|

市場調查報告書

商品編碼

1687083

紙板包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Paperboard Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

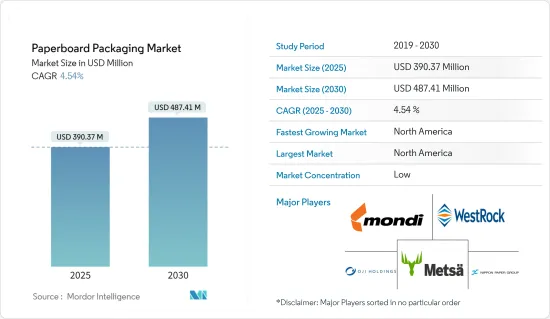

紙板包裝市場規模預計在 2025 年為 3.9037 億美元,預計到 2030 年將達到 4.8741 億美元,預測期內(2025-2030 年)的複合年成長率為 4.54%。

主要亮點

- 紙板包裝是包裝食品市場的首選。它用於各種食品,包括湯、調味品和乳製品。紙板通常覆蓋有聚合物或塑膠以保持其清潔和防污。與玻璃或金屬相比,它可以減輕最終產品的總重量,同時保持食物的新鮮度。紙板是一種完美的包裝材料,因為它沒有氣味和味道。

- 越來越明顯的是,當談到包裝時,消費者更重視可回收性和生物分解性,而不是再生性。這顯示消費者越來越擔心包裝廢棄物對環境的未來影響。美國超過 60% 的社區收集和回收紙板包裝。公司也正在朝著推出回收紙板產品的方向發展。例如,Cascades推出了由可回收纖維製成的瓦楞紙托盤,SIG開發了利用消費後廢棄物製成的再生聚合物紙箱。

- 此外,根據聯合國糧食及農業組織(FAO)2023年11月發布的報告,中國國內紙和紙板領域的生產線將對全球貿易動態產生重大影響。中國加強製造能力(特別是紙漿採購能力)的戰略舉措對國際供應鏈構成了挑戰。因此,預計紙板市場將在中國快速成長的生產能力和出口潛力推動下需求上升的帶動下實現成長。

- 不過,聯合國歐洲經濟委員會的報告表示,由於需求減弱和價格下跌,歐洲紙張和紙板產量將在2023年上半年下降,迫使部分機器關閉。預計 2023 年紙和紙板產量將下降 2.7% 至 9,010 萬噸。停產可能會影響紙板市場,因為它可能會收緊供應並影響價格動態。

- 有幾個方面正在推動紙板包裝行業的發展,包括對永續和環保包裝材料的需求不斷增加、電子商務和網路購物的興起、以及食品和飲料行業的成長。此外,先進的包裝和製造流程使該行業能夠生產出高品質、客製化的包裝解決方案,滿足不同行業和客戶的特定需求。

紙板包裝市場趨勢

食品和飲料領域的需求增加

- 食品和飲料產業是紙板包裝的主要終端用戶,佔全球市場佔有率的一半以上。塗佈未漂白紙板廣泛應用於飲料包裝,顯示其多功能性和耐用性。此外,冷凍食品消費的成長趨勢預計將推動對紙板包裝的需求,為紙板包裝市場創造新的機會,以滿足食品和飲料行業不斷變化的消費者需求。

- 折疊紙盒在食品和飲料行業中廣泛應用,為多種產品提供多功能、經濟高效的包裝解決方案。折疊紙盒可以保持穀物、零食和糖果零食等乾貨的新鮮度,同時為品牌和產品資訊提供充足的空間。輕質而堅固的結構可實現高效的儲存和運輸,有助於簡化物流業務。此外,折疊式紙盒易於打開和關閉,為消費者提供了更大的便利,並延長了產品的商店壽命。

- 根據美國人口普查局的資料,美國食品和飲料企業的每月銷售額正在創造可觀的收益,證實該行業的龐大消費正在推動對紙板包裝的需求。隨著製造商尋求永續且經濟高效的解決方案來滿足其食品和飲料包裝需求,該國紙板包裝市場的成長預計將上升。

