|

市場調查報告書

商品編碼

1472217

濃縮咖啡市場:依產地、類型、包裝、通路分類:2023-2032 年全球機會分析與產業預測Coffee Concentrates Market By Source, By Type, By Packaging, By Distribution Channel : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

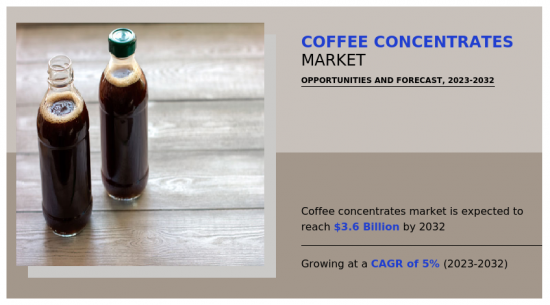

2022年,全球咖啡濃縮物市場價值為22.419億美元,預計到2032年將達到36.322億美元,2023年至2032年的複合年成長率為5.0%。

濃縮咖啡是將粗磨咖啡豆在水中浸泡較長時間(通常12至24小時)而獲得的濃咖啡。這個過程從咖啡豆中提取風味、香氣和咖啡因,形成高度濃縮的液體。過濾濃縮液以除去粉末。它可以用水或牛奶稀釋,製成各種咖啡飲料,包括冰咖啡、冷萃咖啡和熱咖啡。濃縮咖啡可以在冰箱中長期保存,並且可以客製化您想要的濃度和風味,讓您以多種便捷的方式享受咖啡。

消費者健康意識的增強是人們對低酸咖啡興趣日益濃厚的主要動力,從而推動了濃縮咖啡市場的需求。隨著越來越多的消費者開始關注自己的飲食,人們越來越意識到高酸性食品和飲料對消化器官系統健康的潛在負面影響。傳統的咖啡沖泡方法可能會導致最終產品的酸度較高,這對於胃部敏感或胃酸倒流問題的人來說可能會令人不快。因此,許多注重健康的消費者開始轉向低酸咖啡替代品,例如濃縮咖啡,以享受他們最喜歡的飲料,而不會出現與高酸度相關的消化器官系統不適。

濃縮咖啡提供了一種解決方案,它比傳統咖啡具有更順滑、更溫和的味道,酸度更低。溫和的口味吸引了注重健康的消費者,他們希望在享受咖啡因的同時獲得有益消化器官系統的選擇。由於健康問題和飲食偏好的推動,對低酸咖啡的需求持續成長,預計未來幾年濃縮咖啡市場將顯著成長。製造商開始利用這一趨勢,宣傳濃縮咖啡的低酸益處,並擴大產品線,以滿足注重健康的消費者日益成長的需求。

然而,對咖啡豆價格的依賴是濃縮咖啡市場的主要限制因素,因為咖啡豆價格的變化直接影響生產成本。咖啡豆價格受到多種因素的影響,包括天氣、地緣政治事件和供應鏈中斷。隨著咖啡豆價格上漲,製造商面臨生產成本增加,這可能導致濃縮咖啡產品零售價格上漲。此外,產品價格上漲預計將降低對價格敏感的消費者對濃縮咖啡的承受能力,導致市場需求下降,特別是在景氣衰退或金融不穩定時期。

咖啡豆價格的波動為濃縮咖啡產業的長期規劃和預算帶來了挑戰。製造商難以預測和控制生產成本,從而影響報酬率和整體業務永續性。此外,對咖啡豆價格的依賴使得濃縮咖啡市場容易受到產業無法控制的外部因素的影響,企業必須實施策略性風險管理。因此,預計不確定性的增加可能會阻礙濃縮咖啡產業的投資和擴張,限制市場成長潛力,並抑制產品開發的創新。

功能性濃縮咖啡產品的市場開拓響應了注重健康的消費者不斷變化的偏好,並為市場帶來了巨大的機會。功能性咖啡濃縮物富含多種成分,包括維生素、抗氧化劑和適應原,提供咖啡因以外的健康益處。例如,添加膠原蛋白的配方可促進皮膚健康,添加益生菌的配方可支持腸道健康。這些增強功能符合人們對提供能量並有助於整體健康的產品不斷成長的需求,增加了消費者的興趣並擴大了濃縮咖啡市場。

此外,功能性濃縮咖啡產品的推出使濃縮咖啡對傳統咖啡飲用者的吸引力更加多樣化。尋求特定健康益處和功能的消費者被這些創新產品所吸引,從而擴大了濃縮咖啡市場的基礎。此外,功能性成分的配方為產品差異化和優質化創造了機會,使製造商能夠獲得更高的價格分佈並在市場上獲取價值。因此,功能性咖啡濃縮物產品的開拓為企業滿足消費者新興市場需求、推動成長並在全球競爭的咖啡市場中佔有一席之地提供了策略機會。

濃縮咖啡市場分為濃縮咖啡、類型、包裝、分銷管道和地區。依產地分類,可分為阿拉比卡、羅布斯塔等。依類型可分為無咖啡因和無咖啡因。依包裝,市場分為瓶子、袋子等。分銷通路分為超級市場/大賣場、B2B、百貨公司、便利商店、網路銷售管道。依地區分類,北美(美國、加拿大、墨西哥)、歐洲(德國、英國、法國、義大利、西班牙、其他歐洲國家地區)、亞太地區(中國、印度、日本、韓國、澳洲、東協、其他亞洲地區)太平洋地區),分析分為拉丁美洲(巴西、哥倫比亞、阿根廷等拉丁美洲地區)及中東/非洲(海合會、非洲等中東/非洲)。

