|

市場調查報告書

商品編碼

1683131

非洲作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Africa Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

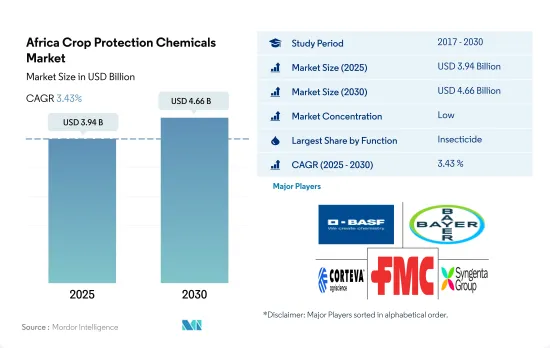

預計 2025 年非洲作物保護化學品市場規模為 39.4 億美元,到 2030 年將達到 46.6 億美元,預測期內(2025-2030 年)的複合年成長率為 3.43%。

農藥主導非洲作物保護化學品市場

- 農業是非洲的主要產業之一。該行業滿足了不斷成長的人口的糧食安全需求,並促進了該地區的經濟成長。該地區多樣的氣候條件有利於種植小麥、玉米、水稻、大豆、向日葵、豆類、菸草、咖啡、可可和茶等多種作物。

- 殺蟲劑在非洲作物保護化學品市場佔據主導地位,2022 年佔 41.7% 的佔有率。根據國際農業和生物科學中心的數據,非洲國家因昆蟲造成的作物損失估計佔每年預期作物產量的 49.0%。但由於氣候變化,蟲害預計會增加,農作物損失可能會更加嚴重。莖蟲、食葉毛蟲、豆葉潛蠅、蚜蟲、薊馬、葉蟬、粉蝨和介殼蟲是造成該地區經濟產量損失的主要害蟲。

- 除草劑是非洲使用第二多的作物保護劑,2022 年的市場佔有率為 30.7%。該地區的雜草侵擾每年平均造成 25-100% 的作物損失。同時,該地區正在實施集約化農業實踐以滿足不斷成長的人口的食物需求,這促進了各種雜草的傳播。過去一段時間,除草劑消費量顯著成長,2017 年至 2022 年期間使用量增加了 8,264 噸。

- 人口增加、可耕地面積減少和糧食安全的提高是推動該地區市場發展的因素,預計預測期內複合年成長率為 3.6%。

由於用於保護作物免受害蟲和雜草侵害的農藥消費量增加,市場正在成長

- 在非洲,對農藥的需求日益增加,以保護作物免受害蟲、疾病和雜草的侵害。該地區的農民嚴重依賴這些化學物質,因為病蟲害的侵襲會對作物造成巨大的損害和損失。

- 秋季蟲害可能導致1,600萬噸玉米短缺,價值近50億美元。國際農業和生物科學中心稱,如果不加以控制,這種玉米蛾每年可能對非洲12個主要玉米生產國造成830萬至2060萬噸的損失。

- 在非洲,2,300萬公頃土地上種植木薯、甘薯、馬鈴薯和山藥等根莖類作物。 5 億至 10 億非洲人食用木薯,但木薯易受病蟲害侵害。木薯花葉病毒和木薯褐條病是影響此作物最重要的疾病。東非和中非每年的經濟損失估計在 19 億美元至 27 億美元之間。

- 該國最重要的作物是玉米、稻米、小麥和高粱。其中,玉米是種植最廣泛的穀物。玉米極易受到二化螟(玉米螟科:玉米蟲)等害蟲的侵害,每年可造成 15% 至 100% 的嚴重產量損失。事實上,東非農民報告稱,僅二化螟造成生產損失就高達 4.5 億美元。這些因素正在推動農藥的消費,預計作物保護化學品市場在預測期內的複合年成長率將達到 3.6%。

非洲作物保護化學品市場的趨勢

採用病蟲害綜合治理策略和其他替代方案(如輪作)顯著減少了每公頃農藥的消費量

- 過去一段時間,非洲每公頃土地的農藥消費量明顯下降。 2017年農藥消費量為每公頃1175公克。但隨後的努力已成功將這一水準降低了每公頃 96 克,降至目前的每公頃 1,079 克。農藥使用量的大幅減少是多種因素的結果,包括實施優先考慮永續和生態友善方法的改良農業實踐。農民擴大採用綜合病蟲害管理、輪作和生物病蟲害防治等創新技術,以盡量減少每公頃土地使用的化學農藥量。

- 除草劑是該地區使用的主要農業化學產品,但近年來,每公頃除草劑消費量大幅下降,到 2022 年將與 2017 年相比下降至 34 克。除草劑消費量的大幅減少歸功於綜合雜草管理 (IWM) 方法的成功。在這種方法下,農民採用了各種創新策略,包括多樣化種植系統、機械除草、輪作和使用覆蓋作物。這些生態友善技術減少了對除草劑的依賴,促進了永續農業,改善了土壤健康並有助於保護生物多樣性。

