|

市場調查報告書

商品編碼

1684006

越南除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年)Vietnam Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

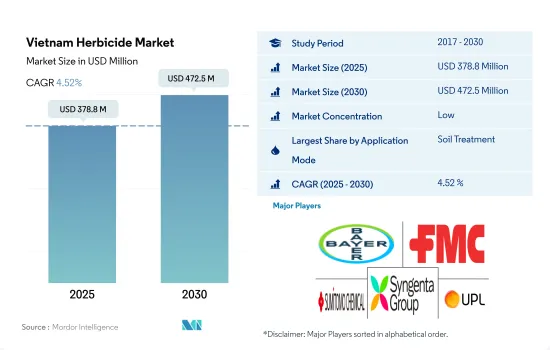

預計 2025 年越南除草劑市場規模將達到 3.788 億美元,到 2030 年將達到 4.725 億美元,預測期內(2025-2030 年)的複合年成長率為 4.52%。

傳統除草劑的土壤處理及其對保護主要作物品質的有效性可能會提高土壤處理的採用率。

- 在越南,人們以各種方式使用除草劑來有效控制農田中的雜草。透過採用正確的施用方法,農民可以施用除草劑,有效覆蓋特定區域,並最大限度地減少浪費,從而節省成本。效率的提高將最佳化除草劑的使用,從而降低農民的投入成本。

- 2022年,土壤施用是農業除草劑噴灑的主流類型,佔除草劑噴灑總量的46.4%。穀物和穀類產品佔據最大的市場佔有率,為 64.6%。土壤施用除草劑是優選的,因為它們有助於透過防止或減少雜草生長來保護作物和穀類的品質。

- 2022年,葉面噴布在除草劑施用領域排名第二,市場佔有率為33.2%。這是因為葉面噴布除草劑具有快速起效的特性,可以快速破壞目標雜草的生理過程。這種快速作用會導致雜草枯萎、變黃並死亡。這種優勢在處理侵略性強或競爭性強的雜草品種時非常有用,因為如果不加以有效控制,這些雜草品種很快就會佔領作物的主導地位。

- 在越南的農業領域,使用除草劑的目的是最大限度地提高作物的生產力並提高作物的整體盈利。除草劑應用形式的市場佔有率預計將實現 4.9% 的複合年成長率。

越南除草劑市場趨勢

出於保護作物免受雜草侵害和提高產量的需求,耐除草劑作物的採用預計將推動除草劑的消費。

- 2021 年至 2022 年,越南的除草劑消費量預計將穩定成長。這種成長趨勢可以歸因於多種因素,包括採用抗除草劑作物、農業實踐以及採用的雜草管理策略。此外,基改作物的傳播也導致除草劑使用量激增。

- 越南基改耐除草劑玉米(GM玉米)的種植面積大幅擴大。 2019 年,越南農民在 92,000 英畝土地上種植了基改玉米,特別是抗除草劑玉米。與前一年(2018 年)相比,種植面積增加了 88%。基因改造耐除草劑作物的日益普及是 2018 年至 2019 年該國除草劑消費量增加的驅動力之一。

- 雜草的存在對作物產量構成重大威脅並造成重大損失。因此,農民嚴重依賴除草劑來控制雜草生長並盡量減少產量損失。預計這一因素將進一步推動除草劑市場的成長。

- 此外,雜草的持久性和適應性預計將需要增加除草劑的施用率和使用具有不同作用方式的多種除草劑。

- 因此,採用耐除草劑作物(包括基因改造品種)將導致更高的除草劑施用率和多種除草劑的使用,以滿足控制雜草和減少產量損失的需求。預計這些因素將推動除草劑的消費。

越南農業模式的改變導致土壤劣化和雜草叢生

- 越南高地的農業正從短作長期休耕轉變為短作短期休耕或永久種植。結果,經常出現土壤劣化和雜草過度生長的情況。水稻是越南的主要作物,而柿子(Echinochloa crus-galli)是稻田中最具破壞性的雜草之一。在湄公河三角洲地區,這種雜草導致 2021 年直播稻米區的產量損失了 46%。

- 甲草胺是一種選擇性、系統性除草劑,透過抑制光合作用用於控制玉米、甘蔗、馬鈴薯和番茄等主要國內作物中的闊葉雜草。 2022 年,其價值為每噸 16,600 美元。

- 2022 年,越南常見的系統性除草劑2,4-二氯苯氧乙酸(2,4-D) 的價格為每噸 2,300 美元。 2,4-D 用於控制草皮、草坪、田間作物和果菜中的闊葉雜草。

- 同樣,二甲戊靈是一種選擇性出苗前除草劑,2022 年的價格為每噸 3,300 美元。可廣譜防治馬鈴薯、菸草、高粱、水稻和甘蔗中的一年生雜草和闊葉雜草。 2022年,越南將從印度進口約3,000噸二甲戊靈。

- 不同的天氣條件會對植物造成損害和壓力,這會對植物的健康產生負面影響,因為它們無法忍受極端的壓力。氣溫、濕度和降雨的極端變化以及冰雹、乾旱和颱風等天氣條件促進了雜草的生長。這將進一步導致除草劑需求增加,從而推高國內活性成分的價格。

越南除草劑產業概況

越南除草劑市場較為分散,前五大公司佔了24.69%的市場。市場的主要企業有:拜耳股份公司、FMC株式會社、住友化學、先正達集團和UPL有限公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 越南

- 價值鍊和通路分析

第5章市場區隔

- 執行模式

- 化學噴塗

- 葉面噴布

- 燻蒸

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001708

The Vietnam Herbicide Market size is estimated at 378.8 million USD in 2025, and is expected to reach 472.5 million USD by 2030, growing at a CAGR of 4.52% during the forecast period (2025-2030).

