|

市場調查報告書

商品編碼

1636273

中國電動汽車電池材料:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)China Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

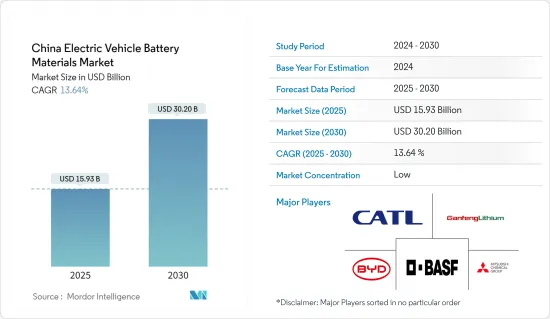

預計2025年中國電動車電池材料市場規模為159.3億美元,預計2030年將達302億美元,預測期間(2025-2030年)複合年成長率為13.64%。

主要亮點

- 從長遠來看,擴大電動車銷售以及政府措施和政策法規等因素預計將成為預測期內中國電動車電池材料市場最重要的促進因素之一。

- 另一方面,由於我們依賴進口原料,我們很容易受到價格波動的影響,預計這將對市場研究產生負面影響。

- 電池技術進步的需求持續成長。預計這一因素將在未來為市場創造一些機會。

中國電動汽車電池材料市場趨勢

鋰離子電池類型主導市場

- 全球鋰離子電動車電池市場是一個充滿活力、機會與挑戰並存的市場。鋰離子二次電池比其他電池技術更受歡迎,這主要是由於其良好的容量重量比。鋰離子二次電池由於具有長壽命、低維護、使用壽命長、價格大幅下降等優異的性能特徵而變得越來越受歡迎。

- 儘管鋰離子電池的價格分佈歷來高於同類產品,但市場領導者已投入並加強研發力度,以實現規模經濟。這種競爭的加劇不僅提高了電池性能,也降低了鋰離子電池的價格。

- 近年來,鋰離子電池和電池組的價格持續下降,對終端用戶產業的吸引力越來越大。電池價格在2022年短暫上漲後,2023年持續下跌。一個關鍵亮點是,鋰離子電池組的成本下降了 14%,降至 139 美元/kWh 的歷史最低水準。

- 在環境問題日益嚴重的情況下,中國政府是電動車的熱情支持者,並正在努力實現雄心勃勃的淨零碳排放目標。對電動車儲存能力至關重要的鋰的需求強勁,全球各大公司都在加緊鋰礦開採。

- 2024年7月,中國東部山東省宣布計畫投資1,000億元人民幣(約138億美元)。這個雄心勃勃的藍圖涵蓋了電極材料、電解液、電池和組裝的產業鏈。山東的策略不僅旨在實現消費電池的多元化和提高質量,還注重加強研發。省政府支持濟南、青島等城市發展原料生產和電池組裝企業,滿足當地新能源汽車生產企業的需求。

- 2024 年 2 月,CATL 推出了革命性的磷酸鋰鐵(LFP) 電池,一次充電的續航里程令人難以置信,超過 1,000 公里(621 英里)。這項創新可望擴大中國對原料的需求。

- 這種發展將導致鋰離子電池的需求激增,從而導致未來幾年對各種原料的需求增加。

擴大電動車銷量

- 在電動車銷售快速成長和國家對永續交通的承諾的推動下,中國電動車(EV)電池材料市場正在快速擴張。作為電動車採用的世界領導者,中國對基本電池材料(鋰、鎳、鈷和錳)的需求正在迅速成長。這些材料對於製造鋰離子電池至關重要,而鋰離子電池是電動車儲能的關鍵技術。

- 中國強勁的電動車銷售已成為電池材料市場的主要催化劑。近年來,由於政府慷慨的獎勵和補貼,以及旨在減少二氧化碳排放和污染防治的強力的政策框架,中國電動車的普及迅速。政府的新能源汽車(NEV)指令要求汽車製造商生產一定比例的電動車,進一步加速了這一勢頭。

- 這種勢頭正在加速。 CATL正在提高產能,以滿足快速成長的電動車電池需求。此外,寧德時代還在研發方面投入巨資,旨在降低成本,同時提高電池性能。

- 值得注意的是,寧德時代於2024年6月與特斯拉建立戰略合作關係,承諾向特斯拉上海超級工廠供應鋰離子電池。此次合作凸顯了中國電池製造商與國際電動車製造商之間日益密切的關係。