- 生活方式的改變和年輕消費者數量的增加導致對品牌和包裝產品的需求激增。根據Appmysite在2024年2月發布的消息,美國三分之一的顧客每週至少使用兩次線上食品訂購服務。因此,食品宅配和零售業對便利性、環保包裝選擇的需求日益成長,預計將推動對紙板包裝等永續、多功能包裝解決方案的需求。

- 例如,2023 年 11 月,主要企業Ariake 宣布將把食品無菌填充到 SIG 紙盒包裝中。 Ariake 打算透過推出一系列採用 SIG Slimline 紙盒包裝的優質液體湯來擴大其湯品組合。

- 由於人口成長、可支配收入增加和對永續性的重視程度不斷提高等因素,印度、中國和日本等國家對紙板包裝的需求正在增加。在印度,不斷壯大的中產階級和環保包裝的監管要求正在推動食品和飲料包裝對紙板解決方案的需求。中國作為全球製造地的地位及其不斷成長的城市人口正在推動食品和飲料行業對紙板包裝的強勁需求。

- 同樣,在永續性和品質至關重要的日本,食品和飲料行業依靠紙板包裝來滿足消費者對環保、高品質包裝解決方案的偏好。總的來說,這些國家為紙板包裝製造商提供了絕佳的機會,使他們能夠滿足食品和飲料行業日益成長的需求,同時實現永續性目標。

北美地區成長率穩定

- 北美仍然是紙板包裝產品的主要市場之一。北美食品和飲料行業嚴重依賴紙板包裝,包括折疊紙盒和瓦楞紙板。這些包裝解決方案耐用、多功能且環保,是運輸和儲存各種食品和飲料的理想選擇。無論是穀物盒包裝、果汁容器或冷凍食品包裝,紙板材料對於確保產品完整性同時保持永續性目標至關重要。

- 此外,折疊紙盒的可自訂特性使品牌能夠在商店以有吸引力的方式來展示他們的產品,從而增加消費者的吸引力並在競爭激烈的市場中推動銷售。此外,瓦楞紙箱是北美食品和飲料行業必不可少的二級或三級包裝,為產品在供應鏈中移動時提供額外的保護並提供品牌機會。

- 北美電子商務市場嚴重依賴紙板包裝市場來實現安全且有效率的產品運輸。瓦楞紙箱對於在運輸過程中保護產品、減少破損以及最大限度地減少因包裝篡改而造成的退貨至關重要。隨著網路購物的迅猛成長,確保產品完好無損地送達客戶已成為首要任務。瓦楞紙箱能夠提供堅固的保護,避免衝擊和搬運事故,從而確保貨物從倉庫到門的完整性。可自訂的設計可對各種尺寸和形狀的產品進行安全包裝,從而提高物流鏈的效率。

- 根據聯合國糧食及農業組織的資料,2023年美國紙和紙板產能為54,183公噸。儘管市場動態不斷變化,但美國穩定的紙板生產能力凸顯了該行業的彈性和穩定性。這種穩定的生產能力代表了各個領域對紙板產品的持續需求,也反映了美國強大的製造業基礎設施和持續滿足國內和國際市場需求的努力。

- 人們對塑膠使用的環境問題的日益關注,加上組織和政府推廣永續包裝材料的舉措,預計將在未來幾年推動紙板市場的擴張。

- 此外,市場先驅者正透過參與併購和研發策略,擴大投資於創新和客製化的包裝解決方案。例如,2023 年 8 月,百事可樂宣布將在北美採用紙板作為其飲料多件包裝。該公司的目標是實現 2025 年的可回收性目標。

紙板包裝產業概況

紙板包裝是一種堅固、輕巧、用途廣泛的解決方案,同時也具有成本效益。可回收的特性使紙板成為永續包裝的可行選擇,尤其是與塑膠等替代品相比。這種適應性進一步凸顯了其對眾多終端用戶產業的適用性。

