|

市場調查報告書

商品編碼

1685935

北美農業機械:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)North America Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

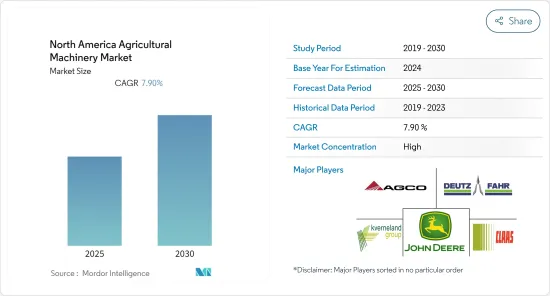

預測期內北美農業機械市場預計複合年成長率為 7.9%

主要亮點

- 農場整合的不斷增加、光明的經濟前景、龐大的生產基地以及政府透過補貼不斷增加的支持正在推動大容量農業機械和設備的銷售。根據設備工業協會(AEM)的數據,2021年北美銷售的曳引機和聯合收割機總數為36萬台。今年,美國和加拿大幾乎所有類型的農業曳引機和聯合收割機的銷售量都增加了 10% 或更多。

- 大片農田的存在,農業機械化的需求很高。此外,北美擴大使用配備監控技術的智慧聯合收割機來提高農業產量。預計人事費用上升、曳引機和收割機採用機器人系統和 GPS、大型農場對大容量機械的需求增加以及自行式機械的日益普及將在預測期內推動市場成長。美國農業機械巨頭約翰迪爾 (John Deere) 已著手收購人工智慧Start-UpsBlue River Technology,以加強其基於人工智慧的曳引機創新流程。這些技術創新有望從長遠來看推動對技術先進的曳引機的需求。

- 現在,全國各地的農民都可以及時獲得農機貸款補貼,貸款利率和還款計畫靈活。因此,即使是小農戶現在也能夠投資大型農業機械。美國政府透過美國農業部直接經營貸款、美國農業部經營小額貸款和美國農業部擔保經營貸款為農業設備提供融資。信貸寬鬆和農民轉向技術來提高生產力使得一系列機器獲得了兩位數的利潤,刺激了該地區的市場成長。

北美農業機械市場趨勢

農業機械普及率高、創新能力強

曳引機技術的快速發展正在徹底改變北美農業。隨著對作物的需求不斷增加,農業成本不可避免地上升,曳引機成為高效農業不可避免的一部分。根據加拿大農業人力資源委員會預測,到2029年,加拿大農業勞動力短缺數量預計將翻倍,達到12.3萬人。 2020-21年,農業勞動力短缺對該國農民造成約29億美元的損失,預計未來幾年短缺情況將進一步擴大。加拿大的平均農場規模也逐年擴大,這可能會促進農業機械(曳引機、聯合收割機等)的銷售。

近年來,農場管理的永續性需求引發了對高度發展和高效機械的需求,推動了所研究市場的成長。例如,根據設備製造商協會的數據,2020年6月自走式聯合收割機的銷售量從125台增加到143台,累計銷售量(2020年1月至2020年10月)達264台,比去年同期成長3.1%。

因此,曳引機已經處於技術前沿,擁有基於人工智慧的工具,可用於資料傳輸和更好的決策流程。 2022年,加拿大農業和食品部宣布透過農業科學計畫提供超過100萬美元的資金,幫助生產者改善農場管理和收益。預計這些技術進步將從長遠來看推動對技術先進的曳引機的需求,從而在未來幾年推動市場發展。

美國主導市場

大規模農場經營、勞動力減少以及提高農業生產率的需求是研究期間該地區農業機械銷售的主要驅動力。農業是美國的主要職業之一,農業機械化被認為是提高生產力、銷售和出口的重要原因。

美國市場以低功率曳引機的銷售為主,其中40匹馬力以下的曳引機佔有很大的佔有率。據估計,在一個技術先進的農場,一個農民可以生產足夠的糧食來養活近 1,000 人。然而,在20世紀,這個限制是25,比例為1:130。目前,技術進步主要集中在農田曳引機的使用。

在美國等已開發國家,更換週期較短,僅9年,這導致對新型曳引機的需求增加,帶動了北美市場的發展。例如,約翰迪爾在薩爾蒂約生產 105-140 馬力的曳引機,而 CNH Industrial 的 New Holland 分部在克雷塔羅生產 90-115 馬力的曳引機。 John Deere、New Holland、Valtra 和 Pauny 是領先的曳引機製造商。

