|

市場調查報告書

商品編碼

1640539

亞太地區黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Asia-Pacific Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

亞太地區黏合劑和密封劑市場規模預計在 2025 年為 320.8 億美元,預計到 2030 年將達到 429.2 億美元,預測期內(2025-2030 年)的複合年成長率將超過 6%。達到。

該地區受到了新冠肺炎疫情的不利影響。該地區的黏合劑和密封劑市場也面臨類似的情況。然而,目前它已達到疫情前的水平,預計市場將以顯著的速度成長。

預計在預測期內,全球包裝和建築行業的不斷擴張將推動對黏合劑和密封劑的需求。

然而,政府關於使用揮發性有機化合物的嚴格環境法規預計將阻礙市場擴張。

生物基黏合劑的創新和發展以及向複合材料黏合的轉變可能會為黏合劑和密封劑市場提供機會。

中國將成為該地區最大的黏合劑和密封劑市場,其消費由汽車、建築、電子和包裝等終端用戶產業推動。

亞太地區黏合劑和密封劑市場的趨勢

包裝領域佔據市場主導地位

- 紙包裝產品包括折疊紙盒、瓦楞紙箱、紙袋、液體紙板等。隨著有組織零售業的大幅成長,由於超級市場和現代購物中心的激增,對紙質包裝的需求預計會增加。

- 很大比例的工業產品都是經過包裝出售的,這要么是因為儲存和運輸的穩定性要求,要么是出於美觀的原因。當今使用的大多數包裝材料都是透過將不同的材料黏合在一起而製成的,需要使用黏合劑。

- 加速這一領域成長的一些關鍵因素是電子商務平台的擴張和大眾收入水準提高導致的消費增加。

- 中國是亞太地區包裝產業的主要貢獻者。中國在2021-2025年五年規劃中表示,將提高塑膠回收和焚燒能力,推廣「綠色」塑膠產品,並打擊包裝和農業中的塑膠濫用。新的五年計畫還呼籲鼓勵商店和宅配業者減少「不合理」的塑膠包裝,並計劃到 2025 年將都市區垃圾焚燒率從去年的 58 萬噸提高到每天 80 萬噸左右。預計此類發展將增加國內對可回收軟質塑膠包裝的需求。預計預測期內阿里巴巴等電子商務巨頭的崛起將推動包裝市場的發展。例如,在阿里巴巴為期10天的購物活動「雙11」期間,中國消費者收到了約19億件貨物。

- 在印度,塑膠包裝每年以 20-25% 的速度成長,目前產量為 680 萬噸,而紙包裝的價值為 760 萬噸。這些趨勢對包裝行業的黏合劑消費產生了積極影響。

- 2022 年 6 月,環境部下屬聯邦機構中央污染控制委員會 (CPCB) 宣布了一系列禁止某些一次性塑膠產品的措施。預計這些措施將促進該國對紙質包裝的需求。

- 此外,印度等國家對網路食品訂購的需求正在增加,從而推動了包裝食品盒在食品包裝市場的利用率。例如,2022 年 2 月,知名宅配公司 Zomato 報告稱,過去五年來,Zomato 上宅配餐廳的平均每月活躍用戶成長了 6 倍,而平均月交易客戶成長了 13次。

- 隨著網路科技和網路應用的興起,網路零售購物一直在高速成長,這主要支持了包裝產業的發展。

- 根據韓國英國商會介紹,韓國食品飲料產業以大賣場為主導,透過電商平台擴大銷售。預計到 2024 年,韓國餐飲市場規模將達到 761 億英鎊(899.8 億美元)。

- 此外,政府推行的永續包裝措施也要求採用紙包裝產品。例如,作為韓國2050年碳中和目標的一部分,韓國環境部宣布,從2022年6月10日起,連鎖咖啡館和速食店將要求對一次性杯子繳納300韓元(0.25美元)的押金。此規定適用於分店超過 100分店、門市超過 38,000 家的連鎖企業。