- 透過採用 IPM 策略、種植抗病作物、替代性病蟲害控制手段以及提高對農藥負面影響的認知,到 2022 年,農民將比 2017 年減少每公頃殺菌劑使用量 38 克,減少殺蟲劑使用量 23 克。

需求增加和供應有限將導致活性成分價格大幅波動

- Cypermethrin是該地區用於控制水稻、棉花、大豆和蔬菜等作物害蟲的主要殺蟲劑。由於需求量大,2022 年Cypermethrin的價格與 2017 年相比每公噸上漲了 3,186.2 美元。這一上漲是由於當地產量有限,導致嚴重依賴進口來滿足需求。

- Atrazine是南非和奈及利亞等玉米生產國使用的主要除草劑,這些國家 88% 的玉米種植面積都使用阿特拉津來除草。Atrazine的用途廣泛,涉及多種陸地糧食作物和非作物、森林、住宅草坪、高爾夫球場、休閒區和牧場,並且是農場廣泛使用的除草劑。由於Atrazine在各類作物中的應用不斷擴大,其價格與前一年同期比較穩步上漲,2022 年與 2017 年相比每噸成長了 3,292.7 美元。

- Glyphosate是該地區第二常用的除草劑,並且由於其價格低廉而被廣泛接受。許多農民選擇Glyphosate作為主要的除草解決方案。 2022年,有效成分Glyphosate的價格為每噸1,143.2美元。

- 該地區農藥活性成分的價格在過去一段時間內大幅上漲,每公噸上漲了 1,580.9 美元。價格高企主要原因是該地區生產能力有限。過去五年來,非洲農藥進口量大幅增加,對進口產品的依賴加劇,導致該地區農藥價格上漲。

非洲作物保護化學品產業概況

非洲作物保護化學品市場細分化,前五大公司佔24.91%。該市場的主要企業包括BASF公司、拜耳公司、科迪華農業科技公司、富美實公司和先正達集團

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 有效成分價格分析

- 法律規範

- 南非

- 價值鏈與通路分析

第 5 章。市場細分,包括市場規模(美元和數量)、2030 年預測和成長前景分析

- 功能

- 殺菌劑

- 除草劑

- 殺蟲劑

- 滅螺劑

- 殺線蟲劑

- 執行模式

- 化學噴塗

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 南非

- 非洲其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 51595

The Africa Crop Protection Chemicals Market size is estimated at 3.94 billion USD in 2025, and is expected to reach 4.66 billion USD by 2030, growing at a CAGR of 3.43% during the forecast period (2025-2030).

Insecticides dominate the African crop protection chemicals market

- Agriculture is one of the major sectors in Africa. This sector fulfills the growing population's food security needs and helps the region to grow economically. The region's diverse climate conditions are favorable to the various crops, including wheat, maize, rice, soybeans, sunflower, beans, tobacco, coffee, cocoa, and tea.

- Insecticides dominated the African crop protection chemicals market, accounting for a share of 41.7% in 2022. Crop losses in African countries due to insects are estimated at 49.0% of the expected total crop yield each year, according to the Centre for Agriculture and Biosciences International. However, some crop losses may be even worse, and the effects of the changing climate are expected to increase the damage done by insects. Stem borers, leaf-eating caterpillars, bean flies, aphids, thrips, leafhoppers, whiteflies, and beetles are major pests that cause economic yield losses in the region.

- Herbicides are the second most used crop protection chemicals in Africa, accounting for a market share of 30.7% in 2022. On average, the region is losing up to 25-100% crop losses to weed infestations every year. At the same time, the region is implementing intensive agricultural practices to meet the food needs of a growing population, which favors the infestation of various weed species. During the historical period, the consumption of herbicides witnessed significant growth, and the usage increased by 8,264 metric tons between 2017 and 2022.

- Growing population, a decrease in arable land, and a rise in food security are some driving factors of the market in the region, and the market is anticipated to witness a CAGR of 3.6% during the forecast period.

The market is growing due to the rising consumption of pesticides to protect crops from pests and weeds

- The demand for pesticides in Africa is increasing to protect crops from pests, diseases, and weeds. Farmers in the region depend heavily on these chemicals as pest and disease infestations can result in substantial crop damage and loss.

- The fall armyworm infestation can lead to a shortage of 16 million metric tons of maize worth almost USD 5 billion. According to the Centre for Agriculture and Biosciences International, if this moth is not properly controlled, it has the potential to cause annual losses of 8.3 to 20.6 million tons in 12 of Africa's major maize-producing nations.

- Africa cultivates root and tuber crops such as cassava, sweet potato, potato, and yam on 23 million hectares of land. Cassava is consumed by 500 million to 1 billion Africans, but it is susceptible to insect pests and disease. The cassava mosaic virus and cassava brown streak disease are the most significant diseases affecting the crop. The annual economic losses in eastern Africa and central Africa are estimated to be between USD 1.90-2.70 billion.

