|

市場調查報告書

商品編碼

1636203

亞太地區廢棄物管理:市場佔有率分析、產業趨勢和成長預測(2025-2030)Asia-Pacific Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

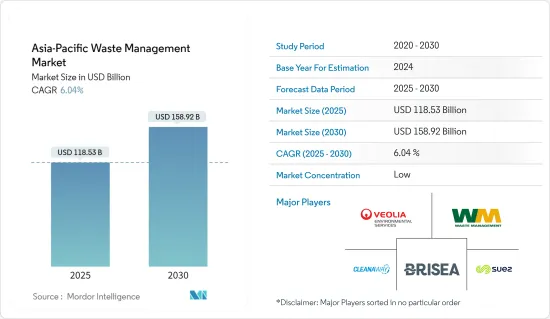

預計2025年亞太地區廢棄物管理市場規模為1,185.3億美元,預估2030年將達1,589.2億美元,預測期間(2025-2030年)複合年成長率為6.04%。

過去 50 年來,各國的廢棄物產生量均有所增加。然而,日本和韓國最近卻出現了下滑。例如,韓國正在進行的生產者延伸責任(EPR)系統要求產品製造商收集和回收其產品中的廢棄物。這些政府措施和法規有助於廢棄物處理公司在該國有效運作。

在廢棄物管理流程中採用物聯網、人工智慧和機器人等最尖端科技正在為產業帶來革命性的變化。 2023 年 9 月,印度梅加拉亞邦推出了人工智慧驅動的廢棄物管理方法。一艘支援人工智慧的機器人船撿起了傾倒在湖中的大量垃圾。與手動方法相比,此過程更有效且耗時更少。

亞太地區對再生材料的需求正在增加。各國正在投資先進的回收技術,將廢棄物加工成可重複使用的材料,為回收商創造新的市場機會。

例如,2024年5月,蔚山大學(UC)和蔚山國際發展合作中心(UIDCC)與聯合國環境規劃署國際環境技術中心合作,在韓國蔚山共同舉辦了為期五天的能力建設計畫。該活動展示了塑膠回收再利用技術的進步,並強調了社區對環保措施的參與。

亞太地區廢棄物管理市場趨勢

塑膠廢棄物推動亞太地區的廢棄物管理

- 亞太地區正遭受大量未經管理的塑膠廢棄物的困擾,全球對更有效的廢棄物管理解決方案的需求不斷成長。這種緊迫性正在推動對先進廢棄物管理技術和基礎設施增強的需求。這鼓勵私人組織和政府增加對尖端廢棄物處理和回收技術的開發和實施的投資。

- 例如,到2024年,中國將在塑膠廢棄物不當方面領先亞太國家,估計數量將達到5,500萬噸。同年,紐西蘭脫穎而出,產生了 8,410 噸處理不當的塑膠廢棄物。

- 2024年6月,澳洲聯邦委員會提出了22項建議,以應對該國水域的塑膠污染。 2022年11月,澳洲加入終結塑膠污染遠大志向聯盟,進一步強調其遏止塑膠污染的承諾。該聯盟旨在透過一項新條約到 2040 年消除全球塑膠污染。

- 這些行動塑造了亞太地區廢棄物管理的格局,並凸顯了對先進回收技術、加強廢棄物收集系統和創新廢棄物減少策略的迫切需求。

中國的廢棄物管理措施推動市場成長和創新

- 中國國家統計局資料顯示,截至2022年,中國約有444個衛生垃圾掩埋場。過去十年,中國廢棄物排放穩定成長,2022年將達到約2.445億噸。

- 此外,到2022年,中國普通工業廢棄物固態廢棄物產生量將達到410億噸。廢棄物排放的激增凸顯了中國對先進廢棄物管理技術和服務的迫切需求,這一趨勢預計將推動亞太地區廢棄物管理市場的成長和創新。

- 2017年,中國發起了全國性的廢棄物分類宣傳活動,以應對這項廢棄物挑戰。到2020年,80多個城市全面實施或測試了廢棄物、可回收物、危險廢棄物和剩菜等分類的城市垃圾分類規定。計劃從 2025 年到 2030 年將這種隔離系統擴展到所有城市。該舉措預計將刺激廢棄物管理領域的成長和創新,並推動整個亞太地區的投資和技術進步。

