|

市場調查報告書

商品編碼

1640647

紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

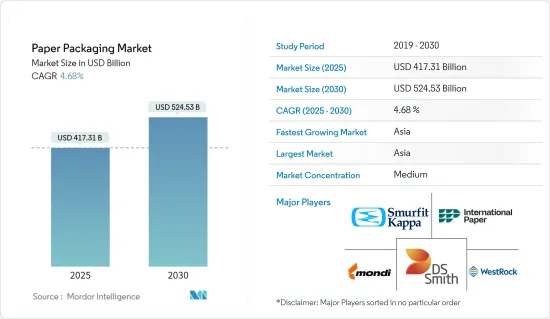

預計 2025 年紙包裝市場規模為 4,173.1 億美元,到 2030 年將達到 5,245.3 億美元,預測期內(2025-2030 年)的複合年成長率為 4.68%。

紙質包裝是一種多功能且經濟有效的保護、保存和運輸各種產品的方法。此外,它們還可以進行客製化,以滿足您的客戶和產品的特定需求。重量輕、生物分解性、可回收等特性是紙包裝的優點,使其成為不可或缺的組成部分。

關鍵亮點

- 全球消費者越來越意識到包裝對環境的危害,並將購買習慣轉向更環保的選擇。消費者、政府和媒體正在向製造商施壓,要求他們製造的產品、包裝和生產流程更加環保。此外,人們願意為這種環保包裝支付更多金額。由於這些趨勢,紙包裝行業預計會成長。

- 電子商務銷售額的不斷成長和對折疊式紙盒包裝的需求不斷增加正在推動市場的發展。然而,高性能替代品的出現可能會抑制市場的成長。紙板包裝是最受歡迎的環保包裝選擇之一。與體積較大的包裝解決方案相比,這種包裝形式佔用空間小,且可以生產多種尺寸,適用於幾乎所有最終用戶領域。

- 此外,消費者正在支持循環經濟模式並選擇更永續包裝和運輸的產品。透過使用紙板,品牌製造商旨在減少碳足跡和環境污染。電子商務為品牌透過包裝實現差異化創造了新的機會。它提供了保護整個供應鏈中的產品所需的基本實力,並使製造商能夠整合增強消費者體驗的增值功能。

- 此外,紙板包裝廣泛應用於零售和電子商務,其中亞馬遜等公司處於領先地位,擁有超過 5,000 萬用戶。隨著網際網路和智慧型手機的普及和都市化的快速發展,中國和印度等經濟體的電子商務市場預計將擴大。據IBEF稱,到2026年終,印度電子商務市場規模預計將達到2,000億美元,高於2017年的385億美元。

- 紙包裝市場面臨的挑戰是需要用紙來包裝重型材料,因此該行業需要與聚合物和金屬包裝行業保持平衡。此外,森林砍伐導致紙張生產過程中釋放戴奧辛,造成環境問題。這些因素可能會阻礙紙包裝市場的發展。

紙包裝市場趨勢

食品和飲料行業預計將佔據主要市場佔有率

- 紙是食品包裝最廣泛使用的材料之一。紙張是一種環保的包裝材料,是食品包裝的理想選擇。它主要用於直接包裝貨物,以便於運輸或儲存的初級包裝。紙和紙板也用於製作微波爆米花袋、烘焙紙和速食容器。預計紙包裝市場將受到消費者對包裝食品環境問題意識不斷增強的推動。

- 此外,紙張是一種隨時可用且廉價的資源。它廣泛應用於食品和飲料領域。這些材料可以回收利用,製造用於包裝應用的模製物品和其他與飲料接觸的物品,例如杯子、袋子和液體包裝。

- 此外,國際食品和飲料公司正在響應消費者的需求,目標是使所有包裝可回收或生物分解。例如,百加得宣布計劃透過發明一種新型紙質飲料瓶,在 2030 年消除塑膠,加入全球反對一次性塑膠的運動。對循環經濟理念的承諾有可能為造紙業帶來更大的進步。