相關人員的主要利益

- 該報告提供了 2022 年至 2032 年濃縮咖啡市場分析的細分市場、當前趨勢、估計/趨勢分析和動態的定量分析,並確定了濃縮咖啡市場的可行市場機會。

- 我們提供市場研究以及與市場促進因素、市場限制和市場機會相關的資訊。

- 波特的五力分析揭示了買家和供應商的潛力,幫助相關人員做出利潤驅動的業務決策並加強供應商和買家網路。

- 濃縮咖啡市場細分的詳細分析將有助於確定市場機會。

- 每個地區的主要國家都根據其對全球市場的收益貢獻繪製了地圖。

- 市場參與者定位有助於進行基準比較,並提供對市場參與者當前位置的清晰了解。

- 該報告包括對區域和全球濃縮咖啡市場趨勢、主要企業、細分市場、應用領域和市場成長策略的分析。

可使用此報告進行客製化(請聯絡銷售人員以了解額外費用和時間表)

- 消費者購買行為分析

- 產品生命週期

- 監管指引

- 根據客戶興趣加入公司簡介

- 按國家或地區進行的附加分析 – 市場規模和預測

- 公司簡介的擴充列表

- 主要參與者的詳細資料(Excel格式,包括位置、聯絡資訊、供應商/供應商網路等)

- 客戶/消費者/原料供應商名單-價值鏈分析

- 產品消費分析

- SWOT分析

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 主要影響因素

- 關鍵投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 抑制因素

- 機會

第4章濃縮咖啡市場:依產地分類

- 概述

- 阿拉比卡

- 羅布斯塔

- 其他

第5章濃縮咖啡市場:依類型

- 概述

- 不含咖啡因

- 不含咖啡因

第6章濃縮咖啡市場:依包裝分類

- 概述

- 瓶子

- 小袋

- 其他

第7章濃縮咖啡市場:依通路分類

- 概述

- 超級市場-大賣場

- 公司間交易

- 百貨公司

- 便利商店

- 網路銷售管道

第8章濃縮咖啡市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- ASEAN

- 其他亞太地區

- 拉丁美洲

- 巴西

- 哥倫比亞

- 阿根廷

- 其他拉丁美洲

- 中東/非洲

- GCC

- 南非

- 其他中東/非洲

第9章 競爭格局

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 有競爭力的儀表板

- 競爭熱圖

- 2022年主要企業定位

第10章 公司簡介

- Nestle SA

- Starbucks Corporation

- The JM Smucker Company

- All American Coffee LLC

- Califia Farms, LLC

- Javo Beverage Company, Inc.

- Javy Coffee Company

- Grady's Cold Brew

- Kohana Coffee LLC.

- Climpson & Sons

The global coffee concentrates market was valued at $2,241.9 million in 2022, and is projected to reach $3,632.2 million by 2032, registering a CAGR of 5.0% from 2023 to 2032.

Coffee concentrates is a potent form of coffee, obtained by steeping coarsely ground coffee beans in water for an extended period, typically 12 to 24 hours. This process extracts the flavor, aroma, and caffeine from the beans, resulting in a highly concentrated liquid. The concentrates is then strained to remove the grounds, yielding a strong and flavorful brew. It is diluted with water or milk to create various coffee beverages, including iced coffee, cold brew, or even hot coffee. Coffee concentrates offers a convenient and versatile way to have coffee, as it is stored in the refrigerator for an extended period and customized according to personal preference for strength and flavor.

Increase in health consciousness among consumers is a major driving factor behind the rise of interest in low-acid coffee options, which in turn, has boosted the market demand for coffee concentrates. With more consumers becoming conscious of their dietary choices, there is a growing awareness of the potential adverse effects of high-acid foods and beverages on digestive health. Traditional coffee brewing methods sometimes result in a higher acidity level in the final product, which causes discomfort for individuals with sensitive stomachs or acid reflux issues. As a result, many health-conscious consumers have inclined toward low-acid coffee alternatives, such as coffee concentrates, to experience their favorite beverage without the digestive discomfort associated with higher acidity levels.

Coffee concentrates offers a solution by providing a smoother, milder flavor profile with reduced acidity compared to conventionally brewed coffee. The milder flavor appeals to health-conscious consumers, seeking a gentler option for their digestive systems while still indulging in their caffeine fix. As the demand for low-acid coffee options continues to rise, fueled by health concerns and dietary preferences, the coffee concentrates market is anticipated to experience significant growth in coming years. Manufacturers have started investments in this trend by promoting the low-acid benefits of coffee concentrates and expanding their product lines to cater to the increasing demand from health-conscious consumers.

However, dependency on coffee bean prices poses a significant restraint on the coffee concentrates market as fluctuations in the cost of coffee beans directly impact production expenses. Coffee bean prices are subject to various factors, including weather conditions, geopolitical events, and supply chain disruptions. When coffee bean prices rise, manufacturers face increased production costs, potentially leading to higher retail prices for coffee concentrates products. Moreover, surge in price of the product is anticipated to make coffee concentrates less affordable for price-sensitive consumers, resulting in a decline in market demand, especially during economic downturns and periods of financial uncertainty.

