|

市場調查報告書

商品編碼

1636472

北美電動車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)North America Electric Vehicle Battery Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

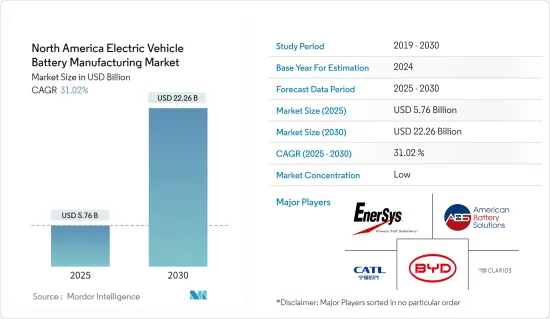

北美電動車電池製造市場規模預計到2025年為57.6億美元,預計到2030年將達到222.6億美元,預測期內(2025-2030年)複合年成長率為31.02%。

主要亮點

- 未來幾年,在政府支持和政策的推動下,北美電動車電池製造市場預計將主要受到電動車日益普及的推動。

- 然而,來自亞太地區成熟電池市場的競爭對北美電動車電池製造市場構成了挑戰。

- 然而,隨著北美國家推動電池製造供應鏈的在地化,大量的市場成長機會正在出現。

- 隨著美國政府加大力度提高電池製造水平以及電動車普及率的飆升,預計美國將引領市場並實現最顯著的成長。

北美電動車電池製造市場趨勢

電動汽車電池顯著成長

- 在技術進步、監管加強和消費者偏好不斷變化的推動下,北美電動車電池市場正在經歷強勁而快速的成長,尤其是在純電動車 (BEV) 領域。僅依靠電池供電的電動動力傳動系統運行的純電動車在世界向永續交通的轉變中發揮著至關重要的作用。

- 在北美,隨著汽車製造商和政策制定者承諾雄心勃勃地減少溫室氣體排放,純電動車產業將會成長。遏制碳排放和遵守嚴格排放標準的努力正在推動純電動車的生產和擴散。與混合動力汽車不同,純電動車的特點是沒有廢氣排放。

- 根據國際能源總署(IEA)的報告,自 2021 年以來,電動車銷量激增,成長了一倍多,達到 727,730 輛。這一勢頭仍在持續,2022 年售出 1,117,719 套,2023 年躍升至 1,584,113 套。這種銷售熱潮與這些車輛的主要動力來源鋰離子電池的需求激增密切相關。

- 北美不斷成長的電池製造能力對於純電動車領域的成功至關重要。鑑於依賴進口電池零件和原料的地緣政治和物流障礙,建立強大的國內供應鏈變得越來越重要。為此,北美市場的投資不斷增加,多家公司在全部區域建立了「超級工廠」。

- 例如,本田汽車工業計劃投資110億美元加強在加拿大安大略省的電動車和電池產能,並計劃於2028年開始營運。這項雄心勃勃的計劃是本田迄今為止在加拿大最大的投資,目標是每年生產 24 萬輛電動車和 36 吉瓦時電池。

- 這些戰略定位的設施通常位於汽車製造地附近,對於實現規模經濟、控制生產成本以及讓純電動車更廣泛地為消費者所用至關重要。由於靠近汽車生產基地,供應鏈流暢,可以實現準時生產。

- 考慮到這些動態,電池電動車領域預計在未來幾年將顯著成長。

美國主導市場

- 美國是北美電動車電池製造市場的關鍵參與者,其特點是創新活躍、政策支援和策略投資。由於國家迫切需要向更永續的交通生態系統過渡,電動車電池市場正在迅速擴大。政府對消費者和製造商的重大獎勵正在支持這項轉變。

- 電動車購買稅額扣抵和大量研發資金等聯邦政策旨在鼓勵創新並增加電動車的採用。此外,《降低通貨膨脹法》等最近的立法包括鼓勵國內生產電動車電池的重要條款,為公司在該國建立製造設施提供財政獎勵。

- 例如,根據美國環保基金會的數據,2023年即將建成的電池生產設施的總產能總合131GWh。據預測,到2025年,這一數字可能迅速上升至738GWh,年增率超過154%。此次擴張將顯著影響電動車電池製造市場,使其能夠滿足電動車日益成長的需求。

- 創新是美國電動車電池製造市場的核心。美國公司和研究機構處於開發下一代電池技術的最前沿,其中包括固態電池,這些技術有望在能量密度、安全性和生命週期方面取得顯著改善。