- 市場各個參與企業都在不斷創新各自的產品,以建立全球框架。 2023 年 5 月,Smurfit Kappa 完成了一項投資計劃,以 4,000 萬歐元(4,388.6 萬美元)大幅擴建其位於 Pruszkw 的包裝工廠。此次擴建預計將使 Smurfit Kappa 成為波蘭最大的包裝廠之一,同時也是歐洲技術最先進、最現代化的包裝廠之一。

- 消費者的生活方式越來越忙碌,因此他們不斷尋求更容易拿起、處理、食用和攜帶的食物。各大品牌正努力透過使食品包裝便攜化來滿足這項需求。包裝製造商選擇使用紙張來包裝食品,因為這種包裝非常輕且易於運輸。此外,近年來食品包裝變得更加環保。大公司非常熱衷於尋找環保解決方案,他們正在放棄使用一次性塑膠,轉而使用生物分解性、可回收甚至可重複使用的包裝。

- 食品業的成長推動了對折疊紙盒、瓦楞紙箱和液體紙板箱的需求,而這種成長是由對已調理食品、冷凍食品和包裝食品的需求不斷成長所推動的。例如,根據美國人口普查局的數據,2023年美國食品和飲料零售商的年銷售額將達到約9,850億美元,高於2019年的7,744億美元。因此,食品和飲料銷量的增加將影響紙包裝市場的成長。

亞太地區可望佔據主要市場佔有率

- 預計亞太地區將在所研究的市場中實現顯著成長。由於該地區生產設施數量的增加、消費者意識的增強以及直通包裝行業的發展,市場正在不斷擴大。由於中國和印度等開發中國家對紙漿和紙張的需求不斷增加,該地區預計將迅速擴張。

- 在中國,運輸包裝市場隨著消費的成長,帶動了對紙包裝的需求。城市人口的增加、電子商務行業的發展、紙漿價格的下降以及人們對環保包裝意識的增強,預計將推動該地區紙包裝市場的發展。

- 據印度造紙工業協會 (IPMA) 稱,到 2026-27 年,印度的紙張消費量預計將以每年 6-7% 的速度成長,達到 3000 萬噸。預計這一成長主要得益於對教育和識字能力的重視程度提高以及有組織零售業的成長。

- 此外,中國終端用戶產業的紙張消費量正在成長,影響了瓦楞紙板等紙製品的生產。根據中國國家統計局的資料,2024年1月和2月,加工紙和紙板的產量隨著需求的增加而增加。中國累計紙及紙板產量約 2,242 萬噸,高於 2023 年 8 月的 1,225 萬噸。

- 日本雀巢公司正在為一系列品牌和產品探索新的包裝選擇。而且由於公司每天銷售約400萬件產品,它也積極進行材料研究,以進一步減少對環境的影響。此外,政府限制塑膠廢棄物的多項措施也影響了市場成長。因此,消費者意識的不斷增強以及食品飲料以及該地區其他領域的成長正在推動市場成長。

紙包裝產業概況

紙包裝市場由多家參與企業細分,包括國際紙業、Mondi、Smurfit Kappa 和 WestRock 公司。為了保持市場佔有率,各家公司正在不斷創新並建立策略聯盟。公司不斷創新和重新設計包裝,以提供更好的性能、提高適銷性和增強永續性。

- 2024 年 2 月,Mondi Group 將透過其創新的紙本 Eco Wicket Bag 擴大其生產範圍,以滿足對永續家庭和個人護理 (HPC) 包裝日益成長的需求,特別是對一次性尿布和女性用衛生用品的需求。透過擴大其位於匈牙利蘇扎達 (Suzáda) 工廠的生態門袋生產,Mondi 將進一步利用集團從自身紙張生產到塗層和加工的一體化價值鏈。

- 2024年1月,WestRock宣布計劃在威斯康辛州Pleasant Prairie建造新的瓦楞包裝工廠,以滿足客戶日益成長的需求。預計該項投資將提高該公司在五大湖地區的生產能力並增強其成本狀況。預計建設成本約1.4億美元。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 工業供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 阻隔性塗層紙板產品的開發

