|

市場調查報告書

商品編碼

1708219

茶葉包裝市場機會、成長動力、產業趨勢分析及2025-2034年預測Tea Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

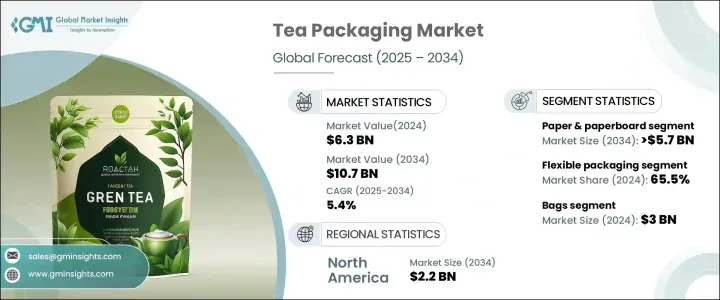

2024 年全球茶葉包裝市場價值為 63 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5.4%。這一成長受到全球茶葉消費量成長、即飲茶飲選擇的快速擴張以及對優質茶產品需求不斷成長的推動。由於茶仍然是全球第二大消費飲料,包裝製造商面臨持續的壓力,需要開發創新和高品質的解決方案,以保持茶的新鮮度和香氣,同時保持成本效益。現代茶葉消費者重視永續性,推動了對由可生物分解和可回收材料製成的包裝的需求。符合這些環保偏好的品牌透過採用環保包裝解決方案獲得了競爭優勢。

此外,有機茶和特色茶的日益普及也加速了對體現產品高品質特性的優質包裝的需求。包含可重新密封、防潮和避光功能的包裝設計正在成為標準功能,確保產品的壽命並提升消費者體驗。隨著全球茶葉消費趨勢指向更健康的生活方式和對特色飲料的興趣增加,對先進和永續包裝解決方案的需求預計將推動市場大幅成長。此外,電子商務的興起也增加了對堅固、美觀、實用的包裝的需求,這種包裝必須能夠承受運輸的嚴酷考驗,同時保持產品的完整性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 63億美元 |

| 預測值 | 107億美元 |

| 複合年成長率 | 5.4% |

茶葉包裝市場依材料分類,包括塑膠、紙和紙板、金屬等。受人們對可生物分解和可回收包裝的日益青睞的推動,預計到 2034 年,紙和紙板行業的產值將達到 57 億美元。由於紙質包裝重量輕、可堆肥、可回收等特點,許多茶葉品牌正在轉向使用紙質包裝。高階品牌和專業品牌也開始採用精心製作的紙板紙盒,以符合其環保的品牌形象並滿足消費者對永續實踐的期望。隨著消費者對環境影響的認知不斷增強,提供可堆肥和可重複使用包裝選擇的品牌正在獲得更高的客戶忠誠度和市場差異化。

軟包裝憑藉其重量輕、成本效益高以及出色的保鮮能力,在 2024 年佔據了 65.5% 的市場佔有率。這種包裝通常由層壓薄膜、小袋和可重複密封的袋子製成,可有效防止水分、氧氣和光線,確保茶葉在較長時間內保持其品質。隨著對便利性和更長保存期限的需求不斷成長,靈活的包裝解決方案變得越來越受歡迎,尤其是對於即飲茶和特殊茶。

預計到 2034 年,北美茶葉包裝市場規模將達到 22 億美元,這得益於優質和有機茶產品日益普及以及對永續包裝解決方案的日益重視。預計到 2034 年,光是美國市場規模就將成長至 19 億美元,這得益於茶葉消費量的增加、向高階有機產品的轉變以及對環保包裝的持續偏好。由於消費者要求保持新鮮度和真實性的特色茶,對有效保持產品品質的包裝解決方案的需求從未如此高漲。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 茶葉消費量上升

- 永續包裝需求不斷成長

- 茶產品的高階化

- 電子商務的擴張

- 即飲茶(RTD)日益流行

- 產業陷阱與挑戰

- 永續性和環境議題

- 原料成本波動

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 塑膠

- 紙和紙板

- 金屬

- 其他

第6章:市場估計與預測:依包裝類型,2021 年至 2034 年

- 主要趨勢

- 軟包裝

- 硬質包裝

第7章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 包包

- 袋裝

- 條狀包裝和小袋裝

- 罐子和容器

- 盒子和紙箱

- 其他

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳新銀行

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Amcor plc

- Berry Global Inc.

- Constantia Flexibles

- Coveris

- Duropack Limited

- Huhtamaki

- Mondi

- Printpack

- ProAmpac

- Sappi

- Sonoco Products Company

- SPG-Pack

- Sprinpak

- Swisspac Packaging

- Transcontinental Inc.

- WestRock Company

- Winpak LTD.

The Global Tea Packaging Market was valued at USD 6.3 billion in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. This growth is fueled by the rising global consumption of tea, the rapid expansion of ready-to-drink options, and the increasing demand for premium tea products. As tea remains the second most widely consumed beverage globally, packaging manufacturers are under constant pressure to develop innovative and high-quality solutions that preserve freshness and aroma while maintaining cost-effectiveness. Modern tea consumers prioritize sustainability, driving the need for packaging made from biodegradable and recyclable materials. Brands that align with these environmental preferences are gaining a competitive edge by adopting eco-friendly packaging solutions.

