|

市場調查報告書

商品編碼

1687984

英國設施管理產業:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)United Kingdom (UK) Facility Management Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

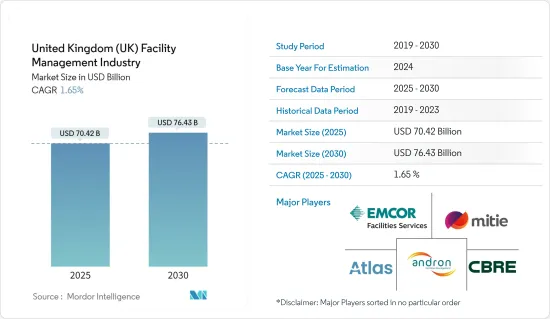

英國設施管理產業預計將從 2025 年的 704.2 億美元成長到 2030 年的 764.3 億美元,預測期內(2025-2030 年)的複合年成長率為 1.65%。

主要亮點

- 就成熟度和複雜度而言,英國是歐洲最成熟、最複雜的設施管理服務市場之一。隨著設施管理服務滲透率的不斷上升,供應商正積極專注於專業化服務,以在因該地區宏觀經濟和社會變化而發生巨大變化的行業中站穩腳跟。

- 過去十年來,在該國營運的各類服務提供者一直致力於擴大其業務,以利用日益成長的設施管理需求,特別是考慮到當前外包非核心功能的趨勢。這一趨勢為我國設施管理和企業房地產的創新使用創造了更多機會。根據法國巴黎銀行房地產部預測,2023年英國將成為商業房地產投資金額最大的國家,達到約435億歐元。

- 政府也在努力糾正中小企業之間的生產力差距。例如,英國政府最近撥款5,600萬歐元加強領導和管理技能。這筆資金也是英國商業、能源和工業戰略部(BEIS)和戰略部宣布的《商業生產力評估》的一部分,該評估制定了一項十點行動計劃,以幫助英國企業利用技術來提高生產力並推動市場成長。

- 此外,隨著偏好轉向外包設施管理服務以降低成本,設施管理產業預計將會擴張。透過外包建築營運和維護,公司可以節省大量成本,同時專注於其核心競爭力。根據建築業主和管理者協會(BOMA)的一項調查,私人商業房地產平均每平方英尺的維護和維修花費 2.15 美元。該金額不包括與維護設施相關的費用,例如清潔和維護的人事費用。公司可以透過外包來節省資金,並利用節省的時間來更好地利用員工從事核心業務。

- 此外,各市場供應商正在透過多份合約來擴大業務。例如,2023 年 1 月,索迪斯宣布已贏得一份為期五年的契約,為世界銀行倫敦辦事處提供整合性機構管理(IFM)。作為每年 200 萬英鎊協議的一部分,索迪斯將提供服務以聯繫員工並盡可能地使職場環境具有吸引力。服務包括餐飲、酒店、清潔、技術服務、接待、賓客服務和內部健身房管理。

- 2023 年 9 月,總部位於法蘭克福附近新伊森堡的歐洲重要綜合設施管理公司 Apreona 收購了 JCW Group Limited (JCW)。兩家公司將共同建構一個堅實的綜合設施管理平台。兩家公司互補的企業模式、地理分佈和客戶組合將確保 Apreona 在英國和歐洲的現有和新客戶實現強勁的內部成長。

- 市場競爭加劇將影響現有供應商的利潤率和成長。供應商之間的競爭程度極高,導致該國的FM服務商品化。但隨著經濟情勢逐漸穩定,市場需求預計將逐步改善,市場參與者的利潤空間也將擴大。英國皇家測量師學會英國設施管理市場研究表明,未來幾年利潤率、工作量和就業機會預計將擴大。

- 通貨膨脹上升可能會在多個方面影響英國設施管理市場的成長。如果通貨膨脹導致人事費用、材料和設備等投入成本上升,設施管理公司可能面臨營運費用增加,這可能會對他們的利潤率造成壓力,除非他們能夠透過提高價格將這些成本轉嫁給客戶。根據英國國家統計局的數據,2024 年 3 月英國通膨英國3.2%,低於上個月的 3.4%。 2022年9月至2023年3月期間,英國經歷了七個月的兩位數通膨,並在2022年10月升至11.1%的高峰。

英國設施管理產業趨勢

單一 FM 服務可望佔據主導地位

- 與單一設施管理服務提供者合作時,通常會將任務管理外包給獨立的營業單位。一個組織還可以針對其需要的每項服務使用不同的服務提供者,例如清潔、接待、自動販賣機等。使用專業服務提供者的服務有幾個優點。