- 2023年,中國電動車產業與前一年同期比較成長約22.7%,純電動車銷量約540萬輛,較2019年的83萬輛大幅成長。

- 中國政府繼續透過各種措施支持電動車產業,包括稅收優惠、對製造商和消費者的補貼以及對充電基礎設施的投資。這些措施旨在透過使電動車變得更加實惠和方便來提高採用率,從而增加對電池材料的需求。電池技術的創新也在塑造市場。比亞迪等公司正在開發新型電池化學材料,例如磷酸鋰鐵(LFP)電池,其能量密度比傳統鋰離子電池略低,但更安全、更便宜。這些進步對於讓電動車更容易進入大眾市場至關重要。

- 中國電動車電池材料市場前景十分光明。憑藉政府的持續支持、技術進步和戰略產業夥伴關係關係,中國有望保持在全球電動車市場的領先地位。主要電池製造商產能的持續擴張以及對永續實踐的重視可能會確保基本材料的穩定供應並支持電動車產業的快速成長。

中國電動汽車電池材料產業概況

中國電動車電池材料市場已腰斬。市場的主要企業包括(排名不分先後)寧德時代新能源科技有限公司、比亞迪汽車、贛鋒鋰業、BASF股份公司和三菱化學集團公司。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車銷量成長

- 政府扶持措施及措施

- 抑制因素

- 對原料供應的依賴

- 促進因素

- 供應鏈分析

- PESTLE分析

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子電池

- 鉛酸電池

- 其他

- 材料

- 正極

- 負極

- 電解

- 分隔符

- 其他

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Contemporary Amperex Technology Co., Limited

- BYD Auto Co., Ltd.

- Ganfeng Lithium

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Sumitomo Chemical Co., Ltd.

- BTR New Material Group Co. Ltd.

- Shanshan Co.

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章市場機會與未來趨勢

- 電池技術的進步

簡介目錄

Product Code: 50003560

The China Electric Vehicle Battery Materials Market size is estimated at USD 15.93 billion in 2025, and is expected to reach USD 30.20 billion by 2030, at a CAGR of 13.64% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as growing electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the China Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the country's reliance on imported raw materials makes the industry vulnerable to price fluctuation, which is expected to negatively impact the market studied.

- Nevertheless, there is continued growing demand for advancements in battery technology. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Materials Market Trends

Lithium-ion Battery Type to Dominate the Market

- The global lithium-ion electric vehicle battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion rechargeable batteries are outpacing other battery technologies in popularity, primarily due to their advantageous capacity-to-weight ratio. Their adoption is further fueled by superior performance attributes, such as longevity, low maintenance, an extended shelf life, and a notable decrease in price.

- While lithium-ion batteries traditionally commanded a higher price point than their counterparts, leading market players have been channeling investments into achieving economies of scale and bolstering R&D efforts. This intensified competition has not only enhanced battery performance but also driven down lithium-ion battery prices.

- Recent trends show a consistent decline in the prices of lithium-ion batteries and cell packs, making them increasingly attractive to end-user industries. After a brief uptick in 2022, battery prices continued their downward trajectory in 2023. A significant highlight was the 14% drop in lithium-ion battery pack costs, reaching a record low of USD 139/kWh.

- Amid rising environmental concerns, the Chinese government is fervently championing electric vehicles, aligning its efforts with ambitious net-zero carbon emission targets. Lithium, a crucial component for EV storage capacity, is in high demand, prompting leading global companies to ramp up lithium extraction.

- In July 2024, Shandong province in eastern China unveiled plans for a substantial 100 billion yuan (USD 13.8 billion) investment. The ambitious blueprint encompasses an industrial chain spanning electrode materials, electrolytes, battery cells, and assembly. Shandong's strategy not only aims to diversify and enhance the quality of consumer batteries but also emphasizes bolstering R&D. The provincial government is backing Jinan and Qingdao cities to nurture companies in raw material production and battery assembly, catering to the demands of local new energy vehicle manufacturers.

- In February 2024, CATL introduced a groundbreaking lithium iron phosphate (LFP) battery boasting an impressive driving range of over 1,000 kilometers (621 miles) on a single charge. This innovation is poised to amplify raw material demand in China.

- Given these developments, the demand for lithium-ion batteries is set to surge, subsequently driving up the need for various raw materials in the coming years.

