|

市場調查報告書

商品編碼

1683979

亞太除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)Asia Pacific Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

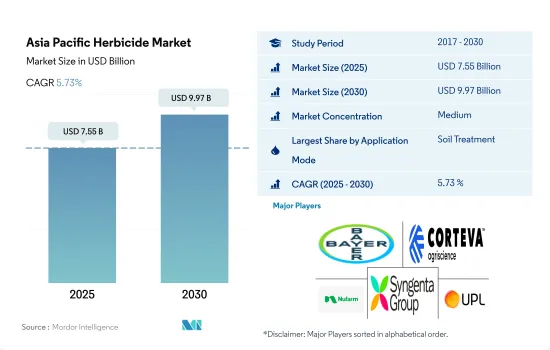

亞太除草劑市場規模預計在 2025 年為 75.5 億美元,預計到 2030 年將達到 99.7 億美元,預測期內(2025-2030 年)的複合年成長率為 5.73%。

雜草侵染和隨之而來的農作物產量下降正在推動市場

- 亞太地區作物種類繁多,既有水稻、小麥、玉米、大豆等主糧作物,也有棉花、甘蔗、水果、作物等經濟作物,這些作物都面臨多種雜草的威脅。 2022年,土壤治療方法佔亞太除草劑市場的最大佔有率,為46.8%,市場規模達30億美元。土壤處理包括將除草劑直接施用於土壤,是一種有效的除草方法。此方法可在種植前或作物出苗後使用,針對土壤中存在的雜草種子、幼苗或已成熟的雜草。

- 2022 年,葉面噴布除草劑佔 32.6% 的市場佔有率,價值 21 億美元。這種方法對於闊葉雜草、莎草、禾本科植物甚至水生雜草都非常有效。將除草劑直接施用於這些雜草的葉子上,可以達到最大程度的吸收和控制。葉面噴布的靈活性使得農民能夠在雜草活躍生長階段針對性地除草,以獲得最佳效果。

- 2022 年,化學噴灑佔除草劑施用方式的 18.9%,價值 12 億美元。這種成長是由於微灌溉系統的普及以及除草劑在農田中均勻施用和分佈的便利。

- 燻蒸可以提供有效的、有針對性的雜草控制,特別是在其他方法效果較差的封閉迴路境中。它可以到達難以控制的雜草的種子、根系和繁殖體。

- 由於每種技術的優勢和獨特性,預計預測期內每種技術的市場都會成長。

全部區域水稻等主糧作物的除草劑使用量正在增加

- 亞太地區除草劑市場在過去一段時間內穩步成長,預計到 2022 年該地區將佔據全球除草劑市場的大部分佔有率。丁草胺、敵稗、Pretilachlor、2,4-D、雙草醚鈉和氰氟草酯是該地區常用的一些除草劑。

- 水稻是亞洲最重要的作物,佔全球水稻產量和消費量的90%。除草劑主要用於穀物和穀類,因為亞太地區是稻米等主食穀物的最大出口區和生產區。 2022 年,穀物和穀類產品的以金額為準佔比為 56.6%。

- 該地區的許多國家都採用了綜合雜草管理措施,包括使用所有可用的相容控制策略來最大限度地減少產量損失。新引進的雜草需要立即根除,以免蔓延到其他地區,但可以使用除草劑來控制。在菲律賓的新怡詩夏省和伊洛伊洛省,透過結合栽培管理並適當使用除草劑,產量分別提高了約10%至15%。

- 然而,雜草群體中除草劑抗性的出現帶來了重大挑戰,因為它限制了有效雜草管理的除草劑選擇。同時,日本等各國政府正在投資研究舉措,以發現新的雜草及其相應的除草劑。這些政策鼓勵農民採取作物保護措施,旨在促進這一領域的成長。預計該部分在預測期內(2023-2029 年)的複合年成長率將達到 6.1%。

亞太地區除草劑市場趨勢

水稻等主要作物雜草滋生日益嚴重,需要有效的除草措施,導致每公頃除草劑消費量增加

- 在亞太地區,每公頃除草劑的使用量與前期相比大幅增加。這是由於農業中雜草的普遍存在,雜草成為各種疾病的傳播媒介,導致該地區真菌感染疾病增加,作物損失增加。日本每公頃除草劑的消費量在歷史時期內顯著增加,估計比亞太其他地區高出約 7%。該國每公頃除草劑使用量的增加是由於多種因素造成的,包括農業人口老化、勞動力短缺和農田面積增加。因此,水稻和大豆等主要作物的雜草管理已從人工除草轉變為使用除草劑。

- 緬甸每公頃除草劑消費量位居該地區第二,2022年每公頃消耗量為2200克,高於2017年的1600克。這一成長很大程度上得益於採用適當的雜草管理技術來控制雜草,提高水稻等主要作物的農業產量。旱季因雜草造成的水稻平均產量損失約65%,雨季則約34%。該國農民嚴重依賴除草劑產品來控制主要作物的雜草,導致每公頃除草劑的消費量增加。