- 單一服務提供者提供正確的客戶服務並協助簡化業務,使您能夠專注於核心業務。讓專家管理您的任務將顯著提高效率和服務品質。它也使得公司的員工能夠專注於最重要的業務領域,並節省非核心活動的資源。

- FM外包廣泛應用於公共部門、專業服務、醫療保健、技術、物流、製造、零售和教育等各個領域。 FM 服務覆蓋的領域差異很大,主要取決於其類型、公司規模和其所在的領域。一些組織可能只需要單一服務解決方案提供商,進一步推動該國對單一 FM 的需求。

- 國內建設產業越來越重視永續的建築方法和生命週期管理,這推動了對能夠支援建築整個生命週期(從設計和施工到程序和維護)的設施管理服務的需求。單一設施管理系統提供了一種整體方法來管理建築物的整個生命週期,確保永續性和長壽命。根據英國國家統計局的數據,2023 年,英國建築業的附加價值毛額(GVA) 達到近 1,087 億英鎊,而前一年為 1,244 億英鎊。

- 現代建築配備了日益複雜的系統和技術,包括暖通空調系統、安全系統、能源管理系統和智慧建築技術。單一設施管理系統提供了整合的解決方案,可以有效地管理和最佳化這些系統,最大限度地提高營運效率並節省成本。

- 當選擇單一服務提供者時,公司會將日常業務委託給專業提供者。透過聘請專家,您可以確保卓越的服務品質和效率。使用多個服務提供者是一項耗時的工作,需要管理多個供應商並帶來相關風險。鑑於新興經濟體和已開發經濟體的規模,不可能與單一的供應商或服務商合作。不幸的是,許多企業仍然以單一思維經營,並依賴單一的物業管理服務提供者來滿足其所有需求。

預計商業終端用戶領域將佔據主要市場佔有率

- 隨著企業優先考慮業務效率、租戶滿意度、法規遵循和風險管理以保持競爭優勢並實現房地產投資回報最大化,商業領域對設施管理服務的需求持續成長。商業服務供應商(例如製造商總部、IT和電信業者以及其他服務供應商)使用的辦公大樓主要稱為商業終端用戶部門。因此,提供商業建築裝飾、必要的室內設備、管理等的整體重要性呈指數級成長,從而促進了該地區商業部門市場的發展。

- 商業建築通常具有複雜的基礎設施和系統,需要定期維護,包括暖通空調、電氣、管道和安全系統。設施管理服務可以幫助確保這些系統有效運作,並最大限度地減少停機時間和業務中斷。

- 根據建築業培訓委員會的數據,英國商業建築產出將在 2023 年成長 4%,預計 2024 年也將實現同樣的成長。此外,根據英國國家統計局的數據,到 2025 年,英國住宅和非住宅建築收入預計將達到約 1,389.3 億美元。商業建設的成長可能會導致包括商業房地產在內的新建築增加,從而進一步創造市場需求。

- 商業設施也面臨各種風險,包括安全威脅、設備故障和自然災害。設施管理服務可以透過實施安全措施、進行預防性維護和製定緊急應變計畫來保護居住者和資產,從而幫助降低這些風險。

- 此外,該市場為供應商提供了實施和執行各種基於物聯網的設施管理解決方案的機會,並促進了英國智慧建築市場的發展。其背景是人們對智慧建築的興趣日益濃厚以及物聯網技術的建立。此外,行業供應商商業敏銳度的提升和各行業經濟的多樣化預計將最大限度地增加該地區對設施管理服務的需求。

- 2023 年 1 月,設施管理公司 Fisco UK 與 (MWS) 託管工作場所服務供應商 Apogee Corporation 合作,擴展其整體 IT 服務,並為其基本客群提供更自動化和整合的解決方案組合。透過此次合作,與先前的 MWS 供應商相比,該公司將其客戶的機器運作提高了約 28%。這些重大發展有望推動英國商業領域對 FM 服務的需求。

英國設施管理產業概況

英國設施管理市場較為分散,參與者規模各異,競爭激烈。隨著企業繼續進行策略性投資以抵消目前正在經歷的經濟放緩,預計該市場將出現多起收購、合併和聯盟。

- 2023 年 8 月,勞斯萊斯任命房地產集團 JLL 負責其包括英國在內的整個房地產投資組合的全球設施業務。根據 2024 年 2 月開始的長期協議的一部分,仲量聯行將業務勞斯萊斯的全球戰略設施管理合作夥伴,涵蓋六個國家 44 個地點的 1500 萬平方英尺的製造、倉庫和辦公空間。