Growing Electric Vehicle Sales

- China's electric vehicle (EV) battery materials market is expanding rapidly, fueled by soaring EV sales and a national commitment to sustainable transportation. As the global leader in EV adoption, China's appetite for essential battery materials-lithium, nickel, cobalt, and manganese-has surged. These materials are pivotal for crafting lithium-ion batteries, the primary technology for EV power storage.

- China's booming EV sales are a primary catalyst for its battery materials market. In recent years, bolstered by generous government incentives, subsidies, and a robust policy framework targeting carbon emission reductions and air pollution combat, China has witnessed a meteoric rise in EV adoption. The government's New Energy Vehicle (NEV) mandate, compelling automakers to produce a specific percentage of EVs, further amplifies this momentum.

- Contemporary Amperex Technology Co. Limited (CATL), a frontrunner in battery manufacturing, is ramping up its production capacity to cater to the surging demand for EV batteries. Additionally, CATL is channeling substantial investments into research and development, aiming to boost battery performance while curtailing costs.

- In a notable move, CATL forged a strategic alliance with Tesla in June 2024, committing to supply lithium-ion batteries for Tesla's Shanghai Gigafactory. This partnership highlights the deepening ties between Chinese battery producers and international EV manufacturers.

- In 2023, China's electric vehicle sector grew by approximately 22.7% year-on-year, with battery EV sales soaring to about 5.4 million, a significant leap from 0.83 million in 2019.

- The Chinese government continues to support the EV sector through various measures, including tax incentives, subsidies for both manufacturers and consumers and investments in charging infrastructure. These policies are designed to make EVs more affordable and convenient, thereby driving higher adoption rates and, consequently, increasing the demand for battery materials. Innovations in battery technology are also shaping the market. Companies like BYD are developing new battery chemistries, such as lithium iron phosphate (LFP) batteries, which are safer and cheaper, although with slightly lower energy density than traditional lithium-ion batteries. These advancements are crucial for making EVs more accessible to the mass market.

- The outlook for the EV battery materials market in China is highly positive. With continued support from the government, technological advancements, and strategic industry partnerships, China is well-positioned to maintain its leadership in the global EV market. The ongoing expansion of production capacities by major battery manufacturers and the emphasis on sustainable practices will likely ensure a steady supply of essential materials, supporting the rapid growth of the EV sector.

China Electric Vehicle Battery Materials Industry Overview

The China Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are Contemporary Amperex Technology Co., Limited, BYD Auto Co., Ltd, Ganfeng Lithium, BASF SE, and Mitsubishi Chemical Group Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted byr Leading Players

- 6.3 Company Profiles

- 6.3.1 Contemporary Amperex Technology Co., Limited

- 6.3.2 BYD Auto Co., Ltd.

- 6.3.3 Ganfeng Lithium

- 6.3.4 BASF SE

- 6.3.5 Mitsubishi Chemical Group Corporation

- 6.3.6 UBE Corporation

- 6.3.7 Umicore SA

- 6.3.8 Sumitomo Chemical Co., Ltd.

- 6.3.9 BTR New Material Group Co. Ltd.

- 6.3.10 Shanshan Co.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

02-2729-4219

+886-2-2729-4219

2025-2033 年電動車電池外殼市場報告(按電池格式類型、材料、車輛類型和地區)

2025-2033 年電動車電池外殼市場報告(按電池格式類型、材料、車輛類型和地區) 中國電動車閥控密封鉛酸電池:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

中國電動車閥控密封鉛酸電池:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 中東及非洲電動車電池材料市場佔有率分析、產業趨勢、統計及成長預測(2025-2030)

中東及非洲電動車電池材料市場佔有率分析、產業趨勢、統計及成長預測(2025-2030) 中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太地區電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區電動汽車電池 -市場佔有率分析、產業趨勢、成長預測(2025-2030) 亞太地區電動汽車電池材料:市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區電動汽車電池材料:市場佔有率分析、產業趨勢、成長預測(2025-2030) 亞太地區電動車 VRLA 電池:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

亞太地區電動車 VRLA 電池:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車 VRLA 電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

北美電動車 VRLA 電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 北美電動車電池材料:市場佔有率分析、行業趨勢和成長預測(2025-2030)

北美電動車電池材料:市場佔有率分析、行業趨勢和成長預測(2025-2030)

▼