亞太地區廢棄物管理產業概況

亞太地區廢棄物管理市場由提供廢棄物收集、回收和危險廢棄物處理等服務的本地和全球公司主導。蘇伊士環境公司、威立雅環境服務公司和廢棄物管理公司等行業巨頭處於領先地位,利用其豐富的專業知識和最尖端科技在全部區域提供全面的廢棄物管理解決方案。

同時,澳洲的 Cleanaway Waste Management 和日本的 Daiseki 等區域性公司也佔據了顯著的市場佔有率,提供針對當地需求和法規結構的服務。 BRISEA Group Inc.、Attero 和 Remondis AG &Co.Kg 等著名公司支援先進的回收和廢棄物處理技術。這些公司正在共同重塑這一領域,實施全球最佳實踐,倡導永續性,並滿足亞太地區對有效廢棄物管理解決方案日益成長的需求。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

- 分析方法

- 調查階段

第3章執行摘要

第4章市場洞察

- 目前的市場狀況

- 科技趨勢

- 洞察供應鏈/價值鏈分析

- 產業監管洞察

- 洞察產業技術進步

第5章市場動態

- 市場促進因素

- 快速都市化和人口成長

- 政府法規和舉措

- 市場限制因素

- 文化和行為障礙

- 農村地區缺乏基礎設施

- 市場機會

- 不斷成長的回收市場

- 廢棄物技術

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第6章 市場細分

- 依廢棄物類型

- 工業廢棄物

- 都市固態廢棄物

- 電子廢棄物

- 塑膠廢棄物

- 醫療廢棄物及其他廢棄物(包括建築廢棄物)

- 依廢棄方法分類

- 掩埋

- 焚化

- 回收

- 其他處置方法

- 按國家/地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

第7章 競爭格局

- 市場集中度概覽

- 公司簡介

- Suez Environment SA

- Waste Management Inc.

- Cleanaway Waste Management

- Veolia Environmental Services

- BRISEA Group Inc.

- Attero

- Remondis AG & Co. Kg

- Daiseki Co. Ltd

- Averda

- Clean Harbors Inc.*

- 其他公司

第8章 市場機會及未來趨勢

第9章 附錄

The Asia-Pacific Waste Management Market size is estimated at USD 118.53 billion in 2025, and is expected to reach USD 158.92 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

Over the past 50 years, waste generation has risen across all nations. However, Japan and Korea have recently shown a decline. For example, Korea's ongoing Extended Producer Responsibility (EPR) scheme mandates that product manufacturers collect and recycle the waste from their products. These governmental initiatives and regulations have helped waste management companies to operate effectively within the country.

Adopting cutting-edge technologies such as IoT, AI, and robotics in waste management processes is revolutionizing the industry. In September 2023, the Indian state of Meghalaya introduced an AI-enabled waste management method. The AI-enabled robotic boat collects vast quantities of garbage dumped in a lake. Compared to manual labor, this process is effective and less time-consuming.

The APAC region is seeing an increase in the demand for recycled materials. Countries are investing in advanced recycling technologies to process waste into reusable materials, creating new market opportunities for recycling businesses.

For instance, in May 2024, Ulsan College (UC) and the Ulsan International Development Cooperation Center (UIDCC) hosted a five-day capacity-building program in Ulsan, Republic of Korea, in partnership with the UNEP's International Environmental Technology Center. This event showcased advancements in plastic recycling technologies and emphasized community involvement in environmental initiatives.

Asia-Pacific Waste Management Market Trends

Plastic Waste Driving Waste Management in Asia-Pacific

- The Asia-Pacific region grapples with a staggering volume of mismanaged plastic waste, propelling a global call for more effective waste management solutions. This urgency accentuates the demand for advanced waste management technologies and infrastructure enhancements. Driven by this, private entities and governments increasingly invest in developing and deploying cutting-edge waste processing and recycling technologies.

- For instance, in 2024, China led the Asia-Pacific nations in mismanaged plastic waste, with an estimated 55 million metric tons. New Zealand stood out in the same year, accounting for 8.41 thousand metric tons of mismanaged plastic waste.

- In June 2024, an Australian federal committee made 22 recommendations to combat plastic pollution in the nation's water bodies. In November 2022, Australia's commitment to curbing plastic pollution was further underscored as it joined the High Ambition Coalition to End Plastic Pollution. This coalition aims to eradicate global plastic pollution by 2040 through a new treaty.

