在 2024 年預算中累計40.6 兆印度盧比(27 億美元)用於開發新首都。政府相關人員報告說,總統府和幾棟住宅大樓正在迅速動工,預計 2024 年竣工。建築投資的激增將推動對黏合劑和密封劑的需求。

- 在汽車領域,黏合劑和密封劑對於黏合材料、確保耐用性和提高車輛性能至關重要。隨著汽車生產和銷售的擴大,黏合劑和密封劑的成長預計在預測期內上升。

- 根據OICA(國際汽車構造組織)的資料,2023年印尼汽車產量為139萬輛,低於2022年的147萬輛。然而,汽車銷量成長13%,2023年達到101萬輛。

- 經過強勁復甦後,印尼汽車市場不僅在2023年實現反彈,也超過了疫情前的數字。然而,根據 GAIKINDO 的數據,2024 年 1 月出現了挫折,汽車總體銷量從 2023 年的 94,087 輛下降了 26% 至 69,619 輛。乘用車下降20%至56,007輛,商用車下降43%至13,612輛。儘管如此,GAIKINDO 預計 2024 年汽車銷量將達到約 110 萬輛。

- 在電子領域,黏合劑和密封劑對於黏合材料、確保耐用性和提高設備性能至關重要。隨著電子產業的發展,對這些黏合劑和密封劑的需求也在成長。

- 根據印尼電子產品生產商協會(Gabel)的資料,電子產品的國內銷售通常每年成長約11%。 Gabel也預測電子產業將顯著成長,預計2024年將成長5%至10%。

- 鑑於各行業的這些趨勢,印尼對黏合劑和密封劑的需求預計在未來幾年將成長。

東南亞黏合劑和密封劑產業概況

東南亞的黏合劑和密封劑市場較為分散。主要參與企業(排名不分先後)包括 3M、Arkema、Sika AG、HB Fuller、Henkel AG & Co. KGaA。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 建築業需求不斷成長

- 包裝產業的採用率提高

- 其他司機

- 抑制因素

- 關於VOC排放的嚴格環境法規

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 黏合技術

- 水性的

- 丙烯酸纖維

- 乙烯醋酸乙烯酯(EVA)乳液

- 聚氨酯分散體和CR(氯丁橡膠)膠乳

- 聚醋酸乙烯酯(PVA)乳液

- 其他水性膠黏劑

- 溶劑型

- 苯乙烯-丁二烯橡膠(SBR)

- 苯乙烯-丁二烯橡膠(SBR)

- 聚丙烯酸酯 (PA)

- 其他溶劑型膠黏劑

- 反應性

- 環氧樹脂

- 改性壓克力

- 矽膠

- 聚氨酯

- 厭氧的

- 氰基丙烯酸酯

- 其他反應型黏合劑

- 熱熔膠

- 乙烯醋酸乙烯酯

- 苯乙烯嵌段共聚物

- 熱塑性聚氨酯

- 其他熱熔膠

- 其他

- 水性的

- 密封膠產品類型

- 矽膠

- 聚氨酯

- 丙烯酸纖維

- 聚醋酸乙烯酯

- 其他

- 最終用戶產業

- 建築/施工

- 紙/紙板包裝

- 運輸

- 木工/細木工

- 鞋類/皮革

- 醫療保健

- 電力/電子

- 其他

- 地區

- 印尼

- 馬來西亞

- 菲律賓

- 新加坡

- 泰國

- 越南

- 其他東南亞地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- ADB Sealant Co., Ltd

- Arkema Group

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- Dymax Corporation

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Jowat AG

- Mapei Inc.

- MUNZING Corporation

- Pidilite Industries Ltd.

- Sika AG

- Tesa SE(A Beiersdorf Company)

- Wacker Chemie AG

第7章 市場機會及未來趨勢

- 生物基膠黏劑的創新與發展

- 重點轉向粘合複合材料

- 其他機會

The Southeast Asia Adhesives And Sealants Market size is estimated at USD 3.79 billion in 2025, and is expected to reach USD 5.15 billion by 2030, at a CAGR of greater than 6.3% during the forecast period (2025-2030).

