|

市場調查報告書

商品編碼

1636448

北美電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)North America Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

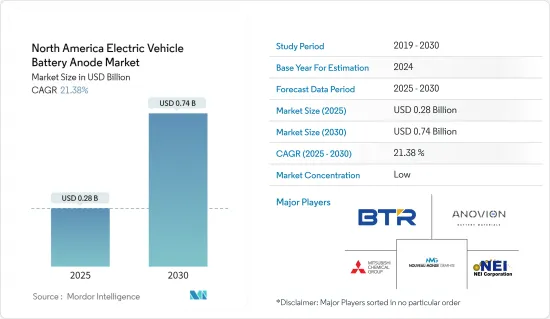

預計2025年北美電動車電池負極市場規模為2.8億美元,2030年預計將達7.4億美元,預測期內(2025-2030年)複合年成長率為21.38%。

主要亮點

- 電動車的普及、政府的支持措施以及鋰離子電池價格的下降將支持預測期內的市場成長。

- 相反,由於國內電池組件產量有限,市場可能面臨挑戰。

- 然而,負極材料和高效電解質的持續研究和進展為市場擴張提供了一個有希望的機會。

- 隨著汽車產業需求的增加,美國很可能透過擴大負極材料的使用來引領市場。

北美電動車電池負極市場趨勢

鋰離子電池類型預計將佔據較大佔有率

- 從歷史上看,鋰離子電池為從行動電話到個人電腦的家用電子電器提供動力。然而,它們的作用已經擴大,並已成為北美混合動力汽車和全電動汽車 (EV) 的首選動力源。這種變化主要是由於電動車的環境效益,它不排放二氧化碳和氮氧化物等溫室氣體。

- 在北美,鋰離子電池由於其良好的容量重量比而比其他類型的電池更受歡迎。鋰離子電池的卓越性能、長壽命和降低成本進一步推動了其採用。高能量密度和長循環壽命使鋰離子電池成為電動車製造商的最佳選擇。隨著北美國家擴大電動車產量,對適合鋰離子技術的先進製造設備的需求不斷增加,推動了對電池負極材料的需求。

- 鋰離子電池在北美市場佔據主導地位的關鍵因素是價格下降。過去十年,技術進步、規模經濟和複雜的製造流程顯著降低了鋰離子電池的成本。

- 2023年,鋰離子電池組價格將與前一年同期比較%至139美元/kWh。隨著電池價格下降,電動車將變得更加便宜,從而導致電動車的採用率和市場佔有率增加。需求的激增推動了包括負極在內的電池組件消費量的增加,並推動了提高電池性能的技術進步。

- 展望未來,由於該地區將重點增加陽極材料和陰極材料等鋰離子電池製造組件的產量,預計鋰離子電池陽極市場將在預測期內成長。

- 例如,2024年4月,澳洲Sicona Battery Technologies公司計劃在美國東南部建立矽碳負極材料初始生產設施。矽碳負極擴大用於電動車 (EV) 電池的生產。傳統的鋰離子電池通常使用石墨負極,但矽碳負極具有多種優勢,特別是在能量密度方面。該公司計劃在2030年將美國的產量擴大到每年26,500噸。

- 因此,由於電動車中鋰離子電池的使用量增加和價格下降,預計鋰離子電池陽極細分市場在預測期內將大幅成長。

預計美國將主導市場

- 近年來,在電動車普及和對尖端電池技術需求不斷增加的推動下,美國電動車電池負極市場迅速擴大。

- 隨著美國電動車銷量的飆升,電池製造商正在加大對國內生產的投資,從而增加了對電動車電池負極的需求。根據國際能源總署(IEA)的報告,2023年美國電動車銷量將達139萬輛,較2022年的99萬輛大幅成長。

- 在政府的大力支持下,電池製造商正在美國建造新的電動車(EV)工廠。這種擴張將顯著增加對電動車生產所用材料的需求,特別是電池和陽極。例如,2024年1月,美國能源局撥款1.31億美元用於推進電動車電池和充電系統研發的計劃。

- 展望未來,隨著電動車越來越普及,在國家電池技術研發努力的推動下,電池陽極市場可望成長。特別是,創新的矽碳複合陽極比傳統石墨陽極具有更高的能量密度,對於擴大電動車的續航里程至關重要。Panasonic和 LG Energy Solution 等領先公司以及 Sila Nanotechnologies 等新興企業正在投入資源進行研發,以提高負極的效能和穩定性。

- 此外,Nouveau Monde Graphite 在為加拿大魁北克快速成長的鋰離子電池和燃料電池市場開發碳中性電池陽極材料方面發揮先鋒作用。

- 鑑於電動車普及率和技術進步的軌跡,美國將在預測期內引領市場。

北美電動車電池負極產業概況

北美電動車電池負極市場處於減半狀態。市場主要企業包括(排名不分先後)BTR新材料集團、三菱化學集團公司、Anovion LLC、Nouveau Monde Graphite Inc和NEI Corporation。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 政府對電池製造的措施和投資

- 電池原物料成本下降

- 抑制因素

- 國內電池零件製造的限制

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子

- 鉛酸

- 其他

- 材料

- 鋰

- 石墨

- 矽

- 其他

- 地區

- 美國

- 加拿大

- 其他北美地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

貝特瑞新材料集團

- Anovion LLC

- Mitsubishi Chemical Group Corporation

- Nouveau Monde Graphite Inc

- NEI Corporation

- Targray Industries Inc.

- Nexeon Lid.

- LG Chem Ltd

- Tokai Carbon Co., Ltd.

- Nippon Carbon Co., Ltd.