The volatility in coffee bean prices creates challenges for long-term planning and budgeting within the coffee concentrates industry. Manufacturers find it difficult to predict and manage production costs, affecting profit margins and overall business sustainability. In addition, dependency on coffee bean prices makes the coffee concentrates market vulnerable to external factors beyond the industry's control, making it essential for businesses to implement strategic risk management practices. Thus, an increase in level of uncertainty is anticipated to discourage investment and expansion initiatives within the coffee concentrates sector, limiting the growth potential of the market and potentially hindering innovation in product development.

The development of functional coffee concentrates products has created significant opportunities in the market, catering to the evolving preferences of health-conscious consumers. Functional coffee concentrates are enriched with various ingredients such as vitamins, antioxidants, and adaptogens, offering additional health benefits beyond caffeine. For instance, formulations with added collagen promote skin health, while those containing probiotics support gut health. These functional enhancements align with the growing demand for products that provide energy and contribute to overall well-being, driving consumer interest and expanding the market for coffee concentrates.

Moreover, the introduction of functional coffee concentrates products has diversified the appeal of coffee concentrates beyond traditional coffee drinkers. Consumers seeking specific health benefits or functional properties are drawn to these innovative offerings, broadening the demographic reach of the coffee concentrates market. In addition, incorporation of functional ingredients creates opportunities for product differentiation and premiumization, allowing manufacturers to command higher price points and capture value in the market. As a result, the development of functional coffee concentrates products represents a strategic opportunity for companies to meet evolving consumer demands, drive growth, and carve out a niche in the competitive coffee market globally.

The coffee concentrates market is segmented into source, type, packaging, distribution channel, and region. By source, the market is classified into Arabica, robusta, and others. Depending on type, it is divided into caffeinated and decaffeinated. On the basis of packaging, the market is fragmented into bottles, pouches, and others. According to distribution channels, it is segregated into supermarkets/hypermarkets, B2B, departmental stores, convenience stores, and online sales channel. Region-wise, the market is analyzed across North America (the U.S., Canada, and Mexico), Europe (Germany, the UK, France, Italy, Spain, and the rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia, ASEAN, and the rest of Asia-Pacific), Latin America (Brazil, Colombia, Argentina, and the rest of Latin America), and Middle East and Africa (GCC, South Africa, and the rest of MEA).

Major players operating in the global coffee concentrates market are Nestle SA, Starbucks Corporation, The J.M. Smucker Company, All American Coffee LLC, Califia Farms, LLC, Javo Beverage Company, Inc., Javy Coffee Company, Grady's Cold Brew, Kohana Coffee, and Climpson & Sons.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the coffee concentrates market analysis from 2022 to 2032 to identify the prevailing coffee concentrates market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the coffee concentrates market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global coffee concentrates market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Consumer Buying Behavior Analysis

- Product Life Cycles

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- List of customers/consumers/raw material suppliers- value chain analysis

- Product Consumption Analysis

- SWOT Analysis

Key Market Segments

By Type

- Caffeinated

- Decaffeinated

By Packaging

- Bottles

- Pouches

- Others

By Source

- Arabica

- Robusta

- Others

By Distribution Channel

- Supermarkets-Hypermarkets

- Business-to-business

- Departmental Stores

- Convenience Stores

- Online Sales Channel

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Asean

- Rest of Asia-Pacific

- Latin America

- Brazil

- Colombia

- Argentina

- Rest of Latin America

- Middle East and Africa

- Gcc

- South Africa

- Rest of Middle East And Africa

Key Market Players:

- Nestle SA

- Starbucks Corporation

- The J.M. Smucker Company

- All American Coffee LLC

- Califia Farms, LLC

- Javo Beverage Company, Inc.

- Javy Coffee Company

- Grady's Cold Brew

- Kohana Coffee LLC.

- Climpson & Sons

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

CHAPTER 4: COFFEE CONCENTRATES MARKET, BY SOURCE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Arabica

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Robusta

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Others

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

CHAPTER 5: COFFEE CONCENTRATES MARKET, BY TYPE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Caffeinated

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Decaffeinated

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: COFFEE CONCENTRATES MARKET, BY PACKAGING

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Bottles

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Pouches

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Others

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL

- 7.1. Overview

- 7.1.1. Market size and forecast

- 7.2. Supermarkets-Hypermarkets

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by region

- 7.2.3. Market share analysis by country

- 7.3. Business-to-business

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by region

- 7.3.3. Market share analysis by country

- 7.4. Departmental Stores

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by region

- 7.4.3. Market share analysis by country

- 7.5. Convenience Stores

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by region

- 7.5.3. Market share analysis by country

- 7.6. Online Sales Channel

- 7.6.1. Key market trends, growth factors and opportunities

- 7.6.2. Market size and forecast, by region

- 7.6.3. Market share analysis by country

CHAPTER 8: COFFEE CONCENTRATES MARKET, BY REGION

- 8.1. Overview

- 8.1.1. Market size and forecast By Region

- 8.2. North America

- 8.2.1. Key market trends, growth factors and opportunities

- 8.2.2. Market size and forecast, by Source

- 8.2.3. Market size and forecast, by Type

- 8.2.4. Market size and forecast, by Packaging

- 8.2.5. Market size and forecast, by Distribution Channel

- 8.2.6. Market size and forecast, by country

- 8.2.6.1. U.S.