Additionally, the growing popularity of organic and specialty teas is accelerating the demand for premium packaging that reflects the high-quality nature of the product. Packaging designs that incorporate resealable options, moisture barriers, and light protection are becoming standard features, ensuring product longevity and enhancing the consumer experience. As global tea consumption trends point toward healthier lifestyles and increased interest in specialty beverages, the need for advanced and sustainable packaging solutions is expected to drive substantial market growth. Moreover, the rise of e-commerce has increased the need for sturdy, attractive, and functional packaging capable of withstanding the rigors of shipping while maintaining product integrity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.3 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 5.4% |

The tea packaging market is categorized by materials, including plastic, paper and paperboard, metal, and others. The paper and paperboard segment is expected to generate USD 5.7 billion by 2034, driven by the increasing preference for biodegradable and recyclable packaging. Many tea brands are shifting toward paper-based packaging due to its lightweight, compostable, and recyclable nature. Premium and specialty brands are also embracing crafted paperboard cartons to align with their environmentally friendly brand image and meet consumer expectations for sustainable practices. As consumer awareness around environmental impact grows, brands that offer compostable and reusable packaging options are experiencing higher customer loyalty and market differentiation.

Flexible packaging held a dominant 65.5% market share in 2024 due to its lightweight nature, cost-effectiveness, and superior ability to preserve the freshness of tea. This type of packaging, often made from laminated films, pouches, and resealable bags, provides exceptional protection against moisture, oxygen, and light, ensuring the tea maintains its quality for extended periods. As the demand for convenience and longer shelf life grows, flexible packaging solutions are becoming increasingly popular, especially for ready-to-drink and specialty teas.

The North America Tea Packaging Market is expected to reach USD 2.2 billion by 2034, propelled by the rising popularity of premium and organic tea products and a growing emphasis on sustainable packaging solutions. The U.S. market alone is forecasted to grow to USD 1.9 billion by 2034, driven by increased tea consumption, a shift toward higher-end organic products, and an ongoing preference for eco-conscious packaging. As consumers demand specialty teas that maintain freshness and authenticity, the need for packaging solutions that effectively preserve product quality has never been higher.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising tea consumption

- 3.2.1.2 Growing demand for sustainable packaging

- 3.2.1.3 Premiumization of tea products

- 3.2.1.4 Expansion of e-commerce

- 3.2.1.5 Rising popularity of ready-to-drink (RTD) teas

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sustainability and environmental concerns

- 3.2.2.2 Fluctuating raw material costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2021 – 2034 ($ Mn & Kilo Tons)

- 6.1 Key trends

- 6.2 Flexible packaging

- 6.3 Rigid packaging

Chapter 7 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn & Kilo Tons)

- 7.1 Key trends

- 7.2 Bags

- 7.3 Pouches

- 7.4 Stick pack & sachets

- 7.5 Jars & containers

- 7.6 Boxes & cartons

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Berry Global Inc.

- 9.3 Constantia Flexibles

- 9.4 Coveris

- 9.5 Duropack Limited

- 9.6 Huhtamaki

- 9.7 Mondi

- 9.8 Printpack

- 9.9 ProAmpac

- 9.10 Sappi

- 9.11 Sonoco Products Company

- 9.12 SPG-Pack

- 9.13 Sprinpak

- 9.14 Swisspac Packaging

- 9.15 Transcontinental Inc.

- 9.16 WestRock Company

- 9.17 Winpak LTD.

印度的紅茶市場:各類型,各流通管道,各用途,各地區,機會,預測,2019年~2033年

印度的紅茶市場:各類型,各流通管道,各用途,各地區,機會,預測,2019年~2033年 硬茶市場規模、佔有率及成長分析(酒精濃度、口味、通路及地區)-2025-2032 年產業預測

硬茶市場規模、佔有率及成長分析(酒精濃度、口味、通路及地區)-2025-2032 年產業預測 全球茶葉市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年茶葉市場:依茶葉種類、茶葉形式、通路及地區分類即飲茶市場規模、佔有率和成長分析(按類型、類別、分銷管道、添加劑、包裝、價格和地區)-2025-2032 年產業預測

全球茶葉市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年茶葉市場:依茶葉種類、茶葉形式、通路及地區分類即飲茶市場規模、佔有率和成長分析(按類型、類別、分銷管道、添加劑、包裝、價格和地區)-2025-2032 年產業預測 辣木茶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按形式、按性質、按配銷通路、按地區和競爭,2020-2030F全球茶葉市場預測(2025-2030年)2024 年至 2031 年茶葉市場類型、形式、類別、分銷管道和地區

辣木茶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按形式、按性質、按配銷通路、按地區和競爭,2020-2030F全球茶葉市場預測(2025-2030年)2024 年至 2031 年茶葉市場類型、形式、類別、分銷管道和地區 全球茶葉市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033)速溶茶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F

全球茶葉市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033)速溶茶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F