北美農機產業概況

北美農業機械市場格局趨於穩定,大型企業佔據主導地位。市場的主要企業包括迪爾公司、愛科集團、Same Deutz-Fahr Deutschland GmbH、CLAAS 集團、Kverneland 集團等。各公司正在創新新型機械以滿足不斷變化的消費者需求,提供使農業更有效率、更容易的新技術。在所研究的市場中,許多國際參與者正在與國內參與者合作,以擴大其影響力並擴展其高階、價值導向多功能曳引機產品系列的服務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 市場限制

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場區隔

- 類型

- 聯結機

- 小於40馬力

- 40至100馬力

- 超過100馬力

- 四輪驅動農用曳引機

- 裝置

- 犁

- 光環

- 耕耘機和耕耘機

- 其他設備

- 灌溉機械

- 噴水灌溉

- 滴灌

- 其他灌溉機械

- 收割機

- 聯合收割機

- 青貯收割機

- 其他收割機械

- 牧草和飼料機械

- 草坪修剪機

- 打包機

- 其他牧草和飼料機械

- 其他類型

- 聯結機

- 地區

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

第6章競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- AGCO Corporation

- CLAAS Group

- CNH Industrial NV

- Deere & Company

- Kubota Corporation

- Kverneland Group

- Morris Industries Ltd

- Netafim Irrigation Inc.

- Same Deutz-Fahr Deutschland GmbH

- Vaderstad Industries Inc.

第7章 市場機會與未來趨勢

The North America Agricultural Machinery Market is expected to register a CAGR of 7.9% during the forecast period.

Key Highlights

- Increased farm consolidation, positive economic outlook, large production base, and greater government support through subsidies are driving sales of high-capacity agricultural machinery and equipment. According to the Association of Equipment Manufacturers (AEM), the total number of tractors and combines sold in 2021 in North America was 360,000 units. That year, there was a sale increase of over 10% in nearly every segment of agricultural tractors and combines in the United States and Canada.

- The presence of extensive farmland has led to high demand for farm mechanization. Furthermore, the North American region is experiencing a rise in the use of smart combine harvesters equipped with monitoring technologies to boost farm production. Rising labor costs, the incorporation of robotic systems and GPS in tractors and harvesters, increased demand for high-capacity machinery due to large farms, and the increasing popularity of self-propelled machines are expected to drive market growth during the forecast period. The US-based agricultural machinery giant, John Deere, began enhancing the AI-based innovation process in tractors by acquiring an AI start-up, Blue River Technology. Such innovations are expected to drive the demand for technologically advanced tractors in the long term.

- Farmers in the country have been able to avail timely subsidies in the form of agriculture equipment loans at flexible interest rates and repayment schedules. This, in turn, has helped even small-scale farmers to invest on primary agricultural equipment. The US government extends loans for farm equipment through USDA Direct Operating Loans, USDA Operating Microloans, and USDA Guaranteed Operating Loans. The farmers inclinination toward technology due to easy loans and to enhance productivity has resulted in double-digit gains for various machineries, thus is fuelling the market growth in the region.

North America Agricultural Machinery Market Trends

High Adoption of and Innovations in Farm Machinery

Rapid technological developments in tractors are currently revolutionizing farming in North America. Farm costs are inevitably higher with the increasing demand for food crops, thus, making tractors an inevitable part of efficient farming. According to the Canadian Agriculture Human Resource Council, Canada's farm labor deficit is anticipated to double by 2029 and lead to a 123,000-worker shortage. During 2020-2021, the farm labor shortage cost around USD 2.9 billion for farmers in the country, and this shortage is anticipated to grow over the coming years. This will boost agricultural machinery sales (tractors, combines, etc.) as the average farm size in Canada is also growing every year.

The need for sustainability in the management of farm operations has induced the demand for highly developed and efficient machinery in recent years and is driving the growth of the market studied. For instance, according to the Association of Equipment Manufacturers, the sale of self-propelled combine harvesters in June 2020 increased from 125 units to 143 units, resulting in year-to-date sales (January 2020 - October 2020) of 264 units, which was 3.1% higher when compared to the same period in the previous year.

