|

市場調查報告書

商品編碼

1519902

全球二手卡車市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Used Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

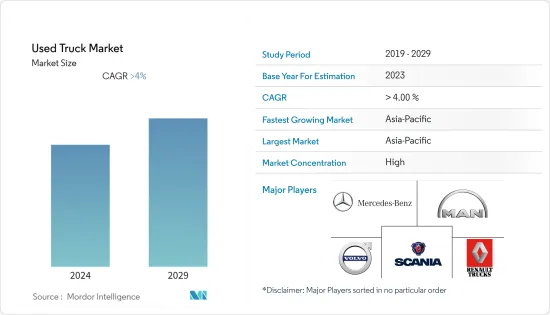

全球二手卡車市場規模預計到2024年將達到476.2億美元,2029年將達到610.9億美元,2024-2029年預測期間複合年成長率將超過5.23%。

近年來,全球二手卡車市場經歷了顯著成長。這種成長是由建築、農業和電子商務活動的增加所推動的。二手卡車的價值提案已成為開拓全球二手卡車市場的關鍵驅動力。

多年來,二手卡車的需求不斷成長,因為與新卡車相比,其成本較低,而且建築和物流行業對貨物的需求不斷增加。然而,卡車製造商提供的獎勵和折扣、新技術、燃油效率(以較低的價格提供)以及新卡車的停機時間更少等因素導致客戶更喜歡新卡車而不是二手卡車。

此外,建築、農業和電子商務活動的增加增加了對物資運輸的需求,導致過去三年全球二手卡車銷售增加。二手卡車的價值提案是促進二手卡車市場成長的主要因素。

因此,二手卡車價格的下降和駕駛品質的提高預計將在預測期內提振各個客戶群的需求。

二手卡車市場趨勢

重卡成主力細分市場

重型卡車在二手卡車市場中佔據主導地位是因為它們在物流、建築和大型運輸等關鍵行業中發揮重要作用。例如,2022 年全球電子商務產業估值為 2,809 美元,而 2021 年為 2,805 美元。預計未來幾年複合年成長率將繼續以10%以上的速度成長。這些車輛對於運輸重型和大量貨物(尤其是遠距運輸)至關重要,並且對於這些部門的有效運作至關重要。它處理多樣化和高要求任務的能力使其成為首選。

與輕型卡車相比,重型卡車以其堅固的結構和較長的使用壽命而聞名。這種耐用性是二手市場的重要因素,因為它可以確保買家即使在二手車型中也能獲得可靠的性能。其製造品質旨在承受嚴格的使用和惡劣的條件,對於依賴重型起重和運輸的企業來說是一項值得的投資。

技術進步和更嚴格的排放法規促進了舊重型卡車流入二手市場,從而推動了舊車型的周轉。較新的車型燃油效率更高且更環保,使舊車型在二手市場上更容易買到且價格更實惠。這些動態確保了重型卡車的穩定供應,並保持其在二手卡車市場的受歡迎程度和主導地位。

亞太地區是二手卡車市場快速成長的地區

亞太地區二手卡車市場的快速成長主要得益於經濟的強勁開拓和重點產業的擴張。該地區經濟體多元化,從新興經濟體到已開發經濟體,對重型運輸的物流、建築和製造業的需求不斷成長。基礎建設的增加,特別是在印度和印尼等國家,進一步加速了這項需求。

這些不斷成長的經濟體對成本效益和效率的日益關注也推動了對二手卡車的需求。發展中國家的預算限制和對可靠運輸解決方案的需求使二手卡車成為平衡成本和性能的有吸引力的選擇。

作為亞太地區最大的市場,中國憑藉其龐大的製造業基礎和全球貿易中心的地位發揮著舉足輕重的作用。國內對在廣闊領土上運輸貨物的巨大需求,加上對道路和基礎設施開拓的大量投資,為二手卡車創造了有利的市場。此外,中國鼓勵用更新的卡車更換舊的、效率較低的卡車的政策創造了一個充滿活力的二手市場,鞏固了其作為該地區最大市場的地位。

近年來,印度對二手車的需求迅速成長。印度市場主要受到電子商務和物流需求不斷成長、全國基礎設施開發和建設計劃不斷增加的推動。例如,2022 年 6 月,道路運輸和公路部在比哈爾邦巴特那和哈吉布爾啟動了 15 個國家高速公路計劃,總價值 1,358.5 億盧比(17 億美元)。由於如此大規模的新車採購需要很高的預算和成本,預計大型商用車的需求將會增加,進而導致二手卡車的需求增加。