- 8.2.6.1.1. Market size and forecast, by Source

- 8.2.6.1.2. Market size and forecast, by Type

- 8.2.6.1.3. Market size and forecast, by Packaging

- 8.2.6.1.4. Market size and forecast, by Distribution Channel

- 8.2.6.2. Canada

- 8.2.6.2.1. Market size and forecast, by Source

- 8.2.6.2.2. Market size and forecast, by Type

- 8.2.6.2.3. Market size and forecast, by Packaging

- 8.2.6.2.4. Market size and forecast, by Distribution Channel

- 8.2.6.3. Mexico

- 8.2.6.3.1. Market size and forecast, by Source

- 8.2.6.3.2. Market size and forecast, by Type

- 8.2.6.3.3. Market size and forecast, by Packaging

- 8.2.6.3.4. Market size and forecast, by Distribution Channel

- 8.3. Europe

- 8.3.1. Key market trends, growth factors and opportunities

- 8.3.2. Market size and forecast, by Source

- 8.3.3. Market size and forecast, by Type

- 8.3.4. Market size and forecast, by Packaging

- 8.3.5. Market size and forecast, by Distribution Channel

- 8.3.6. Market size and forecast, by country

- 8.3.6.1. Germany

- 8.3.6.1.1. Market size and forecast, by Source

- 8.3.6.1.2. Market size and forecast, by Type

- 8.3.6.1.3. Market size and forecast, by Packaging

- 8.3.6.1.4. Market size and forecast, by Distribution Channel

- 8.3.6.2. UK

- 8.3.6.2.1. Market size and forecast, by Source

- 8.3.6.2.2. Market size and forecast, by Type

- 8.3.6.2.3. Market size and forecast, by Packaging

- 8.3.6.2.4. Market size and forecast, by Distribution Channel

- 8.3.6.3. France

- 8.3.6.3.1. Market size and forecast, by Source

- 8.3.6.3.2. Market size and forecast, by Type

- 8.3.6.3.3. Market size and forecast, by Packaging

- 8.3.6.3.4. Market size and forecast, by Distribution Channel

- 8.3.6.4. Italy

- 8.3.6.4.1. Market size and forecast, by Source

- 8.3.6.4.2. Market size and forecast, by Type

- 8.3.6.4.3. Market size and forecast, by Packaging

- 8.3.6.4.4. Market size and forecast, by Distribution Channel

- 8.3.6.5. Spain

- 8.3.6.5.1. Market size and forecast, by Source

- 8.3.6.5.2. Market size and forecast, by Type

- 8.3.6.5.3. Market size and forecast, by Packaging

- 8.3.6.5.4. Market size and forecast, by Distribution Channel

- 8.3.6.6. Rest of Europe

- 8.3.6.6.1. Market size and forecast, by Source

- 8.3.6.6.2. Market size and forecast, by Type

- 8.3.6.6.3. Market size and forecast, by Packaging

- 8.3.6.6.4. Market size and forecast, by Distribution Channel

- 8.4. Asia-Pacific

- 8.4.1. Key market trends, growth factors and opportunities

- 8.4.2. Market size and forecast, by Source

- 8.4.3. Market size and forecast, by Type

- 8.4.4. Market size and forecast, by Packaging

- 8.4.5. Market size and forecast, by Distribution Channel

- 8.4.6. Market size and forecast, by country

- 8.4.6.1. China

- 8.4.6.1.1. Market size and forecast, by Source

- 8.4.6.1.2. Market size and forecast, by Type

- 8.4.6.1.3. Market size and forecast, by Packaging

- 8.4.6.1.4. Market size and forecast, by Distribution Channel

- 8.4.6.2. India

- 8.4.6.2.1. Market size and forecast, by Source

- 8.4.6.2.2. Market size and forecast, by Type

- 8.4.6.2.3. Market size and forecast, by Packaging

- 8.4.6.2.4. Market size and forecast, by Distribution Channel

- 8.4.6.3. Japan

- 8.4.6.3.1. Market size and forecast, by Source

- 8.4.6.3.2. Market size and forecast, by Type

- 8.4.6.3.3. Market size and forecast, by Packaging

- 8.4.6.3.4. Market size and forecast, by Distribution Channel

- 8.4.6.4. South Korea

- 8.4.6.4.1. Market size and forecast, by Source

- 8.4.6.4.2. Market size and forecast, by Type

- 8.4.6.4.3. Market size and forecast, by Packaging

- 8.4.6.4.4. Market size and forecast, by Distribution Channel

- 8.4.6.5. Australia

- 8.4.6.5.1. Market size and forecast, by Source

- 8.4.6.5.2. Market size and forecast, by Type

- 8.4.6.5.3. Market size and forecast, by Packaging

- 8.4.6.5.4. Market size and forecast, by Distribution Channel

- 8.4.6.6. Asean

- 8.4.6.6.1. Market size and forecast, by Source

- 8.4.6.6.2. Market size and forecast, by Type

- 8.4.6.6.3. Market size and forecast, by Packaging

- 8.4.6.6.4. Market size and forecast, by Distribution Channel

- 8.4.6.7. Rest of Asia-Pacific

