|

市場調查報告書

商品編碼

1636454

北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)North America Electric Vehicle Battery Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

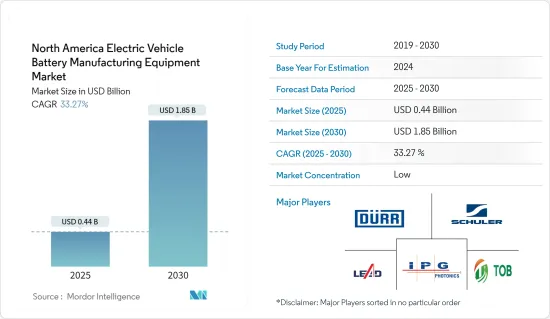

預計2025年北美電動車電池製造設備市場規模為4.4億美元,2030年達18.5億美元,預測期間(2025-2030年)複合年成長率為33.27%。

主要亮點

- 從中期來看,該地區電動車滲透率的提高以及政府的支持措施和法規等因素預計將成為預測期內北美電動車電池製造設備市場的最大推動力之一。

- 另一方面,亞太地區等現有電池市場正在競爭。這對預測期內的北美電動車電池製造設備市場構成威脅。

- 北美國家電池製造供應鏈在地化的持續努力預計將在未來幾年為市場創造一些機會。

- 由於政府加大力度建立電池製造和提高電動車的普及率,預計美國將主導市場並在預測期內實現最高成長。

北美電動車電池製造設備市場趨勢

狹縫和電極製造經歷了巨大的成長

- 狹縫和電極製造領域在北美電動車電池製造設備市場中發揮著至關重要的作用。該細分市場強調精度、效率和適應性的重要性,特別是在電動車需求迅速成長的情況下。該部分包括一系列複雜的工藝,將塗層電極材料轉化為最終結構並將其組裝成電池/電池。這些電池對於電動車電池的性能和可靠性至關重要。

- 在北美,交通運輸變得更加電氣化,分切製程將大卷塗層電極材料切成窄條。這些條帶必須滿足各種電池設計的精確規格。正極通常是鋁,負極是銅,最重要的是高精度地執行此過程,以避免損壞活性鋰化合物和集流體箔等精緻材料。

- 截至2024年1月,國家再生能源實驗室的資料顯示,其在北美的電極和電池製造情況中佔有很大佔有率。美國以 80 家設施和 66 家公司位居榜首,其次是加拿大,擁有 11 家設施和公司,北美其他地區、中東和非洲則擁有 4 家設施和 2 家公司。

- 這證實了北美電動車(EV)電池製造設備市場的活躍成長。設施的數量表明必要的基礎設施已經到位,可以滿足對電動車不斷成長的需求。

- 切割後,電極製造過程開始。在這裡,各個條帶被切割成精確的尺寸並準備組裝。此準備工作包括添加極耳以及施加保護塗層和處理,以增強電極性能和壽命。

- 此外,北美市場對創新和永續性的重視正在推動分切設備和電極製造設備的進步。製造商正在積極尋求減少廢棄物並提高材料可回收性的方法。我們的目標是提高產量比率、減少廢品,並引入系統來回收和再循環電極塗層和製備階段的多餘材料和溶劑。

- 例如,2023 年 9 月,橡樹嶺國家實驗室的工程師推出了突破性的乾電池製造流程。這項創新解決了通常依賴有毒溶劑的傳統濕漿法的挑戰。這種依賴不僅增加了生產成本,也帶來健康和環境風險。 Oakridge的無溶劑製程生產的電池更輕、更耐用,並且在使用後保持高能源儲存能力。

- 鑑於這些進步和對精確度的重視,狹縫電極製造業預計在未來幾年將顯著成長。

美國主導市場

- 在美國,電動車電池製造設備市場受到推動產業成長的多種因素的支持,包括聯邦激勵措施、地方政府措施和私人投資。例如,投資電池製造的公司可以獲得各種稅額扣抵和津貼,降低新進入障礙並幫助現有公司擴張。

- 例如,從2023年開始,美國政府將透過《通膨削減法案》提供稅額扣抵,《兩黨基礎設施法案》則分配高達1兆美元的稅額扣抵以促進能源轉型。根據《減少通貨膨脹法案》,電池生產商可以獲得每千瓦時 35 美元的電池生產信貸和每千瓦時 10 美元的電池模組生產信貸。此外,公司還可以申請電極活性材料成本 10% 的折扣。值得注意的是,企業可以靈活地將這些稅額扣抵轉讓或出售給其他納稅人。