- 因此,由於黏合劑和密封劑在紙張、紙板和包裝行業的廣泛應用,以及由於包裝材料需求的增加(主要是由於市場成長),預計預測期內該地區該行業的黏合劑和密封劑消費量將進一步成長。

中國在亞太地區佔主導地位

- 亞太地區的黏合劑和密封劑消費以中國為主。建設活動的成長、包裝產業消費的增加以及電子產品生產支持國際市場的需求是推動該國黏合劑和密封劑市場消費的一些主要因素。

- 中國的成長主要得益於住宅和商業建築業的快速擴張以及國家經濟的擴張。中國正在推動並持續推動都市化進程,預計2030年都市化率將達70%。因此,中國等國家建築活動的活性化預計將刺激該地區黏合劑產業的發展。所有這些因素都傾向於增加全部區域黏合劑的需求。

- 根據中國國家統計局的數據,預計2022年建築業產值將達到31.2兆元(4.5兆美元),高於2021年的29.31兆元(4.2兆美元)。此外,根據住宅及城鄉建設部的預測,到2025年,中國建築業預計仍將佔GDP的6%。

- 中國乘用電動車(EV)市場持續大幅成長,預計 2022 年電動車銷量將年與前一年同期比較87%。比亞迪、五菱、奇瑞、長安、廣汽是佔據電動車市場主導的中國品牌,本土品牌佔81%。此外,2022年比亞迪的市場佔有率將年增11%與前一年同期比較,中國市場前10款電動車款中,將有6款是比亞迪品牌。

- 此外,中國政府預測2025年電動車普及率將達20%。預計這將導致汽車電池的生產和消費增加,從而增加對黏合劑和密封劑的需求。

- 此外,中國是世界上最大的電子製造基地之一,為韓國、新加坡和台灣等現有的上游製造商帶來了激烈的競爭。智慧型手機、OLED 電視和平板電腦等電子產品在市場消費性電子領域的需求成長最快。

- 在中國,由於進口自中國的電子產品的國家對電子產品的需求不斷增加,以及中階的可支配收入不斷提高,電子產品產量預計將實現成長。

- 因此,預計預測期內終端用戶行業的所有這些趨勢都將推動該國黏合劑和密封劑市場的成長。

亞太地區膠黏劑和密封劑產業概況

亞太地區的黏合劑和密封劑市場本質上是部分合併的。主要企業(不分先後順序)包括 3M、阿科瑪、西卡、富樂公司和漢高公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 東南亞國家包裝產業的成長

- 建築業需求不斷成長

- 其他促進因素

- 限制因素

- 有關 VOC排放的嚴格環境法規

- 原物料價格上漲

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 通過粘合樹脂

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 矽膠

- 氰基丙烯酸酯

- 乙烯-醋酸乙烯共聚物,

- 其他樹脂(聚酯、橡膠等)

- 按黏合技術

- 溶劑型

- 反應性

- 熱熔膠

- 紫外線固化膠合劑

- 水性

- 通過密封樹脂

- 矽膠

- 聚氨酯

- 丙烯酸纖維

- 環氧樹脂

- 其他樹脂(瀝青、聚硫化物紫外線固化等)

- 按最終用戶產業

- 航太

- 車

- 建築和施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他終端用戶產業(電子、消費品/DIY 等)

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- Dow

- DuPont

- Dymax Corporation

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Jowat AG

- Mapei Inc.

- Tesa SE(A Beiersdorf Company)

- Pidilite Industries Ltd.

- Sika AG

- Wacker Chemie AG

第7章 市場機會與未來趨勢

- 生物基膠黏劑的創新與發展

- 向複合黏合的轉變

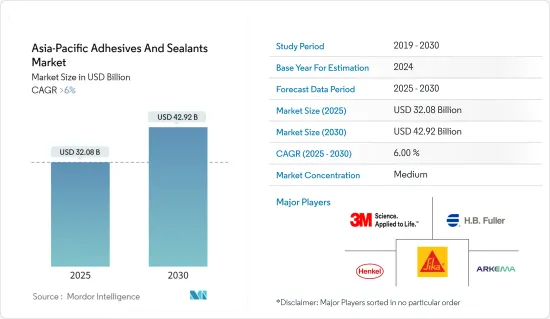

The Asia-Pacific Adhesives And Sealants Market size is estimated at USD 32.08 billion in 2025, and is expected to reach USD 42.92 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The region was negatively affected by the COVID-19 pandemic. The adhesives and sealants market in the region also faced a similar situation. However, the market has now reached pre-pandemic levels, and it is expected to grow at a significant pace.