The Southeast Asia adhesives and sealants market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

- Over the short term, growing demand from the construction sector and increasing adoption in the packaging industry are the major factors driving the demand for the market studied.

- However, stringent VOC emissions regulations related to adhesives and sealants are expected to hinder the market's growth.

- Nevertheless, the innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials is expected to create new opportunities for the market studied.

- Indonesia is expected to dominate the market and witness the highest growth during the forecast period.

Southeast Asia Adhesives and Sealants Market Trends

Building and Construction Segment to Witness Fastest Growth

- Adhesives and sealants, due to their unique characteristics and physical properties, play a pivotal role in the building and construction industry, establishing it as the leading end-user segment in the market.

- Key properties of adhesives and sealants encompass strong cohesion, adhesion, and elasticity, coupled with high cohesive strength and flexibility. They also exhibit a high elastic modulus, resist thermal expansion, and withstand environmental challenges such as UV light, corrosion, saltwater, rain, and other weathering conditions.

- Common applications span across HVAC systems, concrete work, joint cementing, resilient flooring, roofing, and fixed window frames.

- In Southeast Asia, rising construction activities in nations like Indonesia, the Philippines, Malaysia, Vietnam, and Thailand are propelling the demand for adhesives and sealants.

- Malaysia's construction sector, buoyed by substantial government backing, is rapidly modernizing and expanding. As per Malaysian Industrial Development Finance Berhad (MIDF), the sector has seen six consecutive growth periods.

- In the last quarter of 2023, construction commenced on a 17,000 m2, seven-story data center called the Cyberjaya Data Centre in Cyberjaya, Selangor, Malaysia. The Cyberjaya Data Centre comprises 1,830 cabinets with a capacity of 12 MW. Construction is projected to be completed by the second quarter of 2025, thus increasing the demand for the market studied.

- According to the Department of Budget and Management, the Philippines government spent PHP 1204.6 billion (~USD 22 billion) on infrastructure and capital outlays in 2023, marking a 19% rise from the prior year, thus increasing the demand for the market studied.

- As per the data from the Building and Construction Authority, Singapore's construction contracts are projected to be valued between SGD 27 billion (~USD 20.6 billion) and SGD 32 billion (~USD 24.4 billion) in 2023. Public sector projects are anticipated to make up about 60% of this demand, driven by a robust pipeline of public housing initiatives from the Housing Development Board (HDB). Additionally, with a surge in projects like water treatment plants and educational facilities, the demand for adhesives and sealants in Singapore is set to rise.

- Government initiatives and numerous ongoing and planned infrastructure projects are set to influence the demand for adhesives and sealants in Southeast Asia during the forecast period. For instance, In Phuket, Thailand, the Kathu-Patong Tunnel Project, part of the Kathu-Patong Expressway Project, is set to construct a 1.85-kilometer tunnel. With an estimated cost of THB 14.67 billion (~USD 0.43 billion), completion is anticipated by 2027.

- Thailand, a major tourist hub, is seeing significant investments in malls, luxury hotels, and more. The Pattaya Marriott Marquis Hotel, boasting over 900 guest rooms, is the standout project, aiming for a 2024 launch. This dual-property development also features a 398-room JW Marriott and the Pattaya Beach Resort & Spa. By 2027, Marriott plans to introduce four new hotels across its three brands in Bangkok and Pattaya, adding to its existing portfolio of 45 hotels and resorts in Thailand, nine of which are in collaboration with Asset World Corporation.

- As per the data from General Statistics Office of Vietnam, in 2023, Vietnam's construction sector contributed over VND 640.72 trillion (~USD 0.03 trillion) to the GDP, representing 6.27% of the nation's total GDP, which was approximately VND 10.2 thousand trillion (~USD 0.0004 trillion).

- Given these dynamics, the aforementioned factors are poised to shape the demand trajectory for adhesives and sealants in the coming years.

Indonesia to Dominate the Market

- Indonesia leads Southeast Asia in the consumption of adhesives and sealants. Key drivers for this growth include rising construction activities, booming electronics production, and heightened demand in the footwear, leather, and healthcare sectors.