- 提高消費者對紙包裝的認知

- 市場限制

- 森林砍伐對紙包裝的影響

- 營運成本增加

第6章 世界再生紙產量統計

- 廢紙產量

- 廢紙進口額及進口量

- 廢紙出口額及數量

- 主要國家廢紙產量

第7章 紙板進出口場景

- 箱板紙出口:金額和數量(百萬美元,百萬噸)

- 箱板紙進口:金額和數量(百萬美元,百萬噸)

第 8 章市場細分

- 按年級

- 紙板

- 固體漂白硫酸鹽 (SBS)

- 未漂白固態硫酸鹽 (SUS)

- 折疊式箱板 (FBB)

- 塗佈再生紙板 (CRB)

- 無塗佈再生紙板 (URB)

- 其他

- 箱板紙

- 白色牛皮紙

- 其他牛皮卡紙

- 白色頂部測試襯墊

- 其他測試襯墊

- 半化學凹槽

- 回收瓦楞紙

- 紙板

- 按產品

- 折疊式紙盒

- 瓦楞紙箱

- 其他

- 按最終用戶產業

- 食物

- 飲料

- 醫療

- 個人護理

- 家居用品

- 電器

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 亞洲

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 北美洲

第9章 競爭格局

- 公司簡介

- International Paper Company

- Mondi Group

- Smurfit Kappa Group

- DS Smith PLC

- Eastern Pak Limited

- WestRock Company

- Packaging Corporation of America

- Cascades Inc.

- Nippon Paper Industries Ltd

- Sonoco Products Company

第10章 投資分析

第 11 章 市場的未來

The Paper Packaging Market size is estimated at USD 417.31 billion in 2025, and is expected to reach USD 524.53 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

Paper packaging is a versatile and cost-efficient method to protect, preserve, and transport a wide range of products. In addition, it can be customized to meet the customers' or product-specific needs. Attributes like lightweight, biodegradability, and recyclability are the advantages of paper packaging, making it an essential component.

Key Highlights

- Consumers globally are becoming more conscious of the environmental hazards of packaging and are moving their purchasing habits to more environment-friendly options. Consumers, the government, and the media are pressuring manufacturers to make their products, packaging, and processes more environmentally friendly. Also, individuals are willing to pay more for these types of conscious packaging. The paper packaging industry is anticipated to grow due to these trends.

- The expansion of e-commerce sales and the rising demand for folded carton packaging drive the market. However, the availability of high-performance substitutes will likely restrain the market's growth. Paperboard packaging is one of the most popular eco-friendly packaging options. Compared to bulkier packaging solutions, this packaging format can be created in various sizes with a small footprint, making it suitable for use in almost all end-user sectors.

- Moreover, consumers support the circular economy model, choosing products packaged and shipped more sustainably. Brand manufacturers aim to reduce their carbon footprint and environmental pollution by using cartonboards. E-commerce has created additional opportunities for brand manufacturers to differentiate themselves through packaging. Manufacturers can provide the essential strength to protect their products throughout the supply chain and integrate value-added features that improve the consumer experience.

- Furthermore, retail and e-commerce rely extensively on paperboard-based packaging, with companies such as Amazon setting the pace with more than 50 million subscribers. In economies such as China and India, the e-commerce market is expected to expand because of rising internet and smartphone penetration and rapid urbanization. According to IBEF, the Indian e-commerce market is anticipated to reach USD 200 billion by the end of 2026, from USD 38.5 billion in 2017.

- The challenge faced by the paper packaging market is the need for paper to package heavy materials, resulting in the industry needing to be more balanced by the polymers and metal packaging industries. Furthermore, deforestation causes the release of dioxins during paper production, causing environmental concerns. Such factors might hinder the paper packaging market.

Paper Packaging Market Trends

The Food and Beverage Segments are Expected to Hold Significant Market Share

- Paper is among the widely used materials for food packaging. Paper is an environment-friendly packaging material, making it an ideal option for food packaging. It is mainly used to package goods directly for transporting and storing primary packages. Paper and paperboard are also used to make microwave popcorn bags, baking paper, and fast-food containers. The market for paper packaging is anticipated to be propelled by high consumer awareness of the environmental concerns of packaged food.