- Maize, rice, wheat, and sorghum are the most important food crops grown in the country. Among these, maize is the most widely grown cereal crop. It is highly susceptible to pests, like Chilo partellus Swinhoe (Crambidae), which can cause significant yield losses ranging from 15% to 100% annually. In fact, farmers in eastern Africa have reported production losses of up to USD 450 million due to Chilo partellus alone. These factors are expected to drive the consumption of pesticides, and the crop protection chemicals market is expected to register a CAGR of 3.6% during the forecast period.

Africa Crop Protection Chemicals Market Trends

Adoption of IPM strategies and other alternative methods like crop rotations significantly reduces pesticide consumption per hectare

- During the historical period, there has been a remarkable decline in pesticide consumption per hectare within Africa. In 2017, the pesticide consumption rate stood at 1,175 g per ha. However, subsequent efforts have successfully reduced it by 96 g per ha, resulting in a current rate of 1,079 g per ha. This significant reduction in pesticide usage was due to a combination of various factors, which include the implementation of improved agricultural practices that prioritize sustainable and eco-friendly methods. Farmers have increasingly adopted innovative techniques such as integrated pest management, crop rotation, and biological pest control, which have minimized the need for chemical pesticide usage per hectare.

- Herbicides are majorly utilized pesticide products in the region, but in recent years, the herbicide consumption per hectare is significantly reduced by 34 g in 2022, as compared to 2017. This substantial decrease in herbicide consumption was due to the successful implementation of integrated weed management (IWM) practices. Under this approach, farmers have adopted a range of innovative strategies such as diversified cropping systems, mechanical weed control, crop rotation, and the use of cover crops. These environment-friendly techniques have contributed to reducing herbicide reliance and also promoted sustainable agriculture, enhancing soil health and conserving biodiversity.

- Farmers adopt IPM strategies, disease-resistant crops, and alternatives to control pests and diseases, raising awareness of pesticide's negative effects, thus reducing fungicide and insecticide use per hectare by 38 and 23 g per ha in 2022, compared to 2017.

Increasing demand and limited availability majorly fluctuate the active ingredient prices

- Cypermethrin is the predominant insecticide utilized in the region to control pests affecting crops such as rice, cotton, soybeans, and vegetables. Due to its high demand, the price of Cypermethrin rose by USD 3,186.2 per metric ton in 2022 compared to 2017. This increase was due to its limited production within the region, leading to a significant dependence on imports to meet the demand.

- Atrazine stands as the primary herbicide utilized in maize-producing countries like South Africa and Nigeria, with 88% of the maize area employed for weed control. Its usage extends to various terrestrial food crops, non-food crops, forests, residential turf, golf courses, recreational areas, and rangelands, making it a widely adopted weed control measure on farms. Due to its expanding application across various crops, the price of Atrazine has been steadily increasing Y-o-Y, with a growth recorded at USD 3,292.7 per metric ton in 2022 compared to 2017.

- Glyphosate is widely embraced as the second most used herbicide in the region, primarily due to its affordability. Many farmers opt for glyphosate as their primary weed control solution. In 2022, glyphosate's active ingredient was priced at USD 1,143.2 per metric ton.

- During the historical period, prices of pesticide-active ingredients in the region experienced a substantial increase, amounting to an increase of USD 1,580.9 per metric ton. This surge may be mainly attributed to the region's limited production capacity. Over the past five years, there has been a notable rise in pesticide imports into Africa, leading to heightened dependence on imported products and consequent price escalation in the region.

Africa Crop Protection Chemicals Industry Overview

The Africa Crop Protection Chemicals Market is fragmented, with the top five companies occupying 24.91%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

- 5.4 Country

- 5.4.1 South Africa

- 5.4.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國作物保護化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國作物保護化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 亞太地區作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 南美作物保護化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

南美作物保護化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 法國作物保護化學品市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

法國作物保護化學品市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 越南作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

越南作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025 年至 2033 年,作物保護化學品市場規模、佔有率、趨勢及預測(按產品類型、產地、作物類型、形式、應用方式和地區分類)

2025 年至 2033 年,作物保護化學品市場規模、佔有率、趨勢及預測(按產品類型、產地、作物類型、形式、應用方式和地區分類) 2025 年作物保護化學品全球市場報告

2025 年作物保護化學品全球市場報告 作物保護化學品的全球市場(2018年~2034年)

作物保護化學品的全球市場(2018年~2034年) 作物保護化學品市場 - 成長、未來展望、競爭分析,2025-2033 年

作物保護化學品市場 - 成長、未來展望、競爭分析,2025-2033 年 作物保護化學品市場規模、佔有率、成長分析、按產品、按應用、按來源、按地區 - 產業預測,2024-2031年

作物保護化學品市場規模、佔有率、成長分析、按產品、按應用、按來源、按地區 - 產業預測,2024-2031年

▼