Expanding packaging and building and construction industries around the globe are likely to drive demand for adhesives and sealants during the forecast period.

However, strict environmental regulations set by the government on the use of volatile organic compounds are anticipated to hamper market expansion.

The innovation and development of bio-based adhesives and shifting focus toward adhesive bonding for composite materials are likely to offer opportunities for the adhesives and sealants market.

China stands to be the largest market for adhesives and sealants in the region, where the consumption is driven by the end-user industries, such as automotive, construction, electronics, and packaging.

APAC Sealants & Adhesives Market Trends

Packaging Segment to Dominate the Market

- Packaging products in paper packaging comprises folding cartons, corrugated boxes, paper bags, and liquid paperboard. With the considerable increase in organized retail, the demand for paper packaging is anticipated to increase due to the rapid increase in supermarkets and modern shopping centers.

- An extremely high proportion of industrial products are sold in packages, either due to stability requirements for storage and transport or aesthetic reasons. Most packaging materials presently used are different materials laminated together, which require the use of adhesives.

- One of the critical factors that have been accelerating the growth of the segment includes a growing e-commerce platform and increasing consumption with the rise in income levels of the masses.

- China is a major contributing country in the APAC region for the packaging industry. In a 2021-2025 "five-year plan," China announced it would improve its plastic recycling and incineration capacities, promote "green" plastic products, and combat the misuse of plastic in packaging and agriculture. The new five-year plan would push merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons last year. Such developments are expected to increase the country's demand for recyclable flexible plastic packaging. Over the projection period, the rise of e-commerce giants like Alibaba is expected to fuel the packaging market. For example, Chinese shoppers received approximately 1.9 billion shipments during Alibaba's Double 11 shopping event, which lasted 10 days.

- In India, plastic packaging is growing at a significant rate of 20-25% annually and has reached 6.8 million tons, whereas paper packaging is valued at 7.6 million tons. These trends positively impacted the consumption of adhesives in the packaging sector.

- In June 2022, the Central Pollution Control Board (CPCB), a federal agency under the Ministry of the Environment, released a list of steps to outlaw specific single-use plastic products by June 2022. Such measures are anticipated to drive the demand for paper packaging in the country.

- Moreover, in a country such as India, the growing demand for online food ordering is increasing, pushing the usage of packaged food boxes in the food packaging market. For instance, in February 2022, Zomato, one of the prominent food delivery companies, said that the average monthly active food delivery restaurants have grown by 6x, and average monthly transacting customers have grown by 13x on Zomato over the past five years.

- Online retail shopping is increasing at a higher rate with the rising internet technologies and web applications, which have primarily supported the packaging industry's growth.

- According to the British Chamber of Commerce in Korea, South Korea's F&B business is defined by hypermarket dominance and expanding sales through e-commerce platforms. The F&B market in South Korea is expected to reach GBP 76.1 billion (USD 89.98 billion) by 2024.

- Furthermore, the government initiatives for sustainable packaging are mandating the adoption of paper packaging products. For instance, as part of South Korea's 2050 carbon neutrality goal, the South Korean Ministry of Environment has announced that disposable cups from chain cafes and fast-food restaurants will require a 300 KRW (USD 0.25) deposit starting on June 10, 2022. This regulation applies to chains with more than 100 branches and 38,000 stores.

- Therefore, with extensive application in the paper, board, and packaging industry and increased demand for packaging materials mainly due to the growing e-commerce industry, the consumption of adhesives and sealants in this segment is expected to increase further in the region over the forecast period.