- 2023 年 7 月,總部位於波爾圖的 Infraspeak 籌集了 750 萬歐元的 A 輪融資,以在全球擴展其智慧設施管理平台。資金籌措將用於擴大公司團隊和國際擴張。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估宏觀經濟因素對市場的影響

第5章 市場動態

- 市場促進因素

- FM 商品化程度不斷提高

- 新興產業 IFM 和非核心業務外包需求不斷成長

- 最佳化工作場所並重新專注於生產力

- 市場限制

- 公共部門市場飽和

- 競爭加劇影響現有供應商的利潤率

- 英國財務管理勞動力分析與就業趨勢

第6章 市場細分

- 設施管理類型

- 內部設施管理

- 外包設施管理

- 單調頻

- 捆綁 FM

- 整合調頻

- 依產品類型

- 硬體維修

- 建築維運與房地產服務

- 機械、電氣和管道服務

- 其他硬體維修服務

- 軟調頻

- 安全與保全服務

- 辦公室支援服務

- 清潔服務

- 餐飲服務

- 其他軟體 FM 服務

- 硬體維修

- 按最終用戶產業

- 商業

- 設施

- 公共/基礎設施

- 工業

- 其他最終用戶產業

- 按地區

- 倫敦和英格蘭東南部

- 英格蘭西南部

- 英格蘭中西部和東部

- 英格蘭北部

- 其他地區

第7章 競爭格局

- 公司簡介

- CBRE Group Inc.

- Mitie Group PLC

- EMCOR Facilities Services Inc.

- Cushman & Wakefield PLC

- G4S Facilities Management UK Limited

- ISS UK

- Serco Group PLC

- Kier Group PLC

- Sodexo Facilities Management Services

- Compass Group

- Equans

- VINCI Facilities Limited

- Aramark Facilities Services

- Andron Facilities Management

- CSM Facilities Management Group

- 主要供應商市場佔有率分析

第8章投資分析

第9章:未來市場展望

簡介目錄

Product Code: 67228

The United Kingdom Facility Management Industry is expected to grow from USD 70.42 billion in 2025 to USD 76.43 billion by 2030, at a CAGR of 1.65% during the forecast period (2025-2030).

Key Highlights

- In terms of maturity and sophistication, the United Kingdom is one of Europe's most mature and sophisticated markets for facility management services. Given the increasing penetration of facility management services, providers are actively focusing on specialized services to obtain a foothold in the industry, which also saw many changes due to the region's macroeconomic and social changes.

- Various service providers operating in the country have emphasized growing their presence over the last decade to benefit from the increasing demand for facility management, especially with the current trend favoring outsourcing non-core functions. Given the dynamics across the country, the country is witnessing increased opportunities to leverage facility management and corporate real estate in innovative ways. According to BNP Paribas Real Estate, in 2023, the United Kingdom headed the ranking as the country with the most significant value of commercial real estate investments, amounting to about EUR 43.5 billion.

- The government is also focusing on closing the country's productivity gap for small to medium enterprises. For instance, in the recent past, the British government pledged EUR 56 million to enhance leadership and management skills. The funding also forms part of the Business Productivity Review announced by the Department for Business, Energy, and Industrial Strategy (BEIS) and Strategy, which sets out a 10-point action plan to help UK companies harness technology and boost productivity, thereby driving the market growth.

- Also, the facility management industry is expected to expand due to consumers' shifting preferences toward outsourced facility management services to cut costs. Businesses may save significantly by outsourcing building operations and maintenance while concentrating on their core competencies. Research by the Building Owners & Managers Association (BOMA) found that, on average, private commercial properties spend USD 2.15 on maintenance and repairs per square foot. Expenditures associated with maintaining the facility, such as labor costs for cleaning and upkeep, are not included in this amount. Businesses can save expenses and leverage the time saved by outsourcing to better use their workers in their core operations.

- Moreover, various market vendors are expanding their business operations through multiple contracts. For instance, in January 2023, Sodexo announced that it won a five-year contract to offer integrated facilities management (IFM) for a global bank's London offices. As part of the GBP 2 million-a-year contract, Sodexo would deliver services that connect with employees and make their working environment as engaging as possible. The services include catering, hospitality, cleaning, technical services, reception and guest services, and the management of the in-house gym.

- In September 2023, Apleona, a significant European integrated facilities management company based in Neu-Isenburg near Frankfurt (Main), acquired JCW Group Limited (JCW). The two companies will form a robust platform for integrated facilities management. Their complementary enterprise models, regional footprints, and client portfolios will secure strong organic growth with existing and recent Apleona clients in the United Kingdom and Europe.