全球紙板包裝市場高度分散。市場領導者正專注於新產品創新,並著手進行策略性收購以擴大其市場佔有率。市場的主要企業包括日本製紙工業公司、Mondi、Metsa Board、Westrock、Oji Holdings 和 ITC Limited。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭威脅

第5章 市場動態

- 市場促進因素

- 電子商務產業需求強勁

- 擴大輕質材料的使用

- 市場限制

- 森林砍伐對紙包裝的影響

- 營運成本增加

- 紙板進出口場景

- 紙板出口:金額和數量

- 紙板進口:金額和數量

第6章 市場細分

- 按年級

- 紙板

- 瓦楞紙板原紙

- 其他等級

- 依產品類型

- 折疊式紙盒

- 瓦楞紙箱

- 其他類型

- 按最終用戶產業

- 食物

- 飲料

- 衛生保健

- 個人護理

- 家居用品

- 電器

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 亞洲

- 中國

- 日本

- 印度

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 北美洲

第7章 競爭格局

- 公司簡介

- International Paper Company

- Mondi Plc

- Smurfit Kappa Group

- DS Smith Plc

- WestRock Company

- Packaging Corporation of America

- Cascades Inc.

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Rengo Co. Ltd

- Graphic Packaging International

- Metsa Board Oyj

- Sonoco Products Company

- Visy Industries

- Seaboard Folding Box Company Inc.

第8章投資分析

第9章:未來市場展望

The Paperboard Packaging Market size is estimated at USD 390.37 million in 2025, and is expected to reach USD 487.41 million by 2030, at a CAGR of 4.54% during the forecast period (2025-2030).

Key Highlights

- Paperboard packaging is the preferred option in the packaged food market. It can be found in various foods, including soups, seasonings, and dairy products. Paperboard is usually covered with polymers or plastics to keep it clean and unspoiled. Compared to glass and metal, it helps reduce the final product's total weight while maintaining the freshness of the food product. Paperboard is the perfect packing material because of its odor and taste neutrality.

- It is becoming increasingly clear that consumers value recyclability and biodegradability over reusability regarding packaging. This indicates a growing concern among consumers about the future environmental impact of packaging waste. More than 60% of communities in the United States collect and recycle paperboard packaging. Companies are also taking steps to introduce recyclable paperboard products. For instance, Cascades has launched a cardboard tray made from recyclable fibers, while SIG has developed cartons made from recycled polymers that use post-consumer waste.

- Furthermore, according to the FAO's (Food and Agriculture Organization of United Nations) report published in November 2023, China's domestic production line in the paper and paperboard sectors is poised to impact global trade dynamics significantly. With a focus on bolstering its manufacturing capabilities, especially in pulp sourcing, China's strategic initiatives pose challenges to international supply chains. Consequently, the paperboard market is anticipated to witness growth, driven by increased demand fueled by China's burgeoning production capabilities and potential exports.

- However, in the first half of 2023, according to the UNECE report, reduced demand and declining prices led to decreased paper and paperboard production in Europe, prompting the closure of several machines. The outlook for producing paper and paperboard in 2023 indicates a 2.7% decline to 90.1 million tonnes. This downtime is likely to impact the paperboard market by tightening supply and potentially affecting pricing dynamics.

- Several aspects, including the increasing demand for sustainable and eco-friendly packaging materials, the rise in e-commerce and online shopping, and the growth of the food and beverage industry, drive the development of the paperboard packaging industry. Additionally, technological advancements and manufacturing processes have enabled the industry to produce high-quality and customized packaging solutions that serve the specific needs of different industries and customers.