China to Dominate in the Asia-Pacific Region

- China dominates the region's consumption of adhesives and sealants. Growing construction activities, increasing consumption in the packaging industry, and electronics production to support demand in the international market are some of the key factors driving the consumption of the adhesives and sealants market in the country.

- China's growth is fueled mainly by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- China's passenger electric vehicle (EV) market continues to grow at an impressive rate, with EV sales rising by 87% YoY in 2022. BYD, Wuling, Chery, Changan, and GAC are some of the top Chinese brands that dominate the EV market, with local brands commanding 81%. Additionally, in 2022, BYD increased its market share by over 11% Y-o-Y, with six out of the top 10 EV models in the Chinese market coming from the brand.

- Moreover, the Chinese government estimates a 20% penetration rate of electric vehicle production by 2025. Hence, this is anticipated to increase the production and consumption of vehicle batteries, thus increasing demand for adhesives and sealants in the market.

- Furthermore, China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand.

- In China, electronics production is projected to grow with the rising demand for electronic products in countries importing electronic products from China and the increase in the disposable income of the middle-class population.

- Hence, all such trends in the end-user industries are expected to drive the growth of the adhesives and sealants market in the country over the forecast period.

APAC Sealants & Adhesives Industry Overview

The Asia-Pacific adhesives and sealants market is partially consolidated in nature. The major players (not in any particular order) include 3M, Arkema, Sika AG, H.B. Fuller Company, and Henkel AG & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Packaging Industry in South-East Asia Countries

- 4.1.2 Growing Demand in Construction Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 High Fluctuations in Raw Material Pricing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Adhesives Resin

- 5.1.1 Polyurethane

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Silicone

- 5.1.5 Cyanoacrylate

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins (Polyester, Rubber, etc.)

- 5.2 Adhesives Technology

- 5.2.1 Solvent-borne

- 5.2.2 Reactive

- 5.2.3 Hot Melt

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Sealants Resin

- 5.3.1 Silicone

- 5.3.2 Polyurethane

- 5.3.3 Acrylic

- 5.3.4 Epoxy

- 5.3.5 Other Resins (Bituminous, Polysulfide UV-Curable, etc.)

- 5.4 End-User Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Woodworking And Joinery

- 5.4.8 Other End-user Industries (Electronics, Consumer/DIY, etc.)

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Indonesia

- 5.5.6 Malaysia

- 5.5.7 Thailand

- 5.5.8 Vietnam

- 5.5.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Dymax Corporation

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Huntsman International LLC

- 6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.14 Jowat AG

- 6.4.15 Mapei Inc.

- 6.4.16 Tesa SE (A Beiersdorf Company)

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

- 6.4.19 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Toward Adhesive Bonding for Composite Materials

2025 年至 2033 年絕緣玻璃用黏合劑和密封劑市場報告(按樹脂類型、最終用戶和地區分類)

2025 年至 2033 年絕緣玻璃用黏合劑和密封劑市場報告(按樹脂類型、最終用戶和地區分類) 2025 年防水黏合劑和密封劑全球市場報告

2025 年防水黏合劑和密封劑全球市場報告 混合黏合劑和密封劑市場報告(按樹脂類型(MS 聚合物混合材料、環氧聚氨酯、環氧氰基丙烯酸酯等)、最終用途行業(建築、交通、電子等)和地區 2025-2033 年

混合黏合劑和密封劑市場報告(按樹脂類型(MS 聚合物混合材料、環氧聚氨酯、環氧氰基丙烯酸酯等)、最終用途行業(建築、交通、電子等)和地區 2025-2033 年 中東和非洲黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

中東和非洲黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 北美黏合劑和密封劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

北美黏合劑和密封劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 南美洲的黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030)

南美洲的黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030) 東南亞黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030)

東南亞黏合劑和密封劑:市場佔有率分析、產業趨勢、成長預測(2025-2030) 歐洲黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲黏合劑和密封劑:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 美國黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030)

美國黏合劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030) 馬來西亞的黏合劑和密封劑:市場佔有率分析、行業趨勢、成長預測(2025-2030)

馬來西亞的黏合劑和密封劑:市場佔有率分析、行業趨勢、成長預測(2025-2030)