- 市場排名分析

- 其他主要企業名單

第7章 市場機會及未來趨勢

- 增加其他電池化學物質的研究和開發

The North America Electric Vehicle Battery Anode Market size is estimated at USD 0.28 billion in 2025, and is expected to reach USD 0.74 billion by 2030, at a CAGR of 21.38% during the forecast period (2025-2030).

Key Highlights

- In the forecast period, the market is poised for growth, driven by the rising adoption of electric vehicles, supportive government initiatives, and declining prices of lithium-ion batteries.

- Conversely, the market may face challenges due to the limited domestic manufacturing of battery components.

- However, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market expansion.

- With increasing demand from the automotive sector, the United States is set to lead the market, bolstered by its growing application of anode materials.

North America Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Historically, lithium-ion batteries powered consumer electronics, from mobile phones to personal computers. However, their role has expanded, becoming the preferred power source for hybrid and fully electric vehicles (EVs) in North America. This shift is primarily attributed to the environmental benefits of EVs, which produce no CO2, nitrogen oxides, or other greenhouse gases.

- In North America, lithium-ion batteries are outpacing other battery types in popularity due to their favorable capacity-to-weight ratio. Their adoption is further fueled by superior performance, extended shelf life, and declining costs. With high energy density and long cycle life, lithium-ion batteries have become the go-to choice for EV manufacturers. As countries in North America ramp up EV production, there's a growing demand for advanced manufacturing equipment tailored to lithium-ion technology, thereby driving the demand for battery anode material.

- A significant driver of lithium-ion batteries' market dominance in North America is their decreasing prices. Over the last decade, technological advancements, economies of scale, and refined manufacturing processes have led to a significant drop in lithium-ion battery costs.

- In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, leading to increased adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, due to the region's heightened emphasis on boosting the production of lithium-ion battery manufacturing components, such as anode and cathode materials, the market for lithium-ion battery anodes is projected to grow during the forecast period.

- For instance, in April 2024, Sicona Battery Technologies, based in Australia, is set to establish its inaugural production facility for silicon-carbon anode materials in the Southeastern United States. Silicon-carbon anodes are increasingly being used in the manufacturing of electric vehicle (EV) batteries. Traditional lithium-ion batteries typically use graphite anodes, but silicon-carbon anodes offer several advantages, particularly in terms of energy density. By 2030, the company plans to expand its U.S. production to a total output of 26,500 tons annually.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

United States of America is Expected to Dominate the Market

- In recent years, the United States EV battery anode market has rapidly expanded, fueled by the rising adoption of electric vehicles and the demand for cutting-edge battery technologies.

- As electric vehicle sales surge in the United States, battery manufacturers are increasingly investing in domestic production, thereby driving up demand for EV battery anodes. The International Energy Agency reported that U.S. EV car sales reached 1.39 million units in 2023, a notable rise from 0.99 million in 2022.

- With strong government support, battery manufacturers are setting up new plants for electric vehicles (EVs) in the United States. This expansion is set to significantly elevate the demand for materials, especially battery anodes, used in EV production. For example, in January 2024, the U.S. Department of Energy allocated USD 131 million to projects aimed at advancing research and development in EV batteries and charging systems.

- Looking ahead, as EV adoption continues to rise, the battery anode market is poised for growth, bolstered by the nation's R&D efforts in battery technology. Notably, the innovative silicon-carbon composite anodes, which promise higher energy density than traditional graphite anodes, are pivotal for extending the EV range. Major players like Panasonic and LG Energy Solution, alongside newcomers like Sila Nanotechnologies, are pouring resources into R&D to boost anode performance and stability.

- Moreover, Nouveau Monde Graphite is pioneering the development of a carbon-neutral battery anode material in Quebec, Canada, targeting the burgeoning lithium-ion and fuel cell markets.

- Given the trajectory of EV adoption and technological advancements, the U.S. is poised to lead the market during the forecast period.

North America Electric Vehicle Battery Anode Industry Overview

The North America electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Mitsubishi Chemical Group Corporation, Anovion LLC, Nouveau Monde Graphite Inc, and NEI Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Limited Domestic Manufacturing of Battery Components

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1

BTR New Material Group Co., Ltd

- 6.3.2 Anovion LLC

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Nouveau Monde Graphite Inc

- 6.3.5 NEI Corporation

- 6.3.6 Targray Industries Inc.

- 6.3.7 Nexeon Lid.

- 6.3.8 LG Chem Ltd

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Nippon Carbon Co., Ltd.

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Battery Chemistries

全球矽陽極鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球矽陽極鋰離子電池市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 南美洲電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)德國電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)

南美洲電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)德國電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車電池負極:市場佔有率分析、產業趨勢、成長預測(2025-2030) 鋰離子電池陽極市場:按材料、電池類型和最終用途分類 - 全球預測 2025-2030

鋰離子電池陽極市場:按材料、電池類型和最終用途分類 - 全球預測 2025-2030 鋰離子電池用矽負極 - 專利形勢的分析(2024年)

鋰離子電池用矽負極 - 專利形勢的分析(2024年) 2024-2031年全球矽陽極鋰離子電池市場

2024-2031年全球矽陽極鋰離子電池市場 矽陽極鋰離子電池市場:成長、未來前景、競爭分析,2024-2032

矽陽極鋰離子電池市場:成長、未來前景、競爭分析,2024-2032 鋰離子電池負極市場、佔有率、規模、趨勢、產業分析報告:依材料、電池產品、最終用戶、地區、細分市場預測,2024-2032

鋰離子電池負極市場、佔有率、規模、趨勢、產業分析報告:依材料、電池產品、最終用戶、地區、細分市場預測,2024-2032 鋰離子電池負極的全球市場:按材料、電池產品、最終用途和地區分類 - 到 2028 年的預測

鋰離子電池負極的全球市場:按材料、電池產品、最終用途和地區分類 - 到 2028 年的預測