Paperboard Packaging Market Trends

Increasing Demand from Food and Beverage Segment

- The food and beverage industry is the primary end-user of paperboard packaging, commanding over half of the global market share. The coated, unbleached paperboard has extensive use in packaging beverages, showcasing its versatility and durability. Furthermore, the growing trend towards frozen food consumption is expected to fuel demand for folding carton packaging, presenting additional opportunities for the paperboard packaging market to cater to evolving consumer needs in the food and beverage industry.

- Folding cartons find extensive application within the food and beverage industry, offering a versatile and cost-effective packaging solution for a wide range of products. Folding cartons preserve product freshness for dry goods such as cereals, snacks, and confectionaries while providing ample space for branding and product information. Their lightweight yet sturdy construction ensures efficient storage and transportation, contributing to streamlined logistics operations. Additionally, folding cartons offer consumer convenience through easy opening and reclosing features, enhancing user experience and product longevity on store shelves.

- According to data from the United States Census Bureau, the monthly sales of the US food and beverages store, which generate substantial revenue, underscores the vast consumption within the industry, driving the demand for paperboard packaging. As manufacturers seek sustainable and cost-effective solutions to meet the packaging needs of food and beverage products, the growth of the paperboard packaging market in the country is set to rise.

- Shifts in lifestyle and the increasing number of young consumers are driving a surge in demand for branded and packaged products. According to a news published by Appmysite in February 2024, one in three customers in the United States use online food ordering services at least twice a week. Consequently, the demand for sustainable and versatile packaging solutions, such as paperboard packaging, is expected to rise with the escalating need for convenient and eco-friendly packaging options in the food delivery and retail sectors.

- For instance, in November 2023, Ariake, Japan's leading company of livestock-derived natural seasonings, announced that it would fill food products aseptically in SIG carton packs. Ariake intends to grow its broth portfolio with a new range of premium liquid broths packaged in SIG Slimline carton packs.

- Across countries like India, China, and Japan, the demand for paperboard packaging is propelled by factors including population growth, rising disposable incomes, and an increased focus on sustainability. In India, the burgeoning middle class and regulatory mandates for eco-friendly packaging are boosting demand for paperboard solutions in food and beverage packaging. China's status as a global manufacturing hub and its expanding urban population drive robust demand for paperboard packaging in the food and beverage sector.

- Similarly, in Japan, where sustainability and quality are paramount, the food and beverage industry relies on paperboard packaging to meet consumer preferences for eco-friendly and high-quality packaging solutions. Overall, these countries present significant opportunities for paperboard packaging manufacturers as they cater to the growing needs of the food and beverage industry while aligning with sustainability goals.

North America to Witness Steady Growth Rate

- North America continues to be one of the leading markets for paperboard packaging products, owing to the presence of many players operating in the country. North America's food and beverage industry heavily relies on paperboard packaging, including folding cartons and corrugated boxes, for its products. These packaging solutions offer durability, versatility, and eco-friendliness, making them ideal for transporting and storing a wide range of food and beverage items. Whether it's cereal box packaging, juice containers, or frozen food packaging, paperboard materials are crucial in ensuring product integrity while maintaining sustainability goals.

- Additionally, the customizable nature of folding cartons allows brands to showcase their products attractively on store shelves, enhancing consumer appeal and driving sales in the competitive market. Furthermore, corrugated boxes serve as essential secondary or tertiary packaging in the North American food and beverage industry, providing additional layers of protection and branding opportunities for products as they move through the supply chain.

- The e-commerce market in North America relies heavily on the paperboard packaging market for safe and efficient product transportation. Corrugated boxes are crucial in safeguarding products during transit, reducing damage, and minimizing returns due to tampered packaging. With the exponential growth of online shopping, ensuring that products reach customers intact is paramount. Corrugated boxes provide sturdy protection against impacts and handle mishaps, maintaining the integrity of goods from warehouse to doorstep. Their customizable design allows for secure packaging tailored to various product sizes and shapes, enhancing efficiency in the logistics chain.