Traditional herbicide soil treatments and their effectiveness in protecting the quality of major crops may raise soil treatment adoption

- In Vietnam, herbicides are applied through various modes to control weeds in agricultural practices effectively. Farmers can achieve cost savings by utilizing suitable modes of application, allowing them to apply herbicides, effectively covering specific areas, and minimizing wastage. This increased efficiency leads to optimized herbicide usage, resulting in reduced input costs for farmers.

- In 2022, the dominant mode of herbicide application in agricultural practices was soil application, accounting for 46.4% of the overall herbicide application segment. The grains & cereals segment held the largest market share at 64.6%. The preference for soil treatment herbicides is attributed to their effectiveness in protecting the quality of grains and cereals by preventing or reducing weed growth.

- In 2022, foliar application was the second leading and held a market share of 33.2% in the segment of herbicide application. This is due to foliar herbicides being beneficial due to their fast-acting properties, which can rapidly disrupt the physiological processes of targeted weeds. This swift action results in symptoms like wilting, yellowing, or necrosis in the weeds. This advantage is valuable when tackling aggressive or competitive weed species that have the potential to rapidly dominate the crops if not effectively controlled.

- In the Vietnamese agricultural sector, the utilization of herbicides is aimed at maximizing crop productivity and improving overall crop profitability. The mode of application of herbicides is projected to register a CAGR of 4.9% in terms of market share.

Vietnam Herbicide Market Trends

The adoption of herbicide-tolerant crops with the need to protect the crops from weeds and improve yield is expected to drive the consumption of herbicides

- The consumption of herbicides in Vietnam witnessed a steady upward trend between 2021 and 2022. This increasing trend can be attributed to various factors, including the adoption of herbicide-tolerant crops, agricultural practices, and strategies employed for weed management. Furthermore, the expansion of genetically modified (GM) crops has contributed to the surge in herbicide usage.

- The cultivation of genetically modified herbicide-tolerant maize (GM corn) grew on a significant scale in Vietnam. In 2019, farmers in the country cultivated GM corn, specifically herbicide-tolerant maize, on an expansive 92,000 acres of land. This represented an 88% increase in acreage compared to the previous year, 2018. The increased adoption of GM herbicide-tolerant crops was one of the driving factors behind the rise in herbicide consumption in the country between 2018 and 2019.

- The presence of weeds poses a significant threat to crop yields, causing substantial damage. Consequently, farmers heavily rely on herbicides to regulate weed growth and minimize yield losses. This factor is further expected to bolster the growth of the herbicide market.

- Furthermore, the persistent and adaptable nature of weeds is expected to necessitate higher rates of herbicide application and the utilization of multiple herbicides with diverse modes of action.

- Therefore, due to the adoption of herbicide-tolerant crops, including genetically modified varieties, the need to control weeds and minimize yield losses leads to higher application rates and the use of multiple herbicides. These factors are expected to fuel the consumption of herbicides.

Changing agriculture patterns in Vietnam are leading to soil degradation and high weed infestation

- Agriculture in the uplands of Vietnam is changing from short cultivation-long fallow periods to short cultivation-short fallow periods or even permanent cropping. Soil degradation and high weed infestation are often the consequences. Rice is the major crop in Vietnam, and barnyard grass (Echinochloa crus-galli) is one of the most devastating weeds in the rice fields. In the Mekong Delta, this weed caused 46% rice yield losses in direct-seeded rice areas in 2021.

- Metribuzin is a selective and systemic herbicide that is used to control broadleaved weeds in major crops in the country, like corn, sugarcane, potatoes, and tomatoes, by inhibiting photosynthesis. In 2022, it was valued at USD 16.6 thousand per metric ton.

- In 2022, 2,4-dichlorophenoxyacetic acid (2,4-D), a common systemic herbicide, was valued at USD 2.3 thousand per metric ton in Vietnam. It is used to control broadleaf weeds in turf, lawns, field crops, and fruit and vegetable crops.

- Similarly, pendimethalin is a selective pre-emergence herbicide valued at USD 3.3 thousand per metric ton in 2022. It has broad-spectrum control of annual grasses and broadleaf weeds in potato, tobacco, sorghum, rice, and sugarcane. Vietnam imported around 3.0 thousand metric tons of pendimethalin from India in 2022.

- A variety of weather conditions can cause damage and stress to plants and thus be detrimental to plant health as they cannot survive extreme stress. These conditions, including extremes of temperature, humidity, and rain, as well as hail, drought, and typhoons, lead to increased weed growth. This will further lead to increased herbicide demand, thereby inflating the prices of active ingredients in the country.

Vietnam Herbicide Industry Overview

The Vietnam Herbicide Market is fragmented, with the top five companies occupying 24.69%. The major players in this market are Bayer AG, FMC Corporation, Sumitomo Chemical Co. Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

除草劑安全劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按除草劑、按應用階段、按地區和競爭進行細分,2020-2030F

除草劑安全劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按除草劑、按應用階段、按地區和競爭進行細分,2020-2030F 麥草畏除草劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、配方、物理形態、使用模式、應用時間、地區和競爭進行細分,2020-2030 年預測

麥草畏除草劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按作物類型、配方、物理形態、使用模式、應用時間、地區和競爭進行細分,2020-2030 年預測 中國除草劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

中國除草劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 亞太除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

亞太除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 北美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

北美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 南美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030)

南美除草劑:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印尼除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年)

印尼除草劑市場:佔有率分析、產業趨勢與成長預測(2025-2030年) 印度除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

印度除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 歐洲除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

歐洲除草劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 美國除草劑:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030 年)

美國除草劑:市場佔有率分析、產業趨勢、統計、成長預測(2025-2030 年)

▼