- 8.4.6.7.1. Market size and forecast, by Source

- 8.4.6.7.2. Market size and forecast, by Type

- 8.4.6.7.3. Market size and forecast, by Packaging

- 8.4.6.7.4. Market size and forecast, by Distribution Channel

- 8.5. Latin America

- 8.5.1. Key market trends, growth factors and opportunities

- 8.5.2. Market size and forecast, by Source

- 8.5.3. Market size and forecast, by Type

- 8.5.4. Market size and forecast, by Packaging

- 8.5.5. Market size and forecast, by Distribution Channel

- 8.5.6. Market size and forecast, by country

- 8.5.6.1. Brazil

- 8.5.6.1.1. Market size and forecast, by Source

- 8.5.6.1.2. Market size and forecast, by Type

- 8.5.6.1.3. Market size and forecast, by Packaging

- 8.5.6.1.4. Market size and forecast, by Distribution Channel

- 8.5.6.2. Colombia

- 8.5.6.2.1. Market size and forecast, by Source

- 8.5.6.2.2. Market size and forecast, by Type

- 8.5.6.2.3. Market size and forecast, by Packaging

- 8.5.6.2.4. Market size and forecast, by Distribution Channel

- 8.5.6.3. Argentina

- 8.5.6.3.1. Market size and forecast, by Source

- 8.5.6.3.2. Market size and forecast, by Type

- 8.5.6.3.3. Market size and forecast, by Packaging

- 8.5.6.3.4. Market size and forecast, by Distribution Channel

- 8.5.6.4. Rest of Latin America

- 8.5.6.4.1. Market size and forecast, by Source

- 8.5.6.4.2. Market size and forecast, by Type

- 8.5.6.4.3. Market size and forecast, by Packaging

- 8.5.6.4.4. Market size and forecast, by Distribution Channel

- 8.6. Middle East and Africa

- 8.6.1. Key market trends, growth factors and opportunities

- 8.6.2. Market size and forecast, by Source

- 8.6.3. Market size and forecast, by Type

- 8.6.4. Market size and forecast, by Packaging

- 8.6.5. Market size and forecast, by Distribution Channel

- 8.6.6. Market size and forecast, by country

- 8.6.6.1. Gcc

- 8.6.6.1.1. Market size and forecast, by Source

- 8.6.6.1.2. Market size and forecast, by Type

- 8.6.6.1.3. Market size and forecast, by Packaging

- 8.6.6.1.4. Market size and forecast, by Distribution Channel

- 8.6.6.2. South Africa

- 8.6.6.2.1. Market size and forecast, by Source

- 8.6.6.2.2. Market size and forecast, by Type

- 8.6.6.2.3. Market size and forecast, by Packaging

- 8.6.6.2.4. Market size and forecast, by Distribution Channel

- 8.6.6.3. Rest of Middle East And Africa

- 8.6.6.3.1. Market size and forecast, by Source

- 8.6.6.3.2. Market size and forecast, by Type

- 8.6.6.3.3. Market size and forecast, by Packaging

- 8.6.6.3.4. Market size and forecast, by Distribution Channel

CHAPTER 9: COMPETITIVE LANDSCAPE

- 9.1. Introduction

- 9.2. Top winning strategies

- 9.3. Product mapping of top 10 player

- 9.4. Competitive dashboard

- 9.5. Competitive heatmap

- 9.6. Top player positioning, 2022

CHAPTER 10: COMPANY PROFILES

- 10.1. Nestle SA

- 10.1.1. Company overview

- 10.1.2. Key executives

- 10.1.3. Company snapshot

- 10.1.4. Operating business segments

- 10.1.5. Product portfolio

- 10.1.6. Business performance

- 10.1.7. Key strategic moves and developments

- 10.2. Starbucks Corporation

- 10.2.1. Company overview

- 10.2.2. Key executives

- 10.2.3. Company snapshot

- 10.2.4. Operating business segments

- 10.2.5. Product portfolio

- 10.2.6. Business performance

- 10.2.7. Key strategic moves and developments

- 10.3. The J.M. Smucker Company

- 10.3.1. Company overview

- 10.3.2. Key executives

- 10.3.3. Company snapshot

- 10.3.4. Operating business segments

- 10.3.5. Product portfolio

- 10.3.6. Business performance

- 10.3.7. Key strategic moves and developments

- 10.4. All American Coffee LLC

- 10.4.1. Company overview

- 10.4.2. Key executives

- 10.4.3. Company snapshot

- 10.4.4. Operating business segments

- 10.4.5. Product portfolio

- 10.4.6. Business performance

- 10.4.7. Key strategic moves and developments

- 10.5. Califia Farms, LLC

- 10.5.1. Company overview

- 10.5.2. Key executives

- 10.5.3. Company snapshot

- 10.5.4. Operating business segments

- 10.5.5. Product portfolio

- 10.5.6. Business performance

- 10.5.7. Key strategic moves and developments

- 10.6. Javo Beverage Company, Inc.