- These actions shape the waste management landscape in the Asia-Pacific and emphasize the pressing need for advanced recycling technologies, enhanced waste collection systems, and innovative waste reduction strategies.

China's Waste Management Initiatives Propel Market Growth and Innovation

- Data from the National Bureau of Statistics of China revealed that the nation had around 444 sanitary landfill sites as of 2022. Over the past decade, China has steadily increased its waste output, reaching approximately 244.5 million tons by 2022.

- Furthermore, the volume of regular solid industrial waste produced in China amounted to 41 billion metric tons in 2022. This surge in waste generation underscores the urgent need for advanced waste management technologies and services in China, a trend expected to drive growth and innovation in the APAC waste management market.

- China launched a nationwide waste sorting campaign in 2017 to address this waste challenge. By 2020, over 80 cities had fully implemented or were piloting mandatory sorting of municipal waste into categories such as food waste, recyclables, hazardous waste, and residuals. The plan is to extend this sorting system to all cities between 2025 and 2030. This initiative is expected to spur growth and innovation in the waste management sector, encouraging investments and technological advancements throughout the APAC region.

Asia-Pacific Waste Management Industry Overview

Local and global entities dominate the waste management market in Asia-Pacific, offering services spanning waste collection, recycling, and hazardous waste treatment. Industry behemoths like Suez Environment SA, Veolia Environmental Services, and Waste Management Inc. stand at the forefront, harnessing their vast expertise and cutting-edge technologies to deliver holistic waste management solutions across the region.

Meanwhile, regional players like Australia's Cleanaway Waste Management and Japan's Daiseki Co. Ltd also command notable market shares, tailoring their services to local demands and regulatory frameworks. Noteworthy entities such as BRISEA Group Inc., Attero, and Remondis AG & Co. Kg are championing advanced recycling and waste processing technologies. Collectively, these firms are reshaping the sector, infusing global best practices, championing sustainability, and meeting the surging need for effective waste management solutions in Asia-Pacific.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights into Supply Chain/Value Chain Analysis

- 4.4 Insights into Governement Regualtions in the Industry

- 4.5 Insights into Technological Advancements in the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Urbanization and Population Growth

- 5.1.2 Government Regulations and Initiatives

- 5.2 Market Restraints

- 5.2.1 Cultural and Behavioral Barriers

- 5.2.2 Lack of Infrastructure in Rural Areas

- 5.3 Market Opportunities

- 5.3.1 Growing Recycling Market

- 5.3.2 Waste-to-Energy Technologies

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Waste Type

- 6.1.1 Industrial Waste

- 6.1.2 Municipal Solid Waste

- 6.1.3 E-waste

- 6.1.4 Plastic Waste

- 6.1.5 Biomedical and Other Waste Types (Including Construction Waste)

- 6.2 By Disposal Methods

- 6.2.1 Landfill

- 6.2.2 Incineration

- 6.2.3 Recycling

- 6.2.4 Other Disposal Methods

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Suez Environment SA

- 7.2.2 Waste Management Inc.

- 7.2.3 Cleanaway Waste Management

- 7.2.4 Veolia Environmental Services

- 7.2.5 BRISEA Group Inc.

- 7.2.6 Attero

- 7.2.7 Remondis AG & Co. Kg

- 7.2.8 Daiseki Co. Ltd

- 7.2.9 Averda

- 7.2.10 Clean Harbors Inc.*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

灰渣處理系統市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、按灰渣類型、按最終用途行業、按地區和按競爭細分,2020-2030 年預測)2025年全球水和廢棄物管理諮詢服務市場報告

灰渣處理系統市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、按灰渣類型、按最終用途行業、按地區和按競爭細分,2020-2030 年預測)2025年全球水和廢棄物管理諮詢服務市場報告 全球多氟烷基物質 (PFAS) 廢棄物管理市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年廢棄物管理與收集服務全球市場報告

全球多氟烷基物質 (PFAS) 廢棄物管理市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年2025 年廢棄物管理與收集服務全球市場報告 全球廢棄物管理 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球氣動廢棄物管理系統市場 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美廢棄物管理:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美都市固態廢棄物管理 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)建築廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)越南廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

全球廢棄物管理 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球氣動廢棄物管理系統市場 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美廢棄物管理:市場佔有率分析、產業趨勢和成長預測(2025-2030)北美都市固態廢棄物管理 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)建築廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)越南廢棄物管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)