Thus, the wave of modern technology has already been witnessed in tractors with the application of Artificial Intelligence-based tools for data transmission and precise decision-making processes in cultivation. In 2022 Canada, The Ministry of Agriculture and Agri-Food, announced over USD 1 million in funding for SomaDetect Inc. and Vivid Machines Inc. through the AgriScience Program to help producers improve farm management and their bottom line. Such innovations are projected to induce the demand for technologically developed tractors, in the long run, thus also boosting the market over the coming years.

United States Dominates the Market

Large-scale farming operations, a decline in labor, and the need to enhance the productivity of agriculture are the factors that are mainly driving the sales of agricultural machinery in the region during the study period. Agriculture is one of the major occupations in the United States, where the mechanization of farming is considered an important reason for increased productivity, sales, and export.

The United States market is driven by the sale of low-engine-power tractors with tractors of power less than 40 HP accounting for a major share of the market. It is estimated that on a technologically advanced farm, one farmer can produce enough cereals to feed almost a thousand people. However, in the twentieth century, that was limited to 25 people, with the ratio standing at 1:130. Technological advancements are now directed toward the use of tractors in agricultural fields.

The shorter replacement cycles of 9 years in advanced economies like the United States increase the demand for new tractors, and hence, drive the market in North America. For instance, John Deere manufactures tractors in the 105-140 HP range in Saltillo and CNH Industrial's New Holland division manufactures tractors in the 90-115 HP range in Queretaro. John Deere, New Holland, Valtra, and Pauny are the top tractor manufacturers.

North America Agricultural Machinery Industry Overview

The North American agricultural machinery market is consolidated, with the major players occupying the majority share. The major players in the market are Deere and Co., AGCO Corporation, Same Deutz-Fahr Deutschland GmbH, CLAAS Group, and Kverneland Group, among others. Companies are innovating new types of machinery as per the changing consumer demand and are offering new technologies to bring more efficiency and ease agricultural operations. Many international players in the market studied have also been collaborating with domestic players to increase their reach and expand their services for high-end and value-oriented utility tractor range.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Tractor

- 5.1.1.1 Less than 40 HP

- 5.1.1.2 40 to 100 HP

- 5.1.1.3 Above 100 HP

- 5.1.1.4 4 WD Farm Tractors

- 5.1.2 Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler Irrigation

- 5.1.3.2 Drip Irrigation

- 5.1.3.3 Other Irrigation Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.6 Other Types

- 5.1.1 Tractor

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

- 5.2.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 AGCO Corporation

- 6.3.2 CLAAS Group

- 6.3.3 CNH Industrial NV

- 6.3.4 Deere & Company

- 6.3.5 Kubota Corporation

- 6.3.6 Kverneland Group

- 6.3.7 Morris Industries Ltd

- 6.3.8 Netafim Irrigation Inc.

- 6.3.9 Same Deutz-Fahr Deutschland GmbH

- 6.3.10 Vaderstad Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年農業設備市場規模、佔有率、趨勢及預測(按設備類型、應用、銷售通路和地區)

2025 年至 2033 年農業設備市場規模、佔有率、趨勢及預測(按設備類型、應用、銷售通路和地區) 全球農業和農業金融市場 - 2025-2032

全球農業和農業金融市場 - 2025-2032 歐洲農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農業機械:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)非洲農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

歐洲農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國農業機械:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)非洲農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 農業設備融資市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

農業設備融資市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球農業機械市場(至 2032 年):按功率(<30 馬力、31-70 馬力、71-130 馬力、131-250 馬力、>250 馬力)、類型(曳引機、打包機、噴霧器、收割機)、功能、曳引機驅動、電動機區

全球農業機械市場(至 2032 年):按功率(<30 馬力、31-70 馬力、71-130 馬力、131-250 馬力、>250 馬力)、類型(曳引機、打包機、噴霧器、收割機)、功能、曳引機驅動、電動機區 收穫前設備市場規模、佔有率及成長分析(按類型、分佈、應用和地區)-2025-2032 年產業預測

收穫前設備市場規模、佔有率及成長分析(按類型、分佈、應用和地區)-2025-2032 年產業預測 歐洲精準除草市場:按應用、應用地點、類型和國家進行分析和預測(2024-2034 年)

歐洲精準除草市場:按應用、應用地點、類型和國家進行分析和預測(2024-2034 年) 2025年全球農業機械和設備市場報告

2025年全球農業機械和設備市場報告