- 10.6.1. Company overview

- 10.6.2. Key executives

- 10.6.3. Company snapshot

- 10.6.4. Operating business segments

- 10.6.5. Product portfolio

- 10.6.6. Business performance

- 10.6.7. Key strategic moves and developments

- 10.7. Javy Coffee Company

- 10.7.1. Company overview

- 10.7.2. Key executives

- 10.7.3. Company snapshot

- 10.7.4. Operating business segments

- 10.7.5. Product portfolio

- 10.7.6. Business performance

- 10.7.7. Key strategic moves and developments

- 10.8. Grady's Cold Brew

- 10.8.1. Company overview

- 10.8.2. Key executives

- 10.8.3. Company snapshot

- 10.8.4. Operating business segments

- 10.8.5. Product portfolio

- 10.8.6. Business performance

- 10.8.7. Key strategic moves and developments

- 10.9. Kohana Coffee LLC.

- 10.9.1. Company overview

- 10.9.2. Key executives

- 10.9.3. Company snapshot

- 10.9.4. Operating business segments

- 10.9.5. Product portfolio

- 10.9.6. Business performance

- 10.9.7. Key strategic moves and developments

- 10.10. Climpson & Sons

- 10.10.1. Company overview

- 10.10.2. Key executives

- 10.10.3. Company snapshot

- 10.10.4. Operating business segments

- 10.10.5. Product portfolio

- 10.10.6. Business performance

- 10.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 02. COFFEE CONCENTRATES MARKET FOR ARABICA, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. COFFEE CONCENTRATES MARKET FOR ROBUSTA, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. COFFEE CONCENTRATES MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. GLOBAL COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 06. COFFEE CONCENTRATES MARKET FOR CAFFEINATED, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. COFFEE CONCENTRATES MARKET FOR DECAFFEINATED, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. GLOBAL COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 09. COFFEE CONCENTRATES MARKET FOR BOTTLES, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. COFFEE CONCENTRATES MARKET FOR POUCHES, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. COFFEE CONCENTRATES MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. GLOBAL COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 13. COFFEE CONCENTRATES MARKET FOR SUPERMARKETS-HYPERMARKETS, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. COFFEE CONCENTRATES MARKET FOR BUSINESS-TO-BUSINESS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. COFFEE CONCENTRATES MARKET FOR DEPARTMENTAL STORES, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. COFFEE CONCENTRATES MARKET FOR CONVENIENCE STORES, BY REGION, 2022-2032 ($MILLION)

- TABLE 17. COFFEE CONCENTRATES MARKET FOR ONLINE SALES CHANNEL, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. COFFEE CONCENTRATES MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 19. NORTH AMERICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 20. NORTH AMERICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 21. NORTH AMERICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 22. NORTH AMERICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 23. NORTH AMERICA COFFEE CONCENTRATES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 24. U.S. COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 25. U.S. COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 26. U.S. COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 27. U.S. COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 28. CANADA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 29. CANADA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 30. CANADA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 31. CANADA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 32. MEXICO COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 33. MEXICO COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 34. MEXICO COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 35. MEXICO COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 36. EUROPE COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 37. EUROPE COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 38. EUROPE COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 39. EUROPE COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 40. EUROPE COFFEE CONCENTRATES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 41. GERMANY COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 42. GERMANY COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 43. GERMANY COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 44. GERMANY COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 45. UK COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 46. UK COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 47. UK COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 48. UK COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 49. FRANCE COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 50. FRANCE COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 51. FRANCE COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 52. FRANCE COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 53. ITALY COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 54. ITALY COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 55. ITALY COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 56. ITALY COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 57. SPAIN COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 58. SPAIN COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 59. SPAIN COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 60. SPAIN COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 61. REST OF EUROPE COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 62. REST OF EUROPE COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 63. REST OF EUROPE COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 64. REST OF EUROPE COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 65. ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 66. ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 67. ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 68. ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 69. ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 70. CHINA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 71. CHINA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 72. CHINA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 73. CHINA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 74. INDIA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 75. INDIA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 76. INDIA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 77. INDIA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 78. JAPAN COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 79. JAPAN COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 80. JAPAN COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 81. JAPAN COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 82. SOUTH KOREA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 83. SOUTH KOREA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 84. SOUTH KOREA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 85. SOUTH KOREA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 86. AUSTRALIA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 87. AUSTRALIA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 88. AUSTRALIA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 89. AUSTRALIA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 90. ASEAN COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 91. ASEAN COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 92. ASEAN COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 93. ASEAN COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 94. REST OF ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 95. REST OF ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 96. REST OF ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 97. REST OF ASIA-PACIFIC COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 98. LATIN AMERICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 99. LATIN AMERICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 100. LATIN AMERICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 101. LATIN AMERICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 102. LATIN AMERICA COFFEE CONCENTRATES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 103. BRAZIL COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 104. BRAZIL COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 105. BRAZIL COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 106. BRAZIL COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 107. COLOMBIA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 108. COLOMBIA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 109. COLOMBIA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 110. COLOMBIA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 111. ARGENTINA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 112. ARGENTINA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 113. ARGENTINA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 114. ARGENTINA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 115. REST OF LATIN AMERICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 116. REST OF LATIN AMERICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 117. REST OF LATIN AMERICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 118. REST OF LATIN AMERICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 119. MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 120. MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 121. MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 122. MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 123. MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 124. GCC COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 125. GCC COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 126. GCC COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 127. GCC COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 128. SOUTH AFRICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 129. SOUTH AFRICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 130. SOUTH AFRICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 131. SOUTH AFRICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 132. REST OF MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY SOURCE, 2022-2032 ($MILLION)