- The growing competition in the market impacts the profit margins and growth of existing vendors. The competition level between suppliers is so high that FM services are transitioning to commoditized in the country. However, the country's recovering economic stability is anticipated to improve the market demand gradually and, subsequently, the profit margins of the market players. As suggested by the UK Facilities Management Market Survey by RICS, the profit margins, workloads, and employment opportunities are anticipated to grow over the next couple of years.

- Increasing inflation can affect the growth of the United Kingdom facility management market in several ways. If inflation leads to higher costs for inputs such as labor, materials, and equipment, facility management companies may face increased operating expenses, potentially squeezing profit margins unless they can pass these costs onto clients through higher prices. According to the Office for National Statistics (UK), the UK inflation rate was 3.2% in March 2024, compared with 3.4% in the previous month. Between September 2022 and March 2023, the United Kingdom experienced seven months of double-digit inflation, which peaked at 11.1% in October 2022.

United Kingdom (UK) Facility Management Industry Trends

Single FM Service is Expected to Hold Significant Share

- Delegating task management to separate entities is common when working with a single facility management service provider. It also entails a different service provider for each service the organization needs, such as cleaning, reception, and vending machines. Using the services of specialized service providers includes several advantages.

- It allows customers to focus on their core business, while single-service providers provide adequate customer services and help operational efficiency. Experts handling task management will result in much higher efficiency and service quality. It will also free company employees to focus on the most critical business areas while saving resources for non-core activities.

- Outsourced FM is used significantly in various sectors, including the public sector, professional services, healthcare, technology, logistics, manufacturing, retail, and education. The areas that FM services look after vary widely, primarily depending on its type, the company size, and the sector in which it functions. Some organizations may only require a single service solution provider, further driving the demand for single FM in the country.

- Increasing the country's construction sector emphasis on sustainable building practices and lifecycle management has increased the demand for facility management services that can support the whole lifecycle of a building, from design and construction to procedure and maintenance. Single facility management systems provide a holistic approach to managing buildings throughout their lifecycle, ensuring sustainability and longevity. According to the Office for National Statistics (UK), in 2023, the gross value added (GVA) of the construction industry in the United Kingdom amounted to almost GBP 108.7 billion, compared with GBP 124.4 billion in the previous year.

- Modern buildings have increasingly complex systems and technologies, including HVAC systems, security systems, energy management systems, and smart building technologies. Single facility management systems offer integrated solutions to manage and optimize these systems effectively, maximizing operational efficiency and cost savings.

- When businesses choose a single service provider, they outsource their day-to-day operations to a specialist provider. They can be assured of superior service quality and efficiency by hiring specialists. Using several service providers is a time-consuming activity that necessitates the management of multiple vendors and the associated hazards. The scale of the developing and developed economies makes working with a single supplier and servicer impossible. Unfortunately, many businesses still operate with a single mindset, relying on a single property management service provider for all their needs.

The Commercial End-user Segment is Expected to Hold a Significant Market Share

- The commercial segment's demand for facility management services continues to grow as businesses prioritize operational efficiency, occupant satisfaction, regulatory compliance, and risk management to maintain competitive advantage and maximize returns on their real estate investments. Office buildings used by providers of business services, including manufacturers' corporate offices, IT & communication companies, and other service providers, are mainly referred to as the commercial end-user sector. Due to this, the overall supply of commercial building decoration, essential interior fittings, and management has grown drastically in importance, pushing the region's commercial sector market.

- Commercial buildings often have complex infrastructure and systems requiring regular maintenance, including HVAC, electrical, plumbing, and security systems. Facility management services help ensure these systems operate efficiently, minimizing downtime and disruptions to business operations.

- According to the Construction Industry Training Board, in 2023, output for the construction of commercial facilities in the United Kingdom increased by 4%, and it is predicted to be the same in FY 2024. Further, according to the Office for National Statistics (UK), it is projected that the revenue of construction of residential and non-residential buildings in the United Kingdom will amount to around USD 138.93 billion by 2025. Growth in the commercial construction sector leads to an increase in new buildings, including commercial properties, which may further create demand in the market.

- In addition, commercial properties are exposed to various risks, including security threats, equipment failures, and natural disasters. Facility management services help mitigate these risks by implementing security measures, conducting preventive maintenance, and developing emergency response plans to protect occupants and assets.

- Additionally, the market offers several opportunities for vendors to implement and execute various IoT-based facility management and enhance the development of smart buildings within the United Kingdom. This is due to the rising interest in establishing smart buildings and IoT technologies. Also, the surge in the business acumen among industry providers and the diversification of the economy from various industries is anticipated to maximize the demand for facility management services within the region.