因此,由於新興經濟體的影響,亞太市場預計將在未來幾年引領二手卡車產業。

二手卡車產業概述

二手卡車市場的主要參與者是斯堪尼亞、賓士、雷諾、馬斯客和沃爾沃卡車。製造商正致力於推出新產品,透過結合物聯網、人工智慧、智慧導航系統和預防事故技術等先進技術來維持市場競爭力。

- 2022 年 4 月,Ashok Leyland 與 Mahindra First Choice 合作,專用二手商用車業務推出專用混合生態系統。此數位平台有利於舊商用車的更換、妥善處置和購買。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 基礎設施的增加和建設活動的活性化推動了對二手卡車的需求

- 成本效益和可負擔性推動了對二手卡車的需求

- 市場限制因素

- 嚴格的排放法規和安全標準為市場帶來挑戰

- 工業吸引力 - 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔(市場規模:10億美元)

- 車型

- 小卡車

- 中型卡車

- 重型卡車

- 銷售管道

- 獨立經銷商

- 專利權經銷商

- P2P

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 其他地區

- 巴西

- 南非

- 其他國家

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- PACCAR Inc.

- Daimler AG(SelecTrucks)

- Renault SA

- MAN SE(Volkswagen AG)

- Volvo Trucks

- Scania AB(Traton SE)

- Mascus

- Navistar International Corporation

- Enterprise Truck Rental

- Eicher

- Ashok Leyland

- Tata Motors

- AmeriQuest Used Trucks

第7章 市場機會及未來趨勢

- 不斷成長的電子商務和物流行業提供了未來的成長機會

第8章 市場規模及數量預測

第9章 公務車廢氣管理規定

The Used Truck Market size is estimated at USD 47.62 billion in 2024, and is expected to reach USD 61.09 billion by 2029, growing at a CAGR of greater than 5.23% during the forecast period (2024-2029).

The global market for used trucks has witnessed significant growth in recent times. This growth is fueled by increased construction, agriculture, and e-commerce activities, which have spurred the need for material transportation. Their value proposition is a key driver for developing the global used trucks market.

Owing to the low costs compared to the new trucks and rising freight demand across the construction and logistics industries, the demand for used trucks has been significant over the years. However, factors such as the incentives and discounts offered by the truck manufacturers, new technologies, fuel efficiency (available at a low price), and less downtime of new trucks lead to customers preferring new trucks over the used ones.

Moreover, the rise in construction, agriculture, and e-commerce activities has increased the demand for material transportation, resulting in increased sales of used trucks across the world over the past three years. The value proposition of used trucks is the key factor contributing to the growth of the used truck market.

Hence, reduced prices of used trucks and their increased operational quality are expected to boost demand from various customer segments during the forecast period.

Used Truck Market Trends

Heavy-duty Trucks Will be the Leading Segment

The dominance of heavy-duty trucks in the used truck market can be attributed to their integral role in key industries such as logistics, construction, and large-scale transportation. For instance, in 2022, the e-commerce industry worldwide was valued at USD 2809, as compared to USD 2805 in 2021. It is expected to continue to grow with a CAGR of over 10% in the next few years. These vehicles are crucial for moving heavy and large quantities of goods, especially over long distances, which is vital for the efficient functioning of these sectors. Their ability to handle diverse and demanding tasks makes them a preferred choice.

Heavy-duty trucks are known for their robust construction and longer lifespan compared to lighter trucks. This durability is a significant factor in the used market, as it assures buyers of reliable performance even with pre-owned models. Their build quality is designed to withstand rigorous use and harsh conditions, making them a worthwhile investment for businesses that rely on heavy hauling and transportation.

The stream of older heavy-duty trucks into the used market is facilitated by advancements in technology and stricter emission regulations, which prompt the turnover of older models. Newer models are more fuel-efficient and environmentally compliant, making older versions more accessible and affordable in the used market. This dynamic ensures a steady supply of heavy-duty trucks, maintaining their popularity and dominance in the used truck market.

Asia-Pacific is the Fastest Growing Market for Used Trucks

The Asia-Pacific (APAC) region's rapid growth in the used truck market is primarily fueled by the robust economic development and expansion of key industries. This region, characterized by a diverse range of economies from emerging to developed, sees a growing demand in the logistics, construction, and manufacturing sectors, which require heavy-duty transportation. The rise in infrastructure development, particularly in countries like India and Indonesia, further accelerates this demand.