- In addition, paper is one of the readily available, inexpensive resources. It is used extensively in the food and beverage sector. These materials can be recycled to create molded products for packaging applications and other beverage-containing contact items like cups, pouches, and liquid cartons.

- Moreover, international food and beverage businesses have set objectives to make all packaging recyclable or biodegradable in response to consumer demand. For instance, Bacardi stated its intention to eliminate plastic by 2030 by inventing new paper-based beverage bottles, joining the global push against single-use plastics. This dedication to circular economy concepts could result in more significant advancements in the paper industry.

- Various players in the market are constantly innovating products to bolster their foothold globally. In May 2023, Smurfit Kappa completed its investment project, which led to a significant expansion of its packaging plant in Pruszkw with EUR 40 million (USD 43.886 million). This expansion was expected to make Smurfit Kappa one of the largest in Poland and one of Europe's most technologically advanced and modern packaging plants.

- Consumers lead on-the-go lifestyles, and as a result, they continuously seek simpler foods to pick up, handle, eat, or carry. Brands are working harder to make food packaging portable to address this need. Packaging manufacturers depend on paper packaging for food products because these types of packaging are exceptionally lightweight and easy to carry. Moreover, food packaging has become more environmentally friendly in recent years. Big firms abandoned single-use plastics in favor of biodegradable, recyclable, or reusable packaging due to their desire for eco-friendly solutions.

- The growth of the food industry, which, in turn, is driving demand for folding cartons, corrugated boxes, and liquid paperboard boxes, is propelled by the increased need for ready-to-eat, frozen, and packaged goods. For instance, according to the US Census Bureau, in 2023, annual sales of retail food and beverage stores in the United States amounted to ~USD 985 billion, rising from USD 774.4 billion in 2019. Thus, increasing sales of food and beverages impact the growth of the paper packaging market.

Asia-Pacific is Expected to Hold Significant Market Share

- Asia-Pacific is anticipated to record significant growth in the market studied. The market is expanding due to the rising number of production facilities, rising consumerism, and the transit packaging industry in the region. The region is expected to expand quickly due to the increasing need for paper pulp in developing nations like China and India.

- In China, the transportation packaging market is growing along with consumption, fueling the demand for paper packaging. The growing urban population, evolving e-commerce industry, dropping pulp prices, and improving population awareness about environmentally friendly packaging are expected to propel the paper packaging market in the region.

- As per the Indian Paper Manufacturers Association (IPMA), paper consumption in India is expected to witness 6 to 7% annual growth and reach 30 million tonnes by FY 2026-27. This growth is expected to be mainly driven by the growing emphasis on education and literacy, coupled with the increase in organized retail business.

- Furthermore, the growing paper consumption in China throughout the end-user industries is also influencing the production of paper-based products like cardboard. According to data from the National Bureau of Statistics of China, the production of processed paper and cardboard increased simultaneously with their growing demand in January and February 2024. China's cumulative processed paper and cardboard production volume was approximately 22.42 million metric tons, which increased from 12.25 million metric tons in August 2023.

- Nestle, a Japanese company, is looking into new packaging options for various brands and goods. It is also aggressively researching materials to lessen its environmental impact further, as it sells approximately 4 million products daily. Furthermore, several government measures to limit plastic waste influence the market's growth. As a result, increasing consumer awareness and the growth of food, beverage, and other sectors in the region are pushing market's growth.

Paper Packaging Industry Overview

The paper packaging market is fragmented with several players like International Paper, Mondi, Smurfit Kappa, WestRock Company, and more. The companies are innovating and entering into strategic partnerships to retain their market share. Companies constantly innovate with technology and redesign their packaging to get better performance, improve marketability, and enhance sustainability.

- In February 2024, Mondi Group expanded the production of its innovative range of paper-based EcoWicketBags as part of the rising need for sustainable home and personal care (HPC) packaging, specifically for diapers and feminine hygiene products. By expanding the production of EcoWicketBags at its Szada (Hungary) plant, Mondi further leverages the Group's integrated value chain, from in-house paper production to coating and converting.