- In the footwear and leather industry, adhesives and sealants are essential for bonding materials, ensuring durability, and enhancing product performance. As Indonesia's footwear and leather sector expands, so does the demand for these adhesives and sealants.

- Data from Statistics Indonesia reveals that in 2023, the GDP from leather and footwear manufacturing reached approximately IDR 49.24 trillion (~USD 0.0030 trillion), marking a 2% increase from the previous year. This growth underscores Indonesia's emergence as a global manufacturing powerhouse.

- In the healthcare sector, adhesives and sealants are vital for bonding materials, ensuring durability, and enhancing the functionality of medical devices. With the healthcare sector's growth, the demand for adhesives and sealants is set to rise in the coming years.

- Over the past year, Indonesia has bolstered its healthcare sector through significant investments, both domestic and foreign. The 2023 Health Law (Law No.17 of 2023 on Health) eliminated mandatory health spending, introducing a performance-based budgeting system (PBBS) to promote targeted spending. This law also outlines a six-pillar healthcare transformation, highlighting the government's commitment to enhancing Indonesia's healthcare services.

- According to the Ministry of Health (Indonesia), in 2023, Indonesia's medical equipment exports reached approximately USD 3.34 billion, a 22% increase from the previous year, further fueling the healthcare sector's growth, therby supporting the growth of the market studied.

- As Southeast Asia's largest construction market, Indonesia is ramping up government spending on infrastructure and urbanization to meet the bosltering demand for residential and commercial properties, subsequently increasing the need for adhesives and sealants.

- The construction sector is vital to Indonesia's GDP. The Ministry of Finance has allocated an IDR 35 trillion (~USD 0.002 trillion) fund from the 2024 budget to the Public Works and Housing Ministry, aiming to boost infrastructure and housing for civil servants. In Q4 2023, construction began on the Sequoia Hills Sentul Residential Development project, a 95-hectare endeavor in Bogor, West Java, set for completion in 2027, aiming to elevate regional living standards.

- In its 2024 budget, Indonesia has set aside IDR 40.6 trillion (USD 2.7 billion) for its new capital city development. Government officials report rapid advancements, with the presidential office and several residential blocks on track for a 2024 completion. This surge in construction investment is poised to elevate the demand for adhesives and sealants.

- In the automotive sector, adhesives and sealants are crucial for bonding materials, ensuring durability, and enhancing vehicle performance. With the country's expanding vehicle production and sales, growth for adhesives and sealants is anticipated to rise during the forecast period.

- Data from the Organisation Internationale des Constructeurs d'Automobiles (OICA) indicates that Indonesia produced 1.39 million automobiles in 2023, down from 1.47 million in 2022. However, vehicle sales saw a 13% uptick, reaching 1.01 million units in 2023.

- After a strong recovery, Indonesia's vehicle market not only bounced back by 2023 but also exceeded pre-pandemic figures. Yet, January 2024 brought a setback, with GAIKINDO noting a 26% decline in overall vehicle sales, dropping to 69,619 units from 94,087 in 2023. Passenger vehicle sales dipped 20% to 56,007 units, while commercial vehicles saw a sharper 43% drop to 13,612 units. Despite this, GAIKINDO anticipates car sales will reach around 1.1 million units in 2024.

- In the electronics sector, adhesives and sealants are vital for bonding materials, ensuring durability, and enhancing device performance. As the electronics sector grows, so does the demand for these adhesives and sealants.

- Data from the Indonesian Electronics Producers Association (Gabel) indicates that domestic sales of electronic products typically see an annual increase of about 11%. Gabel also projects significant growth for the electronics industry, estimating a rise between 5% and 10% in 2024.

- Given these trends across various industries, the demand for adhesives and sealants in Indonesia is poised for growth in the coming years.