- TABLE 133. REST OF MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 134. REST OF MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022-2032 ($MILLION)

- TABLE 135. REST OF MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022-2032 ($MILLION)

- TABLE 136. NESTLE SA: KEY EXECUTIVES

- TABLE 137. NESTLE SA: COMPANY SNAPSHOT

- TABLE 138. NESTLE SA: PRODUCT SEGMENTS

- TABLE 139. NESTLE SA: SERVICE SEGMENTS

- TABLE 140. NESTLE SA: PRODUCT PORTFOLIO

- TABLE 141. NESTLE SA: KEY STRATERGIES

- TABLE 142. STARBUCKS CORPORATION: KEY EXECUTIVES

- TABLE 143. STARBUCKS CORPORATION: COMPANY SNAPSHOT

- TABLE 144. STARBUCKS CORPORATION: PRODUCT SEGMENTS

- TABLE 145. STARBUCKS CORPORATION: SERVICE SEGMENTS

- TABLE 146. STARBUCKS CORPORATION: PRODUCT PORTFOLIO

- TABLE 147. STARBUCKS CORPORATION: KEY STRATERGIES

- TABLE 148. THE J.M. SMUCKER COMPANY: KEY EXECUTIVES

- TABLE 149. THE J.M. SMUCKER COMPANY: COMPANY SNAPSHOT

- TABLE 150. THE J.M. SMUCKER COMPANY: PRODUCT SEGMENTS

- TABLE 151. THE J.M. SMUCKER COMPANY: SERVICE SEGMENTS

- TABLE 152. THE J.M. SMUCKER COMPANY: PRODUCT PORTFOLIO

- TABLE 153. THE J.M. SMUCKER COMPANY: KEY STRATERGIES

- TABLE 154. ALL AMERICAN COFFEE LLC: KEY EXECUTIVES

- TABLE 155. ALL AMERICAN COFFEE LLC: COMPANY SNAPSHOT

- TABLE 156. ALL AMERICAN COFFEE LLC: PRODUCT SEGMENTS

- TABLE 157. ALL AMERICAN COFFEE LLC: SERVICE SEGMENTS

- TABLE 158. ALL AMERICAN COFFEE LLC: PRODUCT PORTFOLIO

- TABLE 159. ALL AMERICAN COFFEE LLC: KEY STRATERGIES

- TABLE 160. CALIFIA FARMS, LLC: KEY EXECUTIVES

- TABLE 161. CALIFIA FARMS, LLC: COMPANY SNAPSHOT

- TABLE 162. CALIFIA FARMS, LLC: PRODUCT SEGMENTS

- TABLE 163. CALIFIA FARMS, LLC: SERVICE SEGMENTS

- TABLE 164. CALIFIA FARMS, LLC: PRODUCT PORTFOLIO

- TABLE 165. CALIFIA FARMS, LLC: KEY STRATERGIES

- TABLE 166. JAVO BEVERAGE COMPANY, INC.: KEY EXECUTIVES

- TABLE 167. JAVO BEVERAGE COMPANY, INC.: COMPANY SNAPSHOT

- TABLE 168. JAVO BEVERAGE COMPANY, INC.: PRODUCT SEGMENTS

- TABLE 169. JAVO BEVERAGE COMPANY, INC.: SERVICE SEGMENTS

- TABLE 170. JAVO BEVERAGE COMPANY, INC.: PRODUCT PORTFOLIO

- TABLE 171. JAVO BEVERAGE COMPANY, INC.: KEY STRATERGIES

- TABLE 172. JAVY COFFEE COMPANY: KEY EXECUTIVES

- TABLE 173. JAVY COFFEE COMPANY: COMPANY SNAPSHOT

- TABLE 174. JAVY COFFEE COMPANY: PRODUCT SEGMENTS

- TABLE 175. JAVY COFFEE COMPANY: SERVICE SEGMENTS

- TABLE 176. JAVY COFFEE COMPANY: PRODUCT PORTFOLIO

- TABLE 177. JAVY COFFEE COMPANY: KEY STRATERGIES

- TABLE 178. GRADY'S COLD BREW: KEY EXECUTIVES

- TABLE 179. GRADY'S COLD BREW: COMPANY SNAPSHOT

- TABLE 180. GRADY'S COLD BREW: PRODUCT SEGMENTS

- TABLE 181. GRADY'S COLD BREW: SERVICE SEGMENTS

- TABLE 182. GRADY'S COLD BREW: PRODUCT PORTFOLIO

- TABLE 183. GRADY'S COLD BREW: KEY STRATERGIES

- TABLE 184. KOHANA COFFEE LLC.: KEY EXECUTIVES

- TABLE 185. KOHANA COFFEE LLC.: COMPANY SNAPSHOT

- TABLE 186. KOHANA COFFEE LLC.: PRODUCT SEGMENTS

- TABLE 187. KOHANA COFFEE LLC.: SERVICE SEGMENTS

- TABLE 188. KOHANA COFFEE LLC.: PRODUCT PORTFOLIO

- TABLE 189. KOHANA COFFEE LLC.: KEY STRATERGIES

- TABLE 190. CLIMPSON & SONS: KEY EXECUTIVES

- TABLE 191. CLIMPSON & SONS: COMPANY SNAPSHOT

- TABLE 192. CLIMPSON & SONS: PRODUCT SEGMENTS

- TABLE 193. CLIMPSON & SONS: SERVICE SEGMENTS

- TABLE 194. CLIMPSON & SONS: PRODUCT PORTFOLIO

- TABLE 195. CLIMPSON & SONS: KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. COFFEE CONCENTRATES MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF COFFEE CONCENTRATES MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN COFFEE CONCENTRATES MARKET