- In January 2024, WestRock announced plans to construct a new corrugated box plant in Pleasant Prairie, Wisconsin, to fulfill customers' growing needs. This investment is expected to position the company to increase production capabilities and enhance its cost profile in Great Lakes. The construction is slated to cost approximately USD 140 million.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Development of Barrier-coated Paperboard Products

- 5.1.2 Growing Consumer Awareness on Paper Packaging

- 5.2 Market Restraints

- 5.2.1 Effects of Deforestation on Paper Packaging

- 5.2.2 Increasing Operational Costs

6 GLOBAL RECOVERED PAPER PRODUCTION STATISTICS

- 6.1 Recovered Paper, Production Quantity

- 6.2 Recovered Paper, Import Value, and Import Quantity

- 6.3 Recovered Paper, Export Value, and Export Quantity

- 6.4 Recovered Paper Production, by Leading Countries

7 CARTONBOARD EXIM SCENARIO

- 7.1 Cartonboard Exports by Value & Volume (USD million, million tonnes)

- 7.2 Cartonboard Imports by Value & Volume (USD million, million tonnes)

8 MARKET SEGMENTATION

- 8.1 By Grade

- 8.1.1 Carton Board

- 8.1.1.1 Solid Bleached Sulphate (SBS)

- 8.1.1.2 Solid Unbleached Sulphate (SUS)

- 8.1.1.3 Folding Boxboard (FBB)

- 8.1.1.4 Coated Recycled Board (CRB)

- 8.1.1.5 Uncoated Recycled Board (URB)

- 8.1.1.6 Othder Graes

- 8.1.2 Containerboard

- 8.1.2.1 White-top Kraftliner

- 8.1.2.2 Other Kraftliners

- 8.1.2.3 White top Testliner

- 8.1.2.4 Other Testliners

- 8.1.2.5 Semi Chemical Fluting

- 8.1.2.6 Recycled Fluting

- 8.1.1 Carton Board

- 8.2 By Product

- 8.2.1 Folding Cartons

- 8.2.2 Corrugated Boxes

- 8.2.3 Other Types

- 8.3 By End User Industry

- 8.3.1 Food

- 8.3.2 Beverage

- 8.3.3 Healthcare

- 8.3.4 Personal Care

- 8.3.5 Household Care

- 8.3.6 Electrical Products

- 8.3.7 Other End User Industries

- 8.4 By Geography

- 8.4.1 North America

- 8.4.1.1 United States

- 8.4.1.2 Canada

- 8.4.2 Europe

- 8.4.2.1 Germany

- 8.4.2.2 United Kingdom

- 8.4.2.3 Italy

- 8.4.2.4 France

- 8.4.3 Asia

- 8.4.3.1 China

- 8.4.3.2 Japan

- 8.4.3.3 India

- 8.4.3.4 Australia and New Zealand

- 8.4.4 Latin America

- 8.4.4.1 Brazil

- 8.4.4.2 Mexico

- 8.4.5 Middle East and Africa

- 8.4.5.1 United Arab Emirates

- 8.4.5.2 Saudi Arabia

- 8.4.5.3 South Africa

- 8.4.1 North America

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 International Paper Company

- 9.1.2 Mondi Group

- 9.1.3 Smurfit Kappa Group

- 9.1.4 DS Smith PLC

- 9.1.5 Eastern Pak Limited

- 9.1.6 WestRock Company

- 9.1.7 Packaging Corporation of America

- 9.1.8 Cascades Inc.

- 9.1.9 Nippon Paper Industries Ltd

- 9.1.10 Sonoco Products Company

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

2025-2033 年按產品類型、等級、包裝水平、最終用途行業和地區分類的紙包裝市場報告

2025-2033 年按產品類型、等級、包裝水平、最終用途行業和地區分類的紙包裝市場報告 中東和非洲的紙包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲的紙包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太紙包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

亞太紙包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 北美紙包裝:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)

北美紙包裝:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030) 印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

印尼紙包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 拉丁美洲紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

拉丁美洲紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 日本紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

日本紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 歐洲紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 法國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

法國紙包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 義大利紙包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

義大利紙包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)