The increasing focus on cost-effectiveness and efficiency in these growing economies also drives the demand for used trucks. Budget constraints and the need for reliable transportation solutions in developing countries make used trucks an attractive option, balancing cost with performance.

China, as the largest market in APAC, plays a pivotal role due to its massive manufacturing base and status as a global trade hub. Its extensive internal demand for transportation of goods across its vast geographical area, coupled with significant investments in road and infrastructure development, makes it a prime market for used trucks. Furthermore, China's policies that encourage the replacement of older, less efficient trucks with newer models have created a vibrant secondary market, reinforcing its position as the largest market in the region.

India has also witnessed a surge in demand for used cars in recent years. The market in India is primarily driven by the growing demand for e-commerce and logistics and the increasing infrastructure and construction projects across the country. For instance, in June 2022, the Ministry of Road Transport and Highways opened 15 national highway projects worth INR 13,585 crores (USD 1.7 billion) in Patna and Hajipur, Bihar. This is expected to drive the demand for heavy-duty commercial vehicles, which will, in turn, lead to an increase in the demand for used trucks, as purchasing new vehicles on such a large scale is budget-straining and a costly affair.

Thus, owing to its developing/emerging economies, the Asia-Pacific market is expected to lead the used truck industry in the years to come.

Used Truck Industry Overview

Key players operating in the used trucks market are Scania, Mercedes-Benz, Renault, Mascus, and Volvo Trucks. Manufacturers focus on launching new products to stay competitive in the market by incorporating advanced technologies, including IoT, AI, smart navigation systems, and accident prevention technologies.

- In April 2022, Ashok Leyland partnered with Mahindra First Choice Wheels to launch an exclusive hybrid ecosystem for its used commercial vehicle business. The digital platform will facilitate exchanging, properly disposing of, and purchasing old commercial vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Infrastructure and Growing Construction Activities are Driving the Demand for Used Trucks

- 4.1.2 Cost Effectiveness and Affordability are Fueling the Demand for Used Trucks

- 4.2 Market Restraints

- 4.2.1 Stringent Emission and Safety Standards Present Challenges for the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD Billion)

- 5.1 Vehicle Type

- 5.1.1 Light Trucks

- 5.1.2 Medium-duty Trucks

- 5.1.3 Heavy-duty Trucks

- 5.2 Sales Channel

- 5.2.1 Independent Dealer

- 5.2.2 Franchised Dealer

- 5.2.3 Peer-to-peer

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 PACCAR Inc.

- 6.2.2 Daimler AG (SelecTrucks)

- 6.2.3 Renault SA

- 6.2.4 MAN SE (Volkswagen AG)

- 6.2.5 Volvo Trucks

- 6.2.6 Scania AB ( Traton SE)

- 6.2.7 Mascus

- 6.2.8 Navistar International Corporation

- 6.2.9 Enterprise Truck Rental

- 6.2.10 Eicher

- 6.2.11 Ashok Leyland

- 6.2.12 Tata Motors

- 6.2.13 AmeriQuest Used Trucks

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing E-commerce and Logistics Sector Presents Growth Opportunities in Coming Years

8 MARKET SIZE AND FORECAST IN VOLUME

9 REGULATORY GOVERNMENT EMISSION NORMS FOR TRUCKS

印度二手車融資:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓二手車:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印度二手車融資:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓二手車:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 二手卡車市場規模、佔有率及成長分析(按車型、最終用戶、通路和地區)-2025-2032 年產業預測

二手卡車市場規模、佔有率及成長分析(按車型、最終用戶、通路和地區)-2025-2032 年產業預測 2025年全球二手卡車市場報告二手半拖車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、推進類型、銷售管道、地區和競爭細分,2020-2030 年預測2025 年全球二手車市場報告2030 年二手車市場預測:按車型、價格分佈、車齡、最終用戶和地區進行全球分析

2025年全球二手卡車市場報告二手半拖車市場 - 全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、推進類型、銷售管道、地區和競爭細分,2020-2030 年預測2025 年全球二手車市場報告2030 年二手車市場預測:按車型、價格分佈、車齡、最終用戶和地區進行全球分析 二手卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車融資市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車市場規模、佔有率、成長分析、按車輛類型、按供應商類型、按燃料類型、按銷售管道、按地區 - 行業預測,2024-2031 年

二手卡車市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車融資市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測二手車市場規模、佔有率、成長分析、按車輛類型、按供應商類型、按燃料類型、按銷售管道、按地區 - 行業預測,2024-2031 年