- 例如,2023年3月,美國能源局阿貢國家實驗室成為鋰空氣電池先驅。這項技術創新預計將顯著延長電動車的續航里程。該電池的潛在用途包括為汽車和家用飛機動力來源,以及為遠距卡車營運提供動力。值得注意的是,這種設計解決了傳統電池中普遍存在的重大安全問題,因為它消除了與液體電解相關的過熱和火災風險。

- 支持美國電動車電池製造市場擴張的是充電基礎設施網路的擴張。美國正在大力投資開發全面的充電站網路,包括主要交通走廊沿線和都市區的快速充電選項。此外,無線充電和超快速充電等充電技術的創新也在考慮之中,以進一步改善用戶體驗並支援道路上不斷增加的電動車數量。

- 因此,如上所述,美國預計將在預測期內成為市場的主導地區。

北美電動車電池製造業概況

北美電動車電池製造市場已減少一半。市場的主要企業(排名不分先後)是比亞迪、寧德時代新能源科技有限公司、American Battery Solutions, Inc.、EnerSys 和 Clarios。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 電動車的擴張

- 政府支持性法規政策

- 抑制因素

- 與現有市場的競爭

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 透過電池

- 鋰離子

- 鉛酸電池

- 鎳氫電池

- 其他

- 依電池形狀分類

- 方形

- 袋型

- 圓柱形

- 搭車

- 客車

- 商用車

- 其他

- 透過促銷

- 電池電動車

- 油電混合車

- 插電式混合動力電動車

- 按地區

- 美國

- 加拿大

- 其他北美地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BYD Co. Ltd

- Contemporary Amperex Technology Co. Limited

- American Battery Solutions, Inc.

- EnerSys

- GS Yuasa Corporation

- LG Chem Ltd

- Exide Industries

- Panasonic Corporation

- Sionic Energy

- Clarios LLC

- 其他主要企業名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 供應鏈本地化

簡介目錄

Product Code: 50003739

The North America Electric Vehicle Battery Manufacturing Market size is estimated at USD 5.76 billion in 2025, and is expected to reach USD 22.26 billion by 2030, at a CAGR of 31.02% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the North American electric vehicle battery manufacturing market is poised to be significantly driven by the region's increasing adoption of electric vehicles, bolstered by supportive government policies and regulations.

- However, competition looms from established battery markets in the Asia Pacific, presenting a challenge to North America's electric vehicle battery manufacturing landscape.

- Yet, as North American countries push for localized battery manufacturing supply chains, they unveil a plethora of opportunities for the market's growth.

- With the United States government's intensified efforts to bolster battery manufacturing and the surging adoption of electric vehicles, the United States is set to lead the market and is projected to witness the most substantial growth.

North America Electric Vehicle Battery Manufacturing Market Trends

Battery Electric Vehicle to Witness Significant Growth

- Driven by technological advancements, regulatory backing, and evolving consumer preferences, the North American market for electric vehicle batteries is witnessing a robust surge, particularly in the battery electric vehicles (BEV) segment. BEVs, which operate exclusively on battery-powered electric powertrains, play a pivotal role in the global shift towards sustainable transportation.

- In North America, as automakers and policymakers commit to ambitious greenhouse gas emission reductions, the BEV segment is set for growth. The push to curb carbon footprints and adhere to strict emission standards is propelling the production and uptake of BEVs, which stand out by having no tailpipe emissions, unlike their hybrid counterparts.

- Electric vehicle sales, as reported by the International Energy Agency, have seen a meteoric rise since 2021, more than doubling to 727,730 units. The momentum continued with 1,117,719 units sold in 2022, and a leap to 1,584,113 units in 2023. This sales boom is closely linked to the surging demand for lithium-ion batteries, the mainstay power source for these vehicles.

- North America's burgeoning battery manufacturing capacity is crucial for the BEV segment's success. Given the geopolitical and logistical hurdles of depending on imported battery components and raw materials, the establishment of strong domestic supply chains takes on heightened significance. In response, the North American market is witnessing a flurry of investments, with several companies setting up 'gigafactories' across the region.

- As a case in point, Honda Motor is channeling a hefty USD 11 billion into bolstering its electric vehicle and battery production footprint in Ontario, Canada, with plans to commence operations by 2028. This ambitious endeavor, Honda's largest Canadian investment to date, aims for an annual output of 240,000 electric vehicles and 36 gigawatt-hours of batteries.

