|

市場調查報告書

商品編碼

1637751

泰國太陽能:市場佔有率分析、產業趨勢、成長預測(2025-2030)Thailand Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

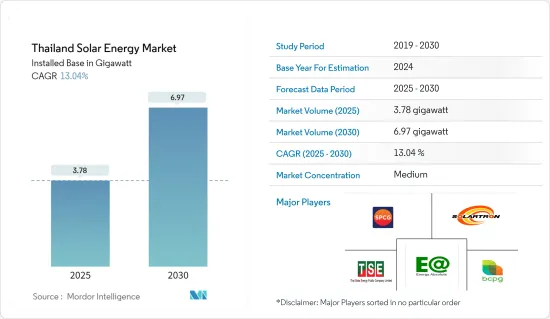

泰國太陽能市場規模(裝置量)預計將從2025年的3.78吉瓦擴大到2030年的6.97吉瓦,預測期間(2025-2030年)複合年成長率為13.04%。

主要亮點

- 從長遠來看,支持措施、電價上漲、技術進步、企業需求和能源安全目標等因素預計將在預測期內推動泰國太陽能市場的發展。

- 另一方面,電網限制、基礎設施差異和能源儲存挑戰嚴重阻礙了預測期內太陽能市場的成長。

- 泰國的目標是到 2037 年實現 30%的可再生能源,這為太陽能市場帶來了重大機會。此外,Energy Absolute 等公司對智慧電網技術、能源儲存系統整合和大規模電池生產的投資將進一步促進太陽能發電工程和電網穩定性。

泰國太陽能市場趨勢

光伏(PV)領域預計將主導市場

- 由於太陽能模組成本下降以及系統適用於發電和熱水等多種應用的多功能性,預計光伏(PV)領域將在預測期內佔據重要的市場佔有率。

- 根據國際可再生能源機構(IRENA)統計,2019年至2023年,泰國裝置容量從2,979MW增加到3,181MW,期間成長率為6.78%。此外,由於政府主導的太陽能發電量的增加和太陽能發電成本的下降,預計泰國的太陽能發電領域將顯著成長。

- 近年來,泰國太陽能發電工程大幅增加。這些舉措符合政府對再生能源的雄心勃勃的承諾,其目標是到 2037 年將再生能源在發電結構中的佔有率從 20% 增加到 50%。

- 例如,2024 年 10 月,TotalEnergies ENEOS 在泰國完成了一個 1.8 MWp浮體式太陽能發電系統,作為其與 S. Kijchai Enterprise 的第二個計劃。系統配備3,000多個模組,每年發電2,650兆瓦時,減少二氧化碳排放1,125噸。該計劃由 TotalEnergies ENEOS 根據長期購電協議資助和營運。

- 此外,2024年5月,海灣能源開發私人有限公司與泰國發電局(EGAT)簽署了為期25年的長期購電協議(PPA),將建設25座太陽能發電廠,總合為1,353兆瓦。計劃是能源監管委員會更大的可再生能源計劃的一部分,計劃於 2024 年至 2029 年在上網電價補貼的基礎上開始商業營運,提供具有成本效益的發電解決方案。

- 由於這些發展,預計太陽能發電領域在預測期內將在泰國佔據主導市場佔有率。

政府扶持措施帶動市場

- 泰國政府鼓勵全國採用可再生能源,力求在七年內將溫室氣體排放減少 20-25%。各國政府也透過提供各種獎勵和監管支持來支持太陽能市場。

- 泰國設定了 2037 年可再生能源佔電力結構 30% 的目標。到 2023 年,我們將安裝 12,547 兆瓦的可再生能源容量,高於 2015 年的 7,902 兆瓦。

- 2024年8月,泰國核准了公共部門節能計劃,旨在每年節省5.85億度。該計劃採用能源服務公司(ESCO)模式,透過長期合約安裝太陽能板和其他節能措施。

- 2024 年 7 月,工業部長 Pimpattla Wichaikul 訪問日本,推動泰國循環經濟,專注於永續發展目標 (SDG) 和碳中和。此次合作還包括太陽能電池板的回收,作為生物、循環和綠色 (BCG) 經濟模式的一部分,旨在加強永續資源管理。