- According to data from the Food and Agriculture Organization of the United Nations, the production capacity of paper and paperboard in 2023 in the United States was 54,183 MT. The consistent production capacity of paperboard in the United States underscores the industry's resilience and stability despite evolving market dynamics. This steady capacity signifies the enduring demand for paperboard products across various sectors, reflecting the nation's robust manufacturing infrastructure and ongoing commitment to meeting domestic and international market needs.

- Growing environmental concerns surrounding plastic usage, coupled with the efforts of organizations and governments to promote sustainable packaging materials, are anticipated to drive the expansion of the paperboard market in the coming years.

- Furthermore, market players increasingly invest in innovative and customized packaging solutions by engaging in mergers and acquisitions or research and development strategies. For instance, in August 2023, PepsiCo announced the adoption of paperboard for beverage multipacks in North America. The company is aiming to make progress on a 2025 recyclability target.

Paperboard Packaging Industry Overview

Paperboard packaging stands out as a robust, lightweight, and versatile solution, all while being cost-effective. Its recyclable nature makes paperboard a prime choice for sustainable packaging, especially when juxtaposed with alternatives like plastic. This adaptability further underscores its suitability across a myriad of end-user industries.

The global paperboard packaging market is highly fragmented. The major players operating in the market are focusing on innovating new products and entering into strategic acquisitions to strengthen their market presence. Some major players operating in the market include Nippon Paper Industries Co. Ltd, Mondi, Metsa Board, WestRock Company, Oji Holdings Corporation, and ITC Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Threat of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong demand from the e-commerce sector

- 5.1.2 Growing adoption of light weighting materials

- 5.2 Market Restraints

- 5.2.1 Effects of Deforestation on Paper Packaging

- 5.2.2 Increasing Operational Costs

- 5.3 Cartonboard EXIM Scenario

- 5.3.1 Cartonboard Exports By Value and Volume

- 5.3.2 Cartonboard Import By Value and Volume

6 MARKET SEGMENTATION

- 6.1 By Grade

- 6.1.1 Cartonboard

- 6.1.2 Containerboard

- 6.1.3 Other Grades

- 6.2 By Product Type

- 6.2.1 Folding Cartons

- 6.2.2 Corrugated Boxes

- 6.2.3 Other Types

- 6.3 By End-User Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Healthcare

- 6.3.4 Personal Care

- 6.3.5 Household Care

- 6.3.6 Electrical Products

- 6.3.7 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Plc

- 7.1.3 Smurfit Kappa Group

- 7.1.4 DS Smith Plc

- 7.1.5 WestRock Company

- 7.1.6 Packaging Corporation of America

- 7.1.7 Cascades Inc.

- 7.1.8 Oji Holdings Corporation

- 7.1.9 Nippon Paper Industries Co., Ltd.

- 7.1.10 Rengo Co. Ltd

- 7.1.11 Graphic Packaging International

- 7.1.12 Metsa Board Oyj

- 7.1.13 Sonoco Products Company

- 7.1.14 Visy Industries

- 7.1.15 Seaboard Folding Box Company Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

3D 印刷紙及紙板包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

3D 印刷紙及紙板包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 撓性紙包裝市場報告:2031 年趨勢、預測與競爭分析

撓性紙包裝市場報告:2031 年趨勢、預測與競爭分析 印度紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度紙和紙板包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)PE塗佈紙市場報告:2031年趨勢、預測與競爭分析箱板紙包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

印度紙包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度紙和紙板包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)PE塗佈紙市場報告:2031年趨勢、預測與競爭分析箱板紙包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2025年全球紙和紙板包裝市場報告2025年全球紙板包裝市場報告

2025年全球紙和紙板包裝市場報告2025年全球紙板包裝市場報告 2030 年禮盒市場預測:按包裝盒類型、材料、分銷管道、應用、最終用戶和地區進行全球分析

2030 年禮盒市場預測:按包裝盒類型、材料、分銷管道、應用、最終用戶和地區進行全球分析 全球紙墊機市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球紙墊機市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年