- These strategically located facilities, often near automotive manufacturing centers, are pivotal for achieving economies of scale, curbing production costs, and broadening the accessibility of BEVs to consumers. Their proximity to automotive hubs ensures a fluid supply chain and supports just-in-time production.

- Given these dynamics, the battery-electric vehicle segment is on track for substantial growth in the coming years.

United States to Dominate the Market

- The United States is a pivotal player in the North American electric vehicle battery manufacturing market, characterized by dynamic technological innovation, policy support, and strategic investments. The market for electric vehicle batteries is rapidly expanding, driven by a national imperative to transition to a more sustainable transportation ecosystem. Substantial government incentives aimed at both consumers and manufacturers support this shift.

- Federal policies, such as tax credits for electric vehicle purchases and substantial funding for research and development, are designed to spur innovation and increase the adoption of electric vehicles. Furthermore, recent legislation, such as the Inflation Reduction Act, includes significant provisions to promote the domestic production of electric vehicle batteries, providing financial incentives for companies to establish manufacturing facilities within the country.

- For instance, according to the United States Environmental Defense Fund, in 2023, the combined announced capacity of upcoming battery production facilities totaled about 131 GWh. Projections indicate this figure will surge, potentially hitting 738 GWh by 2025, translating to an annual growth rate exceeding 154%. This expansion significantly impacts the Electric Vehicle Battery Manufacturing Market, enabling it to meet the increasing demand for electric vehicles.

- Technological innovation is at the core of the United States electric vehicle battery manufacturing market. American companies and research institutions are at the forefront of developing next-generation battery technologies, including solid-state batteries, which promise significant improvements in energy density, safety, and lifecycle.

- For instance, in March 2023, the Argonne National Laboratory, under the United States Department of Energy, pioneered a lithium-air battery. This innovation holds the promise of substantially extending the range of electric vehicles. The battery's potential applications are vast, from powering cars and domestic airplanes to facilitating long-haul truck operations. Notably, this design addresses a critical safety concern prevalent in traditional batteries, as it eliminates the risk of overheating and fire associated with liquid electrolytes.

- A growing network of charging infrastructure supports the expansion of the electric vehicle battery manufacturing market in the United States. Significant investments are being made to develop a comprehensive network of charging stations across the country, including fast-charging options along major transportation corridors and in urban areas. Additionally, innovations in charging technology, such as wireless and ultra-fast charging, are being explored to improve the user experience further and support the growing number of electric vehicles on the road.

- Therefore, as mentioned above, the United States is expected to be the dominant region in the market during the forecast period.

North America Electric Vehicle Battery Manufacturing Industry Overview

The North America Electric Vehicle Battery Manufacturing Market is semi-fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd, Contemporary Amperex Technology Co. Limited, American Battery Solutions, Inc., EnerSys, and Clarios.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Supportive Government Regulations and Policies

- 4.5.2 Restraints

- 4.5.2.1 Competition From Established Markets

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Nickel Metal Hydride Battery

- 5.1.4 Others

- 5.2 Battery Form

- 5.2.1 Prismatic

- 5.2.2 Pouch

- 5.2.3 Cylindrical

- 5.3 Vehicle

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Others

- 5.4 Propulsion

- 5.4.1 Battery Electric Vehicle

- 5.4.2 Hybrid Electric Vehicle

- 5.4.3 Plug-in Hybrid Electric Vehicle

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 American Battery Solutions, Inc.

- 6.3.4 EnerSys

- 6.3.5 GS Yuasa Corporation

- 6.3.6 LG Chem Ltd

- 6.3.7 Exide Industries

- 6.3.8 Panasonic Corporation

- 6.3.9 Sionic Energy

- 6.3.10 Clarios LLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Localization of Supply Chains

02-2729-4219

+886-2-2729-4219

全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO)

全球電池製造機械市場(至 2029 年):按電極層壓機、壓延機、分切機、攪拌機、塗佈和乾燥機、組裝機、成型和測試機以及鋰離子電池(NMC、LFP、NCA、LCO、LMO、LTO) 電池製造中的泵浦和閥門 2023-2027

電池製造中的泵浦和閥門 2023-2027 中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池製造:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電池製造設備:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲電動車電池製造設備:市場佔有率分析、產業趨勢和成長預測(2025-2030) 中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲電動車電池製造:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池製造設備:市場佔有率分析、產業趨勢與成長預測(2025-2030) 亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池製造:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美電動車電池製造設備:市場佔有率分析、產業趨勢、成長預測(2025-2030)

▼