- 2023年5月,泰國發電局(EGAT)為湄宏順府智慧電網先導計畫下的3MW太陽能發電廠和4MW電池儲能(BESS)計劃舉行了商業營運(COD)儀式。

- 此外,2023年3月,泰國國家能源政策委員會(NEPC)在上網電價補貼制度下引入了清潔電力的購買配額。上網電價補貼制度下的稅率為:地面太陽能發電每度2.1679泰銖,太陽能發電+蓄電池每度2.8331泰銖。對於這兩種類型的發電廠,上網電價補貼期均為 25 年。

- 因此,政府的措施和舉措預計將在預測期內推動泰國太陽能市場的發展。

泰國太陽能產業概況

泰國的太陽能市場是半集中的。市場主要企業(排名不分先後)包括 Energy Absolute Public Company Limited、SPCG Public Company Limited、Solartron PCL、Thai Solar Energy PLC 和 BCPG Public Company Limited。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年太陽能裝置容量及預測

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 泰國電費上漲與能源安全目標

- 政府對引進太陽能的支持措施

- 抑制因素

- 電網限制、基礎設施差異和能源儲存挑戰

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔-技術

- 光伏(PV)

- 聚光型太陽熱能發電(CSP)

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略及SWOT分析

- 公司簡介

- SPCG Public Company Limited

- BCPG Public Company Limited(BCPG)

- Thai Solar Energy PLC

- B. Grimm Power Public Company Limited

- Solaris Green Energy Co. Ltd.

- Energy Absolute PCL

- Solartron PLC

- Marubeni Corporation

- Black & Veatch Holding Company

- Jinkosolar Holding Co. Ltd.

- Trina Solar Co., Ltd.

- 其他知名公司名單

- 市場排名分析

第7章 市場機會及未來趨勢

- 智慧電網發展與電網擴建

The Thailand Solar Energy Market size in terms of installed base is expected to grow from 3.78 gigawatt in 2025 to 6.97 gigawatt by 2030, at a CAGR of 13.04% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as supportive policies, rising electricity prices, technological advancements, corporate demand, and energy security goals will likely drive Thailand's solar energy market during the forecast period.

- On the other hand, grid limitations, infrastructure gaps, and energy storage challenges significantly hinder the growth of the solar energy market during the forecast period.

- Nevertheless, Thailand's goal of achieving 30 percent renewable energy by 2037 presents significant opportunities for the solar energy market. Furthermore, The integration of smart grid technologies, energy storage systems, and Investments by companies like Energy Absolute in large-scale battery production further support solar projects and grid stability.

Thailand Solar Energy Market Trends

Solar Photovoltaic (PV) Segment Expected to Dominate the Market

- The solar PV segment is likely to hold the major market share during the forecast period, owing to the declining costs of solar modules and the versatility of these systems for various applications, like electricity generation and water heating.

- According to the International Renewable Energy Agency (IRENA), From 2019 to 2023, Thailand's Solar Photovoltaic (PV) Installed Capacity increased from 2979 MW to 3181 MW, with the growth rate over this period being 6.78 percent. Moreover, the solar PV segment is expected to witness massive growth with the increasing solar PV encouraged by government initiatives and falling solar PV costs in Thailand.

- In recent years, Thailand has seen a significant uptick in solar energy projects. These initiatives align with the government's ambitious commitment to renewables, which targets a 50 percent share in the power generation mix by 2037, up from an earlier goal of 20 percent.

- For instance, in October 2024, TotalEnergies ENEOS completed a 1.8 MWp floating solar PV system in Thailand, their second project with S. Kijchai Enterprise. The system, with over 3,000 modules, generates 2,650 MWh annually, reducing CO2 emissions by 1,125 tons, equivalent to planting 16,800 trees. This project is funded and operated by TotalEnergies ENEOS under a long-term PPA.

- Additionally, in May 2024, Gulf Energy Development Private Limited finalized 25-year-long power purchase agreements (PPAs) with the Electricity Generating Authority of Thailand (EGAT) to construct 25 solar PV farms, totaling 1,353 MW. These projects, part of a larger renewables scheme by the Energy Regulatory Commission, will receive feed-in tariffs and are expected to start commercial operations between 2024 and 2029, offering a cost-effective power solution.

- Owing to such developments, the solar PV segment is expected to have a dominant market share in Thailand during the forecast period.