- 此外,電動車供應鏈在地化的動力強勁,導致對國內電池製造設施的投資增加。美國政府更嚴格的排放法規進一步推動了這一趨勢,促使汽車製造商轉向更永續的電池驅動汽車。

- 根據國家再生能源實驗室的數據,截至 2024 年 1 月,美國有 64 家從事電池製造設備領域的公司,65 家工廠分佈在各個地區。這種強大的基礎設施正在支持電動車電池製造設備市場的成長。

- 創新是美國市場的另一個基石,許多公司都在努力提高電池效率、降低成本並使電池生產更具永續性。重點不僅在於鋰離子技術的進步,還在於探索替代化學物質和解決方案,例如固態電池,預計它有望提高能量密度並改善安全性。

- 因此,預計美國在預測期內將出現強勁成長。

北美電動汽車電池製造設備產業概況

北美電動車電池製造設備市場已被削減一半。該市場的主要企業(排名不分先後)包括Durr AG、Schuler AG、IPG Photonics Corporation、無錫利德智慧裝備和廈門TOB新能源科技。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車的擴張

- 政府支持性法規和措施

- 抑制因素

- 與現有市場的競爭

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 過程

- 混合物

- 塗層

- 日曆

- 狹縫/電極加工

- 其他

- 電池

- 鋰離子

- 鉛酸

- 鎳氫電池

- 其他電池

- 地區

- 美國

- 加拿大

- 其他北美地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Duerr AG

- Schuler AG

- Hitachi Ltd.

- Xiamen Tmax Battery Equipments Limited

- ACEY New Energy Technology

- IPG Photonics Corporation

- Wuxi Lead Intelligent Equipment Co Ltd

- ACEY New Energy Technology

- Xiamen Lith Machine Limited

- Xiamen TOB New Energy Technology Co., Ltd.

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 供應鏈本地化

簡介目錄

Product Code: 50003721

The North America Electric Vehicle Battery Manufacturing Equipment Market size is estimated at USD 0.44 billion in 2025, and is expected to reach USD 1.85 billion by 2030, at a CAGR of 33.27% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing adoption of electric vehicles in the region coupled with supportive government policies and regulations are expected to be among the most significant drivers for the North American Electric Vehicle Battery Manufacturing Equipment Market during the forecast period.

- On the other hand, established battery markets such as Asia Pacific are competing. This poses a threat to the North American Electric Vehicle Battery Manufacturing Equipment Market during the forecast period.

- Nevertheless, continued efforts to localize battery manufacturing supply chains in North American countries are expected to create several opportunities for the market in the future.

- United States is expected to dominate the market and will likely register the highest growth during the forecast period due to the government's rising efforts to establish battery manufacturing and the growing adoption of electric vehicles.

North America Electric Vehicle Battery Manufacturing Equipment Market Trends

Slitting and Electrode Making to Witness Significant Growth

- The slitting and electrode-making segment plays a pivotal role in North America's electric vehicle battery manufacturing equipment market. This segment underscores the importance of precision, efficiency, and adaptability, especially given the surging demand for electric vehicles. It involves a series of intricate processes that convert coated electrode materials into final structures, primed for assembly into battery cells. These cells are crucial for the performance and reliability of electric vehicle batteries.

- In North America, where the drive towards transport electrification is gaining momentum, the slitting process cuts large rolls of coated electrode material into narrower strips. These strips must meet precise specifications for various battery designs. Executing this process with high precision is paramount to avoid damaging delicate materials, including active lithium compounds and current collector foils, which are typically aluminum for cathodes and copper for anodes.

- As of January 2024, data from the National Renewable Energy Laboratory reveals a significant presence in North America's electrode and cell manufacturing landscape. The U.S. leads with 80 facilities and 66 companies, followed by Canada with 11 facilities and companies, and the rest of North America with four facilities and two companies.

- This underscores the vigorous growth of the electric vehicle (EV) battery manufacturing equipment market in North America. The multitude of facilities indicates a well-established infrastructure, crucial for meeting the rising demand for electric vehicles.

- After slitting, the electrode-making process commences. Here, individual strips are cut to precise dimensions and readied for assembly. This preparation may involve adding tabs and applying protective coatings or treatments to boost the electrode's performance and longevity.