- FIGURE 04. TOP INVESTMENT POCKETS IN COFFEE CONCENTRATES MARKET (2023-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL COFFEE CONCENTRATES MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. COFFEE CONCENTRATES MARKET, BY SOURCE, 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR ARABICA, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR ROBUSTA, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 15. COFFEE CONCENTRATES MARKET, BY TYPE, 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR CAFFEINATED, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR DECAFFEINATED, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COFFEE CONCENTRATES MARKET, BY PACKAGING, 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR BOTTLES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR POUCHES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COFFEE CONCENTRATES MARKET, BY DISTRIBUTION CHANNEL, 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR SUPERMARKETS-HYPERMARKETS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR BUSINESS-TO-BUSINESS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR DEPARTMENTAL STORES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR CONVENIENCE STORES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF COFFEE CONCENTRATES MARKET FOR ONLINE SALES CHANNEL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 28. COFFEE CONCENTRATES MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 29. U.S. COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 30. CANADA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 31. MEXICO COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 32. GERMANY COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 33. UK COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 34. FRANCE COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 35. ITALY COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 36. SPAIN COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 37. REST OF EUROPE COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 38. CHINA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 39. INDIA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 40. JAPAN COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SOUTH KOREA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 42. AUSTRALIA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 43. ASEAN COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 44. REST OF ASIA-PACIFIC COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 45. BRAZIL COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 46. COLOMBIA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 47. ARGENTINA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 48. REST OF LATIN AMERICA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 49. GCC COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 50. SOUTH AFRICA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 51. REST OF MIDDLE EAST AND AFRICA COFFEE CONCENTRATES MARKET, 2022-2032 ($MILLION)

- FIGURE 52. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 53. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 54. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 55. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 56. COMPETITIVE DASHBOARD

- FIGURE 57. COMPETITIVE HEATMAP: COFFEE CONCENTRATES MARKET

- FIGURE 58. TOP PLAYER POSITIONING, 2022

菊苣咖啡全球市場規模、佔有率和趨勢分析報告(按類型、按分銷管道、按產品、按地區、展望和預測,2024-2031)

菊苣咖啡全球市場規模、佔有率和趨勢分析報告(按類型、按分銷管道、按產品、按地區、展望和預測,2024-2031) 左旋肉鹼咖啡市場報告:2030 年趨勢、預測與競爭分析

左旋肉鹼咖啡市場報告:2030 年趨勢、預測與競爭分析 咖啡的全球市場的評估:各產品類型,各焙煎,各咖啡因等級,各終端用戶,各流通管道,各地區,機會,預測(2017年~2031年)

咖啡的全球市場的評估:各產品類型,各焙煎,各咖啡因等級,各終端用戶,各流通管道,各地區,機會,預測(2017年~2031年) 全球咖啡濃縮物市場規模、佔有率、成長分析、依品種、咖啡因、依產品 - 2024-2031 年產業預測

全球咖啡濃縮物市場規模、佔有率、成長分析、依品種、咖啡因、依產品 - 2024-2031 年產業預測 氮化咖啡市場 - 全球產業規模、佔有率、趨勢、機會和預測,按咖啡口味(香草、卡斯卡拉、水果和堅果等)、包裝(杯子、罐頭)、地區、競爭細分,2019-2029F

氮化咖啡市場 - 全球產業規模、佔有率、趨勢、機會和預測,按咖啡口味(香草、卡斯卡拉、水果和堅果等)、包裝(杯子、罐頭)、地區、競爭細分,2019-2029F 全球起泡咖啡市場規模、佔有率、成長分析,依類型(即飲 (RTD) 和自己動手 (DIY))、配銷通路(線下市場和線上市場)- 2024-2031 年行業預測

全球起泡咖啡市場規模、佔有率、成長分析,依類型(即飲 (RTD) 和自己動手 (DIY))、配銷通路(線下市場和線上市場)- 2024-2031 年行業預測 全球熱飲(咖啡/茶)市場:分析 - 按產品類型、通路、應用程式、區域、預測(至2030年)

全球熱飲(咖啡/茶)市場:分析 - 按產品類型、通路、應用程式、區域、預測(至2030年) 全球生咖啡市場規模、佔有率、成長分析,按類型、應用、分銷管道 - 產業預測,2024-2031 年

全球生咖啡市場規模、佔有率、成長分析,按類型、應用、分銷管道 - 產業預測,2024-2031 年 全球風味咖啡市場 - 2024 年至 2029 年預測

全球風味咖啡市場 - 2024 年至 2029 年預測 全球咖啡濃縮液市場 - 2023-2030

全球咖啡濃縮液市場 - 2023-2030