Supportive Government Policies to Drive the Market

- The Thai government is encouraging renewable energy installations across the country to reduce greenhouse gas emissions by 20-25% in seven years. The government has also supported the solar power market by providing various incentives and regulatory support.

- Thailand has set a target for renewables to account for 30 percent of the power mix by 2037. In 2023, the country installed 12,547 MW of renewable energy capacity, which was higher than the 7,902 MW installed in 2015.

- In August 2024, Thailand approved an energy-saving scheme targeting public sector agencies, aiming to save 585 million kWh annually. The program will use the energy service company (ESCO) model to install solar panels and other energy-saving measures through long-term contracts.

- In July 2024, Industry Minister Pimphattra Wichaikul visited Japan to promote a circular economy in Thailand, focusing on sustainable development goals (SDGs) and carbon neutrality. The collaboration includes recycling solar panels as part of the Bio, Circular, and Green (BCG) economy model, aiming to enhance sustainable resource management.

- In May 2023, the Electricity Generating Authority of Thailand (EGAT), under the Smart Grid Pilot Project in Mae Hong Son Province, held a Commercial Operation Date (COD) ceremony for the 3 MW Solar Power Plant and 4 MW Battery Energy Storage System (BESS) Project.

- Moreover, in March 2023, Thailand's National Energy Policy Council (NEPC) introduced quotas for purchasing clean electricity via the Feed-in-Tariff Scheme, which will be implemented in two phases. The feed-in tariff rates are 2.1679 THB per unit for ground-mounted solar and 2.8331 THB per unit for solar + storage. Both types of power plants will have a 25-year term for the feed-in tariff.

- Therefore, supportive government policies and initiatives are expected to drive the Thailand solar energy market in the forecast period.

Thailand Solar Energy Industry Overview

The Thailand solar energy market is semi-concentrated. Some of the major companies in the market (in no particular order) include Energy Absolute Public Company Limited, SPCG Public Company Limited, Solartron PCL, Thai Solar Energy PLC, BCPG Public Company Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Energy Installed Capacity and Forecast, until 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Electricity Prices and Energy Security Goals in Thailand

- 4.5.1.2 Supportive Government Policies to Adopt Solar Energy

- 4.5.2 Restraints

- 4.5.2.1 Grid Limitations, Infrastructure Gaps, and Energy Storage Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION - TECHNOLOGY

- 5.1 Solar Photovoltaic (PV)

- 5.2 Concentrated Solar Power (CSP)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 SPCG Public Company Limited

- 6.3.2 BCPG Public Company Limited (BCPG)

- 6.3.3 Thai Solar Energy PLC

- 6.3.4 B. Grimm Power Public Company Limited

- 6.3.5 Solaris Green Energy Co. Ltd.

- 6.3.6 Energy Absolute PCL

- 6.3.7 Solartron PLC

- 6.3.8 Marubeni Corporation

- 6.3.9 Black & Veatch Holding Company

- 6.3.10 Jinkosolar Holding Co. Ltd.

- 6.3.11 Trina Solar Co., Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Smart Grid Development and Grid Expansion

印尼太陽能:市場佔有率分析、產業趨勢、成長預測(2025-2030)

印尼太陽能:市場佔有率分析、產業趨勢、成長預測(2025-2030) 印度太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 東南亞太陽能 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

東南亞太陽能 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 美國太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

美國太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 越南太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

越南太陽能 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030) 全球太陽能光電板市場 - 2024-2031

全球太陽能光電板市場 - 2024-2031 太陽能市場規模、佔有率、成長分析、按技術、按光學模組、按應用、按最終用途、按地區 - 按行業預測,2024-2031 年

太陽能市場規模、佔有率、成長分析、按技術、按光學模組、按應用、按最終用途、按地區 - 按行業預測,2024-2031 年 太陽能的全球市場:各技術,各用途,各地區,機會,預測,2018年~2032年

太陽能的全球市場:各技術,各用途,各地區,機會,預測,2018年~2032年 南歐洲的太陽能光伏發電的展望 2024年

南歐洲的太陽能光伏發電的展望 2024年 2025-2033 年日本太陽能市場規模、佔有率、趨勢和預測(按部署、應用和地區分類)

2025-2033 年日本太陽能市場規模、佔有率、趨勢和預測(按部署、應用和地區分類)