- Furthermore, the North American market emphasizes innovation and sustainability, propelling advancements in slitting and electrode-making equipment. Manufacturers are actively seeking methods to minimize waste and bolster material recyclability. Innovations aim to enhance yield, reduce scrap, and implement systems for recovering and recycling excess materials or solvents from the electrode coating and preparation stages.

- For example, in September 2023, engineers at Oak Ridge National Laboratory introduced a groundbreaking dry battery manufacturing process. This innovation tackles the challenges of the traditional wet slurry method, which often depends on toxic solvents. Such reliance not only escalates manufacturing costs but also poses health and environmental risks. Oak Ridge's solvent-free process yields a battery that's lighter, more durable, and maintains a high energy storage capacity even after use.

- Given these advancements and the emphasis on precision, the slitting and electrode-making segment is poised for significant growth in the coming years.

United States to Dominate the Market

- In the United States, the electric vehicle battery manufacturing equipment market is supported by a confluence of factors, including federal incentives, local government policies, and private investments that collectively enhance the industry's growth. For example, various tax credits and grants are available to companies that invest in battery manufacturing, which lowers the entry barrier for new players and supports the expansion of existing companies.

- For instance, starting in 2023, the United States government is offering Tax Credits via the Inflation Reduction Act, and Bipartisan Infrastructure Law laws have allocated a staggering USD 1 trillion in tax credits to facilitate the energy transition. Under the Inflation Reduction Act, battery producers benefit from manufacturing credits, receiving USD 35 per kilowatt-hour for battery cell production and USD 10 per kilowatt-hour for battery modules. Additionally, companies can claim a 10% reimbursement on costs for electrode-active materials. Notably, businesses have the flexibility to transfer or sell these tax credits to other taxpayers.

- Additionally, there is a strong push towards localizing the electric vehicle supply chain, which has led to increased investments in battery manufacturing facilities across the country. This trend is further bolstered by the United States government's stringent emissions regulations, which encourage automotive manufacturers to shift towards more sustainable, battery-powered vehicles.

- According to the National Renewable Energy Laboratory, as of January 2024, the United States boasted 64 companies operating in the battery manufacturing equipment sector, with 65 facilities spread across various regions. This robust infrastructure drives the growth of the Electric Vehicle Battery Manufacturing Equipment Market.

- Technological innovation is another cornerstone of the United States market, with numerous companies engaged in pioneering work to improve battery efficiency, reduce costs, and enhance the sustainability of battery production. The focus is not only on advancing lithium-ion technology but also on exploring alternative chemistries and solutions, such as solid-state batteries, which promise higher energy densities and improved safety profiles.

- Therefore, the United States is expected to witness significant growth during the forecast period, as mentioned above.

North America Electric Vehicle Battery Manufacturing Equipment Industry Overview

The North America Electric Vehicle Battery Manufacturing Equipment Market is semi-fragmented. Some of the key players in this market (in no particular order) are Duerr AG, Schuler AG, IPG Photonics Corporation, Wuxi Lead Intelligent Equipment Co. Ltd., and Xiamen TOB New Energy Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Regulations and Policies

- 4.5.2 Restraints

- 4.5.2.1 Competition From Established Markets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Process

- 5.1.1 Mixing

- 5.1.2 Coating

- 5.1.3 Calendaring

- 5.1.4 Slitting and Electrode Making

- 5.1.5 Other Process

- 5.2 Battery

- 5.2.1 Lithium-ion

- 5.2.2 Lead-Acid

- 5.2.3 Nickel Metal Hydride Battery

- 5.2.4 Other Batteries

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Duerr AG

- 6.3.2 Schuler AG

- 6.3.3 Hitachi Ltd.

- 6.3.4 Xiamen Tmax Battery Equipments Limited

- 6.3.5 ACEY New Energy Technology

- 6.3.6 IPG Photonics Corporation

- 6.3.7 Wuxi Lead Intelligent Equipment Co Ltd

- 6.3.8 ACEY New Energy Technology

- 6.3.9 Xiamen Lith Machine Limited

- 6.3.10 Xiamen TOB New Energy Technology Co., Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Localization of Supply Chains

02-2729-4219

+886-2-2729-4219

全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO)

全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO) 電池製造中的泵浦和閥門 2023-2027

電池製造中的泵浦和閥門 2023-2027 中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030) 中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030) 亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

▼