- In January 2023, Fisco UK, the facilities management company, partnered with (MWS) managed workplace services provider Apogee Corporation to expand its overall IT offering and deliver a more automated and integrated solutions portfolio to its client base. Through the partnership, the firm has boosted machinery uptime for its clients by around 28% compared to its previous MWS supplier. Hence, these significant developments are poised to drive the demand for FM services in the commercial space in the United Kingdom.

United Kingdom (UK) Facility Management Industry Overview

The UK facility management market is fragmented as it is highly competitive, with several players of different sizes. This market is expected to experience several acquisitions, mergers, and partnerships as enterprises continue to invest in strategically offsetting the present slowdowns they are experiencing.

- August 2023: Rolls-Royce appointed real estate group JLL to run global facilities management operations across the company's real estate portfolio, including the United Kingdom. As part of the long-term contract starting February 2024, JLL would operate as Rolls-Royce's strategic global facilities management partner across 15 million square feet of manufacturing, warehouse, and office area at 44 sites in 6 countries.

- July 2023: Porto-based Infraspeak extended Series A with EUR 7.5 million to fuel the global expansion of its intelligent facility management platform. The funding will be utilized to develop the company's team and fuel its international expansion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Trend Toward Commoditization of FM

- 5.1.2 Growing Demand for IFM and Outsourcing of Non-core Operations from Emerging Verticals

- 5.1.3 Renewed Emphasis on Workplace Optimization and Productivity

- 5.2 Market Restraints

- 5.2.1 Market Saturation in the Public Sector

- 5.2.2 Growing Competition Expected to Impact Profit Margins of Existing Vendors

- 5.3 Workforce Analysis and Employment Trends in the UK FM Industry

6 MARKET SEGMENTATION

- 6.1 By Facility Management Type

- 6.1.1 In-House Facility Management

- 6.1.2 Outsourced Facility Management

- 6.1.2.1 Single FM

- 6.1.2.2 Bundled FM

- 6.1.2.3 Integrated FM

- 6.2 By Offering Type

- 6.2.1 Hard FM

- 6.2.1.1 Building O&M and Property Services

- 6.2.1.2 Mechanical, Electrical, and Plumbing Services

- 6.2.1.3 Other Hard FM Services (includes Energy Services)

- 6.2.2 Soft FM

- 6.2.2.1 Safety and Security Services

- 6.2.2.2 Office Support Services

- 6.2.2.3 Janitorial Services

- 6.2.2.4 Catering Services

- 6.2.2.5 Other Soft FM Services

- 6.2.1 Hard FM

- 6.3 By End-user Industry

- 6.3.1 Commercial

- 6.3.2 Institutional

- 6.3.3 Public/Infrastructure

- 6.3.4 Industrial

- 6.3.5 Other End-user Industries

- 6.4 By Region

- 6.4.1 London and South East England

- 6.4.2 South West England

- 6.4.3 Midlands and East England

- 6.4.4 North of England

- 6.4.5 Rest of the United Kingdom

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 CBRE Group Inc.

- 7.1.2 Mitie Group PLC

- 7.1.3 EMCOR Facilities Services Inc.

- 7.1.4 Cushman & Wakefield PLC

- 7.1.5 G4S Facilities Management UK Limited

- 7.1.6 ISS UK

- 7.1.7 Serco Group PLC

- 7.1.8 Kier Group PLC

- 7.1.9 Sodexo Facilities Management Services

- 7.1.10 Compass Group

- 7.1.11 Equans

- 7.1.12 VINCI Facilities Limited

- 7.1.13 Aramark Facilities Services

- 7.1.14 Andron Facilities Management

- 7.1.15 CSM Facilities Management Group

- 7.2 MARKET SHARE ANALYSIS OF KEY VENDORS

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

02-2729-4219

+886-2-2729-4219

印尼的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年日本的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年義大利設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)設施管理的泰國市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測(2018年~2032年)

印尼的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年日本的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年義大利設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)設施管理的泰國市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測(2018年~2032年) 精神服務市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035)

精神服務市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035) 全球整合性機構管理(IFM) 市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2025 年設施管理服務全球市場報告2018 年至 2032 年全球綜合設施管理市場類型、服務前景、最終用戶、地區、機會和預測評估印度的設施管理市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會及預測,2018~2032年

全球整合性機構管理(IFM) 市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2025 年設施管理服務全球市場報告2018 年至 2032 年全球綜合設施管理市場類型、服務前景、最終用戶、地區、機會和預測評估印度的設施管理市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會及預測,2018~2032年

▼