- 在亞太地區,除中國外,所有國家由於主要作物雜草侵染增加,每公頃除草劑使用量與去年同期相比均增加。但中國實施農藥零成長政策,所以採用其他除草方法。

氣候變遷對作物帶來壓力,進而促進雜草生長,推動市場發展。

- 甲草胺是一種選擇性系統性除草劑,可透過抑制光合作用用於控制玉米、甘蔗、馬鈴薯和番茄等主要作物中的闊葉雜草。 2022 年的價格為每噸 16,600 美元。

- Atrazine是一種廣泛用於控制玉米和水稻作物中的闊葉雜草和禾本科雜草(如稗草、莧菜屬和莧菜)的除草劑。 2022 年,該除草劑的價值為 13,800 美元。

- Paraquat是克無蹤的有效成分,用來控制雜草和草類。它也用於在收穫前乾燥棉花等作物。 2022年Paraquat的價格為每噸4,600美元。中國是Paraquat的主要出口國,其80%以上的Paraquat產量出口到世界各國。

- 二甲戊靈是一種選擇性出苗前除草劑,2022 年的價格為每噸 3,300 美元。可廣譜防治馬鈴薯、菸草、高粱、水稻和甘蔗作物中的一年生雜草和闊葉雜草。同樣,常見的系統性除草劑2,4-二氯苯氧乙酸(2,4-D) 的 2022 年價格評估為每噸 2,300 美元。它用於控制草皮、草坪、田地、果樹和蔬菜作物中的闊葉雜草。

- Glyphosate是頻譜廣譜系統性除草劑和作物乾燥劑,2022 年的價格為每噸 1,100 美元。Glyphosate主要用於控制禾本科、莎草科和闊葉雜草。

- 氣候變遷將損害和給植物帶來壓力,對植物健康產生負面影響,因為它們無法在極端壓力條件下生存,並且會加劇雜草的生長。這將進一步導致對除草劑的需求增加,從而推高有效成分的價格。

亞太除草劑產業概覽

亞太地區除草劑市場適度整合,前五大公司佔50.02%的市佔率。市場的主要企業是:拜耳股份公司、科迪華農業科技、Nufarm Ltd、先正達集團和UPL Limited。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 價值鏈與通路分析

第5章 市場區隔

- 執行模式

- 化學噴塗

- 葉面噴布

- 燻蒸

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001681

The Asia Pacific Herbicide Market size is estimated at 7.55 billion USD in 2025, and is expected to reach 9.97 billion USD by 2030, growing at a CAGR of 5.73% during the forecast period (2025-2030).

The market is being driven by increasing weed infestation and associated yield losses in crops

- The Asia-Pacific region is home to a diverse range of crops, encompassing staple food crops like rice, wheat, corn, and soybeans, as well as cash crops such as cotton, sugarcane, fruits, and vegetables, which face challenges from several weed species. In 2022, the soil treatment method accounted for the largest share of 46.8% in the Asia-Pacific herbicide market, representing a value of USD 3.0 billion. Soil treatment involves the direct application of herbicides to the soil, serving as an effective means of weed control. This method can be utilized either before planting or after crop emergence, targeting weed seeds, seedlings, or established weeds present in the soil.

- In 2022, foliar application of herbicides held a market share of 32.6% and was valued at USD 2.1 billion. This method is highly effective in targeting broadleaf weeds, sedges, grasses, and even aquatic weeds. By directly applying herbicides to the foliage of these weeds, maximum absorption and control can be achieved. The flexibility of foliar application allows farmers to target weeds during their active growth stages for optimal results.

- In 2022, chemigation accounted for 18.9% of herbicide application methods, valued at USD 1.2 billion. This growth is attributed to the increasing adoption of micro-irrigation systems and the ease of herbicide application, ensuring uniform distribution throughout the cropland.

- Fumigation can provide effective and targeted weed control, especially in enclosed environments where other methods may be less effective. It can reach weed seeds, root systems, and weed propagules that are difficult to control through other means.

- Owing to the advantages and specificity of each method, the market for each method is anticipated to grow during the forecast period.

The use of herbicides for major crops like rice is growing across the region

- The herbicide market in Asia-Pacific witnessed steady growth during the historical period, with the region occupying a significant share of the global herbicide market in 2022. Butachlor, propanil, pretilachlor, 2,4-D, bispyribac-sodium, and cyhalofop-butyl are the commonly used herbicides in the region.

- Rice is by far the most important crop in Asia; the region accounts for 90% of the world's production and consumption of rice. Herbicides are mostly used for grains and cereals in the Asia-Pacific as the region is the largest exporter and producer of staple grains such as rice. The grains & cereals segment occupied a share of 56.6% by value in 2022.