Southeast Asia Adhesives and Sealants Industry Overview

The Southeast Asia's adhesives and sealants market is fragmented in nature. The major players (not in any particular order) include 3M, Arkema, Sika AG, H.B. Fuller, and Henkel AG & Co. KGaA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Construction Sector

- 4.1.2 Increasing Adoption in Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesive Technology

- 5.1.1 Water Borne

- 5.1.1.1 Acrylic

- 5.1.1.2 Ethylene Vinyl Acetate (EVA) Emulsion

- 5.1.1.3 Polyurethane Dispersion and CR (Chloroprene Rubber) Latex

- 5.1.1.4 Polyvinyl Acetate (PVA) Emulsion

- 5.1.1.5 Other Water-borne Adhesives

- 5.1.2 Solvent-borne

- 5.1.2.1 Styrene-Butadiene Rubber (SBR)

- 5.1.2.2 Styrene-Butadiene Rubber (SBR)

- 5.1.2.3 Poly Acrylate (PA)

- 5.1.2.4 Other Solvent-borne Adhesives

- 5.1.3 Reactive

- 5.1.3.1 Epoxy

- 5.1.3.2 Modified Acrylic

- 5.1.3.3 Silicone

- 5.1.3.4 Polyurethane

- 5.1.3.5 Anaerobic

- 5.1.3.6 Cyanoacrylate

- 5.1.3.7 Other Reactive Adhesives

- 5.1.4 Hot Melt

- 5.1.4.1 Ethylene Vinyl Acetate

- 5.1.4.2 Styrenic Block Copolymers

- 5.1.4.3 Thermoplastic Polyurethane

- 5.1.4.4 Other Hot Melt Adhesives

- 5.1.5 Other Technologies

- 5.1.1 Water Borne

- 5.2 Sealant Product Type

- 5.2.1 Silicone

- 5.2.2 Polyurethane

- 5.2.3 Acrylic

- 5.2.4 Polyvinyl Acetate

- 5.2.5 Other Product Types

- 5.3 End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Paper, Board, and Packaging

- 5.3.3 Transportation

- 5.3.4 Woodworking and Joinery

- 5.3.5 Footwear and Leather

- 5.3.6 Healthcare

- 5.3.7 Electrical and Electronics

- 5.3.8 Other End-user Industries

- 5.4 Geography

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Philippines

- 5.4.4 Singapore

- 5.4.5 Thailand

- 5.4.6 Vietnam

- 5.4.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 ADB Sealant Co., Ltd

- 6.4.3 Arkema Group

- 6.4.4 Ashland

- 6.4.5 Avery Dennison Corporation

- 6.4.6 Beardow Adams

- 6.4.7 Dow

- 6.4.8 DuPont

- 6.4.9 Dymax Corporation

- 6.4.10 Franklin International

- 6.4.11 H.B. Fuller Company

- 6.4.12 Henkel AG & Co. KGaA

- 6.4.13 Huntsman International LLC

- 6.4.14 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.15 Jowat AG

- 6.4.16 Mapei Inc.

- 6.4.17 MUNZING Corporation

- 6.4.18 Pidilite Industries Ltd.

- 6.4.19 Sika AG

- 6.4.20 Tesa SE (A Beiersdorf Company)

- 6.4.21 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials

- 7.3 Other Opportunities

2025 年至 2033 年絕緣玻璃用黏合劑和密封劑市場報告(按樹脂類型、最終用戶和地區分類)

2025 年至 2033 年絕緣玻璃用黏合劑和密封劑市場報告(按樹脂類型、最終用戶和地區分類) 2025 年防水黏合劑和密封劑全球市場報告

2025 年防水黏合劑和密封劑全球市場報告 混合黏合劑和密封劑市場報告(按樹脂類型(MS 聚合物混合材料、環氧聚氨酯、環氧氰基丙烯酸酯等)、最終用途行業(建築、交通、電子等)和地區 2025-2033 年

混合黏合劑和密封劑市場報告(按樹脂類型(MS 聚合物混合材料、環氧聚氨酯、環氧氰基丙烯酸酯等)、最終用途行業(建築、交通、電子等)和地區 2025-2033 年 中東和非洲黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

中東和非洲黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 亞太地區黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太地區黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 北美黏合劑和密封劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

北美黏合劑和密封劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 南美洲的黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030)

南美洲的黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030) 歐洲黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 美國黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030)

美國黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030) 馬來西亞的黏合劑和密封劑:市場佔有率分析、行業趨勢、成長預測(2025-2030)

馬來西亞的黏合劑和密封劑:市場佔有率分析、行業趨勢、成長預測(2025-2030)