- Many countries in the region have adopted the Integrated weed Management method that entails the use of all available compatible control tactics to minimize yield losses. Newly introduced weeds that would require immediate eradication before they spread to other areas can be controlled with the use of herbicides. It was observed that combining cultural management practices and judicious herbicide usage resulted in higher yields of about 10% to 15% in the Nueva Ecija and Iloilo provinces of the Philippines, respectively.

- However, the occurrence of herbicide resistance in weed populations presents a big challenge as it limits herbicide choices for effective weed management. At the same time, governments of various countries like Japan are investing in research initiatives to discover new weeds and their subsequent herbicides. Such policies are encouraging farmers to adopt crop protection practices that aim to contribute to the growth of the segment. The segment is expected to record a CAGR of 6.1% during the forecast period (2023-2029).

Asia Pacific Herbicide Market Trends

Increased weed infestations in major crops like rice need efficient weed control, boosting the per hectare herbicide consumption

- In the Asia-Pacific region, the use of herbicides per hectare significantly increased over the historical period. This is due to the prevalence of weeds in agriculture, which are acting as vectors for a variety of diseases, resulting in an increase in fungal infections and crop loss in the region. Japan experienced a significant rise in herbicide consumption per hectare over the historical period, which was estimated to be approximately 7% higher than the rest of the Asia-Pacific region. The increasing use of herbicides per hectare in the country is attributed to a combination of factors, including the aging of farmers, a lack of labor, and an increase in agricultural land. This resulted in a shift from manual weeding to the use of herbicides for weed management in major crops such as rice and soybeans.

- Myanmar ranks second in the region in terms of herbicide consumption per hectare, with 2,200 grams of herbicide per hectare consumed in 2022, an increase over the 1,600 grams consumed in 2017. This increase is largely attributed to the implementation of appropriate weed management techniques to control weeds and enhance agricultural production in key crops such as rice. The average yield losses in rice crops due to weeds are approximately 65% and 34% in the dry and wet seasons, respectively. Farmers in the country are majorly reliant on herbicide products to control weeds in major crops, which has led to increased consumption of herbicides per hectare.

- Overall, in the Asia-Pacific region, herbicide use per hectare increased Y-o-Y in all countries except China, as weed infestations increased in the major crops. However, China is using other weed control methods as it implements zero growth policies in pesticides.

Climate change causing stress to crop plants, thus leading to increased weed growth driving the market

- Metribuzin is a selective and systemic herbicide used to control broadleaf weeds in major crops like corn, sugarcane, potatoes, and tomatoes by inhibiting photosynthesis. In 2022, it was priced at USD 16.6 thousand per metric ton.

- Atrazine is an herbicide widely used for the control of broadleaf and grassy weeds like Echinocloa, Elusine spp., and Amaranthus viridis in maize and rice crops. The herbicide was valued at a price of USD 13.8 thousand in 2022.

- Paraquat is the active ingredient in Gramoxone, which is used to control weeds and grasses. It is also used for the desiccation of crops, like cotton, prior to harvest. Paraquat was valued at a price of USD 4.6 thousand per metric ton in 2022. China is a major paraquat export country, and over 80% of its paraquat output is exported to countries worldwide.

- Pendimethalin is a selective pre-emergence herbicide valued at USD 3.3 thousand per metric ton in 2022. It offers broad-spectrum control of annual grasses and broadleaf weeds in potato, tobacco, sorghum, rice, and sugarcane crops. Similarly, 2,4-dichlorophenoxyacetic acid (2,4-D) is a common systemic herbicide that was valued at a price of USD 2.3 thousand per metric ton in 2022. It is used in the control of broadleaf weeds in turf, lawn, field, fruit, and vegetable crops.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant, priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves.

- Climate change can cause damage and stress to plants and be detrimental to plant health as they cannot survive in extreme stress conditions, leading to increased weed growth. This further leads to an increase in herbicide demand, thereby boosting the prices of active ingredients.

Asia Pacific Herbicide Industry Overview

The Asia Pacific Herbicide Market is moderately consolidated, with the top five companies occupying 50.02%. The major players in this market are Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

除草劑安全劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按除草劑、按應用階段、按地區和競爭進行細分,2020-2030F

除草劑安全劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按除草劑、按應用階段、按地區和競爭進行細分,2020-2030F 麥草畏除草劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、配方、物理形態、使用模式、應用時間、地區和競爭進行細分,2020-2030 年預測

麥草畏除草劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、配方、物理形態、使用模式、應用時間、地區和競爭進行細分,2020-2030 年預測 中國除草劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

中國除草劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 北美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

北美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 南美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

南美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印尼除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年)

印尼除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年) 印度除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

印度除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 歐洲除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 美國除草劑:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030 年)

美國除草劑:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030 年) 越南除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年)

越南除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年)

▼